My Stock Portfolio Review, May 2025

Portfolio Performance Overview and Key Stock Highlights

Hello, Investor,

Each month, I provide a transparent update on my portfolio performance, covering the latest news on core stock positions and analyzing recent developments across each holding.

For more frequent updates, follow me on X/Twitter and Threads, for visual infographics on Instagram and on SavvyTrader for portfolio changes.

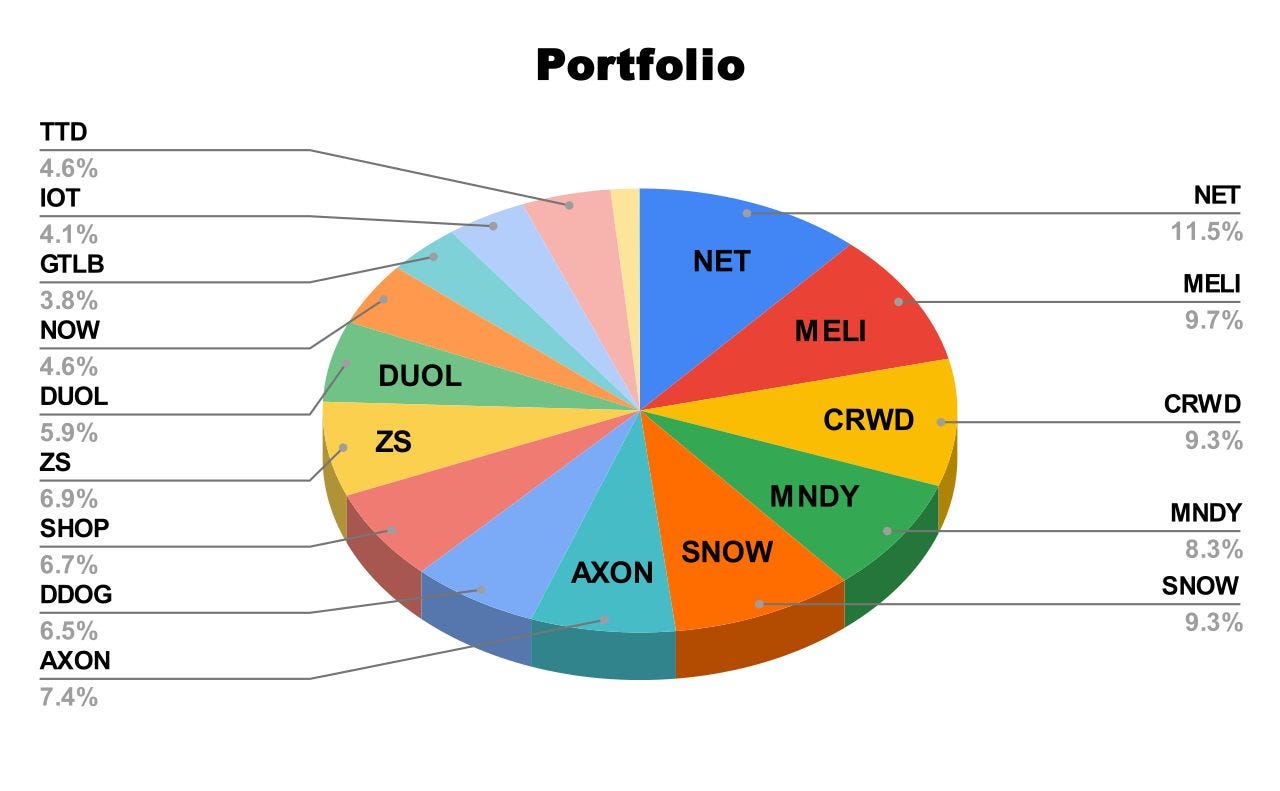

Portfolio Review

Holdings:

Monthly Allocations:

* green (added), orange (trimmed)

Performance (TWR):

Historical performance (TWR):

2020: +110.2% (since 15.04.2020)

2021: +23.7%

2022: -59.6%

2023: +57.3%

2024: +24.9%

Cumulative: +140.1%

A recap of my Portfolio in 2025

January:

⬇️ Trim TSLA

⬆️Add DDOG TTD SHOP MNDY GTLB

February:

❌ TSLA

⬇️ Trim NOW NET

⬆️Add AXON

✅New DUOL

April:

⬇️ Trim CRWD AXON

⬆️Add ZS TTD IOT DUOL

Commentary on my holdings:

Cloudflare NET

The company reported its first quarter of 2025 results.

Thoughts on Cloudflare Earnings Report $NET:

🟢 Positive

Revenue grew to $479.1M, up +26.5% YoY, beating estimates by 2.2%

Operating margin expanded to 11.7%, up +0.5pp YoY

Free cash flow margin improved to 11.0%, up +1.6pp YoY

Net new ARR reached $77M, up +19.1% YoY

Billings grew to $515M, up +32.8% YoY

RPO increased to $1.86B, up +38.8% YoY

13,105 net new customers added, reaching 250,819 total, up +27.2% YoY

$130M 5-year contract closed via Workers.ai, the largest in company history

$1M+ customers up +48% YoY, $5M+ customers up +54% YoY

APAC revenue rose +54% YoY, strongest regional performance

Diluted shares down -2.9% YoY, reducing dilution

Q2 revenue guidance of $500–501M (+24.8% YoY) beat estimates

Zero Trust and SASE deals secured across U.S., EMEA, and APAC

🟡 Neutral

Gross margin at 77.1%, above long-term target but down -2.4pp YoY

EPS of $0.16, in line with estimates

Dollar-based net retention (DBNR) remained flat at 111% QoQ

$100K+ customer cohort added only +30, modest sequential growth

SBC as % of revenue rose to 22%, up +0.7pp QoQ

R&D spend increased to 16% of revenue, up +0.5pp YoY

R&D index (RDI) slightly decreased to 1.63, down -0.03 YoY

Headcount increased to 4,400, up +18.8% YoY

Net margin at -8.0%, though improved +1.3pp YoY

🔴 Negative

Gross margin decline of -240bps YoY, impacted by mix and cost allocation

Pool of Funds contracts created visibility challenges for revenue recognition

Sales & marketing expense remains high at 38.3% of revenue, despite -3.1pp YoY reduction

Basic shares increased +2.1% YoY, slightly dilutive

FX loss of $0.01/share impacted net income

Market Reaction to Earnings Release: The stock price up +8.4% following the earnings release.

Cloudflare is powering AI integrations for companies like Asana, Atlassian, PayPal, Stripe, and Block by enabling Claude, Anthropic’s AI assistant, to securely connect with business tools via MCP servers.

Built on Cloudflare Workers, these connections allow users to complete tasks through conversation instead of switching apps. Companies can now deploy MCP servers in days, with built-in security, authentication, and global performance.

Cloudflare also launched its own MCP servers, letting developers use Claude to build apps, analyze logs, and manage infrastructure directly through chat.

Crowdstrike CRWD

CrowdStrike is extending its business model into a high-potential but underserved segment: small and medium-sized businesses. With just 11% of SMBs currently using AI-driven security, the company sees a clear expansion path by delivering enterprise-grade protection in a simplified, affordable package through Falcon Go.

SMB-focused products offer a new revenue stream with high scalability and low customer acquisition friction, especially as cyberattacks become more frequent and complex. With cybersecurity spend growing among mid-market buyers and AI adoption just beginning, Falcon Go could evolve into a durable long-tail growth driver.

CrowdStrike named Brad Burns as Chief Communications Officer to lead global strategy. He brings 20+ years of experience from Snowflake, Salesforce, and AT&T. Burns will support CrowdStrike’s growth as an AI-driven cybersecurity platform and expand its policy influence. CEO George Kurtz highlighted the need to communicate Falcon’s role against AI-powered threats.

CrowdStrike announced integration into the NVIDIA Enterprise AI Factory validated design, enabling enterprises to secure full-stack AI infrastructure—from data ingestion to deployment. The Falcon platform will now protect systems, models, and workflows built on NVIDIA Blackwell.

CrowdStrike provides real-time, AI-powered protection against threats like data poisoning, model tampering, and sensitive data exposure. The Falcon platform uses a continuous feedback loop, processing trillions of daily events, to deliver machine-speed detection and response.

CrowdStrike has been named Leader and Outperformer in the 2025 GigaOm Radar Report for Identity Threat Detection and Response. It is the only vendor to receive perfect 5 out of 5 scores across all Emerging Feature categories, including AI-Enhanced SecOps and Non-Human Identity Security. The report highlights CrowdStrike as the most mature and complete platform, tying for the highest overall score across Key Features and Business Criteria.

The Falcon platform secures both human and non-human identities across hybrid environments, addressing threats from initial compromise to lateral movement. With 79 percent of initial access attacks now malware-free and the growth of machine identities through agentic AI, identity security has become critical. Falcon uses real-time endpoint signals, expert threat intelligence, and trillions of daily events to drive AI-native protection.

GigaOm highlights Falcon’s capabilities in Proactive Protection, Automated Response, and Cross-Domain Detection, supported by over 1,500 automated actions through Falcon Fusion SOAR. Charlotte AI delivers 98 percent accuracy in triaging detections, accelerating incident response. CrowdStrike’s adversary-centric model provides enhanced visibility into attack paths and enables rapid response before escalation.

CrowdStrike has been recognized as a Customers’ Choice in the 2025 Gartner Peer Insights Voice of the Customer for Endpoint Protection Platforms. It received the most 5-star ratings, totaling 450, and holds a 97 percent Willingness to Recommend based on 601 responses as of January 2025. It is the only vendor recognized in every edition of the report since 2019.

Customers highlight the Falcon platform’s AI-native architecture, multi-OS support, seamless integration, and reliable support. Falcon unifies endpoint, identity, cloud, and SIEM into a single platform, offering cross-domain threat correlation and automated response.

Innovations like CrowdStrike Signal and Charlotte AI enable real-time threat detection and autonomous response. The platform’s architecture supports security consolidation, improves operational efficiency, and enhances SOC performance through AI-driven workflows and automated orchestration.

Monday MNDY

The company reported its first quarter of 2025 results.

Thoughts on MondayCom Earnings Report $MNDY:

🟢 Positive

Revenue grew to $282.3M, up +30.2% YoY, beating estimates by 2.5%

EPS was $1.10, up +59.4% vs estimates

Operating margin improved to 14.5%, up +4.5pp YoY

Net margin rose to 9.7%, up +6.4pp YoY

Free cash flow hit $109.5M, with cash reserves increasing to $1.53B

Work Management adoption expanded, driven by AI-powered enterprise features

CRM accounts reached 31,467, up +13.4% QoQ

Dev accounts grew to 4,266, up +24.3% QoQ

Service accounts rose to 694, up +83.6% QoQ

$100K+ customers grew +45.8% YoY to 1,328

S&M expense ratio fell to 48.1%, down -7.6pp YoY

R&D investment increased, with RDI at 1.91, up +0.04 YoY

AI usage scaled to 26M+ actions, up +150% QoQ

FY25 revenue guidance raised to $1.220B–$1.226B (+25.8% YoY) - monday Service impact modestly included in guidance despite strong growth potential and AI revenue not yet monetized or included in FY25 outlook

🟡 Neutral

NDR stable at 112%, but full-year expected slightly below

NDR for $100K+ accounts improved to 117%, up from 116% LQ

Net new ARR flat YoY at $57M

CAC payback lengthened to 30.1 months, up +4.3 months YoY

R&D expense ratio increased to 19.1%, up +3.0pp YoY

G&A expense ratio rose to 8.5%, up +0.4pp YoY

SBC/revenue decreased slightly to 11%, down -0.5pp QoQ

Diluted shares up +2.0% YoY, with slower QoQ growth

Headcount reached 2,695, up +35.6% YoY

Europe stabilized but remains behind North America

🔴 Negative

Q2 revenue guidance of $292M–$294M implies +24.1% YoY, missing estimates by -0.4%

FCF margin declined to 38.8%, down -2.6pp YoY

Enterprise sales cycles lengthening; expansion decisions face higher scrutiny

Market Reaction to Earnings Release: The stock price up +5.6% following the earnings release.

Datadog DDOG

The company reported its first quarter of 2025 results.

Thoughts on Datadog Earnings Report $DDOG:

🟢 Positive

Revenue rose to $761.6M, up +24.6% YoY, beating estimates by 2.9%.

EPS (non-GAAP) was $0.57, beating by +35.7%.

Free Cash Flow Margin reached 32.1%, up +1.5pp YoY.

RPO climbed to $2.31B, up +33.5% YoY.

Signed 11 $10M+ TCV deals, up from 1 YoY.

New logo dollar value rose +70% YoY, signaling stronger enterprise land motion.

AI-native cohort now contributes 8.5% of ARR, up from 6% QoQ and 3.5% YoY.

Flex Logs hit $50M ARR in 6 quarters—fastest product ramp in company history.

Database Monitoring reached $50M ARR, growing +60% YoY.

Platform adoption deepened: 51% of customers use 4+ products, 13% use 8+.

Security suite now used by 7,500+ customers, including 50%+ of Fortune 500.

🟡 Neutral

Operating margin fell to 21.9%, down -5.0pp YoY, due to rising infrastructure costs.

Gross margin declined to 80.3%, down -2.9pp YoY.

Net margin came in at 3.2%, down -3.7pp YoY.

DBNR remained flat at 119% QoQ.

S&M/revenue held steady at 23.4% YoY.

R&D Index (RDI) slightly down to 0.86, from 0.91 YoY.

CAC payback period extended to 27.2 months, up +5.2 YoY.

Revenue guidance for FY25 raised by $40M, now $3.215B–$3.235B (+20–21% YoY).

Customer count increased by only +500 QoQ, now 30,500 (+8.9% YoY).

🔴 Negative

Gross margin pressure from spiky cloud workloads and early-stage product scaling.

Operating leverage reduced by increased investments and acquisition-related costs.

AI-native concentration risk: largest customer now from AI cohort, introducing volatility potential.

FY25 operating margin guide lowered to 19–20% due to FX (+$15M), M&A (+$10M), and infra costs.

Market Reaction to Earnings Release: The stock price up +2.6% following the earnings release.

Datadog acquired Eppo, a feature flagging and experimentation platform now integrated into its Product Analytics suite. This extends Datadog's capabilities beyond observability into real-time product experimentation and AI model evaluation—building a full-stack analytics solution optimized for AI-native development.

The move creates a new monetization channel. By bundling observability, experimentation, and feature management into a single platform, Datadog strengthens its position across engineering, product, and data science teams. AI workloads demand safe, iterative deployment. Feature testing and A/B frameworks are no longer optional.

Datadog has introduced the first two outputs from Datadog AI Research: Toto and BOOM.

Toto is the first open-source foundation model for observability, trained solely on Datadog’s internal telemetry data. It achieves state-of-the-art performance in time series forecasting and enables zero-shot anomaly detection and capacity planning without manual tuning.

BOOM is the largest public observability time series benchmark, containing 350 million observations across 2807 multivariate series. It addresses challenges like sparsity, cold starts, and spikes, supporting research advancement in forecasting models.

Axon AXON

The company reported its first quarter of 2025 results.

Thoughts on Axon Earnings Report $AXON:

🟢 Positive

Revenue grew to $604M, up +31% YoY, beating estimates by +6.5%

Software & Services revenue rose +38.7% YoY to $263M, with 74.2% gross margin

Connected Devices revenue increased +26.1% YoY to $340.9M, with 50.1% gross margin

ARR reached $1.1B, up +33.8% YoY

Total future contracted revenue increased to $9.90B, up +40.7% YoY

Gross margin (non-GAAP) rose to 63.6%, up +0.4pp YoY

Net new ARR hit $103M, up +10.8% YoY

SG&A improved to 25.2% of revenue, down -2.9pp YoY

Draft One reached ~30K users in under 12 months

TASER 10 adoption pacing 2x faster than TASER 7

Axon Assistant and fixed ALPR cameras generated strong early agency demand

International bookings hit a Q1 record, with broad regional growth

NRR stable at 123%

EPS (non-GAAP) was $1.41, beating estimates by +0.7%

🟡 Neutral

Operating expenses: R&D rose to 15.7% of revenue (+0.8pp YoY)

CAC payback extended to 25.6 months from 21.1 in Q4

FY25 revenue guidance of $2.55–$2.65B (+24.7% YoY) was in line with estimates

FedRAMP approval for FUSUS is pending final certification

🔴 Negative

Operating margin fell to -1.5%, down -5.0pp YoY

Net margin declined to 14.6%, down -14.3pp YoY

SBC/revenue rose to 23%, up +0.5pp QoQ

Basic shares up +2.0% YoY; diluted shares up +5.6% YoY

Tariffs expected to reduce FY EBITDA margin by 50bps

Drone hardware remains supply-constrained

Federal bookings remain limited by budget delays

Market Reaction to Earnings Release: The stock price up +5.7% following the earnings release.

Snowflake SNOW

The company reported its first quarter of 2025 results.

Thoughts on Snowflake Earnings Report $SNOW:

🟢 Positive

Revenue: Q1 product revenue grew +26.2% YoY to $997M, beating estimates by 3.9%

RPO: Reached $6.70B, up +34.3% YoY

Billings: Increased +36.1% YoY to $770M

Operating Margin: Expanded to 8.8%, up +4.4 PPs YoY

EPS: Non-GAAP EPS of $0.24, beating estimates by 14.3%

Customer Growth: Added +451 net new customers, now totaling 11,578 (+17.9% YoY)

$1M+ Customers: Reached 606, up +25.2% YoY

Data Sharing: Grew to 39.0%, up +3.0 PPs QoQ

Free Cash Flow Guidance: Maintained at 25% for FY

FY26 Revenue Guidance Raised: Now $4.325B (+24.9% YoY)

Buybacks: Repurchased 3.2M shares for $491M; $1.5B authorization remains

AI Monetization: Cortex usage strong (5,200+ weekly users), but no direct revenue attribution

🟡 Neutral

Net Revenue Retention: At 124%, down -4 PPs YoY, but still healthy

Total Listings: Marketplace listings at 3,098, up +20.7% YoY but only +54 QoQ

Total Headcount: Increased +12.9% YoY to 8,240, supporting GTM expansion

CapEx: Temporarily elevated due to office expansion, not expected to recur

Payback Period: CAC payback rose to 25.4 months, up +3.7 YoY

R&D Index: Dropped to 1.13, down -0.63 YoY

🔴 Negative

Gross Margin: Product gross margin declined to 75.7%, down -1.3 PPs YoY

FCF Margin: Fell to 17.6%, down -22.4 PPs YoY

Net Margin: Declined to -41.3%, down -3.0 PPs YoY

SBC/Revenue: Still high at 39%, despite -6.3 PPs QoQ improvement

Competitive Pressure: Rising from Microsoft Fabric, especially in mid-market and public sector

Market Reaction to Earnings Release: The stock price up +7.3% following the earnings release.

Snowflake is expanding in automotive with its AI Data Cloud for Manufacturing. Since April 2023, it saw a 416% increase in Data Apps, 185% growth in analytics use, and 188% rise in data science deployments.

The platform supports key industry trends like connected vehicles, autonomy, and Industry 4.0, enabling OEMs and suppliers to collaborate across design, production, and after-sales.

It’s already used by 80% of major OEMs including CarMax, Nissan, and Subaru of New England to boost agility, streamline operations, and enhance customer experience.

Snowflake appointed Bill Scannell to its Board of Directors, effective May 7, 2025. Scannell serves as President of Global Sales and Customer Operations at Dell Technologies, where he has led global growth across 180 countries for nearly 40 years. His expertise in go-to-market strategy and customer engagement will support Snowflake’s AI and data platform expansion.

Shopify SHOP

The company reported its first quarter of 2025 results.

Thoughts on Shopify Earnings Report $SHOP:

🟢 Positive

Revenue grew +26.8% YoY to $2.36B, beating estimates by 1.2%

Free cash flow margin reached 15.4% (+2.9pp YoY), maintaining profitability

Operating margin expanded to 13.9% (+3.1pp YoY)

GPV rose +32.0% YoY to $47.84B, reaching 64% of GMV

Merchant Solutions revenue increased +28.9% YoY to $1.74B

Shop Pay GMV hit $22B (+57% YoY), with growing enterprise adoption

Shop App native GMV surged +94% YoY, up from +84% in Q4

B2B GMV posted triple-digit YoY growth

International GMV grew +31% YoY, with Europe up +36%

Q2 revenue guidance of $2.54B–$2.57B implies +24.9% YoY, 1.9% above consensus

🟡 Neutral

Subscription Solutions revenue up +21.3% YoY to $620M, with stable 80.2% gross margin

MRR grew +20.5% YoY, with 34% from Plus plans

Operating expenses as % of revenue declined: S&M to 16.6%, R&D to 12.4%, G&A to 3.6%

SBC/revenue increased to 5% (+1pp QoQ), but dilution remained minimal

Product innovation and AI use expanding, but impact on cost structure not yet material

Dilution slightly increased: basic shares up 0.6% YoY, +0.1pp QoQ

Merchant Solutions gross margin fell to 38.6% from 40.1% YoY, but up QoQ

🔴 Negative

Gross margin declined to 49.5% (-2.2pp YoY) due to mix shift to lower-margin services

Net margin was -28.9% (-14.2pp YoY) despite strong top-line growth

EPS missed estimates at $0.25 (-3.8%)

Market Reaction to Earnings Release: The stock price up +10.8% following the earnings release.

Zscaler ZS

Zscaler has appointed Raj Judge to its Board of Directors and named him Executive Vice President of Corporate Strategy and Ventures.

Judge brings over 25 years of experience in tech law and venture capital, most recently as Senior Partner and Co-Chair of Emerging Companies and Venture Capital at Wilson Sonsini. He will lead strategic initiatives, identify growth opportunities, and work across internal and external teams to scale Zscaler’s platform.

Zscaler has been named a Leader for the fourth consecutive year in the 2025 Gartner Magic Quadrant for Security Service Edge, positioned highest on the Ability to Execute axis. The recognition reflects Zscaler's continued strength in delivering a cloud-native SSE platform that supports secure, identity- and policy-driven access to internet, SaaS, and private applications.

SSE growth is driven by VPN replacement, Zero Trust adoption, SaaS expansion, and GenAI-related security needs. Gartner projects SaaS to grow over 15 percent annually through 2028.

With over 15 years of security innovation, Zscaler extends Zero Trust Everywhere across users, branches, workloads, and IoT/OT devices, aiming to simplify IT operations while securing enterprise environments at scale.

The company reported its first quarter of 2025 results.

Thoughts on Zscaler Earnings Report $ZS:

🟢 Positive

Revenue grew to $678M, up +22.6% YoY, beating estimates by 1.8%

EPS (non-GAAP) of $0.84, beat estimates by 10.5%

Billings rose to $785M, up +24.9% YoY

RPO reached $4.98B, up +30.2% YoY

ARR hit $2.9B, with consistent +23% YoY growth, tracking toward $3B+ in Q4

ZDX bookings up +70% YoY to $75M

SecOps ACV up +120% YoY driven by Risk360 and UVM adoption

Fortune 500 tech customer expanded ARR +40% to $19M

Fortune 50 auto customer expanded ARR +50%+ to over $10M

New logo ACV up +40% YoY

Z-Flex added over $65M in TCV

APAC revenue up +28.2% YoY

🟡 Neutral

Dollar-Based Net Retention Rate at 114%, down 1 point QoQ due to larger bundled deals

Gross Margin (non-GAAP) at 80.3%, down -1.1 pts YoY

Operating Margin (non-GAAP) at 21.6%, down -0.4 pts YoY

Customer count over $1M ARR grew to 643 (+23 YoY)

Customer count over $100K ARR reached 3,363 (+72 QoQ)

S&M expense improved to 37.0% of revenue, down 2.2 pts YoY

R&D investment rose to 15.6% of revenue, up 1.4 pts YoY

Guidance for Q2 revenue $705M–$707M, in line with expectations

Diluted shares up +2.3% YoY

CAC Payback Period increased to 29.4 months, up +1.7 months YoY

R&D Index (RDI) declined to 1.58, down -0.68 YoY

SBC as % of revenue remains high at 25%, though improved QoQ

🔴 Negative

Free Cash Flow Margin declined to 17.6%, down -4.6 pts YoY

Net Margin dropped to -0.6%, down -4.1 pts YoY

Market Reaction to Earnings Release: The stock price up +5.1% following the earnings release.

Duolingo DUOL

The company reported its first quarter of 2025 results.

Thoughts on Duolingo Earnings Report $DUOL:

🟢 Positive

• Revenue grew to $230.7M, up +37.7% YoY, beating estimates by 3.5%

• EPS reached $0.72, up +35.8% vs. consensus

• Subscription revenue rose to $191.0M, up +45.0% YoY

• Paid subscribers hit 10.3M, up +39.2% YoY

• DAUs reached 46.6M, up +48.4% YoY; MAUs rose to 130.2M

• Billings grew to $272.9M, up +38.0% YoY

• Net new ARR grew +17.6% YoY to $67M

• R&D Index increased to 1.49, up +0.12 YoY

• FY25 revenue guidance raised to $987–996M (+32.5% YoY)

• Max adoption reached 7% of subs, with strong English learner uptake

• 48 AI-generated courses launched in 12 months vs. 100 over 12 years

• Math & Music DAUs surpassed 3M, growing faster than language

• Japan conversion strong; localized TV campaign for Max launched

• S&M, R&D, and G&A as % of revenue all declined YoY

• Dilution moderated: SBC/revenue fell to 13%, down -0.8 pps QoQ

🟡 Neutral

• Gross margin declined to 71.1%, down -1.9 pps YoY, but better than expected

• Operating margin dropped to 25.8%, down -0.3 pps YoY

• FCF margin fell to 44.6%, down -2.2 pps YoY

• Max margins remain low due to GenAI costs; improvement expected H2’25

• Pricing tested across regions; Super price raised for new users

• DET remains strategically important but contribution not broken out

• India and other low-ARPU regions show slower monetization; price cuts planned

• Course expansion includes pairings like Korean for Portuguese speakers, but English learner adoption still lags global trends

• CAC payback period rose to 4.6 months, up +0.2 YoY

• Net margin declined to 15.2%, down -0.9 pps YoY

🔴 Negative

• Max remains priced at $70/year in India, limiting growth in key market

• Perception as beginner tool slows English learner upgrades despite new content

• Institutional adoption of DET remains slow vs. legacy competitors

• App Store fees still a major COGS item; testing off-platform flow may reduce conversions

• Diluted share count up +3.4% YoY, a +4.7 pps QoQ increase

Market Reaction to Earnings Release: The stock price up +7.7% following the earnings release.

The Trade Desk TTD

The company reported its first quarter of 2025 results.

Thoughts on Trade Desk Earnings Report $TTD:

🟢 Positive

Revenue grew +25.5% YoY to $616M, beating estimates by 7.1%

Adjusted EBITDA margin rose to 33.8%, up +0.8pp YoY

Free cash flow margin expanded to 37.7%, up +1.8pp YoY

EPS of $0.33, beating estimates by +32.0%

Operating margin increased to 29.7%, up +1.3pp YoY

Net margin improved to 26.8%, up +0.1pp YoY

Customer retention held at 95%

Retail media growth supported by Walmart DSP and improved attribution

Deutsche Telekom saw 11x conversion lift, 18x CPA improvement on Kokai

OpenPath drove revenue growth: +79% at Arena Group, +97% at NY Post, +39% at Vizio

Two-thirds of clients adopted Kokai, driving strong ROI metrics

40%+ of spend now under JBPs, growing +50% faster than overall spend

International growth outpaced North America for 9th straight quarter

$386M in share repurchases, with $1.7B in cash and no debt

🟡 Neutral

Gross margin declined to 78.3%, down -1.7pp YoY

S&M, R&D, and G&A expenses declined as a % of revenue YoY, showing efficiency gains

Kokai rollout ahead of plan, but full transition still in progress

Sincera integration ongoing; Open Sincera and Deal Desk yet to launch

UID2 adoption strong, but some publishers still under-monetizing

Macro uncertainty and cautious brand budgets require continued focus on efficiency

🔴 Negative

Q2 revenue guidance of $682M (+16.6% YoY) missed consensus by -0.6%

Stock-based comp rose to 21% of revenue, up +3.4pp QoQ

Basic shares increased +1.3% YoY, adding mild dilution

Planning complexity due to 2025 U.S. election cycle and brand budget scrutiny

Market Reaction to Earnings Release: The stock price up +10.8% following the earnings release.

The Trade Desk launched OpenSincera, a free tool providing access to Sincera’s advertising metadata to improve digital ad supply chain transparency. Key metrics include ads-to-content ratio, page weight, ads-in-view, and ad refresh rate. The platform is open to the entire industry and includes an API for third-party integration. Following the Sincera acquisition, this expands data availability beyond the Kokai platform. CEO Jeff Green highlighted the aim to build trust and transparency by sharing supply chain data broadly.

GitLab GTLB

GitLab released GitLab 18, introducing AI-native features to enhance developer productivity and security. GitLab Duo Code Suggestions and Chat are now available at no extra cost for Premium and Ultimate users, offering real-time code generation, refactoring, test creation, and debugging within IDEs.

Core platform upgrades include centralized artifact management, a virtual registry for Maven, and CI/CD enhancements with modular pipeline structures and change detection for improved execution and security. GitLab Query Language enables search and content integration across the platform to improve reporting and team collaboration.

Security and compliance updates include custom compliance frameworks for SOC 2 and ISO 27001, advanced SAST logic, reachability analysis, and vulnerability dashboards. Additional updates include FIDO passkey login, biometric support, and a policy impact assessment tool with a non-blocking warn mode to guide secure development workflows.

GitLab has received FedRAMP Moderate Authority to Operate (ATO) for its GitLab Dedicated for Government platform, sponsored by the GSA (General Services Administration).

This milestone enhances GitLab’s positioning in the public sector, expanding access to its platform for agencies seeking secure cloud software delivery aligned with federal compliance needs.

Samsara IOT

Samsara launched the Upgrade for Smarter Operations program in the US and Canada to help companies using legacy systems like Motive, Verizon Connect, and Geotab switch to its AI-powered platform.

The platform delivers 8x ROI, 99.99% uptime, and is trained on 14T+ data points, offering real-time safety and efficiency insights. Hardware ships within 48 hours and includes a lifetime warranty. Top customers like ArcBest, USIC, and CarMax report faster innovation, better support, and lower costs after switching.

Samsara announced the global launch of Recognition, a new feature that helps fleet managers reinforce safe driving behavior using real-time data and AI-driven insights. Recognition enables managers to highlight streaks, milestones, and compliance improvements, delivering timely feedback through the Samsara Driver App. The tool aims to address high driver turnover, which can reach 94% at large carriers, by increasing engagement and morale. Fleets using Samsara have seen results including a 50% drop in accident costs and turnover at DHL, a 65% reduction in claims at Home Depot, and 70% less distracted driving in Memphis. Recognition is built into the Samsara platform, requiring no additional tools or effort to scale.

Samsara and Rivian announced a new integration enabling real-time access to Rivian vehicle data through the Samsara Platform. The partnership addresses the growing need for efficient management of electric and mixed fleets, especially as Rivian Commercial Vans gain adoption.

Samsara announced the Upgrade for Smarter Operations program across eight European markets, targeting businesses using outdated or unreliable systems such as Lightfoot, Microlise, Webfleet, Geotab, Verizon Connect, and others.

Available in the UK, Ireland, France, Germany, Austria, Switzerland, Netherlands, Belgium, and Luxembourg.

Samsara’s AI dash cams and real-time GPS tracking gave G&M full visibility across its fleet, improving driver safety and operational efficiency. The platform also supports G&M’s fleet electrification strategy by identifying optimal EV candidates based on usage data.

G&M Direct Hire has saved £5.2 million in operational costs by adopting Samsara’s Connected Operations Platform. The company reduced accident-related expenses by £1.8 million, recovered 55 stolen vehicles worth £3 million, and prevented over 940,000 excess miles, saving an additional £400,000. Case settlement times dropped by 50 percent, reducing resolution time by two months.

Thank you for reading!

Follow me for frequent updates on key news on X/Twitter and Threads @SergeyCYW and for visual infographics on Instagram.

For portfolio changes, follow me on SavvyTrader, where you'll find: current portfolio holdings, portfolio performance, trade alerts, and trade history.

Past recaps:

April 2025

March 2025

February 2025

January 2025

December 2024

November 2024

October 2024

September 2024

August 2024

July 2024

June 2024

May 2024

April 2024

March 2024

Disclaimer: This portfolio summary is for informational purposes only and not investment advice. Opinions are my own; please conduct your own due diligence.