Atlassian: Collaboration Software Leader with $176B Market Opportunity

Deep Dive into $TEAM: Valuation, Segment Growth, Key Metrics, Profitability, Expenses, Product Launches, Customer Acquisition, Financial Stability, SBC/Revenue, and Shareholder Dilution.

Atlassian: Company overview

About Atlassian

Atlassian Corporation is a global provider of collaboration and productivity software, founded in 2002 by Mike Cannon-Brookes and Scott Farquhar in Sydney, Australia. Originally launched with $10,000 in credit card debt, Atlassian has grown into a software leader with a market capitalization of $81.59 billion. The company operates dual headquarters in Sydney and San Francisco, employing over 12,000 people across 14 countries. Atlassian serves more than 300,000 customers in over 200 countries, including 92% of Fortune 500 companies. The company went public in December 2015 on NASDAQ under the ticker "TEAM", with an initial market capitalization of $4.37 billion. Its product portfolio includes Jira, Confluence, Trello, Bitbucket, and Jira Service Management.

Company Mission

Atlassian’s mission is to help teams work better together. The company designs scalable collaboration technologies that support digital workplace transformation. Its vision, "Teamwork makes the dream work," reflects a commitment to cross-functional collaboration. Strategic priorities include cloud platform development, workflow automation, team integration, and AI-driven tools. In 2023, Atlassian invested $674 million in R&D, equal to 22% of revenue.

Sector and Market Position

Atlassian operates in the enterprise software sector, focused on collaboration tools for software development, project management, and IT service management. It holds a 48.7% market share in project management software as of 2023, ranking second to Microsoft in software development product revenue. The company competes across three markets: software development, service management, and work management. Key competitors include Microsoft, GitLab, ServiceNow, Asana, Smartsheet, and Monday.com. Atlassian’s viral marketing and self-serve model eliminate traditional sales teams, supporting 81.82% gross margins. Cloud revenue reached $2.48 billion in fiscal 2023, reflecting 67% YoY growth.

Competitive Advantage

Atlassian's integrated product suite supports development, collaboration, and IT workflows through cross-platform functionality. The subscription model drives $2.75 billion in ARR, with 92% customer retention and >120% renewal rates. Its low-touch sales model relies on word-of-mouth and self-service adoption. The platform strategy supports strong cross-sell dynamics. The Atlassian Marketplace allows third-party development, expanding functionality and generating incremental revenue. High product quality and strong customer loyalty allow price increases without slowing growth, especially in the enterprise segment.

Total Addressable Market (TAM)

Atlassian’s serviceable addressable market is estimated at $67 billion, growing at 13% annually. This includes $15 billion for technical teams and $14 billion for non-technical teams, both expanding at 14% CAGR. The total addressable market is projected to reach $176 billion by 2025, growing at 11% annually. The target market includes 2.2 million companies with technical teams and 800,000 companies with more than 10 knowledge workers, totaling a potential 1.1 billion users. Atlassian currently serves 15 million users across 185,000 clients. Morgan Stanley projects 20%+ top-line CAGR, supported by enterprise adoption, seat expansion, cross-selling, and product innovation. The newly launched Rovo product could generate $400–$600 million in Cloud ARR by CY27.

Valuation

$TEAM Atlassian is trading at a Forward EV/Sales multiple of 8.9, significantly below its median of 11.0. The company's current Forward EV/Sales multiple is at historically low levels compared to the valuation lows of 2023–2024.

$TEAM Atlassian trades at a Forward P/E of 52.6, with revenue growth of +21% YoY in the most recent quarter.

The EPS growth forecast for 2026 is 22.4%, with a P/E of 55.9, resulting in a 2026 PEG ratio of 2.5.

The EPS growth forecast for 2027 is 23.2%, with a P/E of 45.7 and a 2027 PEG ratio of 1.9.

The PEG (Price/Earnings to Growth) ratio is a key tool for evaluating growth stocks, introduced by Peter Lynch.

PEG < 1: Undervalued – A ratio below 1 suggests the stock is undervalued. For example, if the P/E is 15 and earnings are expected to grow by 20%, the PEG would be 0.75, indicating a good buying opportunity.

PEG = 1: Fair Value – A PEG of 1 means the stock price matches its growth expectations, representing fair value.

PEG > 1: Overvalued – A PEG above 1 indicates the stock may be overvalued, as its price is higher than its projected growth rate, making it riskier.

Valuation comparison

Analysts forecast 21.3% revenue growth for $TEAM Atlassian in 2025 and 19.9% in 2026. Based on these projections, the company’s P/S multiple suggests it is fairly valued compared to companies in the DevOps sector.

Compared to companies in the CRM sector, $TEAM also appears fairly valued, considering its strong projected revenue growth.

Analysts expect strong revenue growth, so let's examine the key metrics to determine whether these expectations are justified.

We'll evaluate the company's economic moat, which supports long-term revenue growth, analyze revenue trends and the forecast for next quarter, and identify key factors that could help the company exceed expectations and sustain future growth.

We'll assess the performance of key segments, the launch of new products and updates, customer acquisition growth, key financial metrics, financial stability, and margin trends.

Additionally, we'll review the SBC/Revenue ratio, shareholder dilution, and finally, draw conclusions on the company's outlook.

Economic Moat

Atlassian Corporation has established a formidable competitive advantage in the enterprise software market. Let's examine each component of Atlassian's economic moat to understand how the company maintains its market position and defends against competitors.

Economies of Scale

Atlassian benefits from significant economies of scale driven by its viral marketing and self-service sales model. This approach supports 81.82% gross profit margins, while sales, general, and administrative costs remain at just 46% of gross profit. In contrast, Salesforce spends approximately 74% of gross profit on SG&A. With over 300,000 customers in 200+ countries and only 12,000 employees, Atlassian operates with high profitability per customer. As the customer base and product suite grow, operational efficiency continues to scale. This creates a moderate to strong scale advantage that improves with expansion.

Network Effect

Atlassian exhibits a moderate network effect, primarily through its Marketplace and internal collaboration adoption. The Atlassian Marketplace drives product value by enabling third-party developers to build extensions, creating a reinforcing cycle of growth. As usage of products like Jira and Confluence expands within teams, their value increases, generating internal stickiness. Though not as strong as platforms with user-to-user interaction, the growing user base and developer engagement continue to strengthen the ecosystem.

Brand

Atlassian has built a strong brand centered on collaboration and transparency. Its values—"Open company, no bullshit", "Build with heart and balance", and "Be the change you seek"—differentiate it in enterprise software. A 92% customer retention rate and the ability to increase pricing while growing customer count, especially in the enterprise segment, reflect high trust and loyalty. The brand resonates deeply with organizations focused on teamwork, giving Atlassian a durable competitive edge.

Intellectual Property

Atlassian holds 479 patents globally, with 313 granted and 88% active, covering various software technologies. The company’s most cited patent (US7974387B2) has 226 citations from firms like AT&T and Cisco. In 2023, Atlassian invested $674 million in R&D, equal to 22% of revenue and over 60% of gross profit. This level of investment signals a strategy built on continuous innovation. While the IP portfolio provides a moderate moat, sustained R&D is critical to defend against competition. The company’s moat lies more in execution and product quality than patent exclusivity.

Switching Costs

Switching costs are Atlassian’s strongest moat, creating high customer lock-in. Products like Jira, Confluence, and Trello embed deeply in workflows and store extensive operational knowledge. Migration away from Atlassian requires significant retraining, cost, and risk. The impact is seen in the company’s 92% customer retention and >120% renewal rate, as customers not only remain but expand usage. Atlassian’s integrated platform strengthens this lock-in effect, making the ecosystem increasingly central to enterprise operations.

Atlassian's economic moat is multifaceted and robust, with switching costs and brand representing its strongest competitive advantages. The combination of these moat components has enabled Atlassian to maintain its market leadership position and achieve consistent growth despite increasing competition in the enterprise software space.

Revenue growth

$TEAM Atlassian's revenue growth accelerated from 20.5% YoY in Q2 2024 to 21.3% YoY. Based on the forecast for the next quarter, if the company beats its guidance by 3.6%, as it did in Q4, Q1 revenue growth would reach 17.9%, indicating a potential significant deceleration in growth.

RPO is growing faster than revenue, up 42.1% YoY.

Segments and Main Products

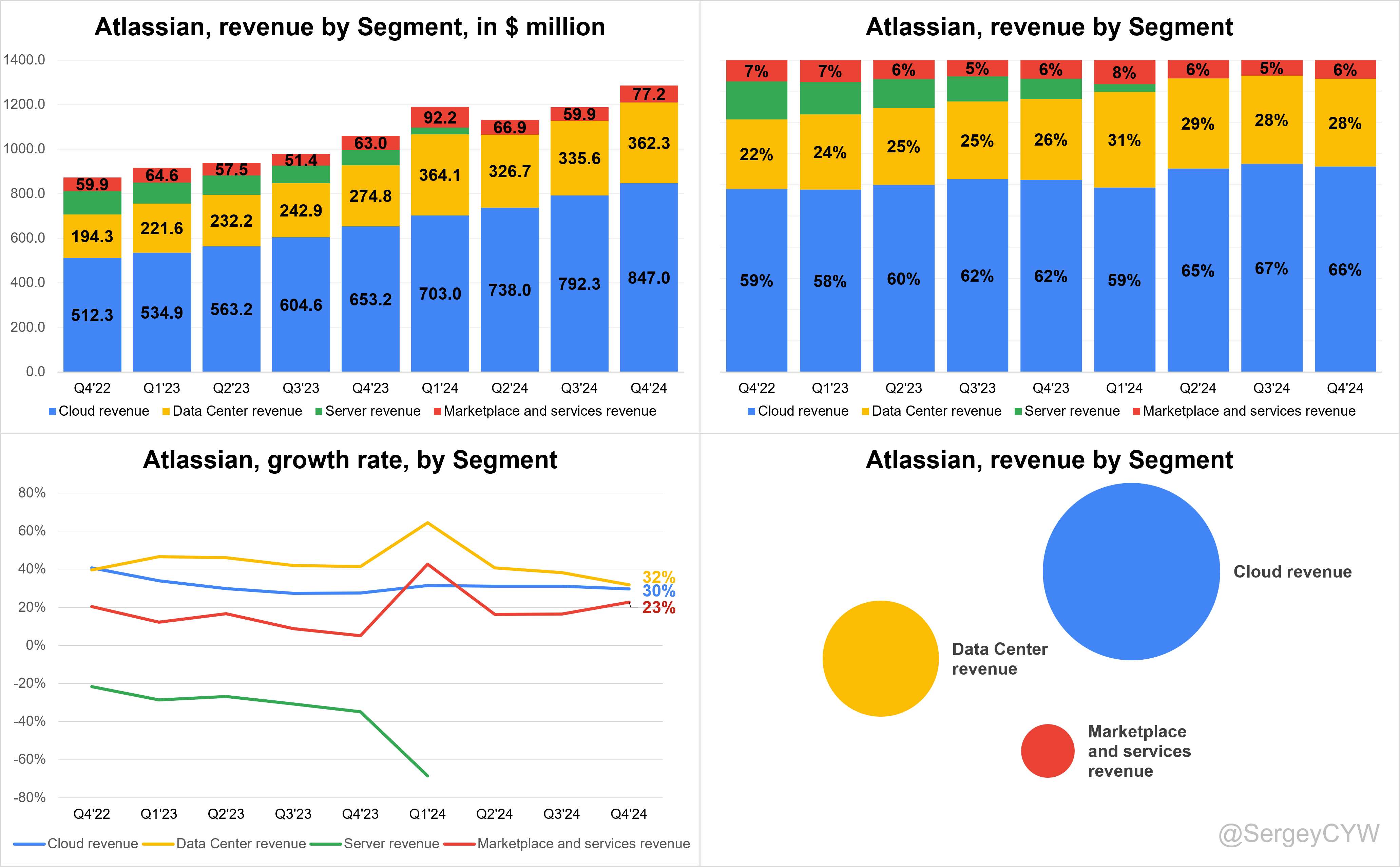

Revenue Segments

Atlassian’s revenue is divided into three core segments: Cloud services, Data Center (which serves organizations requiring on-premises or private cloud deployments), and Marketplace and other revenue, which comes from third-party apps and product integrations that enhance the core platform's capabilities.

Jira

Jira is Atlassian’s leading product and top revenue contributor. Initially built as a bug-tracking solution, it has evolved into a robust platform for agile project management. Jira allows teams to plan, track, and manage tasks and workflows across sprints, becoming essential for software development organizations.

Confluence

Confluence functions as a collaborative workspace for team documentation and content sharing. It supports up to 150,000 users on a single site in Confluence Cloud, enabling large-scale migrations from Data Center and broader organizational deployment. It centralizes knowledge, streamlining cross-team communication and documentation.

Trello

Trello provides a visual, board-based project management interface built on a flexible card system. Its simplicity appeals to both technical and non-technical users. Trello scales from basic task tracking to more advanced workflow coordination, making it versatile across departments.

Bitbucket

Bitbucket delivers source code management for Git repositories, supporting team collaboration in software development. It features inline code comments, pull requests, and native integration with Atlassian’s broader ecosystem, enabling teams to maintain code quality while accelerating delivery.

Atlassian Access

Atlassian Access offers centralized enterprise-level security and administrative controls across all cloud products. It helps organizations manage users and permissions consistently, supports identity integration, and mitigates risks like shadow IT. Access ensures secure scaling without reducing productivity or flexibility.

Main Products Performance in the Last Quarter

$TEAM Revenue by Segment: 94% of the company’s revenue comes from subscriptions, which include Atlassian Cloud (66%) and Data Center (28%) of total revenue. Marketplace and services revenue account for the remaining 6%.

Subscription revenue growth remained strong at +30.2% YoY in Q4, driven primarily by Data Center, which delivered the highest growth at +32% YoY.

Atlassian Cloud grew +30% YoY, while Marketplace and services revenue increased +23% YoY.

Cloud Services

Cloud revenue continues to drive Atlassian’s growth, crossing $5 billion in ARR with 30% YoY subscription revenue growth. Cloud gross margin improved to 85%, supported by engineering-led efficiencies. Upsell to premium and enterprise SKUs rose +40% YoY, highlighting growing enterprise trust. Over 1 million monthly active users now engage with Atlassian Intelligence, marking a major milestone in AI adoption and retention. Paid seat expansion in SMB stabilized. Enterprise migrations and multi-year deal activity remain strong.

Jira

Jira remains the flagship product. Jira Service Management (JSM) has grown into a $500M+ business with over 55,000 customers. Growth is fueled by platform leverage, AI enhancements, and tight integration across the toolset. Atlassian’s end-to-end visibility across the software lifecycle cements Jira as a central workflow engine. The rollout of Jira Product Discovery in premium and enterprise tiers expands reach into product workflows. Demand remains strong for enterprise-grade features and automation.

Confluence

Confluence is benefiting from broader cloud and AI momentum. Loom is now integrated into collaboration workflows, adding value. Atlassian Intelligence and AI-generated meeting summaries are expected to deepen user engagement across documentation layers.

Trello

No new updates were provided. It continues to integrate within the Atlassian suite. AI-powered automation and summarization are likely improving its utility, but Trello is not a key focus for enterprise expansion right now.

Bitbucket

Bitbucket Pipelines supports a hybrid monetization model—seat-based and usage-based. It’s strategic to Atlassian’s developer operations strategy and integrated with AutoDev. Bitbucket showcases Atlassian’s flexible pricing capabilities already live in core workflows.

AI Agents & Rovo

AI is scaling fast. AI feature usage is up 25x YoY, and over 1 million users interact monthly with Atlassian Intelligence. Rovo and AutoDev are still early-stage but position Atlassian ahead of the curve with virtual agents that go beyond chat—they execute tasks, navigate access permissions, and take structured actions. Rovo supports both first-party and user-defined agents. Developers report hours saved weekly. Use cases are growing in service, HR, and support. Atlassian’s multi-model AI strategy—30+ models from 7+ vendors—combined with its proprietary teamwork graph creates a clear moat. Over 50 discrete AI capabilities are live across the product suite. AI is already nudging customers to higher-tier SKUs, driving +40% YoY growth in upgrades.

Data Center

Q3 guidance implies +7% YoY revenue growth, supported by pricing, seat expansion, and cross-sell. Large deals are increasingly structured as hybrid ELAs, giving rights to both Cloud and Data Center. Many customers still run 50–100 instances, delaying full cloud migration, but most are on a path forward. No technical blockers cited. Strong multi-year contract attach rates are improving billings even as revenue recognition lags.

Innovation & Product Updates

Key product launches include Rovo, Compass, and the premium tiers of Jira Product Discovery. Atlassian is executing on its “system of work” vision—becoming the operating layer for modern, tech-driven companies. It is building an enterprise-ready teamwork graph that powers AI, search, and agent functionality across the stack. Internal usage of AI agents has already saved thousands of hours. Loom is now AI-enhanced, with 38 million videos edited by AI in 2024 alone. Enterprise Search is now deeper and more connected. The company is pushing forward in agentic computing, maintaining a leadership position in the virtual teammate category. AI capabilities are deployed at scale and continuously updated under a rigorous multi-model framework.

Revenue by Region

The Americas account for 48% of total revenue, making it Atlassian’s $TEAM largest market, with revenue growing +20% YoY in Q4.

EMEA represents 41% of total revenue, also holding a significant share, and is growing at a faster pace of +24% YoY.

APAC contributes 11% of total revenue and has the slowest growth rate, at +18% YoY.

Market Leaders

DevOps Platforms

$TEAM Atlassian has been named a Leader in the Gartner Magic Quadrant for DevOps Platforms for two consecutive years. The company first received this recognition in 2023 when Gartner published its first-ever Magic Quadrant for DevOps Platforms. This leadership position was maintained in 2024, with Atlassian being recognized again as a Leader in the same category. Atlassian's cloud-based DevOps platform brings together engineering, product, ITOps, and business teams to accelerate engineering, improve application health and reliability, and deliver software faster.

Marketing Work Management Platforms

In December 2024, Atlassian was recognized as a Leader in the 2024 Gartner Magic Quadrant for Marketing Work Management Platforms. This recognition highlights how Atlassian's work management solution, particularly Jira, has become valuable for marketing teams. Jira helps marketers plan, organize, and collaborate with various teams including sales, legal, design, and product to create campaigns efficiently.

Customers

$TEAM Atlassian added 2,605 customers with ARR over $10K, with growth slowing to +15% YoY. While this addition is lower than the same period last year, customer growth remains solid, as Q4 is typically a seasonally strong quarter for the company.

Large Customer Wins

Atlassian delivered a record number of $1 million+ ACV deals in Q2 FY2025. The expansion of large-scale agreements reflects strong product-market fit across the enterprise tier. Over 500 customers now spend $1M+ annually, a figure steadily climbing as adoption of premium and enterprise SKUs accelerates. Notable wins include major organizations across diverse verticals, with a focus on those consolidating collaboration and workflow tools.

Strategic enterprise agreements show rising trust in Atlassian’s unified platform. Companies are committing not only to Jira and Confluence but also to new AI-powered offerings, signaling confidence in Atlassian Intelligence and the emerging Rovo agentic stack. Multi-year contracts and hybrid ELAs contributed meaningfully to billings outperformance, although revenue recognition will follow over time due to accounting treatment.

The Loom acquisition is also driving traction in enterprise, with large customers increasingly integrating video-based collaboration into Jira and Confluence environments. Loom generated 38 million AI-powered videos last year, signaling growing usage at scale within high-value accounts.

Customer Success Stories

Cisco, DHL, and Reddit were highlighted as leading examples of enterprise adoption. These companies are leveraging Atlassian’s cloud platform to bridge gaps between business and technical teams. Jira’s integration with business operations is expanding seat penetration beyond engineering, enabled by the unification of Jira Software and Jira Work Management.

A leading European telecom added Atlassian to its list of top strategic vendors. The CIO explicitly requested that Atlassian become one of its top four partners, alongside hyperscalers. The company presented a detailed roadmap of feature and compliance expectations, which Atlassian is actively addressing. The customer cited the teamwork graph, AI integration, and unified system of work as differentiators.

Another major financial institution accelerated its migration to cloud based on the immediate value perceived in Atlassian Intelligence and analytics capabilities. The decision reflects growing alignment between AI strategy and enterprise customer demands. Speed of deployment, combined with FedRAMP and enterprise-grade compliance, played a key role in this transition.

Customer feedback consistently emphasized Atlassian’s ability to connect strategic goals with operational execution. R&D velocity, AI differentiation, and seamless cross-product integration are driving increasing depth in customer relationships and reinforcing long-term revenue visibility.

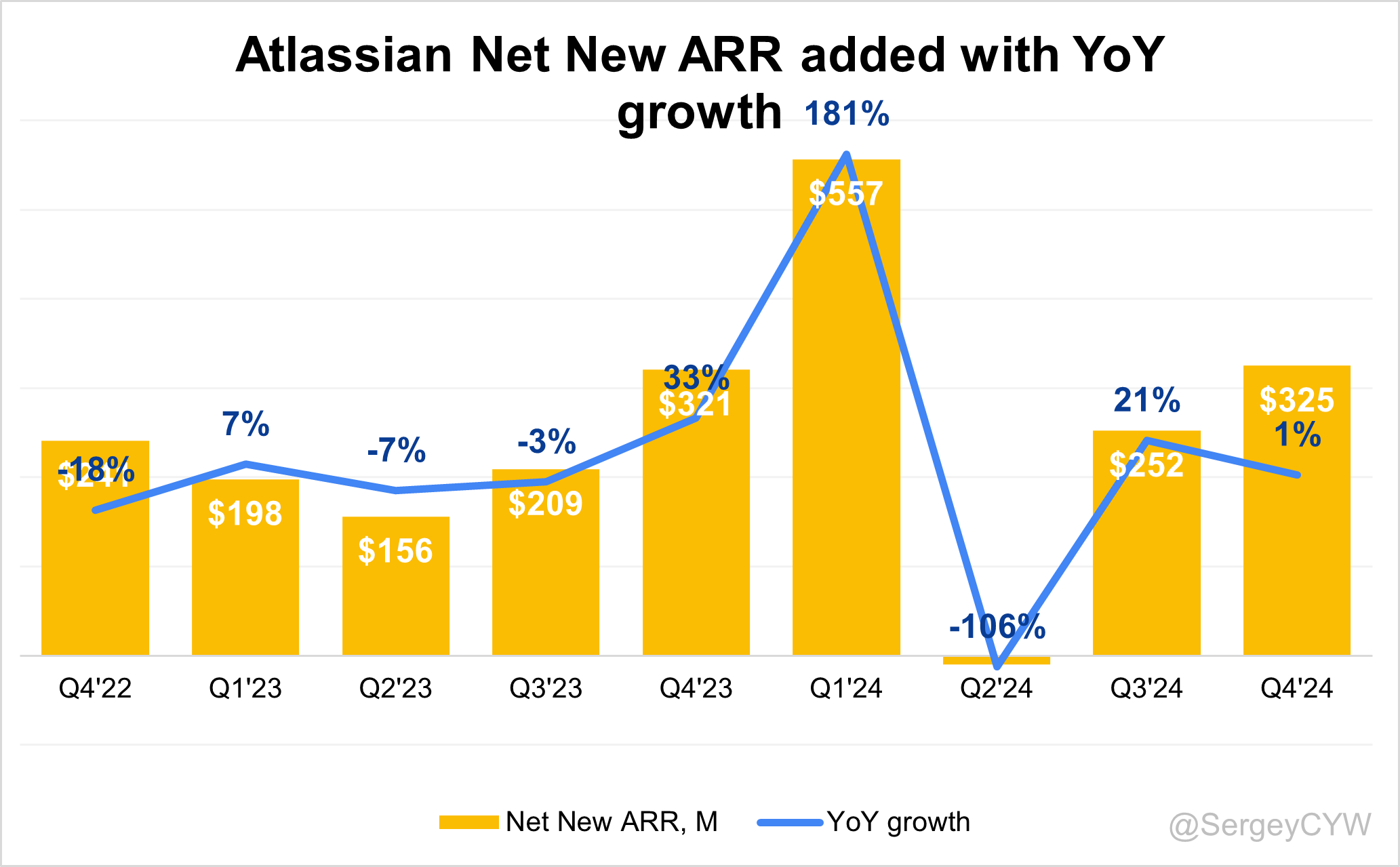

Net new ARR

$TEAM Atlassian added $325 million in net new ARR in Q4 2024, which is 1% higher year-over-year.

This net new ARR addition is roughly in line with the two-year average.

CAC Payback Period and RDI Score

$TEAM Atlassian's return on Sales & Marketing (S&M) spending stands at 9.3, with a CAC Payback Period significantly better than the SaaS average (the median for the SaaS companies I track is 20.8 months). This makes Atlassian’s CAC Payback one of the best among SaaS companies.

The R&D Index (RDI Score) for Q4 is 0.63, which is below the 1.2 median of the SaaS companies I monitor, but still above the broader industry median of 0.7, indicating a healthy level of R&D investment.

An RDI Score above 1.4 is considered best-in-class, underscoring the importance of efficient R&D allocation.

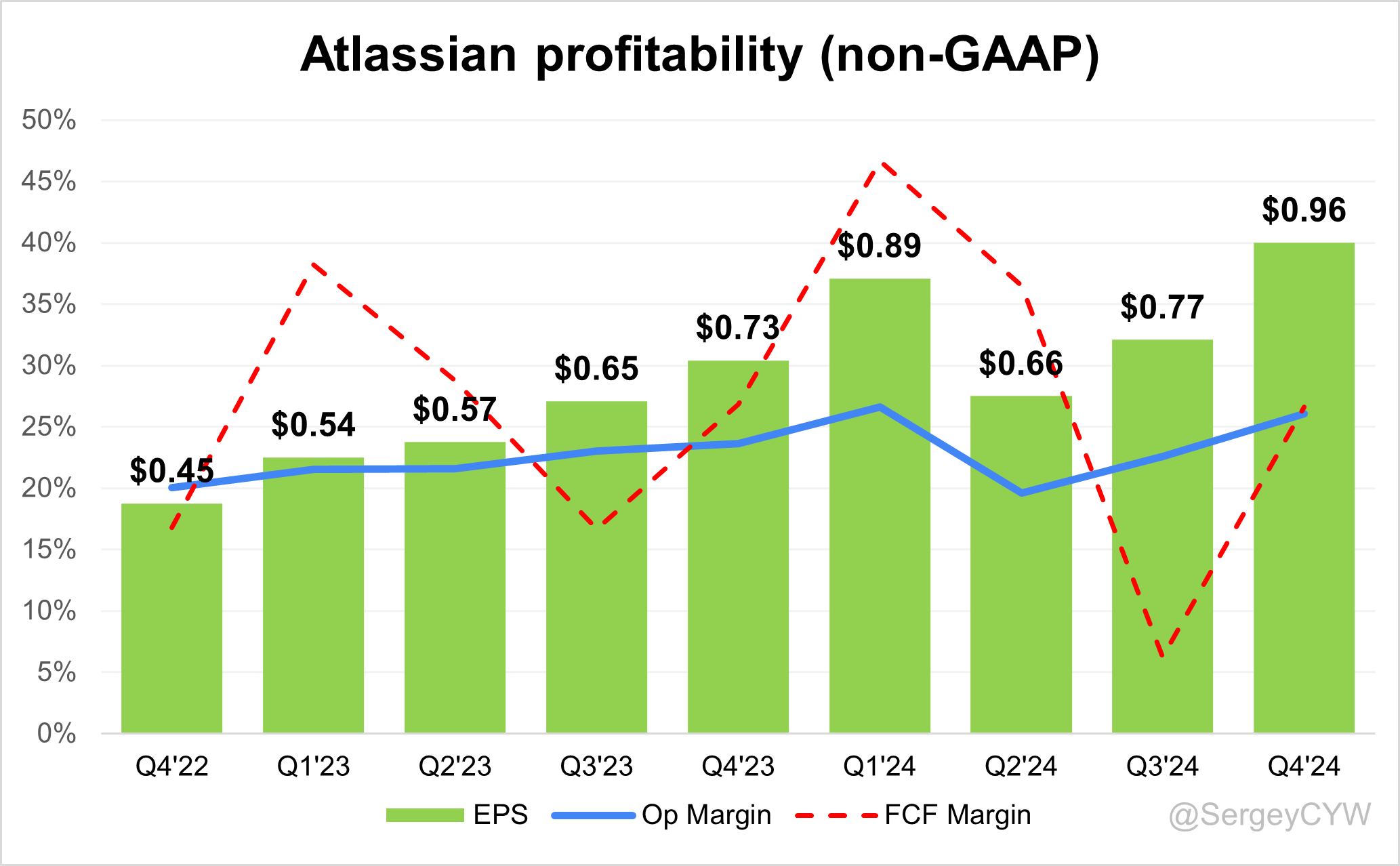

Profitability

Over the past year, $TEAM Atlassian has experienced changes in its margins:

Gross Margin significantly increased from 84.1% to 85.2%.

Operating Margin improved from 23.6% to 26.1%.

Free Cash Flow (FCF) Margin slightly decreased from 26.8% to 26.6%.

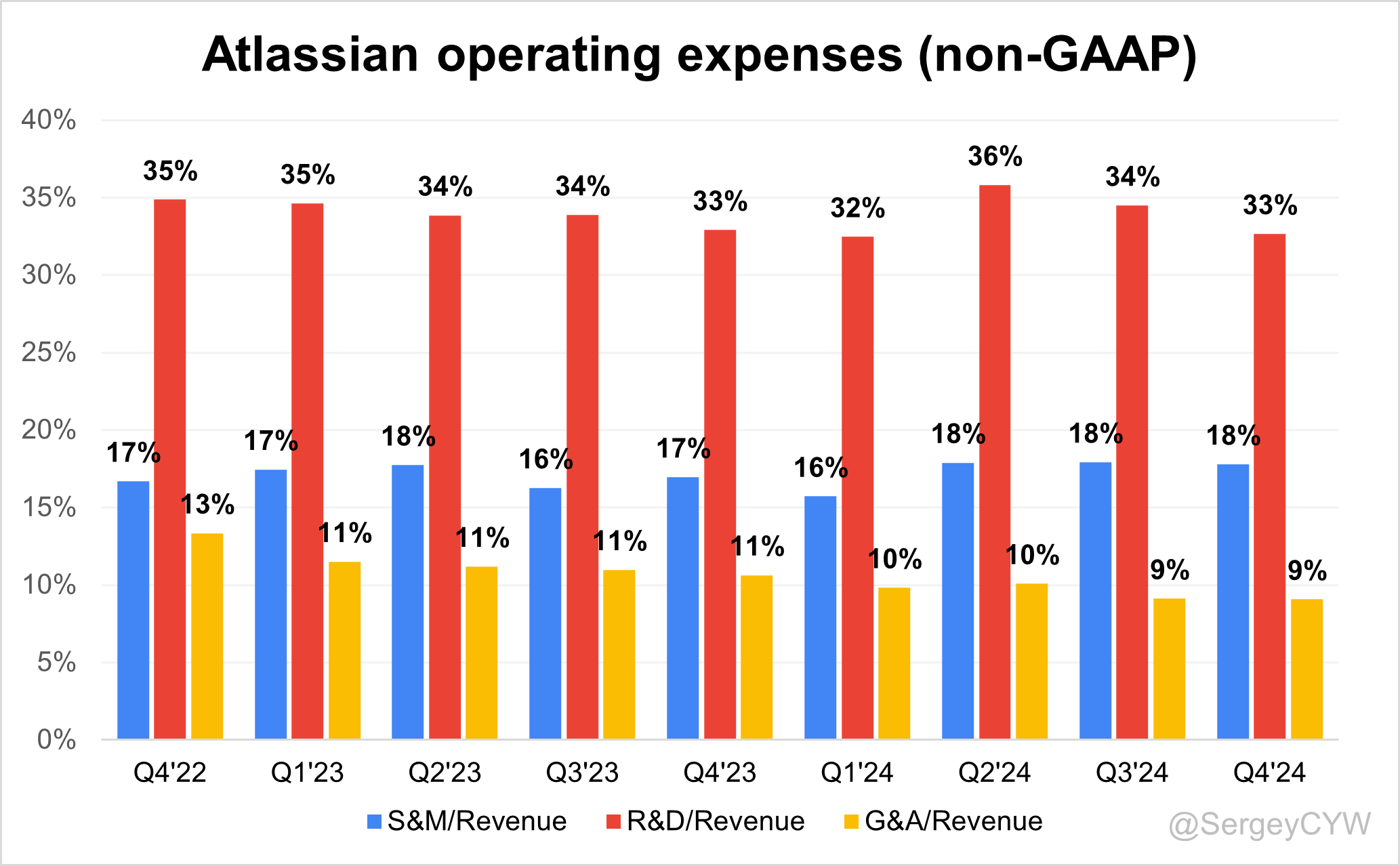

Operating expenses

$TEAM Atlassian's non-GAAP operating expenses have slightly decreased, driven by reduced G&A spending. S&M expenses have slightly increased from 17% two years ago to 18%.

The R&D share remains high at 33%, reflecting the company’s continued investment in future growth through platform enhancements and updates. It's important to note that R&D expenses exceed the combined total of S&M and G&A.

General & Administrative (G&A) expenses have also decreased, from 13% two years ago to 9%.

Balance Sheet

$TEAM Balance Sheet: Total debt stands at $1,245 million, while Atlassian holds $2,469 million in cash and cash equivalents, far exceeding its liabilities and reflecting a healthy balance sheet.

Dilution

$TEAM Shareholder Dilution: Atlassian’s stock-based compensation (SBC) expenses have increased over the past two quarters and now account for 29% of revenue, slightly above the SaaS sector median.

Shareholder dilution remains well-controlled, with the weighted-average number of basic common shares outstanding increasing by 1.0% YoY.

Conclusion

$TEAM Atlassian holds the distinction of being the only platform recognized as a Leader in the Gartner Magic Quadrant for both DevOps and Marketing Work Management. This dual recognition highlights Atlassian's versatility and effectiveness across different team types and workflows, supporting its vision to make Jira the single record of work for all teams. The company’s TAM is estimated at $176 billion. Atlassian's economic moat is anchored by very strong switching costs, driven by deep integration into customer workflows.

Leading Indicators:

• RPO growth of +42.1% is significantly above revenue growth.

• Net new ARR additions are in line with the two-year average, up +1% YoY.

• Customer additions remained strong, although slightly below the level of last year.

Key Indicators:

• CAC Payback Period improved to 9.3 months, one of the best among SaaS companies.

• RDI Score is 0.63, below the SaaS median, but still within a healthy range.

The revenue growth forecast for next quarter suggests a noticeable deceleration, but the leading indicators show strong momentum, suggesting management may have issued a conservative outlook. RPO growth significantly outpaces revenue growth, and net new ARR and customer additions remain strong.

Management emphasized that deeper engagement with Fortune 500 companies, premium product expansion, and AI monetization will drive progress toward the company’s $10 billion annual revenue goal.

Atlassian continues to prioritize R&D investments, with R&D expenses exceeding S&M expenses, reinforcing its focus on innovation.

Valuation appears fair relative to revenue growth forecasts and competitive benchmarks, and the company is trading near historical valuation lows.

The weak guidance for the next quarter raises some concerns, but I continue to keep $TEAM on my watchlist as a strong player in two significant and expanding markets.

The competition with Microsoft is a big threat, how do you assess this risk? IMO sometimes there could be place for several players in the same space but with different customer type.