Will Agentic AI Replace Workflow Platforms, or Make Monday More Essential?

Deep Dive into $MNDY: Valuation, Segment Growth, Key Metrics, Profitability, Expenses, Product Launches, Customer Retention, Financial Stability, SBC/Revenue, and Shareholder Dilution.

Monday revenue grew +26.3% YoY, confirming a deceleration, yet forward-looking signals improved. RPO accelerated to +36.3%, outpacing revenue growth and pointing to strengthening demand. Net new ARR hit a record, customer additions remained strong across total and large accounts, and new products reached 10.2% of ARR, growing far faster than the core business. Valuation now sits near historical lows, despite expectations for Monday to remain one of the fastest-growing CRM platforms into 2026. The setup looks asymmetric. Yet a key concern persists: can revenue growth stabilize before deceleration reshapes investor sentiment further? The answer sits deeper in the data and the execution ahead.

Table of Contents:

1. Company Overview – A brief summary of the company, including its mission, sector, competitive advantage, and total addressable market (TAM).

2. Valuation – Analysis of changes in Forward EV/Sales and Forward P/E multiples, along with comparisons to peers within the same sector.

3. Economic Moat – Evaluation of the company’s moat across five key types: Economies of Scale, Network Effect, Brand, Intellectual Property, and Switching Costs.

4. Revenue Growth – Review of revenue growth dynamics over the past two years.

5. Segments and Main Products – Overview of the company’s business segments, latest quarterly performance by segment, product innovation.

6. Market Leadership – Assessment of the company’s leadership status in its segment, as recognized by reputable rating agencies like Gartner, The Forrester Wave, etc.

7. Customers – Analysis of customer growth trends, customer success stories, and major customer wins. Strategic Partnerships and International Expansion.

8. Key Performance Indicators (KPIs) – Review of Retention, profitability, operating expenses, balance sheet strength, and shareholder dilution.

9. Conclusion – Final thoughts and summary based on the above analysis.

1. Company overview

About Monday

Monday is a global software company that transforms how businesses operate through its cloud-based Work OS platform. The Israeli-based company serves >245,000 customers across more than 200 industries, making it one of the leading work management solutions worldwide. Founded in Israel with headquarters in Tel Aviv, Monday went public in June 2021 and trades on NASDAQ under the ticker MNDY.

Company Mission

Monday’s mission centers on helping teams build a culture of transparency, empowering everyone to achieve more and be happier at work. The company aims to democratize the power of software by making complex work management accessible to users regardless of technical background. The mission focuses on fostering transparency through visual dashboards and empowerment through customizable workflow solutions.

The platform’s low-code/no-code approach directly supports this mission by enabling users to build custom applications without technical expertise. Monday’s commitment to user experience drives continuous product development, with the company investing heavily in AI-powered features to enhance workplace efficiency.

Sector and Market Position

Monday operates in the work management and productivity software sector, specifically targeting the Work OS market. The company offers a multi-product platform including work management, CRM, development tools (monday dev), and service management solutions. The platform serves diverse industries from marketing and sales to IT operations and project management.

The company competes against established players like Atlassian, Wrike, Trello, and Airtable in the collaborative work management space. Monday differentiates itself through its visual interface and customizable workflow capabilities that adapt to various business needs.

Competitive Advantage

Monday’s primary competitive advantage lies in its multi-product platform that runs all core aspects of work within a single ecosystem. The company’s Work OS allows organizations to build custom workflow applications without coding, providing flexibility that traditional project management tools cannot match. The platform’s visual and intuitive interface reduces adoption barriers significantly.

The company’s AI Vision for 2025 focuses on three strategic pillars: AI Blocks, Product Power-ups, and Digital Workforce. Monday observed a tenfold increase in AI feature usage, reaching 10 million AI-powered actions in Q4 2024. The platform’s AI capabilities give SMBs and mid-market companies competitive advantages to scale without increasing resources.

Strong customer retention metrics demonstrate platform stickiness. The platform’s adaptability across 200+ industries provides significant market reach and revenue diversification.

Total Addressable Market (TAM)

Monday addressable market grows from $158B in 2025 to $225B by 2028F, a 12% CAGR, driven by consolidation across multiple software categories that historically lived in separate tools.

Work management remains the largest pillar at $58B, covering collaborative applications and project and portfolio management. Demand here compounds as organizations standardize workflows across teams, turning initial adoption into broad internal expansion with minimal churn.

Service management adds a $45B opportunity tied to IT service management, IT operations, and internal ticketing. Growth is structural, driven by cloud complexity and the replacement of rigid legacy systems with configurable platforms that adapt to internal processes.

CRM contributes $32B, extending the platform into sales productivity, marketing automation, and customer service. This increases monetization depth by attaching revenue-facing functions to existing users instead of relying solely on seat growth.

Dev and DevOps use cases represent $23B, spanning application development, system management, and planning. Adoption in this segment increases stickiness, as workflows become embedded in daily engineering operations.

Adjacent markets are reinforcing TAM expansion. The remote work collaboration tools market is projected to hit $24.41 billion by 2027, growing at 15.2% CAGR. AI-powered workflow management is expected to reach $19.4 billion by 2025. The productivity software partnership market is forecast to grow to $102.58 billion by 2028.

2. Valuation

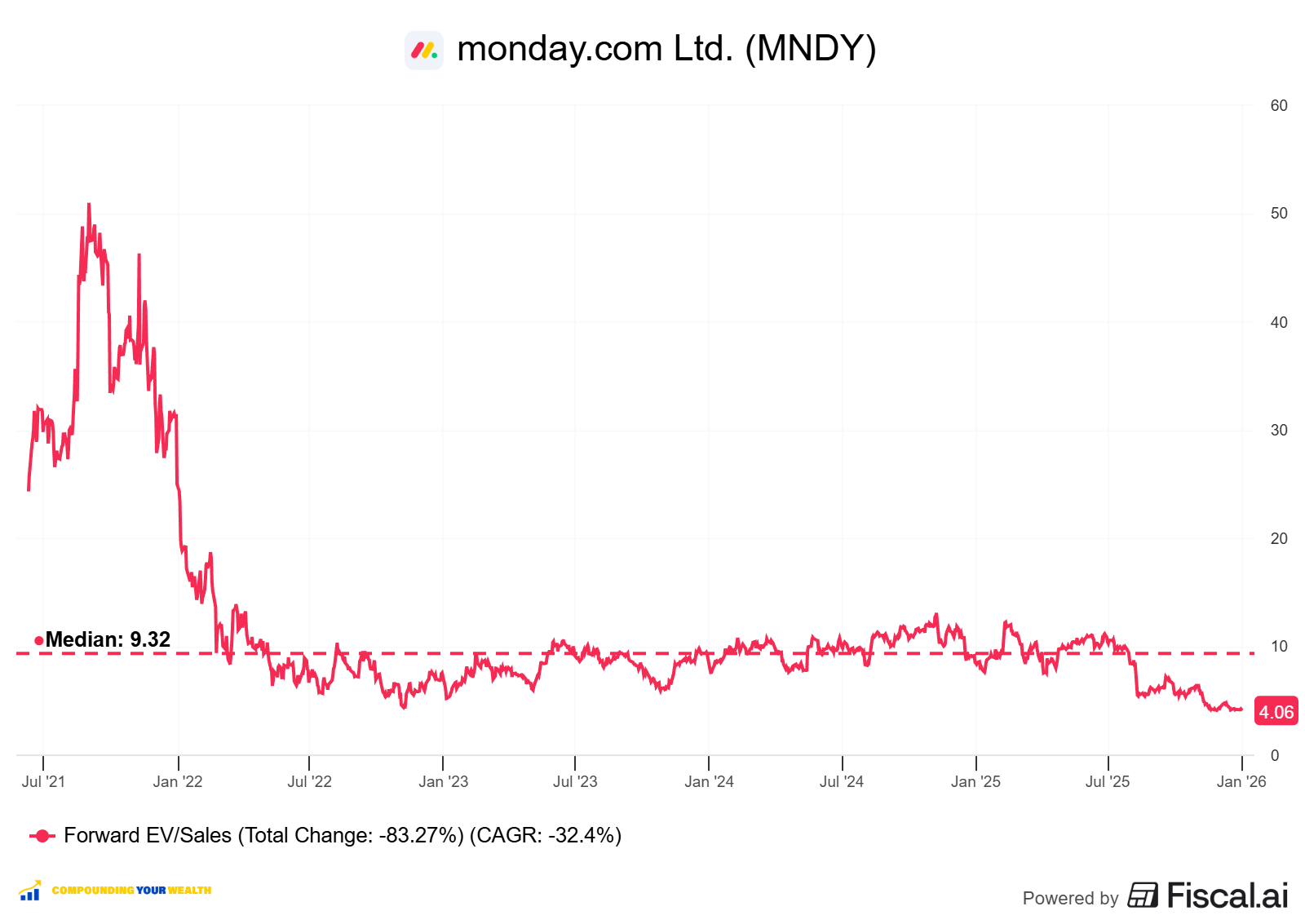

$MNDY is trading at a Forward EV/Sales multiple of 4.1, well below the median of 9.3 and close to historical lows.

Powered by Fiscal.ai — get 15% off with affiliate link for Compounding Your Wealth readers.

$MNDY trades at a Forward P/E of 31.7, with revenue growth of +26.3% YoY in the last quarter. This forward P/E ratio is 1.2 times the anticipated revenue growth rate.

The EPS growth forecast for 2026 is 34.7%, with a P/E of 32.9 and a PEG ratio of 0.9.

Powered by Fiscal.ai — get 15% off with affiliate link for Compounding Your Wealth readers.

The PEG (Price/Earnings to Growth) ratio is a key tool for evaluating growth stocks, introduced by Peter Lynch.

PEG < 1: Undervalued – A ratio below 1 suggests the stock is undervalued. For example, if the P/E is 15 and earnings are expected to grow by 20%, the PEG would be 0.75, indicating a good buying opportunity.

PEG = 1: Fair Value – A PEG of 1 means the stock price matches its growth expectations, representing fair value.

PEG > 1: Overvalued – A PEG above 1 indicates the stock may be overvalued, as its price is higher than its projected growth rate, making it riskier.

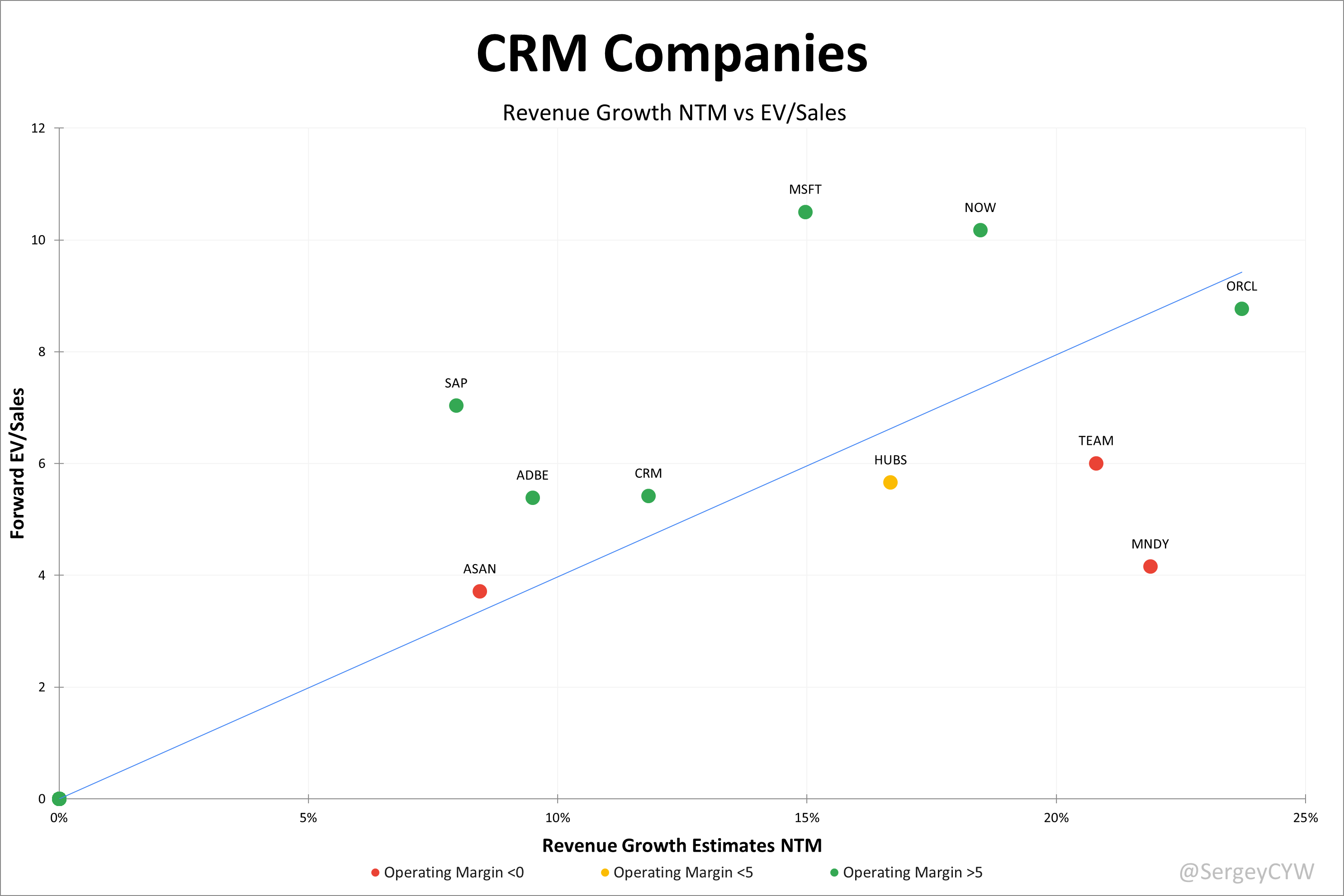

Valuation comparison

Analysts forecast +21.9% NTM revenue growth for $MNDY. Given these projections, the EV/Sales valuation appears undervalued relative to other CRM companies, especially considering $MNDY has one of the highest expected revenue growth in the CRM sector.

Analysts expect strong revenue growth, so let’s examine the key metrics to determine whether these expectations are justified.

We’ll evaluate the company’s economic moat, which supports long-term revenue growth, analyze revenue trends and the forecast for next quarter, and identify key factors that could help the company exceed expectations and sustain future growth.

We’ll assess the performance of key segments, the launch of new products and updates, customer acquisition growth, key financial metrics, financial stability, and margin trends.

Additionally, we’ll review the SBC/Revenue ratio, shareholder dilution, and finally, draw conclusions on the company’s outlook.

3. Economic Moat

Economic Moats enable companies to remain stable during crises and support long-term revenue growth.

Economies of Scale

Monday demonstrates strong economies of scale that expand as the company grows. 89.6% non-GAAP gross margins reflect efficient unit economics, where incremental revenue flows with minimal cost. With $1+ billion ARR and >245,000 customers, fixed development and infrastructure costs are spread across a broad base. A global cloud footprint across multiple regions enables efficient scaling without proportional cost increases. While SaaS competition often caps pricing power, the recent price increase combined with record customer additions shows Monday does, in fact, hold pricing leverage.

Network Effects

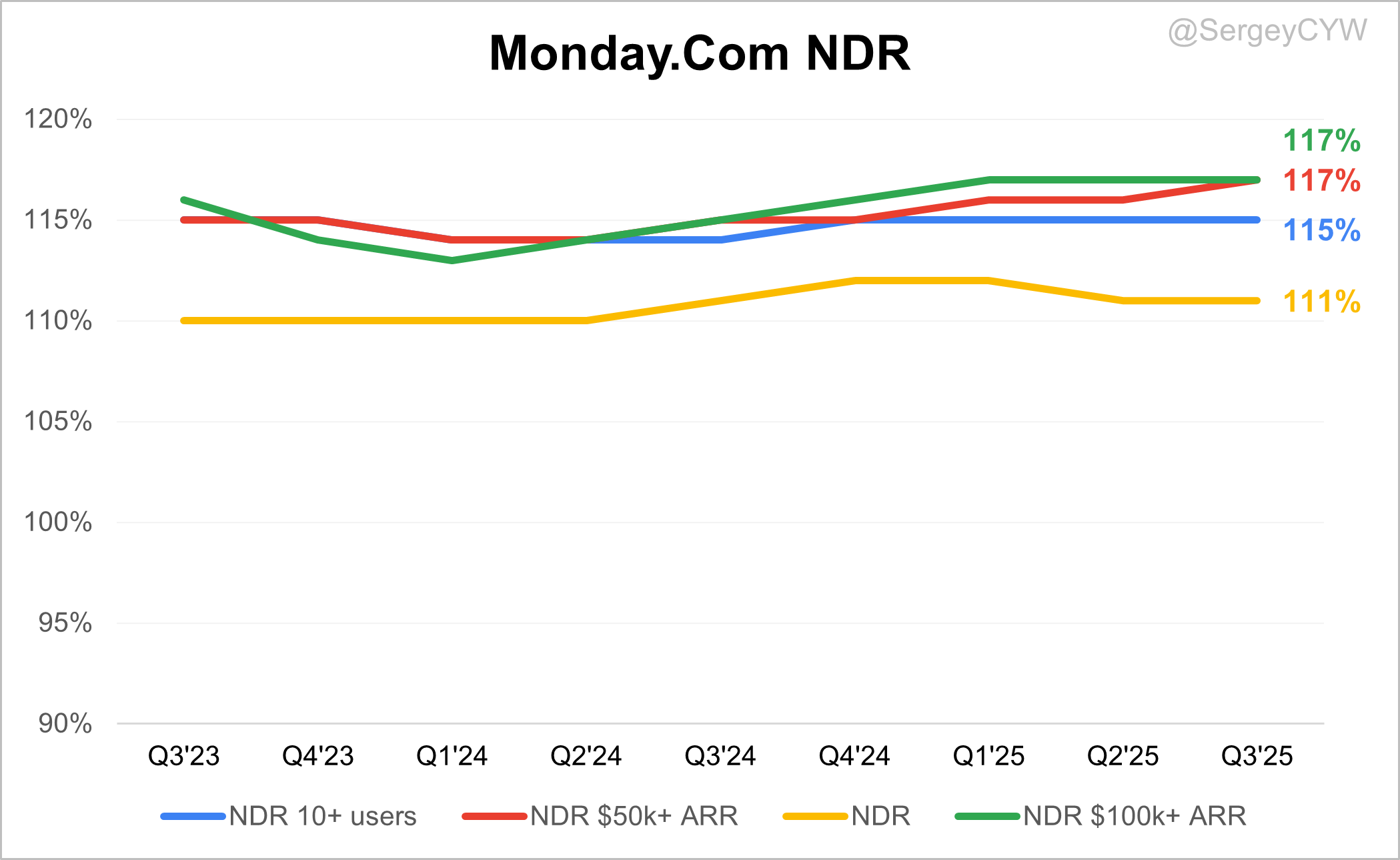

Network effects are moderate but emerging. The Monday Apps Marketplace allows third-party developers to build integrations and extensions, seeding platform dynamics. As the ecosystem grows, customer retention strengthens and replication becomes harder for rivals. A net dollar retention rate of 111% overall, rising to 117% for customers with $50k+ ARR, indicates usage expansion and integration benefits. Yet network effects remain less robust than consumer platforms, as value stems more from internal workflow optimization than external connections.

Brand Strength

Brand strength is a clear asset. Over $200 million was spent on video marketing in 2020–2021, equal to 95% of revenue at the time, cementing recognition in the work management space. Monday is rated 4.5 out of 5 on Gartner Peer Insights and consistently recognized as “most loved” on G2. The company emphasizes trust, transparency, and intuitive design, supported by a distinctive traffic light color system, professional logo, and consistent presence across social, digital, and offline channels.

Intellectual Property

Intellectual property is limited as a moat. Trademarks, service marks, and proprietary technology protect the Work OS platform, but core project management functionality is not easily patentable. The no-code interface and modular building blocks are proprietary but face competition from similar approaches. AI-powered features and the planned Monday Expert AI agent offer temporary differentiation yet remain replicable in a fast-moving SaaS landscape where execution outweighs patents.

Switching Costs

Switching costs form Monday’s strongest moat. Deep workflow embedding creates high barriers to exit, as teams configure custom workflows, automations, and third-party integrations that evolve into critical infrastructure. Over time, the platform becomes a repository of institutional knowledge and business logic. Migration is disruptive and resource-intensive, requiring competitors to deliver not only superior features but also seamless transitions for highly customized processes.

Monday’s economic moat is moderate overall, with switching costs and brand strength providing the primary competitive advantages. The company’s ability to embed itself into customers’ operational workflows creates the strongest defensive position, while continued investment in ecosystem development and AI capabilities may strengthen network effects over time.

4. Revenue growth

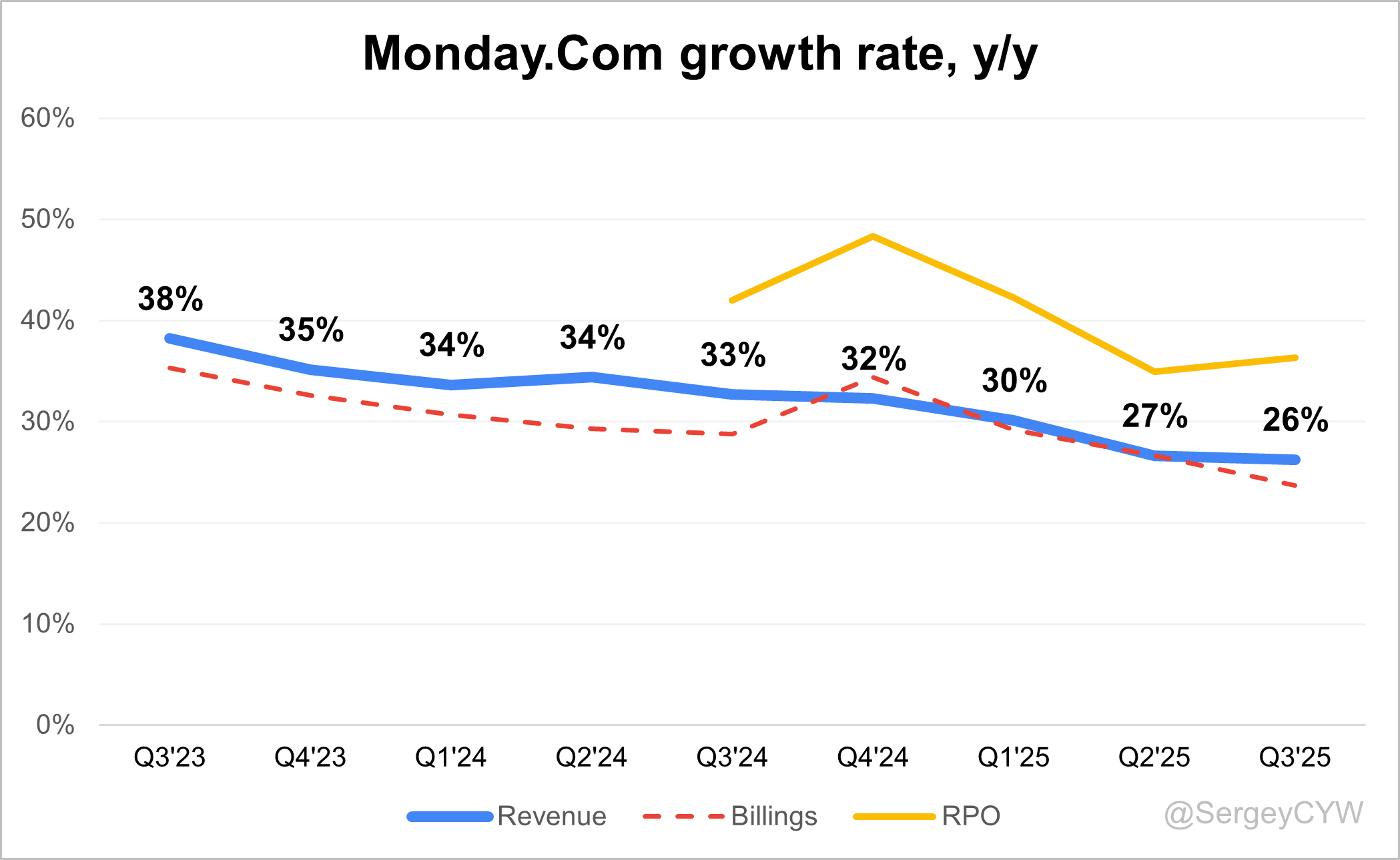

$MNDY’s revenue growth slowed slightly from +26.6% YoY in Q2 to +26.3% in Q3. Based on guidance, even with a 1.2% beat, Q4 growth would fall to ~24.7%, signaling further deceleration.

Billings growth slowed to +23.7%, now below revenue growth.

In contrast, RPO growth accelerated to +36.3%, outpacing revenue growth and supporting long-term demand visibility.

5. Segments and Main Products.

Monday CRM is a fully customizable, AI-powered sales platform that streamlines processes and strengthens customer relationships. It features automated task generation, smart email integrations, personalized sequences, and intuitive pipeline management. By consolidating lead collection, deal tracking, account management, and post-sales activities into one interface, it shortens sales cycles and improves collaboration.

Monday Dev is a centralized hub for software development teams, managing product planning, agile sprints, bug tracking, and release workflows. It integrates with GitHub and Slack, automates repetitive tasks, and provides customizable sprint boards with roadmap planning. Real-time collaboration and analytics expose bottlenecks, improve productivity, and accelerate launches.

Monday Service is an AI-driven Enterprise Service Management platform unifying service operations across IT, HR, customer support, and other functions. It automates ticket classification, routing, and resolution with advanced AI. Customizable workflows, a self-service portal, integrated knowledge bases, and real-time analytics dashboards optimize efficiency and track service trends proactively.

Monday DB 2.0 is a scalable data infrastructure supporting up to 100,000 items per board and 500,000 items per dashboard. It delivers real-time data processing, advanced queries, and seamless integration across the monday ecosystem. This architecture removes performance constraints and allows enterprises to manage complex projects at scale.

Main Products Performance in the Last Quarter

Monday Work Management

Core growth engine powering the move upmarket. Q3 delivered $317M revenue, up 26% YoY, with platform momentum supported by 100,000+ net customer adds and 500,000+ paying customers. Upmarket motion kept accelerating across $50K, $100K, and $500K ARR cohorts, improving expansion quality and retention economics, with overall NDR at 111%. Top-of-funnel in SMB/mid-market stayed choppy in paid search, followed by stabilization late in the quarter; management cited volatility in Google performance and a deliberate shift toward higher-quality pipeline with longer conversion cycles.

Monday CRM

CRM crossed $100M+ in ARR in under two years, with ongoing traction especially in SMB and mid-market. Largest wins increasingly include CRM seats as part of multi-product deployments, including a 5,000-seat European logistics customer with 1,500 CRM seats in a $1M+ deal. CRM growth is being positioned as a cross-sell multiplier rather than a standalone motion, with bundling designed to shorten time-to-value and increase attach.

Monday Dev

Dev is positioned inside the new bundled platform strategy alongside Work Management, CRM, and Service, intended to deliver a unified deployment and drive cross-sell. Management framed the opportunity as underpenetrated: only ~6% of customers currently consume more than one product, leaving significant expansion runway as Dev gets pulled into broader platform deals. Commentary emphasized pipeline quality and multi-product momentum, with limited standalone Dev-specific KPIs disclosed on the call.

Monday Service

Service is highlighted as an early standout. Product is ~9 months into market and already showing stronger enterprise pull, with average Service customer size running at roughly 2x other products. Service is also part of bundle packaging, intended to accelerate adoption in common Work Management + Service workflows and expand seat footprint inside larger accounts.

Monday Campaigns

AI-powered Campaigns launched in September within CRM, reinforcing a connected sales + marketing suite. Management framed Campaigns as a catalyst for CRM adoption and a driver of multi-product value, supported by an expanding AI feature set and growing customer appetite for integrated workflows. No separate revenue contribution was disclosed, but Campaigns was positioned as a key CRM accelerant going into 2026.

Monday Vibe

Vibe is the breakout AI workflow builder. Since gradual release in July, customers created 60,000+ apps in a few months, with rapid enterprise adoption driven by secure, scalable deployment on monday.com infrastructure and granular permissions. Customers are using Vibe to replace point solutions fast: one regulated European insurer avoided a $150,000 third-party software purchase by building a better internal reporting tool in ~20 minutes; a large retailer solved a year-long reporting gap in <30 minutes. Monetization is being shaped via a new tiered model, ranging from unlimited free build/test access to paid tiers scaling with usage; management called Vibe the strongest near-term AI monetization opportunity.

Monday Magic

Magic sits inside the broader AI product stack alongside Sidekick and agents, framed as part of increasing AI engagement across the base. Management emphasized accelerating enthusiasm and adoption, with monetization treated as incremental near term and more meaningful over time through higher platform stickiness and retention economics rather than immediate revenue step-ups.

Agent Factory

Agent Factory is a new AI product enabling customers to design and manage intelligent agents for complex workflow automation, positioned as a standalone solution with flexible, consumption-based pricing. Agents are described as embedded “team members” handling operational tasks like CRM updates, email sends, and follow-ups. Management sees Agent Factory as a potential door-opener into new customer audiences, while also expanding automation value inside existing accounts.

Innovations and product updates

Multi-product execution is outpacing internal milestones: new products now represent 10%+ of total ARR, beating the 2025 target ahead of schedule. Bundles launched across three common combinations, including Work Management with CRM, Service, and Dev, offering commercial advantage and faster deployment for repeatable use cases. AI packaging is being simplified with an AI credit system rolling out in Q4, built from customer feedback to improve transparency and scaling.

6. Market Leader

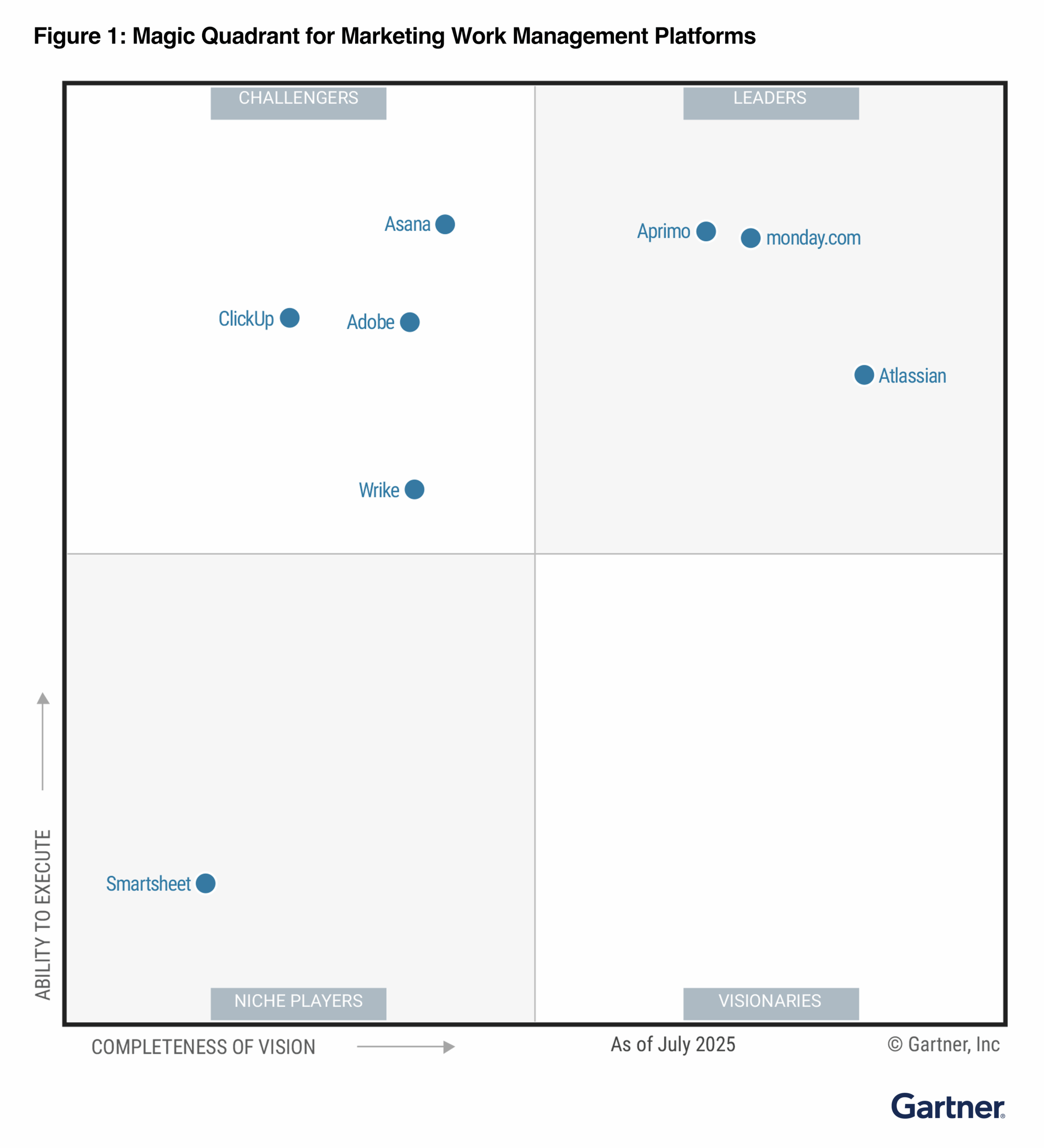

Monday was named a Leader in the 2025 Gartner Magic Quadrant for Marketing Work Management Platforms, becoming the only platform recognized as a Leader across three 2025 Gartner Magic Quadrant reports for the second consecutive year. The platform differentiates through deeply embedded AI that automates execution, accelerates decisions, and delivers enterprise-grade visibility across marketing and cross-functional workflows in a single connected work hub.

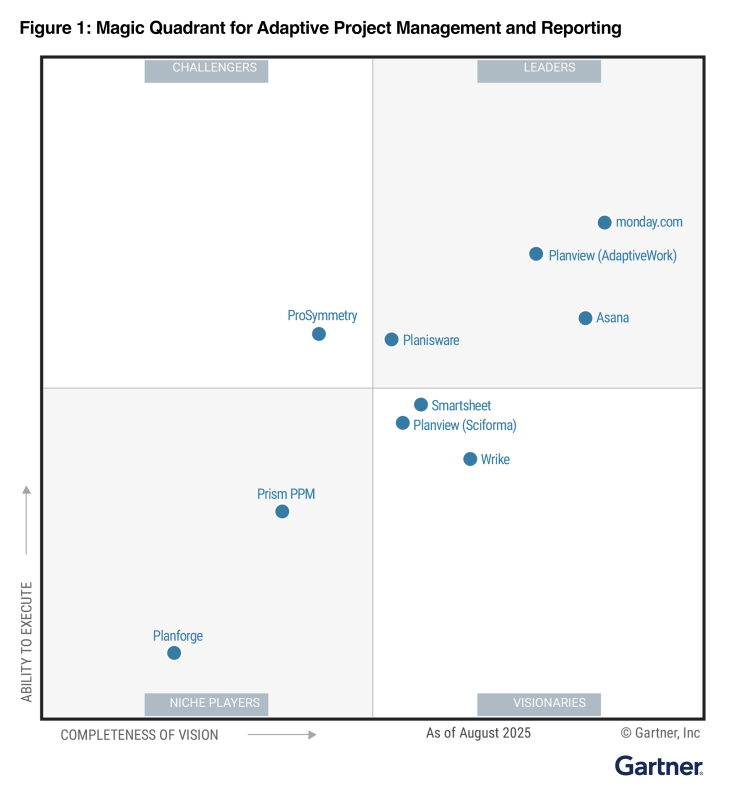

Monday was named a Leader in Gartner’s 2025 Magic Quadrant for Adaptive Project Management and Reporting for the fourth consecutive year. The platform expanded strategic alignment, resource management, and AI-driven risk prediction, strengthening its position as a top enterprise project management solution.

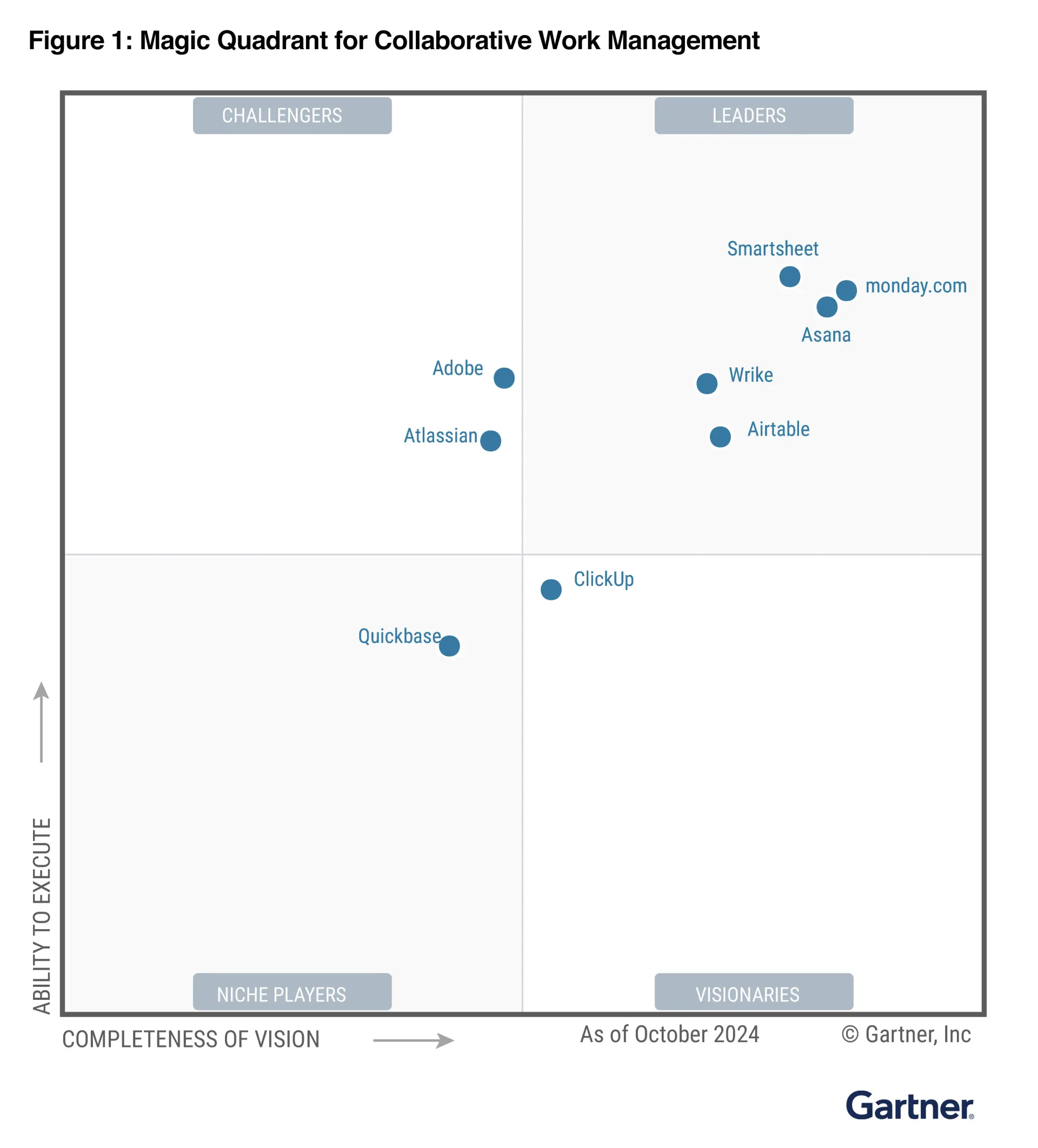

Monday has established itself as a Leader in the Gartner Magic Quadrant for Collaborative Work Management for the second consecutive year in 2024. The company achieved the furthest position in ‘Completeness of Vision’ among all evaluated vendors, demonstrating its strategic market positioning and product innovation capabilities.

Monday was named a Strong Performer in the 2025 Forrester Wave for Collaborative Work Management Tools for the Enterprise. The evaluation covered 10 leading platforms, including Asana, Airtable, and Wrike.

The Forrester report recognized Monday’s low-code/no-code platform as built for enterprise scalability. Its flexible architecture enables dynamic workflow adjustments. The multi-product ecosystem supports end-to-end work management, not just task tracking. The visual interface lowers adoption barriers while preserving advanced functionality for complex enterprise environments.

7. Customers

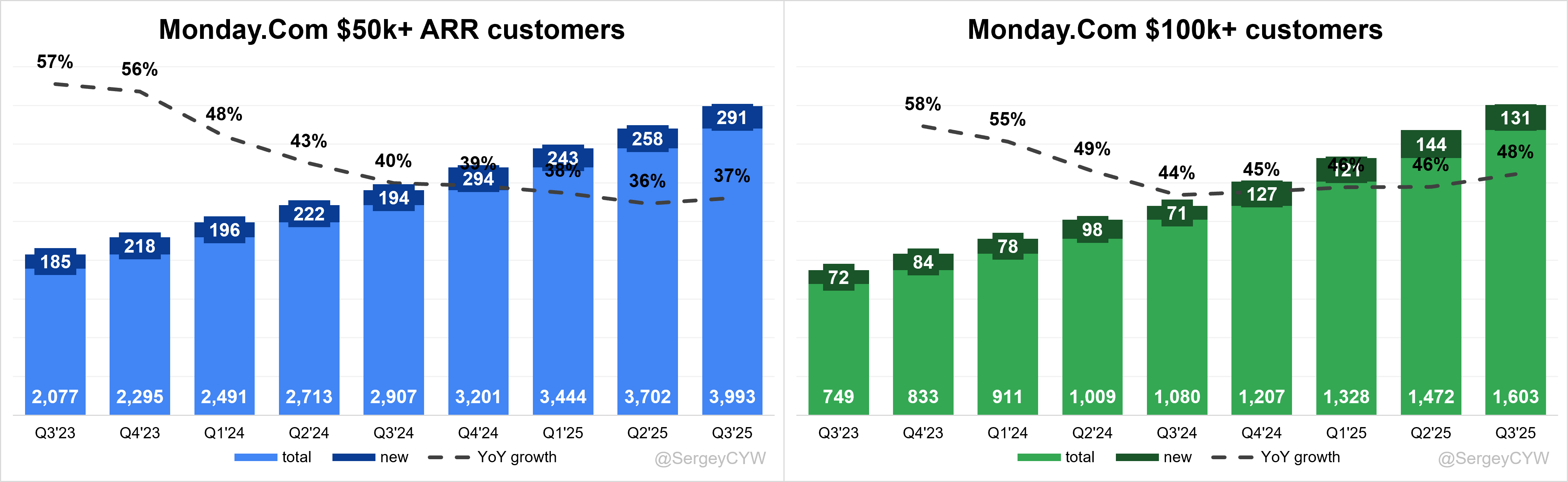

$MNDY added 291 customers with ARR over $50K, representing +37% YoY growth, up from +36% in Q2, and marking a near-record quarterly addition. The company also added 131 customers with ARR over $100K, delivering +48% YoY growth, with growth continuing to accelerate.

Сustomer growth outpacing revenue growth—a positive signal for future expansion and market demand.

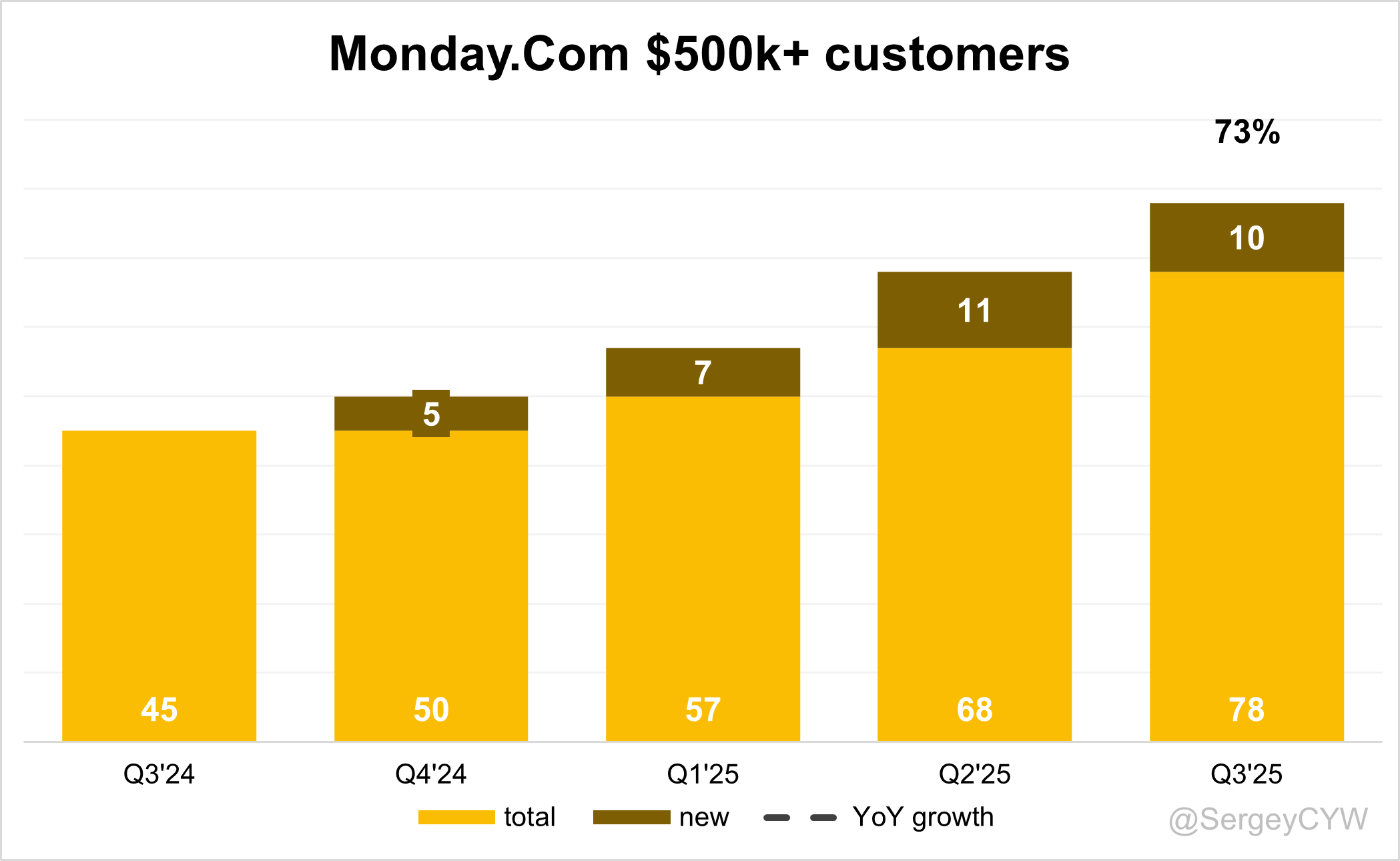

Customers with ARR over $500K grew +73% YoY, with 10 new customers added in Q3.

Large Customer Wins

Monday expanded its footprint with several seven-figure transactions. Each originated as modest $50k land-and-expand deals three to four years ago. The velocity of expansion underscores the company’s growing credibility in complex enterprise environments and the robustness of its up-market motion.

One of the most notable wins came from a European logistics leader that grew to roughly 5,000 seats across CRM, Work Management, and Service. The customer now runs frontline operations, service flows, and sales processes on monday.com and crossed more than $1 million in annual contract value during the quarter. The scope of deployment illustrates both horizontal adoption and cross-product penetration.

A global technology company also expanded materially. It employs monday.com across roughly ten departments and relies on the platform to manage its full M&A pipeline. The relationship began small and expanded into a strategic, multi-team installation. The account has grown into a seven-figure ARR customer and reflects deep entrenchment inside critical workflows.

These patterns show a repeatable trajectory: mid-sized initial deployments evolving into multi-product, multi-department contracts with expanding seat counts and longer terms.

Customer Success Stories

Enterprise demand for AI-powered customization accelerated after the release of Monday Vibe. A highly regulated European insurance firm used Vibe to replace a legacy reporting tool priced at roughly $150,000. Internal teams built a replacement in less than 20 minutes, deployed it immediately, and realized higher utility than the third-party system they had planned to buy. The speed-to-value strengthened overall platform stickiness.

A major retailer experienced a similar outcome. The company had spent a year trying to close a workflow reporting gap. Using monday.com AI capabilities and the Vibe platform, the team constructed a working solution in under 30 minutes. Rapid resolution of a long-standing operational pain point highlighted the platform’s adaptability and positioned monday.com as a core innovation engine within the customer’s stack.

Sales teams echoed this sentiment. Multiple organizations reported building bespoke applications on Vibe during the Elevate user events and unlocking immediate productivity gains. The impact reinforced monday.com’s evolution from a work management platform into an AI-enabled operating system capable of absorbing adjacent software categories.

8. KPI.

Retention

$MNDY Monday’s Net Dollar Retention (NDR) is at 111%, slightly down from 112% in Q1. For customers with ARR over $50K, retention increased to 117%, and for $100K+ customers, it is also 117%. While retention remains strong, it is slightly below the ~120% median for SaaS companies I track.

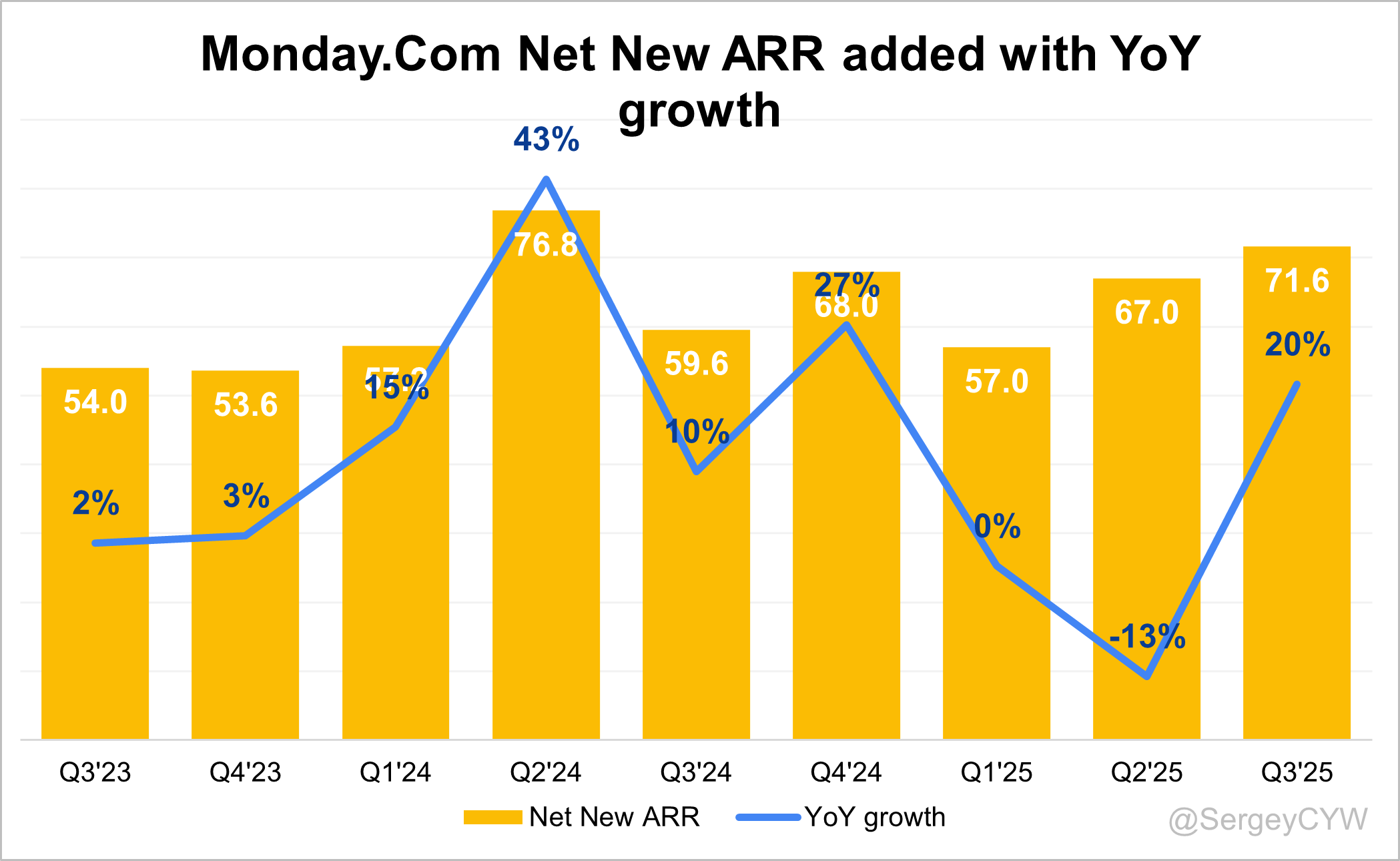

Net new ARR

$MNDY Monday added $71.6M in net new ARR in Q3 2025, up +20% YoY. This addition is above Q3 2024 and 2023 levels, reflecting steady growth.

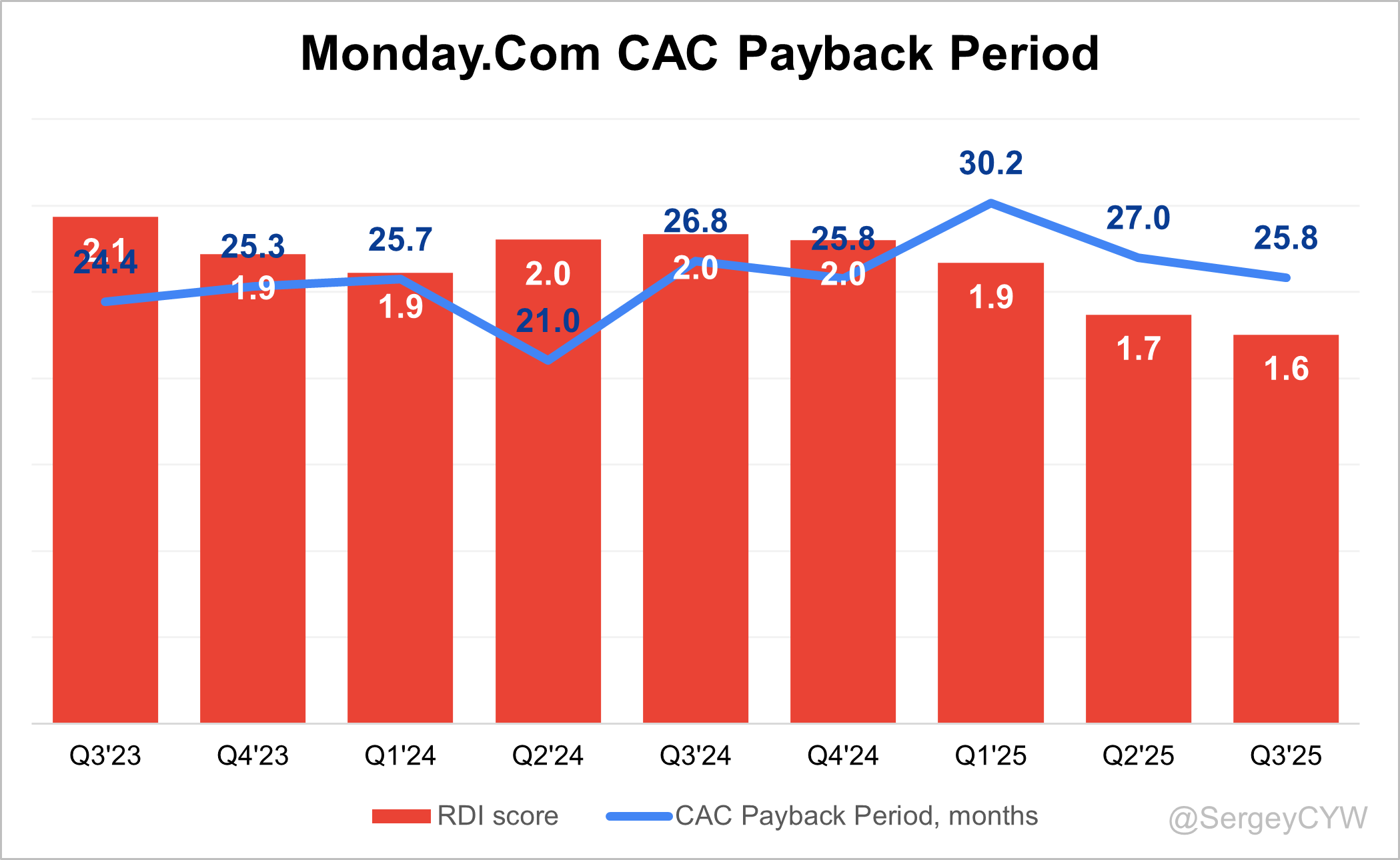

CAC Payback Period and RDI Score

$MNDY Monday’s return on S&M spending improved to 25.8, which is worse than the SaaS median of 21.1.

However, the R&D Index (RDI Score) in Q3 slightly declined to 1.6, but it remains well above the SaaS median of 1.1 and significantly higher than the industry median of 0.7. This highlights strong and efficient investment in innovation.

An RDI Score above 1.4 is indicative of best-in-class performance. The industry median of 0.7 highlights the importance of efficient R&D investment.

Key Metrics

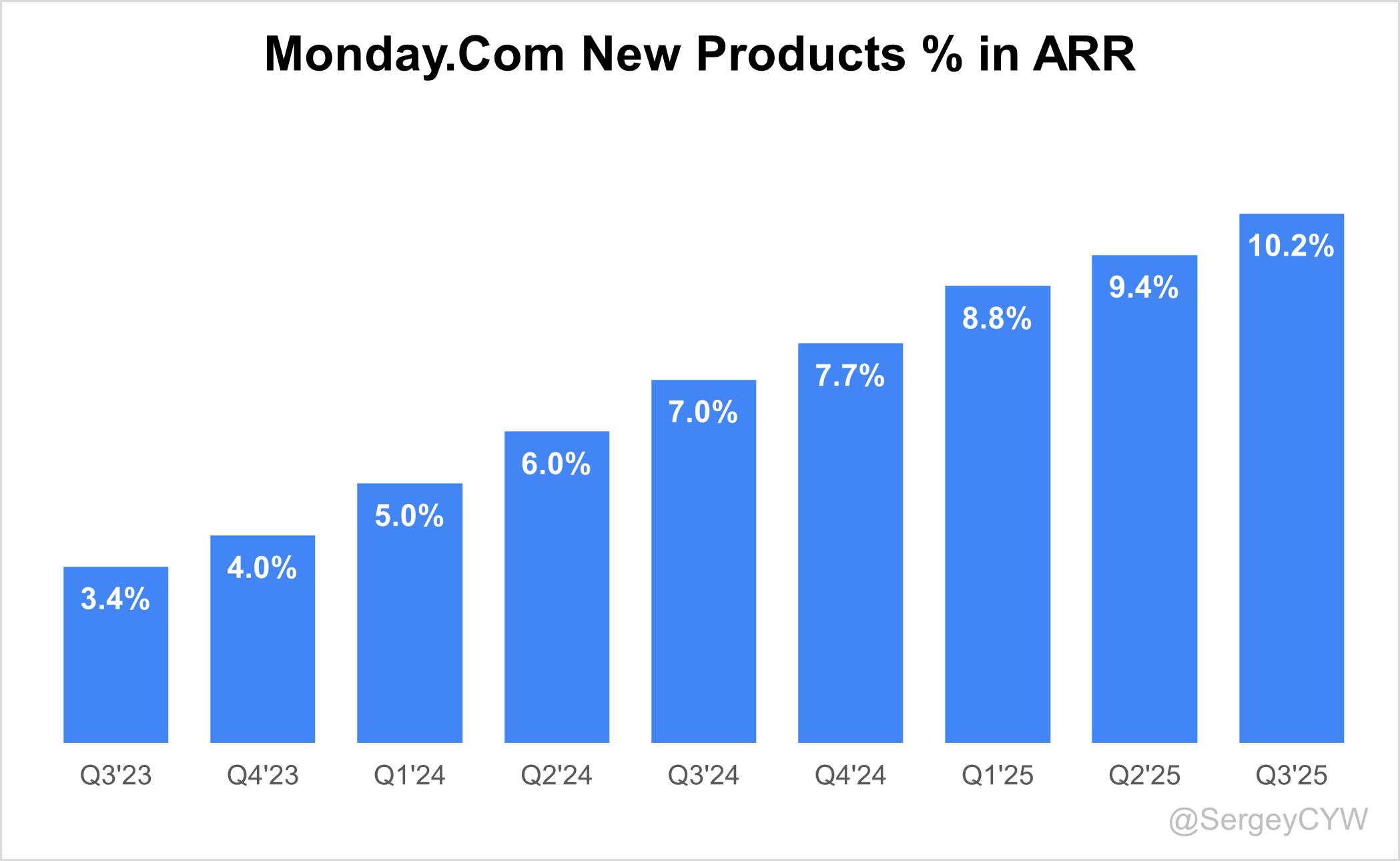

In Q3 2025, $MNDY stopped reporting separate metrics for CRM, developer, and service accounts. After consolidating new products, Monday began reporting the share of new products in total ARR. In Q3, new products reached 10.2% of total ARR, increasing by +3.2 percentage points YoY.

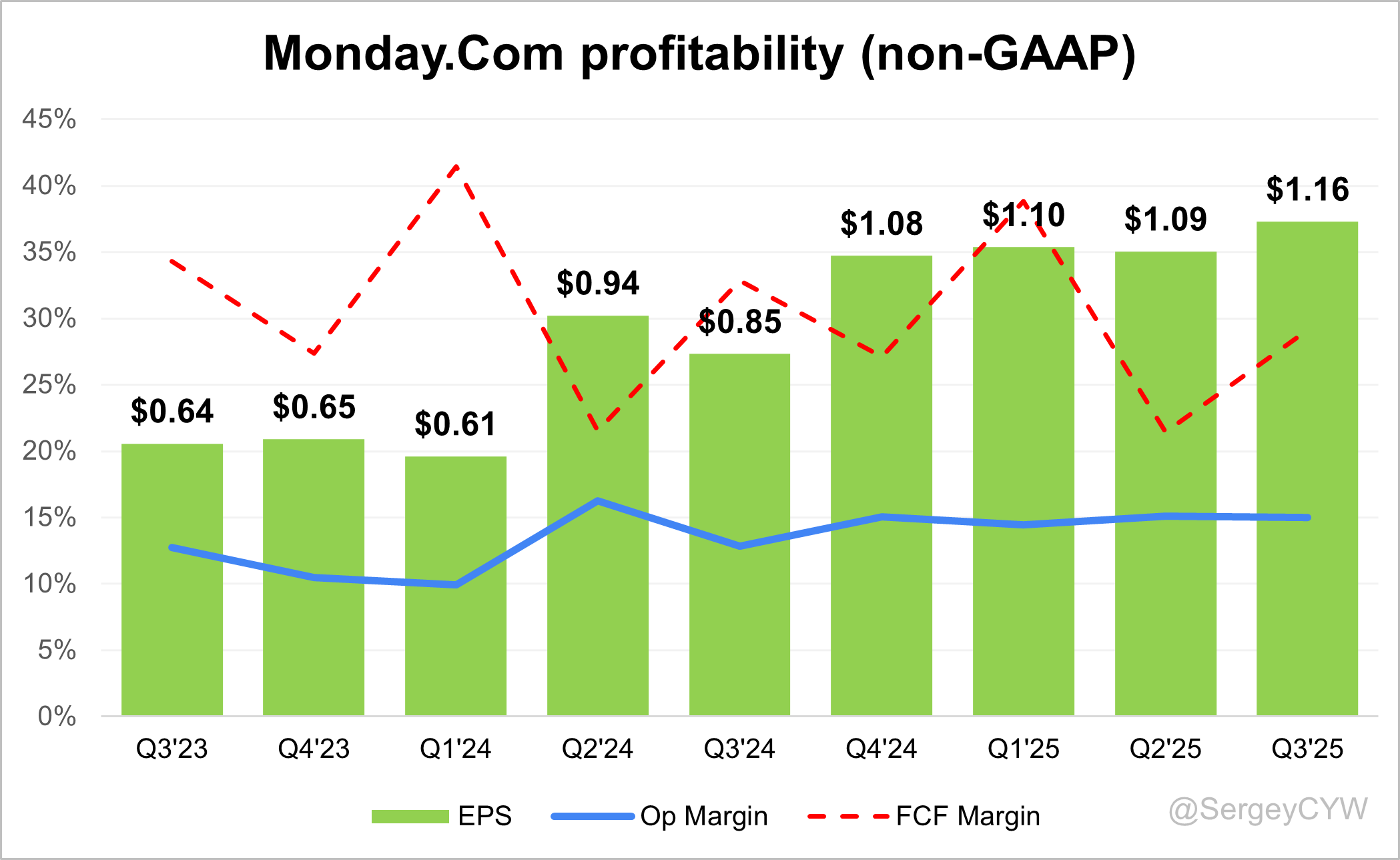

Profitability

Over the past year, $MNDY Monday margins have changed:

Gross Margin slightly decreased from 90.4% to 89.6%.

Operating Margin increased from 12.8% to 14.9%.

Free Cash Flow (FCF) Margin slightly decreased from 32.8% to 29.1%.

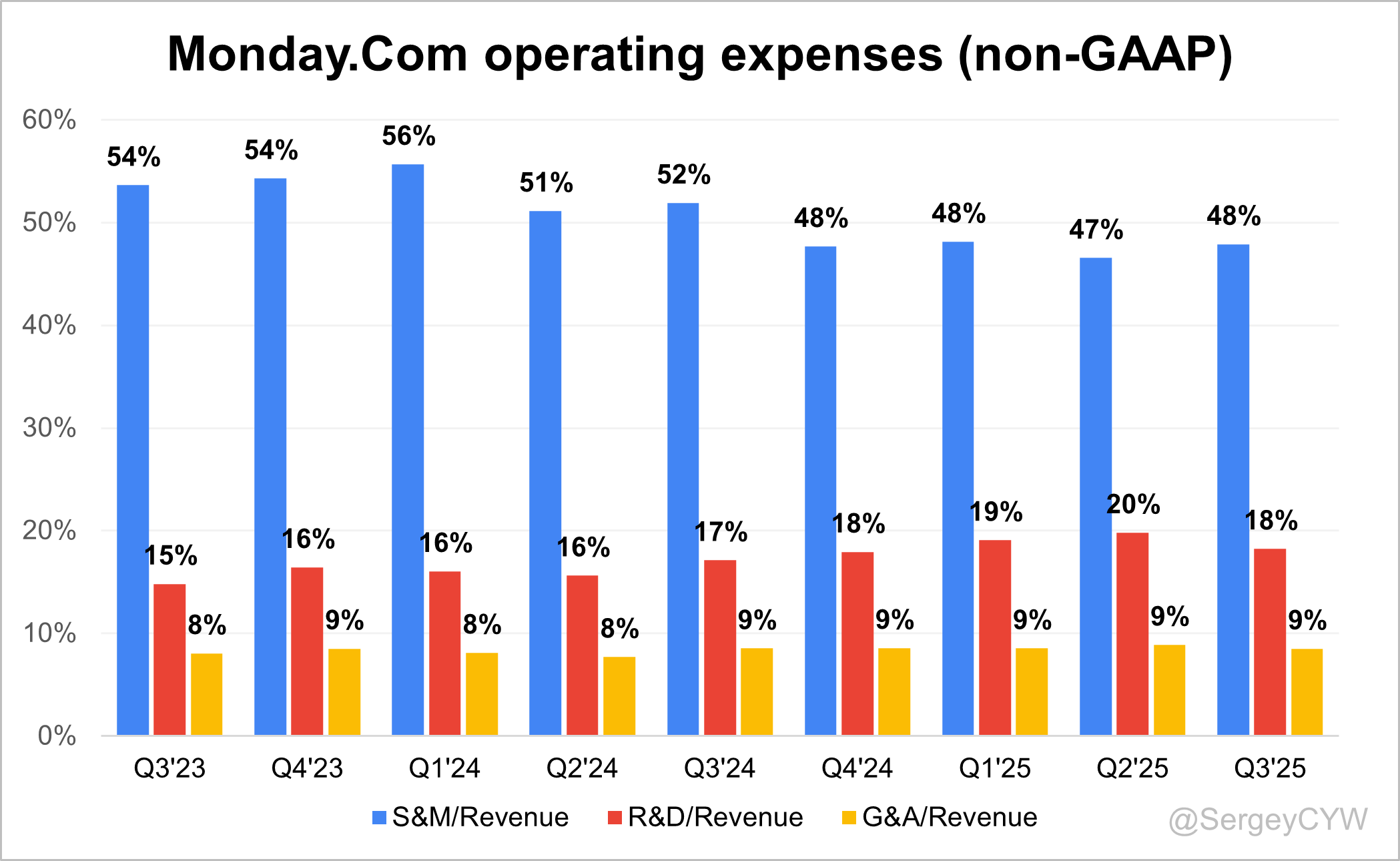

Operating expenses

$MNDY Monday’s Non-GAAP operating expenses have gradually decreased due to a reduction in Sales & Marketing (S&M) spending, which declined from 52% two years ago to 48%.

R&D expenses have increased and remain high at 18%, reflecting the company’s ongoing investment in future growth through product enhancements and updates.

General & Administrative (G&A) expenses have remained steady at 9% over the past two years.

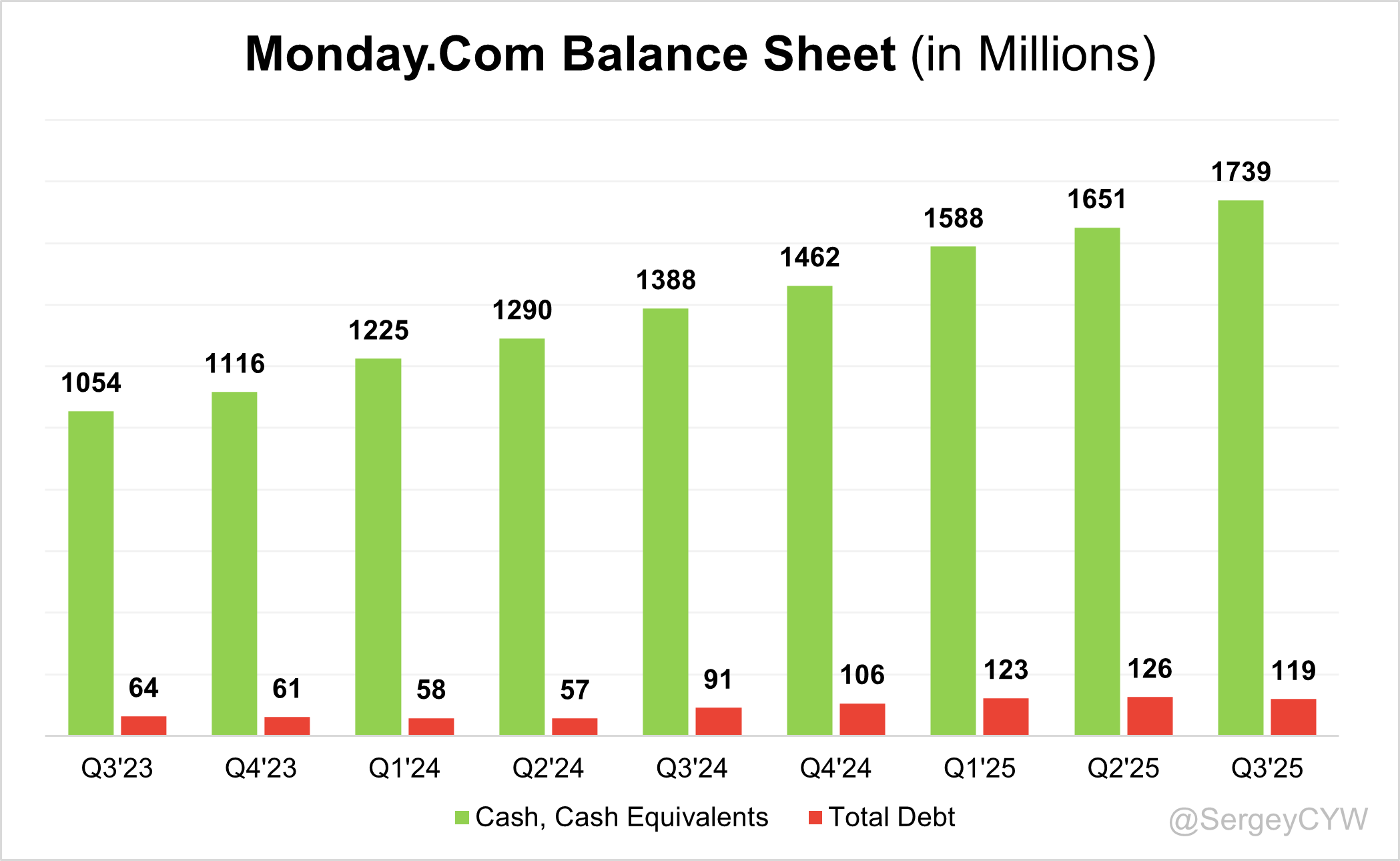

Balance Sheet

$MNDY Balance Sheet: Total debt stands at $119M, while Monday holds $1,739M in cash and cash equivalents, far exceeding its debt and ensuring a healthy balance sheet with virtually no debt.

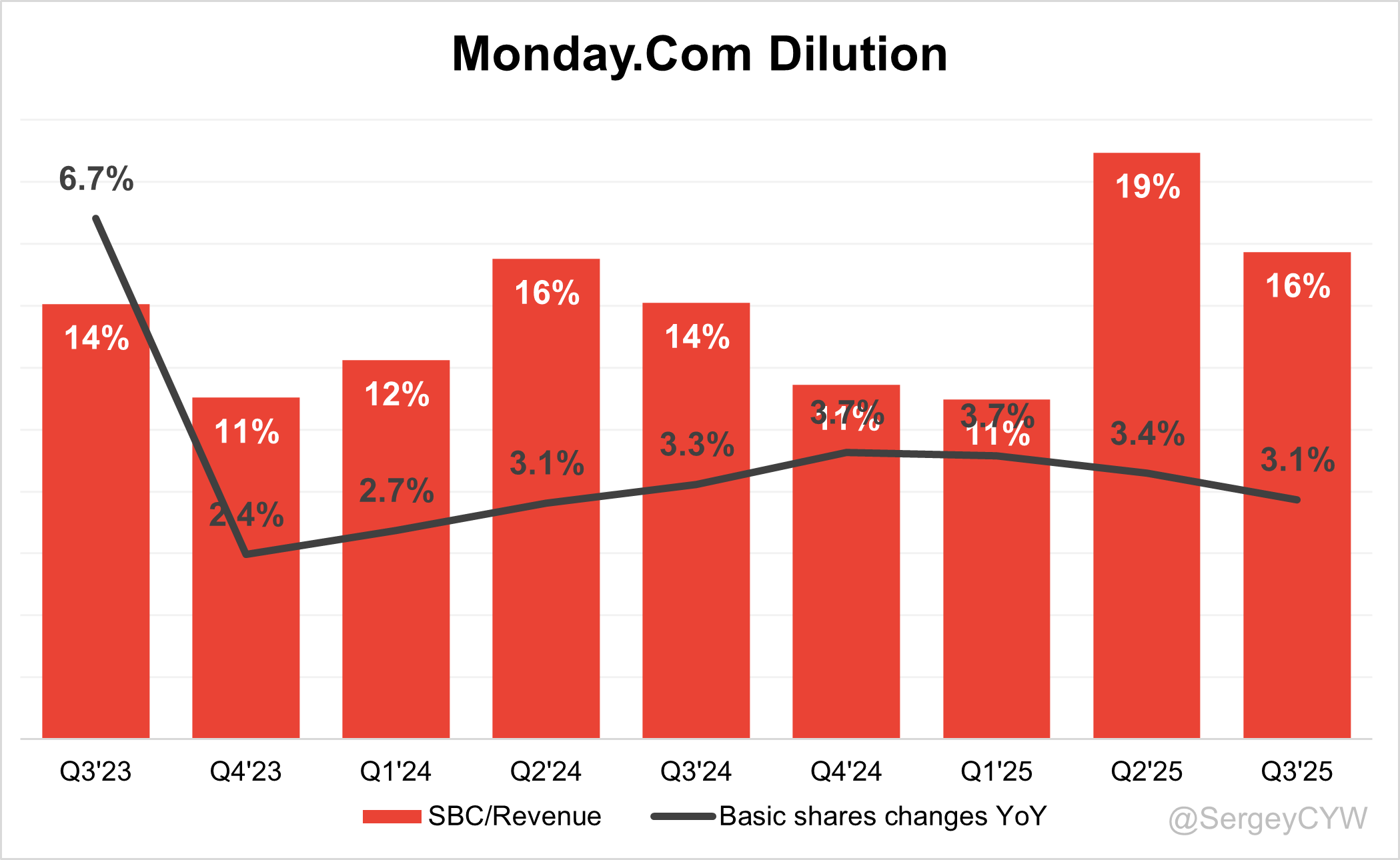

Dilution

$MNDY shareholder dilution improved as stock-based compensation (SBC) declined to 16% of revenue, down from 19% in Q2, and now slightly below peers among high-growth SaaS companies.

While dilution remains elevated, it is under control: the weighted-average basic shares outstanding grew 3.1% YoY, improving from 3.7% in Q1 2025.

9. Conclusion

$MNDY Monday’s revenue growth continued to slow, reaching +26.3% YoY in Q3 .

Leading Indicators

Billings growth came in at +23.7%, slightly below revenue growth, while RPO growth accelerated to +36.3%, growing faster revenue growth.

Net new ARR additions at record level, up 20.0% YoY.

Strong additions of total and large customers.

New products share increased to 10.2% in ARR.

Key Metrics

Net Dollar Retention (NDR) at 111%, for $50k+ large customers NDR increased to 117%.

CAC Payback Period at 25.8 months.

RDI Score at 1.6, which is above the median among SaaS peers I track.

Management’s revenue guidance for the next quarter implies +24.7% YoY growth, assuming a similar 1.2% beat as in Q3, signaling further revenue growth deceleration. This slowdown is a key investor concern, driven by fears that agentic AI could be disruptive to the business. Management attributed the softer guidance to longer enterprise deal cycles and timing effects from the rebalanced go-to-market model.

For Monday, the key inflection point will be stabilizing revenue growth. Factors supporting potential stabilization include near-record customer additions, accelerating growth in larger customers, and RPO growth accelerating in Q3, all of which point to improving forward demand. While management stopped reporting CRM, Dev, and Service account additions, they now disclose the share of new products in ARR, which rose to 10.2% (+3.2pp YoY) — indicating that new products are growing significantly faster than overall revenue.

Valuation sits at the low end of Monday’s historical forward EV/Sales range and looks undervalued relative to peers, especially given its top-tier revenue growth. Analysts currently expect Monday to deliver one of the highest revenue growth rates among CRM companies in 2026. It’s also worth noting that CRM stocks broadly underperformed in 2025, with $MNDY shares down 39%.

R&D/Revenue spending continues to rise, which I view as a positive signal for long-term competitive strength. Monday is strengthening its competitive position and is recognized as a leader in multiple Gartner quadrants.

While competition in CRM is intense and investors expect pressure from agentic AI, Monday is successfully leveraging AI itself. Management noted that AI agents are built directly into the platform’s secure architecture, making them auditable and governed, unlike external copilots.

Management expects Monday’s TAM to reach $225B by 2028, growing at a 12% CAGR. I will continue to monitor revenue growth trends and new product growth. The key catalyst will be stabilization in revenue growth, which could reverse negative sentiment. At current levels, valuation multiples look very attractive, though risks remain.

After Q3 earnings, the stock dropped 15.8%, at which point I slightly increased my position. $MNDY now represents 5.4% of my portfolio.

Thank you for reading!

Follow me for more frequent updates on X/Twitter and Threads, and on LinkedIn. For visual infographics, check out Instagram, and for portfolio changes, follow me on SavvyTrader.

Disclaimer: This earnings review is for informational purposes only and does not constitute financial, investment, or trading advice.

I'm good don't worry 😌

Great article. However, I cannot let myself invest in companies founded in or tied to that country.