Tesla Q2 2024 Earnings Analysis

Dive into $TSLA Tesla’s Q2 2024 earnings with review of financial performance, key metrics, operating expenses, dilution, customer growth, future outlook

Demand

↘️Cars Delivered (443,956, -4.8% YoY) beat est by 1.4%

↗️S/X and others Delivered (21,551, +12.0% YoY)

↘️3/Y Delivered (422,405, -5.5% YoY)

↘️Cars Produced (410,831, -14.4% YoY)

↗️S/X and others Produced (24,255, +24.0% YoY)

↘️3/Y Produced (386,576, -16.0% YoY)

↘️Global vehicle inventory 18 days of supply, -10 QoQ

Financial Results

↗️$25,500M rev (+2.3% YoY, -8.7% LQ) beat est by 3.1%

↘️GM (18.0%, -0.2%pp YoY)🟡

↘️Adjusted EBITDA Margin (14.4%, -4.3%pp YoY)🟡

↘️Operating Margin (6.3%, -3.3%pp YoY)🟡

↗️FCF Margin (5.3%, +1.2%pp YoY)

↘️Net Margin (5.8%, -5.0%pp YoY)🟡

↘️EPS $0.52 missed est by -16.1%

Revenue By Segments

Automotive

↘️$19,878M Total automotive Revenue (-6.5% YoY, 78.0% of total Revenue)

↘️Automotive GM excl. regulatory credits (14.6%, -3.5%pp YoY)🟡

Energy generation and storage

↗️$3,014M Energy generation and storage Revenue (+99.7% YoY, 11.8% of total Revenue)

↗️Energy GM (24.6%, +6.1%pp YoY)

Services

↗️$2,608M Services and other Revenue (+21.3% YoY, 10.2% of total Revenue)

↘️Services GM (6.4%, -1.3%pp YoY)🟡

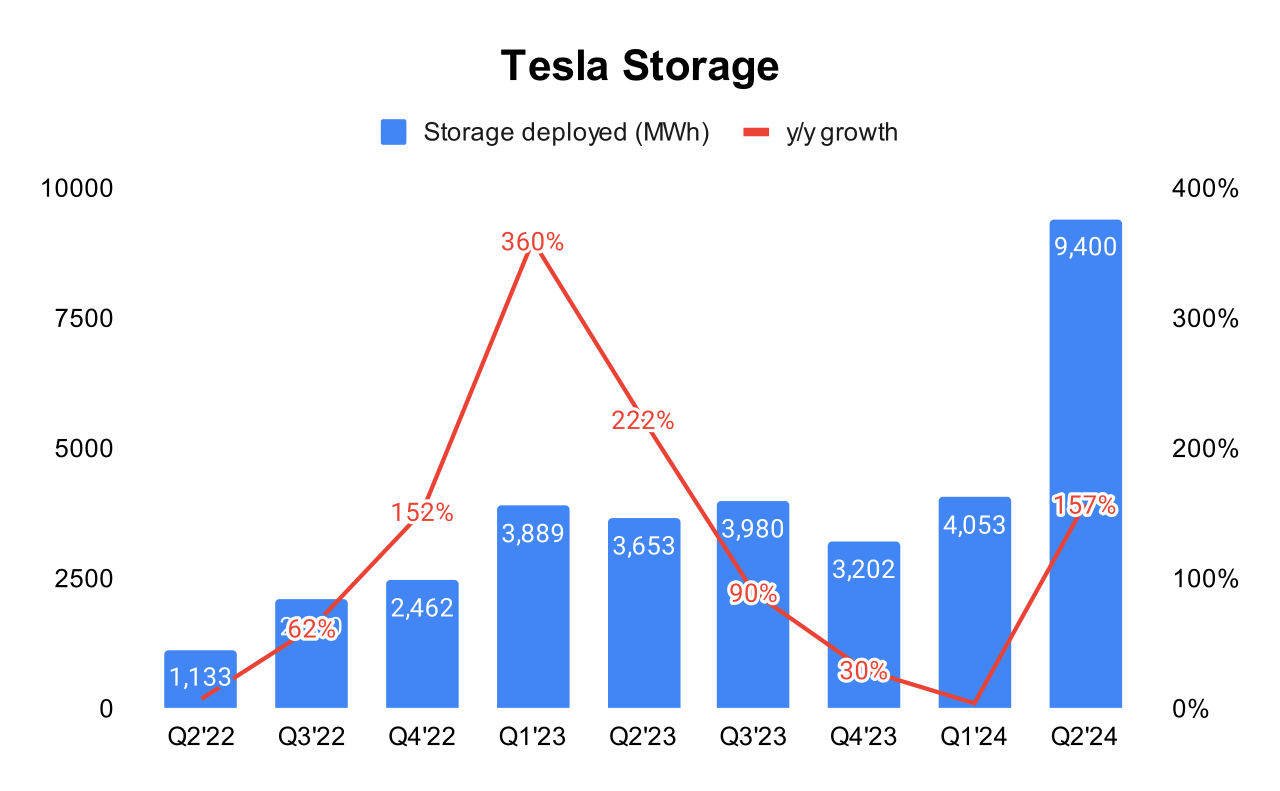

↗️9,400 MWh Storage deployed (+157.0% YoY)

➡️6,473 Supercharger stations (+23.0% YoY)

↗️2,270 CAPEX (+15.0% YoY)

Operating expenses

↘️S&M+G&A/Revenue 5.0% (6.5% LQ)

↘️R&D/Revenue 4.2% (5.4% LQ)

Dilution

↘️SBC/rev 15%, -17.5%pp QoQ

↗️Basic shares up 0.6% YoY, +0.2%pp QoQ🟢

↘️Diluted shares up 0.1% YoY, -0.4%pp QoQ🟢

Key points from Tesla’s Second Quarter 2024 Earnings Call:

EV Market Dynamics:

Tesla observed a significant adoption of EVs but faced challenges due to competitors entering the market and heavily discounting their EVs. This situation is seen as short-term by Tesla.

Despite temporary setbacks from price cuts by competitors, Tesla remains confident about the long-term transition to electrified transport, including not just cars but also aircraft and boats.

Auto Gross Margin:

In response to sustained high interest rates, Tesla introduced competitive financing options which affected revenue per unit in Q2 and are expected to continue into Q3.

Affordable Model:

Tesla plans to deliver a more affordable model in the first half of the next year, focusing on broadening its market reach.

Cybertruck Production Ramp:

Tesla is actively ramping up Cybertruck production, with advancements in 4680 battery cell production playing a crucial role.

Inventory and Delivery:

Tesla's strategy includes maintaining a balance between production output and delivery capabilities, focusing on maximizing efficiency and customer satisfaction.

Full Self-Driving (FSD) Enhancements:

Tesla rolled out FSD version 12.5, which integrates highway and city driving stacks and contains 5x the parameters of the previous version, promising major improvements in performance.

Elon Musk emphasized that FSD and the transition to unsupervised driving will be a significant demand driver for Tesla, expecting unsupervised capabilities to be achieved possibly by the end of the year or next year.

Optimus and Robotaxi Plans:

Tesla is integrating Optimus robots in its factories, with production for external customers planned to start in 2026 after internal use and refinements.

The Robotaxi product reveal has been delayed to October to allow for enhancements. Tesla envisions its full fleet potentially transitioning to Robotaxi service, emphasizing a software-driven, instant scale for deployment.

Energy Business:

The energy segment saw its fastest growth, driven by record revenues and profits, particularly from the deployment of energy storage systems which more than doubled.

Tesla is expanding production capacity in its U.S. factory and constructing a new Megapack factory in China, aiming to double or potentially triple output.

The current challenge is more about meeting demand than increasing production, as the market appetite for Tesla's energy solutions is significant.

Financial Health:

Tesla remains financially robust with strong cash reserves and positive free cash flow, despite ongoing investments and expansions.

Mexico Gigafactory:

The future of the Mexico Gigafactory is uncertain due to potential political changes in the U.S., specifically concerning tariffs on vehicles produced in Mexico as mentioned by former President Trump.

Tesla is pausing significant investments in the Mexico Gigafactory until the political landscape regarding tariffs is clearer, focusing instead on increasing capacity at existing factories.

Future Outlook:

Tesla continues to focus on innovation, affordability, and expanding its product line while maintaining market leadership in the EV and energy sectors. Musk remains optimistic about Tesla’s role in transforming energy systems and transportation globally.

Management comments on the earnings call.

EV Market:

Elon Musk: "We saw large adoption exploration in EVs, and then a bit of a hangover as others struggle to make compelling EVs... We don’t see this as long-term issue, but really -- fairly short-term."

Optimus and Robotaxi Plans:

Elon Musk: "The big -- really by far the biggest differentiator for Tesla is autonomy... we are on track to develop -- to deliver a more affordable model in the first half of next year."

Cybertruck Production Ramp:

Lars Moravy: "Yes, 4680 production ramp strongly in Q2, delivering 51% more cells than Q1 while reducing COGS significantly... We're on track for production launch with dry cathode in Q4."

Energy Business:

Elon Musk: "For the energy business, this is growing faster than anything else. This is -- we are really demand constrained rather than production constrained."

Product Roadmap:

Elon Musk: "We won't get too much into the product roadmap here, because that is reserved for product announcement events. But we are on track to develop -- to deliver a more affordable model in the first half of next year."

Future Outlook:

Elon Musk: "We are changing the energy system, how people move around, how people approach the economy. The undertaking is massive, but I think the future is incredibly bright. I really just can't emphasize just the importance of autonomy for the vehicle side and for Optimus."

Thoughts on Tesla ER $TSLA:

🟢Pros:

+ Cybertruck is in the ramp-up phase (S/X and others produced increased +24% YoY).

+ 4680 production increased about 51% sequentially.

+ Next-generation vehicle production expected to start in the first half of 2025.

+ Tesla Bot Optimus and FSD could be company growth drivers in the future.

+ Global vehicle inventory decreased to 18 (delivered 33,125 more than produced in Q2).

+ Energy generation and storage revenue increased +99.7% YoY; gross margin increased by +6.1 pp YoY.

+ Services Revenue increased by +21.3% YoY.

+ FCF margin is 5.3%, +1.2%pp YoY.

🔴Cons:

- Automotive revenue decreased by 6.5% YoY.

- Tesla cars delivered decreased by 4.8% YoY.

🟡Neutral:

+- Auto gross margin declined to 14.6%. Tesla introduced competitive financing options which affected revenue per unit in Q2 and are expected to continue into Q3.

+- Gross margin, operating margin, and net margin are declining.