Tesla Q1 2024 Earnings Review

$TSLA Q1'24 Results:

Demand

↘️Cars Delivered (386,810, -8.5% YoY) missed est by -10.3%🔴

↗️S/X and others Delivered (17,027, +59.0% YoY)

↘️3/Y Delivered (369,783, -10.3% YoY)

↘️Cars Produced (433,371, -1.7% YoY)

↗️S/X and others Produced (20,995, +8.0% YoY)

↘️3/Y Produced (412,376, -2.1% YoY)

↗️Global vehicle inventory 28 days of supply, +13 QoQ🟡

Financial Results

↗️$21,301M rev (-8.7% YoY, +3.5% LQ) missed est by 4.7%🔴

↘️GM (17.4%, -2.0%pp YoY)🟡

↘️Adjusted EBITDA Margin (15.9%, -2.4%pp YoY)🟡

↘️Operating Margin (5.5%, -5.9%pp YoY)🟡

↘️FCF Margin (-11.9%, -13.8%pp YoY)🟡

↘️Net Margin (5.3%, -5.5%pp YoY)🟡

↘️EPS $0.45 missed est by -11.8%

Revenue By Segments

Automotive

↘️$17,378M Total automotive Revenue (-12.9% YoY, 81.6% of total Revenue)

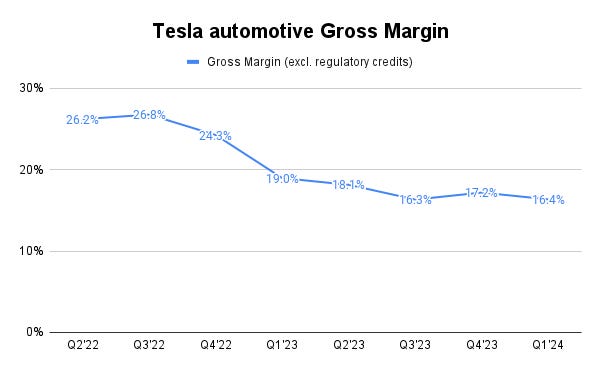

↘️Automotive GM excl. regulatory credits (16.4%, -2.6%pp YoY)🟡

Energy generation and storage

↗️$1,635M Energy generation and storage Revenue (+6.9% YoY, 7.7% of total Revenue)

↗️Energy GM (24.6%, +13.7%pp YoY)🟢

Services

↗️$2,288M Services and other Revenue (+24.6% YoY, 10.7% of total Revenue)

↘️Services GM (3.5%, -3.8%pp YoY)🟡

➡️4,053 MWh Storage deployed (+4.0% YoY)

↗️6,249 Supercharger stations (+26.0% YoY)

↗️2,773 CAPEX (+32.0% YoY)

Operating expenses

↗️S&M+G&A/Revenue 6.5% (5.1% LQ)

↗️R&D/Revenue 5.4% (4.3% LQ)

Dilution

↘️SBC/rev 32%, -1.6%pp QoQ

↘️Basic shares up 0.5% YoY, -0.2%pp QoQ🟢

↘️Diluted shares up 0.5% YoY, -0.1%pp QoQ🟢

Key points from Tesla’s First Quarter 2024 Earnings Call:

Financial Performance:

Tesla announced record profitability in their energy business due to high Megapack deployments. However, auto GM declined from 17.2% to 16.4% due to factors like seasonal revenue decline and costs related to the ramp-up of Model 3 in Fremont.

Cybertruck Ramp:

Cybertruck production reached 1,000 units per week, marking significant progress since the start of production (SOP) late last year. Continued efforts are focused on reducing costs and improving quality despite challenges from new technologies and some supplier limitations. Cybertruck production and the ramp of the third of four lines in Phase 1 are expected to support future increases in production volume.

Vehicle Production and Sales:

Tesla is facing challenges due to a general pullback in EV adoption globally. Despite this, they continue to innovate, with updates to the Model 3 and anticipation of new, more affordable vehicle models using both new and existing platforms, expecting to increase production capacity to over 3 million vehicles.

Vehicle Inventory:

Tesla experienced an increase in inventory due to a mismatch between builds and deliveries, primarily influenced by seasonal demand fluctuations and external factors like disruptions.

The company expects the inventory build to reverse in Q2, returning to positive free cash flow as these mismatches are resolved.

Autopilot and Full Self-Driving (FSD):

Tesla has rolled out FSD Version 12, which is fully AI-driven. They've enabled it for all compatible cars in North America, covering about 1.8 million vehicles. Tesla claims improvements in FSD technology and has reduced the subscription price to $99 per month to boost accessibility and adoption. Tesla is in discussions with a major automaker to license its FSD technology.

AI and Computing Infrastructure:

Tesla has made significant advancements in AI training capabilities, with over 35,000 H100 GPUs currently operational and plans to increase this to 85,000 by the end of the year. Tesla emphasizes their AI inference efficiency, which they claim surpasses any other company.

Humanoid Robot Optimus:

Optimus is expected to start performing simple tasks in Tesla factories by the end of the year and may start external sales by the end of the next year. Elon Musk highlighted the potential value of Optimus, asserting it could surpass all of Tesla’s other ventures.

Regulatory Landscape for Autonomous Driving:

Tesla is optimistic about regulatory approval for unsupervised FSD in the U.S., influenced by the progress other autonomous car companies have made in gaining approvals.

Financial Strategies and Cost Management:

Despite a negative free cash flow of $2.5 billion due to inventory mismatches and high capital expenditures, Tesla expects positive cash flow in the coming quarters. They have also reduced their workforce to save costs, expecting savings of over $1 billion annually.

Future Outlook and Product Roadmap:

Tesla has accelerated its vehicle production roadmap. New models, are expected to be launched earlier than planned, potentially by early 2025 or even late 2024. These models will incorporate features from both the next generation platform and current platforms and will be manufactured on existing production lines, improving production efficiency.

Management comments on the earnings call.

Vehicle Inventory and Financial Strategies

Vaibhav Taneja: "We had negative free cash flow of $2.5 billion in the first quarter. The primary driver of this was an increase in inventory from a mismatch between builds and deliveries as discussed before, and our elevated spend on CapEx across various initiatives, including AI compute. We expect the inventory build to reverse in the second quarter and free cash flow to return to positive again."

Cybertruck Ramp

Lars Moravy: "4680 production increased about 18% to 20% from Q4 reaching greater than 1K a week for Cybertruck, which is about 7 gigawatt hours per year as we posted on X. We expect to stay ahead of the Cybertruck ramp with the cell production throughout Q2 as we ramp the third of four lines in Phase 1, while maintaining multiple weeks of cell inventory to make sure we're ahead of the ramp."

FSD

Elon Musk: "To make it more accessible, we've reduced the subscription price to $99 a month, so it's easy to try out."

Elon Musk: "Regarding FSD Version 12, which is the pure AI-based self-driving, if you haven't experienced this, I strongly urge you to try it out. It's profound and the rate of improvement is rapid."

Elon Musk: "We are making sure that we're being as efficient as possible in our training. It's not just about the number of H100s, but how efficiently they're used."

Future Car Delivery Expectations

Elon Musk: "No, I think we'll have higher sales this year than last year."

Elon Musk: "So to recap in Q1 we navigated several unforeseen challenges as well as the ramp of the updated Model 3 in Fremont."

Future Outlook and Product Roadmap and New Models

Elon Musk: "We’ve updated our future vehicle lineup to accelerate the launch of new models ahead, previously mentioned startup production in the second half of 2025, so we expect it to be more like the early 2025, if not late this year. These new vehicles, including more affordable models, will use aspects of the next generation platform as well as aspects of our current platforms, and will be able to produce on the same manufacturing lines as our current vehicle lineup."

Lars Moravy: "Our first vehicles are planned for late 2025 with external customers starting in 2026."

Vaibhav Taneja: "As we prepare the company for the next phase of growth, we had to make the hard but necessary decision to reduce our head count by over 10%. The savings generated are expected to be well in excess of $1 billion on an annual run rate basis. We are also getting hyper focused on CapEx efficiency and utilizing our installed capacity in a more efficient manner. The savings from these initiatives, including our cost reductions will help improve our overall profitability and ultimately enable us to increase the scale of our investments in AI."

Optimus

Elon Musk: "As I've said before, I think Optimus will be more valuable than everything else combined. Because if you've got a sentient humanoid robots that is able to navigate reality and do tasks at request, there is no meaningful limit to the size of the economy."

Thoughts on Tesla ER $TSLA:

🟢Pros:

+Cybertruck is in the ramp-up phase.

+4680 production increased about 18% to 20% from Q4.

+Next-generation vehicle production expected to start earlier, in early 2025.

+Vehicle production capacity now is 2,350,000, which already implies 27% YoY growth; Elon confirmed the expected increase in production from last year.

+Tesla reduced the price for FSD and expects a significant increase in sales.

+Tesla Bot Optimus and FSD could be company growth drivers in the future.

🔴Cons:

-Automotive revenue decreased by 12.9% YoY.

-Tesla Cars Delivered decreased by 8.5% YoY; almost all automakers reported a decline in sales for the 1st quarter.

🟡Neutral:

+- FCF margin is negative, but Tesla expects positive cash flow in the coming quarters.

+- Automotive GM excl. regulatory credits decreased to 16.4% from 17.2% last quarter; Tesla recently reduced prices on almost all of its vehicles, but COGS per unit continued to decline sequentially.