Snowflake at the Center of the Enterprise AI Revolution — But Can Competition Erode the Moat?

Deep Dive into $SNOW: Valuation, Segment Growth, Key Metrics, Profitability, Expenses, Product Launches, Customer Acquisition, Financial Stability, SBC/Revenue, and Shareholder Dilution.

Snowflake’s Q2 was a clean beat—and a signal. Product velocity is accelerating under Sridhar Ramaswamy: Cortex AI SQL, Gen 2 Warehouse, and Crunchy/Postgres extend the platform from analytics into full-stack AI workloads.

Leading indicators are outpacing revenue, with sales capacity in place and network effects compounding through data sharing and the Marketplace. Stock-based compensation remains elevated but is trending lower; dilution control stays on the checklist. The real question: can Snowflake sustain reacceleration without denting unit economics?

Table of Contents:

1. Company Overview – A brief summary of the company, including its mission, sector, competitive advantage, and total addressable market (TAM).

2. Valuation – Analysis of changes in Forward EV/Sales and Forward P/E multiples, along with comparisons to peers within the same sector.

3. Economic Moat – Evaluation of the company’s moat across five key types: Economies of Scale, Network Effect, Brand, Intellectual Property, and Switching Costs.

4. Revenue Growth – Review of revenue growth dynamics over the past two years.

5. Segments and Main Products – Overview of the company’s business segments, latest quarterly performance by segment, product innovation.

6. Market Leadership – Assessment of the company’s leadership status in its segment, as recognized by reputable rating agencies like Gartner, The Forrester Wave, etc.

7. Customers – Analysis of customer growth trends, customer success stories, and major customer wins.

8. Key Performance Indicators (KPIs) – Review of Retention, net new ARR, CAC payback period, RDI score, Data sharing, Marketplace listings, profitability, operating expenses, balance sheet strength, and shareholder dilution.

9. Conclusion – Final thoughts and summary based on the above analysis.

1. Company overview

About Snowflake

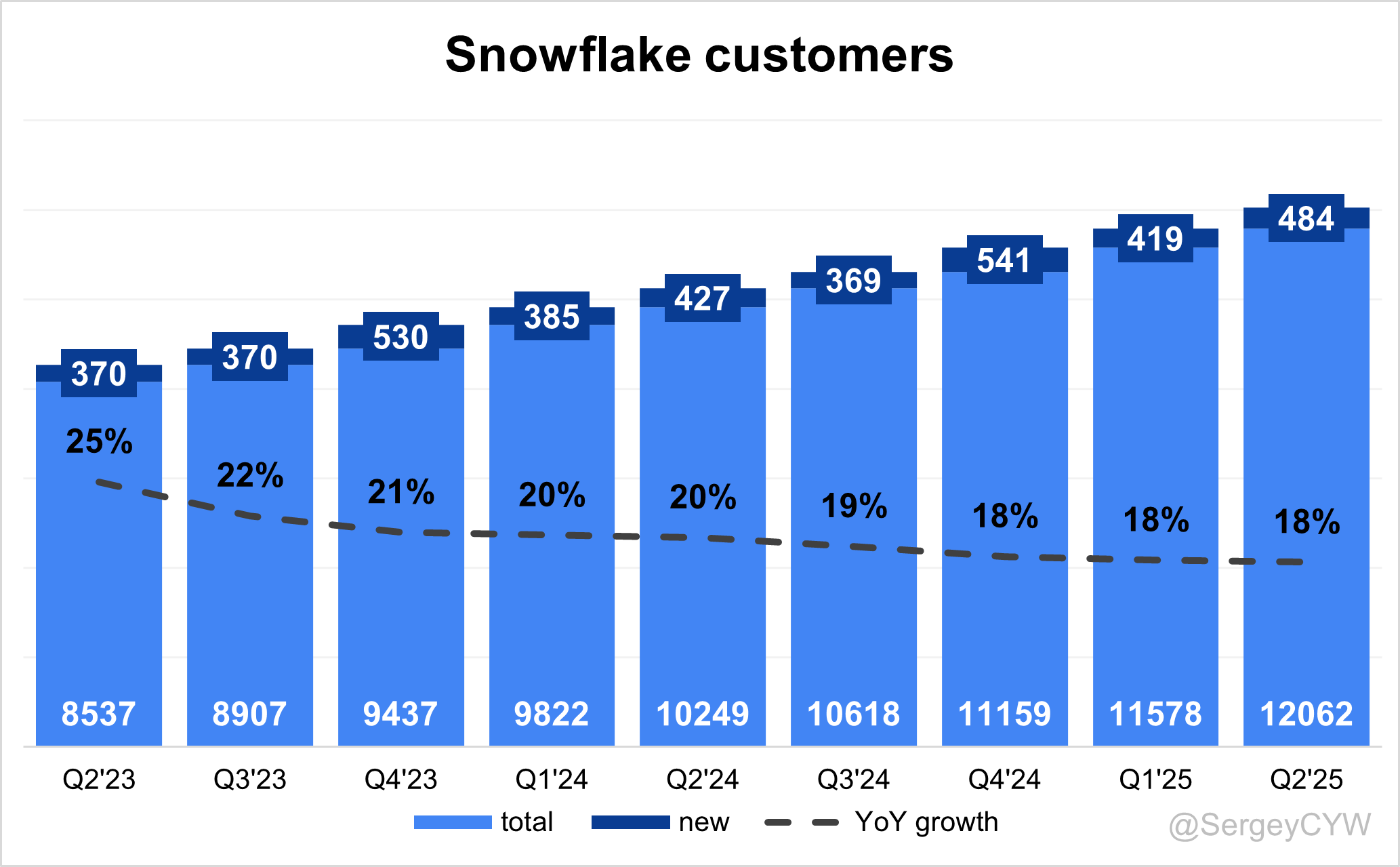

Snowflake Inc. is an American cloud-based data storage company headquartered in Bozeman, Montana. Founded in July 2012 by Benoît Dageville, Thierry Cruanes, and Marcin Żukowski, the company operates a platform enabling data analysis and simultaneous access of data sets with minimal latency. Snowflake runs across Amazon Web Services, Microsoft Azure, and Google Cloud Platform. As of November 2024, the company serves 10,618 customers, including more than 800 members of the Forbes Global 2000, and processes 4.2 billion daily queries across its platform.

Company Mission

Snowflake's mission centers on mobilizing the world's data. The company addresses a fundamental challenge: valuable data remains siloed across organizations. Their vision encompasses a world with endless insights where every organization can tackle current challenges and reveal future possibilities. Snowflake positions itself as the engine powering the AI Data Cloud, creating a global network where thousands of organizations mobilize data with near-unlimited scale, concurrency, and performance.

Sector and Services

Snowflake operates as a data cloud company providing comprehensive data platform services. The platform supports multiple workloads including data warehousing, data lakes, data engineering, artificial intelligence, machine learning, and applications. Key sectors served include advertising, media and entertainment, financial services, healthcare and life sciences, manufacturing, public sector, retail and consumer goods, technology and telecom. The company employs between 5,001-10,000 employees and maintains a public company status.

Competitive Advantage

Snowflake's competitive edge stems from four core technological features. Serverless technology allows all computing resources to be managed and provided on demand by Snowflake. Micro-partitions enable high-performance levels by storing data vertically per column with metadata for accelerated queries. The platform features separation of storage and compute, enabling independent scaling of resources. Multi-cloud functionality provides seamless operation across major cloud platforms. The company's cloud-native architecture built from scratch specifically for cloud environments differentiates it from traditional database providers.

Total addressable market (TAM)

Snowflake’s January 2025 investor update values its total addressable market (TAM) at ~$170B today and projects it will exceed $340B within three years. Analyst forecasts are consistent, estimating the TAM will more than double from $170B in 2024 to $355B by 2029, reflecting a 16% CAGR.

The opportunity spans several high-growth segments. The cloud data warehouse market is expanding from $28.5B in 2023 to $42.4B by 2025 with a 22.3% CAGR. The data analytics platform market is set to grow from $65.2B to $94.7B over the same period, a 20.5% CAGR. Data sharing solutions are accelerating from $13.8B to $24.3B, marking a 32.7% CAGR. The fastest growth is in AI/ML data infrastructure, projected to surge from $19.6B to $41.2B, achieving a 45.1% CAGR.

2. Valuation

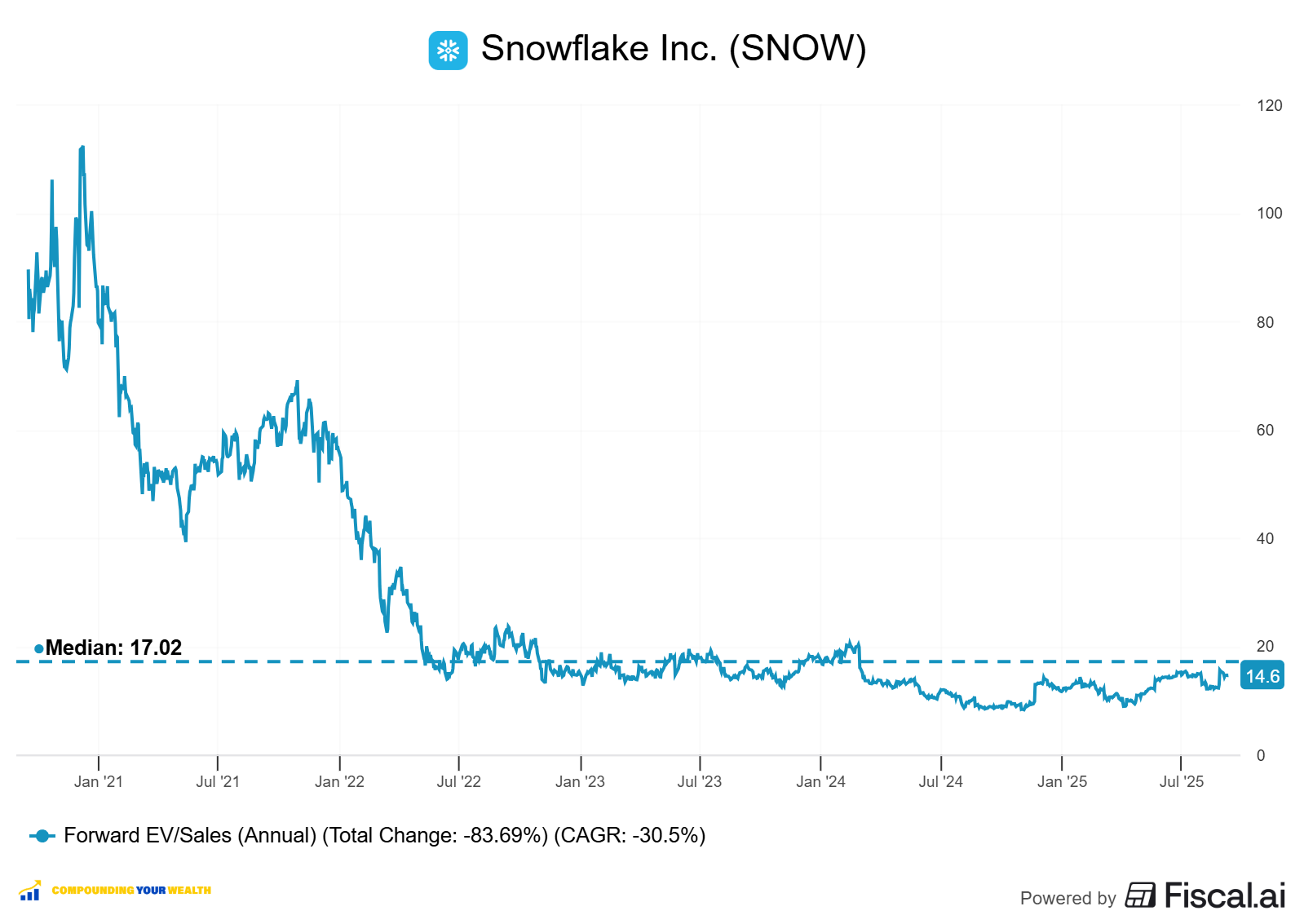

After a significant drop, $SNOW is trading at a Forward EV/Sales multiple of 14.6 —below 2022-2023 low levels and below the median of 17.0.

Powered by Fiscal.ai — get 15% off with affiliate link for Compounding Your Wealth readers.

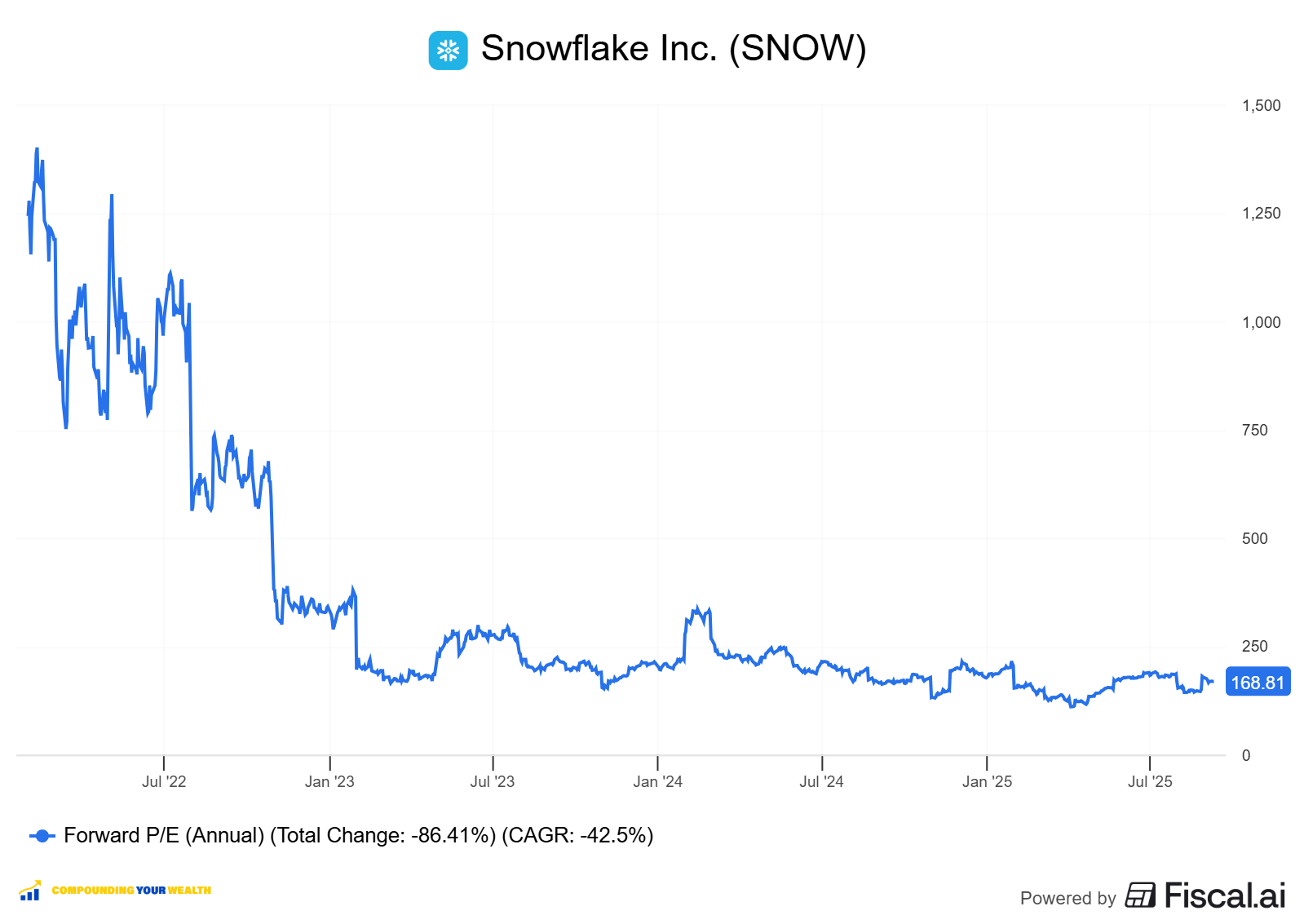

$SNOW trades at a Forward P/E of 168.8. In 2024, under new CEO Sridhar Ramaswamy, the company significantly increased operating expenses, particularly in R&D, returning to an earlier stage of growth.

The EPS growth forecast for 2026 is 36%, 2027 P/E of 199, with a 2026 PEG ratio of 5.2.

The EPS growth forecast for 2027 is 47%, 2027 P/E of 141, with a 2027 PEG ratio of 3.0.

Powered by Fiscal.ai — get 15% off with affiliate link for Compounding Your Wealth readers.

The PEG (Price/Earnings to Growth) ratio is a key tool for evaluating growth stocks, introduced by Peter Lynch.

PEG < 1: Undervalued – A ratio below 1 suggests the stock is undervalued. For example, if the P/E is 15 and earnings are expected to grow by 20%, the PEG would be 0.75, indicating a good buying opportunity.

PEG = 1: Fair Value – A PEG of 1 means the stock price matches its growth expectations, representing fair value.

PEG > 1: Overvalued – A PEG above 1 indicates the stock may be overvalued, as its price is higher than its projected growth rate, making it riskier.

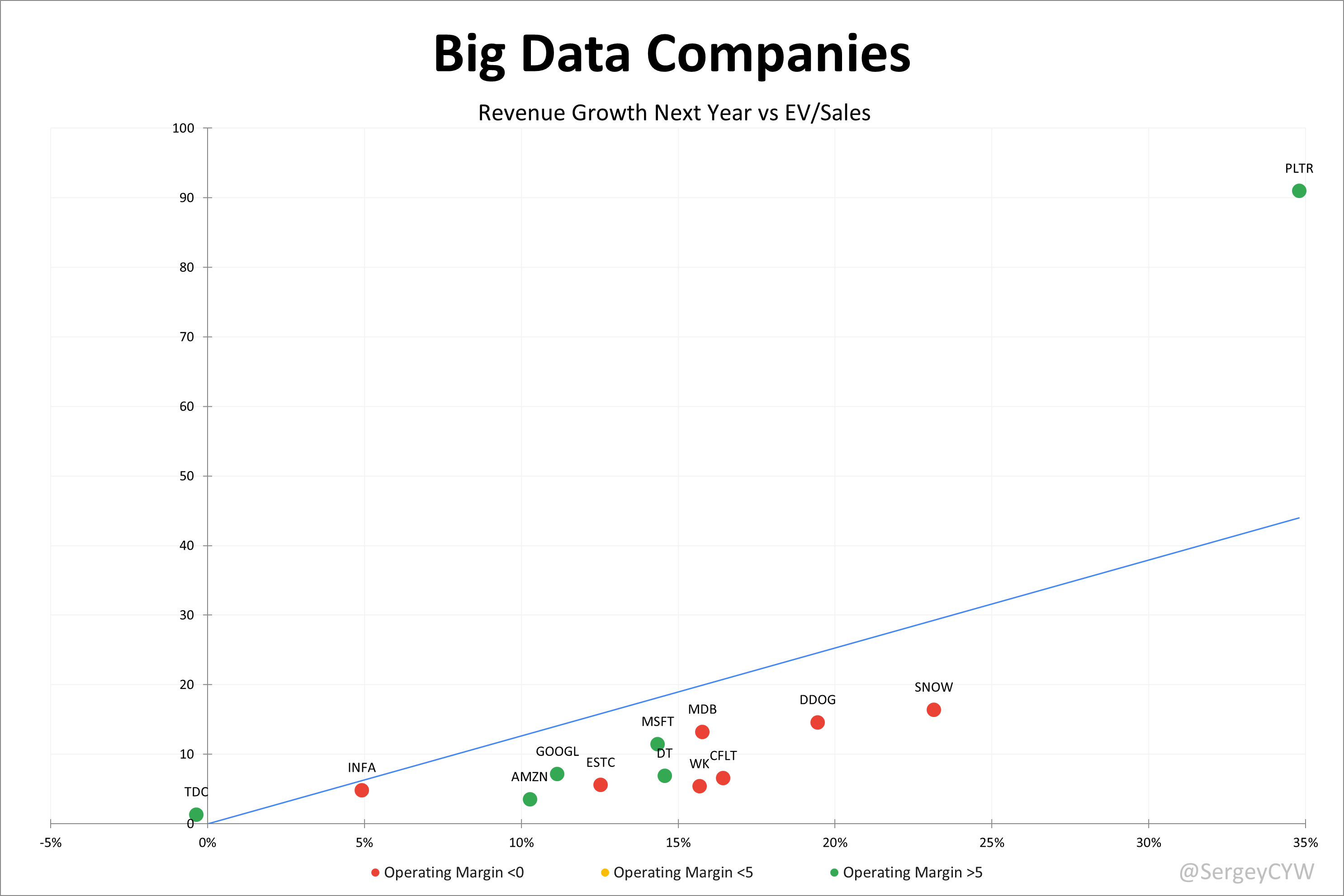

Valuation comparison

Analysts forecast $SNOW's revenue growth at +23.6% in 2026 and +23.8% in 2027, one of the highest among the companies I am monitoring. Considering the 2026 revenue forecast, the valuation based on the EV/S multiple appears undervalued compared to companies in the big data sector.

Analysts expect strong revenue growth, so let's examine the key metrics to determine whether these expectations are justified.

We'll evaluate the company's economic moat, which supports long-term revenue growth, analyze revenue trends and the forecast for next quarter, and identify key factors that could help the company exceed expectations and sustain future growth.

We'll assess the performance of key segments, the launch of new products and updates, customer acquisition growth, key financial metrics, financial stability, and margin trends.

Additionally, we'll review the SBC/Revenue ratio, shareholder dilution, and finally, draw conclusions on the company's outlook.

3. Economic Moat

Snowflake has built a strong economic moat in cloud-based data warehousing and analytics, securing its competitive position and driving long-term revenue growth.

Economies of Scale

Snowflake demonstrates strong economies of scale through its cloud-native architecture serving over 11,000 customers across its platform. The company spreads fixed infrastructure and development costs across this massive customer base, reducing per-user expenses significantly. With $3.95 billion in product revenue for fiscal 2025 and the ability to process 4.2 billion daily queries, Snowflake achieves substantial cost advantages that smaller competitors cannot match. This scalability enhances margins and pricing power, creating a formidable barrier for new entrants who lack the customer density to achieve similar unit economics. The company's 43% free cash flow margin demonstrates how effectively these economies of scale translate into profitability.

Network Effects

The platform exhibits strong network effects that create a self-reinforcing competitive advantage. Snowflake's data-sharing capabilities have expanded dramatically, with data sharing reaching 40% in Q2 2025, significantly up from 25% two years ago. As more organizations join the ecosystem, the data-sharing capabilities become increasingly valuable, making the platform more attractive to new enterprise clients. With 745 Forbes Global 2000 customers and 580 customers generating over $1 million in trailing 12-month product revenue, the network creates substantial value that becomes harder for competitors to replicate. The Snowflake Marketplace added record +302 new listings in Q2 2025, reflecting a 21% year-over-year increase in ecosystem participation.

Brand Strength

Snowflake has established itself as a market leader in cloud data warehousing, known for high performance, scalability, and security. The company serves more than 745 Forbes Global 2000 companies who rely on Snowflake for mission-critical data operations, reinforcing its brand power. CEO Sridhar Ramaswamy positions the company as "the most consequential data and AI company in the world", with more than 11,000 customers betting their business on the platform. This brand recognition drives customer acquisition and retention while commanding premium pricing in enterprise deals. However, Morningstar assigns Snowflake a no-moat rating due to intense competition in the data warehouse space, suggesting brand strength alone may not provide durable competitive advantages.

Intellectual Property

Snowflake's proprietary architecture that decouples storage and compute provides significant technological differentiation and optimizes cost efficiency and performance. The platform's multi-cloud compatibility across AWS, Azure, and Google Cloud creates a unique technological advantage that traditional on-premise and single-cloud solutions cannot match. The company's serverless technology, micro-partitions, and cloud-native architecture built from scratch specifically for cloud environments represent substantial intellectual property moats. Recent infrastructure improvements, including the migration from NGINX to Envoy Proxy, demonstrate ongoing technical innovation that maintains competitive differentiation.

Switching Costs

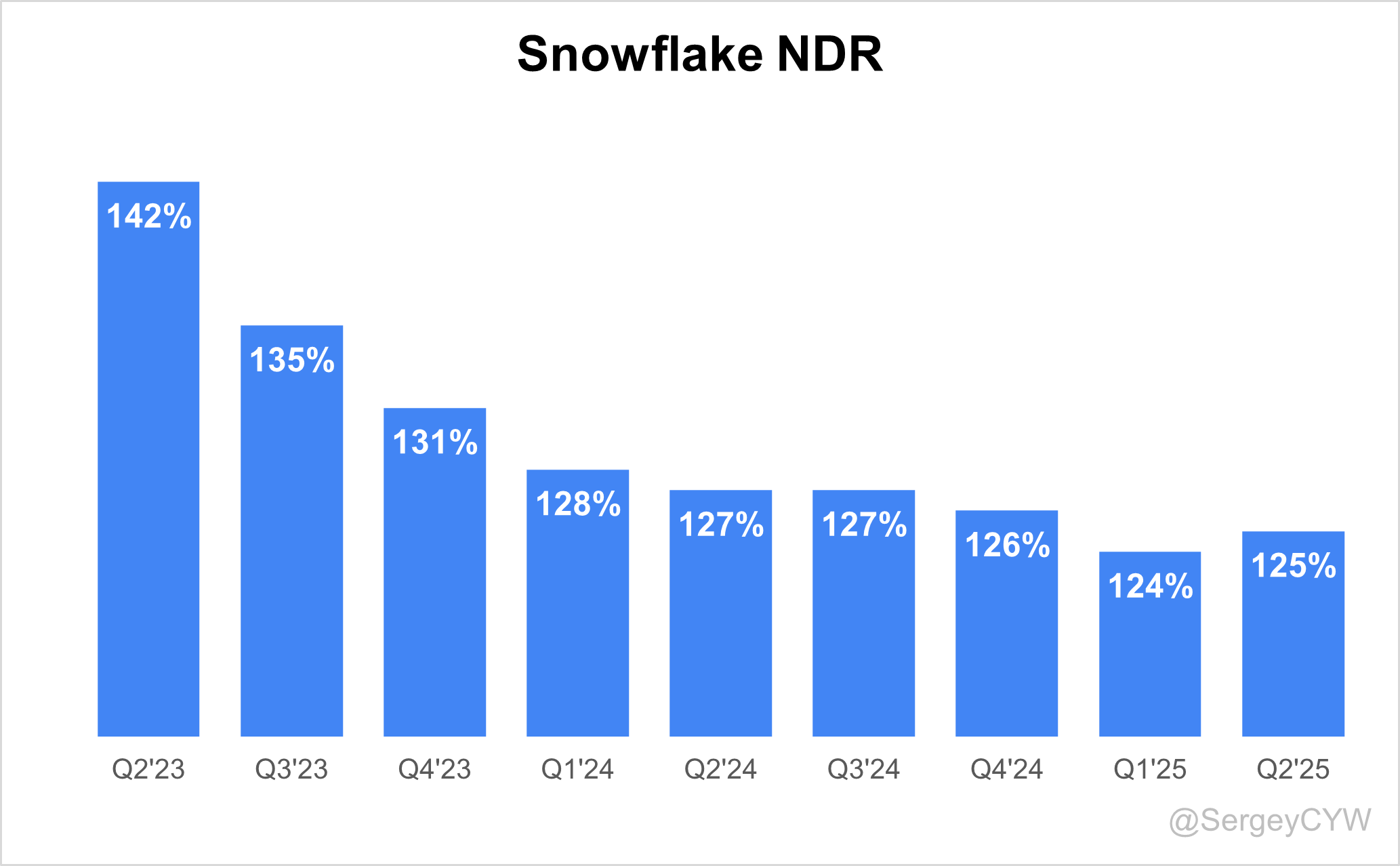

Snowflake creates very high switching costs that lock in customers through operational complexity and risk. Transitioning to another provider requires downtime, retraining, and reconfiguration, creating significant operational risk for enterprises. The 125% net revenue retention rate demonstrates how effectively these switching costs work in practice, as customers not only stay but expand their usage. With more than 6,100 customers using Snowflake's AI and ML technology weekly and extensive data integration, the complexity of migration discourages customer defection and fosters long-term retention. The consumption-based pricing model and deep data integrations create substantial exit barriers for enterprise customers.

Snowflake's economic moat is primarily built on very strong switching costs and network effects and strong economies of scale. While brand strength and intellectual property provide additional protection, the most formidable barriers come from the operational complexity of switching providers and the self-reinforcing value of its data-sharing ecosystem.

4. Revenue growth

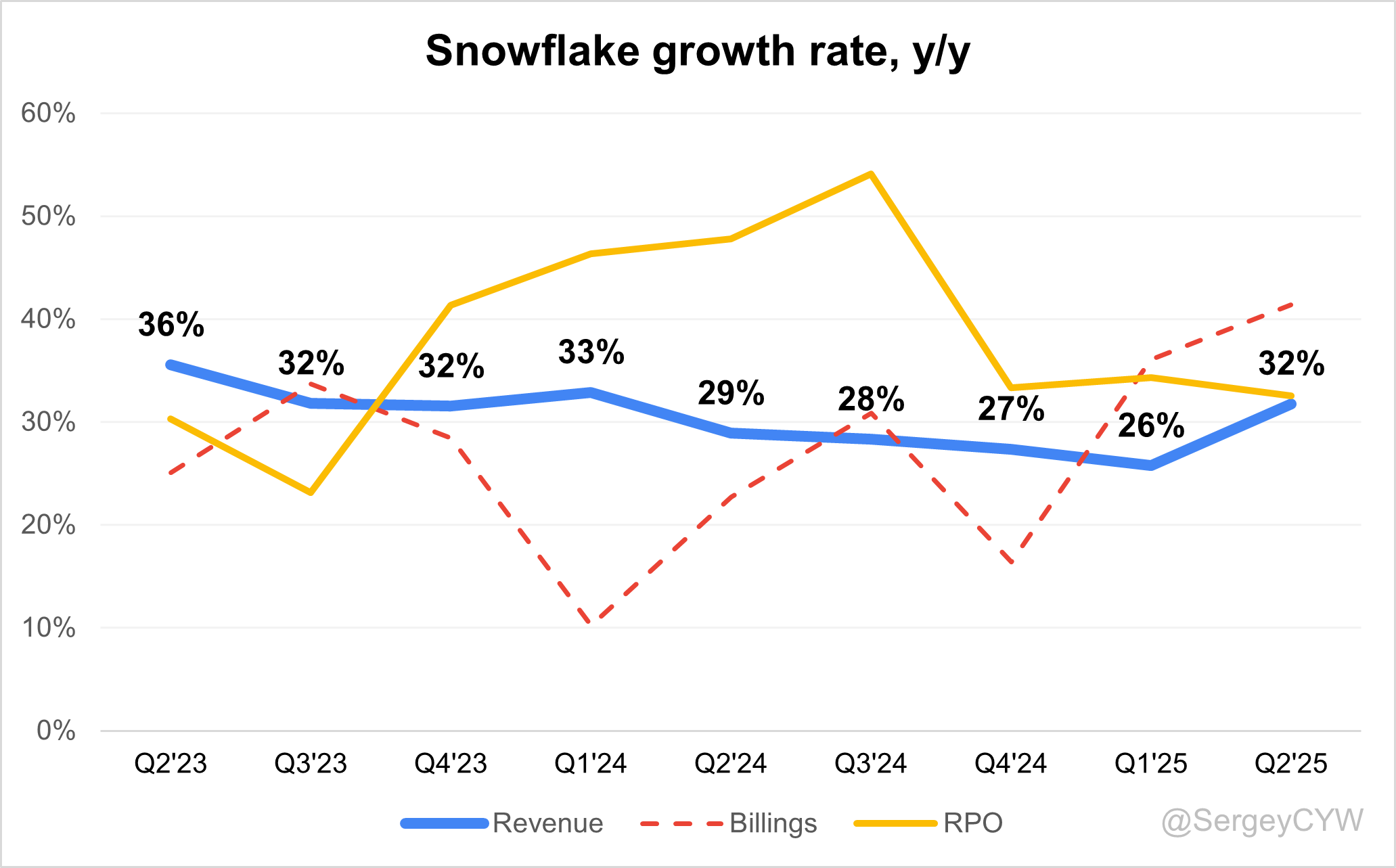

$SNOW’s revenue growth accelerated noticeably from +25.8% YoY in Q1 2025 to +31.8% in Q2.

RPO growth slowed slightly to +32.5% (from +34.3% YoY in Q1 2025), but still outpaces revenue growth. Since Snowflake operates on a usage-based model rather than subscriptions, cRPO is the key metric. cRPO growth accelerated to +32.5% YoY, surpassing total revenue growth.

Billings growth also accelerated to +41.4% YoY, well above the revenue growth rate.

Looking ahead, if the company beats its own guidance by 4.9%—the same as this quarter—Q3 revenue growth would reach 32.1%, signaling continued acceleration.

It’s worth noting that in Q2 the company broke its trend of slowing revenue growth and showed an acceleration, an important milestone for Snowflake.

5. Segments and Main Products.

Snowflake's revenue primarily consists of two segments: Product and Professional Services.

Product segment generates the majority of revenue (95,2%), driven by Snowflake's core offerings like data warehousing, data lakes, data engineering, data science, and secure data sharing capabilities.

Professional Services and Other contribute a smaller portion of revenue at around 4-5%, involving consulting, training, and implementation support to help customers maximize their use of Snowflake's platform.

Key products include Snowpipe for seamless real-time data ingestion from external cloud storage like Amazon S3 or Azure Blob.

Snowflake Marketplace allows verified data sharing and collaboration among organizations, offering datasets and services that meet quality and security standards.

The company's AI initiatives are integrated into its Cortex platform, hosting leading AI models from OpenAI and Anthropic, enabling advanced analytics and AI-driven insights.

Snowflake also offers Native Apps through its Marketplace, enabling customers to deploy third-party solutions directly into their Snowflake instances for enhanced functionality.

The core platform provides integrated cloud services for data warehousing, data lakes, data engineering, analytics, and secure data sharing across scalable cloud infrastructure.

Main Products Performance in the Last Quarter

Cortex AI

Momentum accelerated. AI influenced ~50% of new logos in Q2 and powered ~25% of deployed use cases. ~6,100 accounts now use Snowflake AI weekly. Early enterprise adoption came from Thomson Reuters, deploying agents across finance and HR, and BlackRock, scaling client insights. Monetization aligns with consumption. Broad self-serve adoption precedes large-scale rollouts such as Snowflake Intelligence assistants. The challenge lies in converting pilots into org-wide, high-throughput agents while maintaining governance and minimizing hallucinations.

Apache Iceberg

Adoption continues to rise with 1,200+ accounts now standardizing on Iceberg. Customers seek interoperability and open standards. The challenge comes from competing implementations across the ecosystem. Snowflake differentiates on governance, simplicity, and performance.

Snowpark

Snowpark drives consumption through workload consolidation. Snowpark Connect for Apache Spark (public preview) allows Spark DataFrame and SQL to run directly on Snowflake engines, cutting infrastructure overhead and accelerating migration. Leadership asserts Snowpark outperforms managed Spark. The success metric is workload migration volume. The challenge is proving sustained price-performance across complex pipelines.

OpenFlow

OpenFlow (Datavolo) expanded ingest to structured, unstructured, batch, and streaming data with Oracle CDC support. It opens access to a $17B integration market. Customers gain faster time-to-value and fewer moving parts.

Snowflake Marketplace

Collaboration strengthened as 40% of customers now share data, creating network effects that feed Marketplace usage.

AI & Applications

AI became a major demand catalyst. Influenced ~50% of new logos and accounted for ~25% of use cases. Weekly adoption reached ~6,100 accounts. Cortex AI SQL enables AI models directly in SQL, eliminating data movement. Customers gained day-one access to GPT-5, Anthropic, and open-source models. Broad self-serve usage is now converting to targeted org-wide deployments. Key challenge is scaling agentic workflows with strong governance.

Innovations & Product Updates

Snowflake Intelligence, in public preview, enables natural-language access to enterprise data with agentic actions.

Cortex AI SQL unifies analytics and AI inside the platform.

Gen 2 Warehouse delivers up to 2× faster performance with auto-optimization at no added cost.

Snowflake Postgres (Crunchy integration) brings enterprise-grade Postgres into the AI Data Cloud with preview due in the coming months.

Snowpark Connect eased Spark workload migration.

Velocity remained high with ~250 capabilities GA in the first half of the year.

Leadership Transition

Snowflake appointed Brian Robins as Chief Financial Officer, effective September 22. He succeeds Mike Scarpelli, who will retire as CFO on the same date and transition to an advisory role to ensure continuity. Robins previously served as CFO of GitLab since 2020, overseeing finance, data, and business systems. He also held CFO roles at Sisense, Cylance, AlienVault, and Verisign. He serves on the boards of GitLab Foundation and ID.me and is an advisor at Brighton Park Capital and ForgePoint Capital Cybersecurity.

6. Market Leadership

Gartner ranks Snowflake as a leading provider in the cloud database management systems (DBMS) market. Its Data Cloud is recognized as a unified, cloud-native platform supporting data warehousing, data lakes, analytics, and AI workloads. The company is strong in managing structured and semi-structured data, with multi-cloud support, auto-scaling, and robust data sharing capabilities that differentiate its offering.

Forrester analysis from Snowflake Summit 2025 acknowledges the platform's evolution beyond traditional data warehousing into comprehensive AI capabilities. The research firm recognizes Cortex AISQL as expanding Snowflake's reach into multimodal data analysis, enabling users to query text, images, and audio directly with SQL. Forrester notes Snowflake's approach to multimodal SQL stands out for comprehensive coverage and practical implementation compared to competitors.

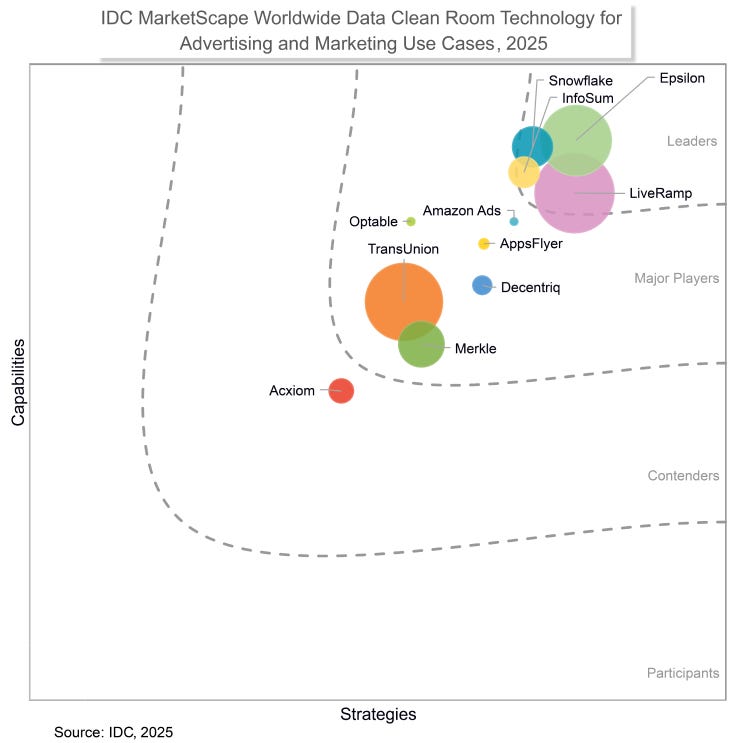

IDC named Snowflake a Leader in the MarketScape for Data Clean Room Technology for Advertising and Marketing Use Cases 2025. The research firm calls Snowflake Data Clean Rooms "an ideal solution for advertisers and marketers seeking secure collaboration tools to optimize campaigns in a privacy-first era". IDC specifically recognizes two core strengths: access controls from heritage of data sharing providing granular role-based access control at table and column level, and neutral and agnostic platform allowing customers to use identity partners of their choice.

7. Customers

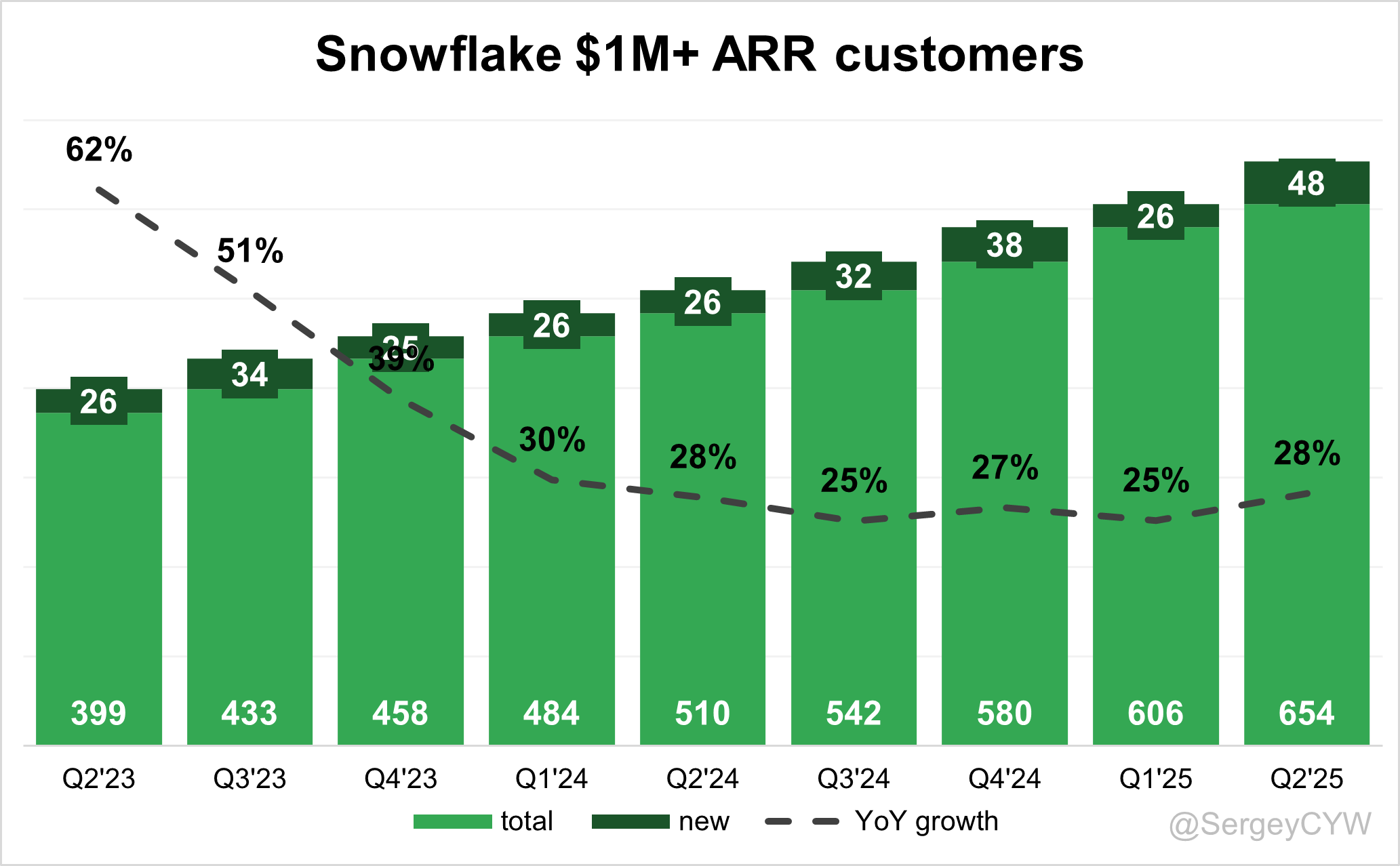

$SNOW added 484 total customers, reflecting +18% YoY growth, which is higher than in Q2 last year. Snowflake also added 48 large customers with $1M+ ARR, and achieved +28% YoY growth in that segment — a record addition.

Customer Success Stories

Hyatt Hotels simplified enterprise data management with Snowflake, consolidating data into a single governed environment. The result was faster, secure access to information that improved decision-making and customer experience. Cambia Health Solutions used Snowflake Intelligence to build its first AI agent, enabling Medicare teams to analyze longitudinal data and deliver more personalized care to 2.6 million members. Duck Creek Technologies applied Snowflake AI to streamline finance, sales, and HR workflows, positioning itself as an innovator in insurance. Thomson Reuters deployed Cortex AI for HR and finance teams, cutting time-to-insight and boosting productivity. BlackRock used Cortex AI to aggregate client data across portfolios, improving service scale and quality, describing the capability as a “superpower.”

Large Customer Wins

Snowflake 50 customers crossed the $1 million TTM revenue threshold, bringing the total to 654. Management emphasized that Global 2000 accounts have the potential to reach $10 million annual spend per customer. High-profile enterprise leaders such as Booking.com, InterContinental Exchange, and Hyatt reinforced the platform’s strength in analytics and governance. Azure cloud revenue surged 40% y/y, aided by joint field alignment with Microsoft and strong EMEA demand. The breadth of strategic relationships—12,000 global partners—expanded Snowflake’s market presence and deal velocity.

8. KPI

Retention

$SNOW Snowflake’s retention rate remains one of the highest in its class at 125% in Q2 2025, increasing by 1 PP QoQ. The company calculates this metric based on data from the past two years, making it a lagging indicator for Snowflake.

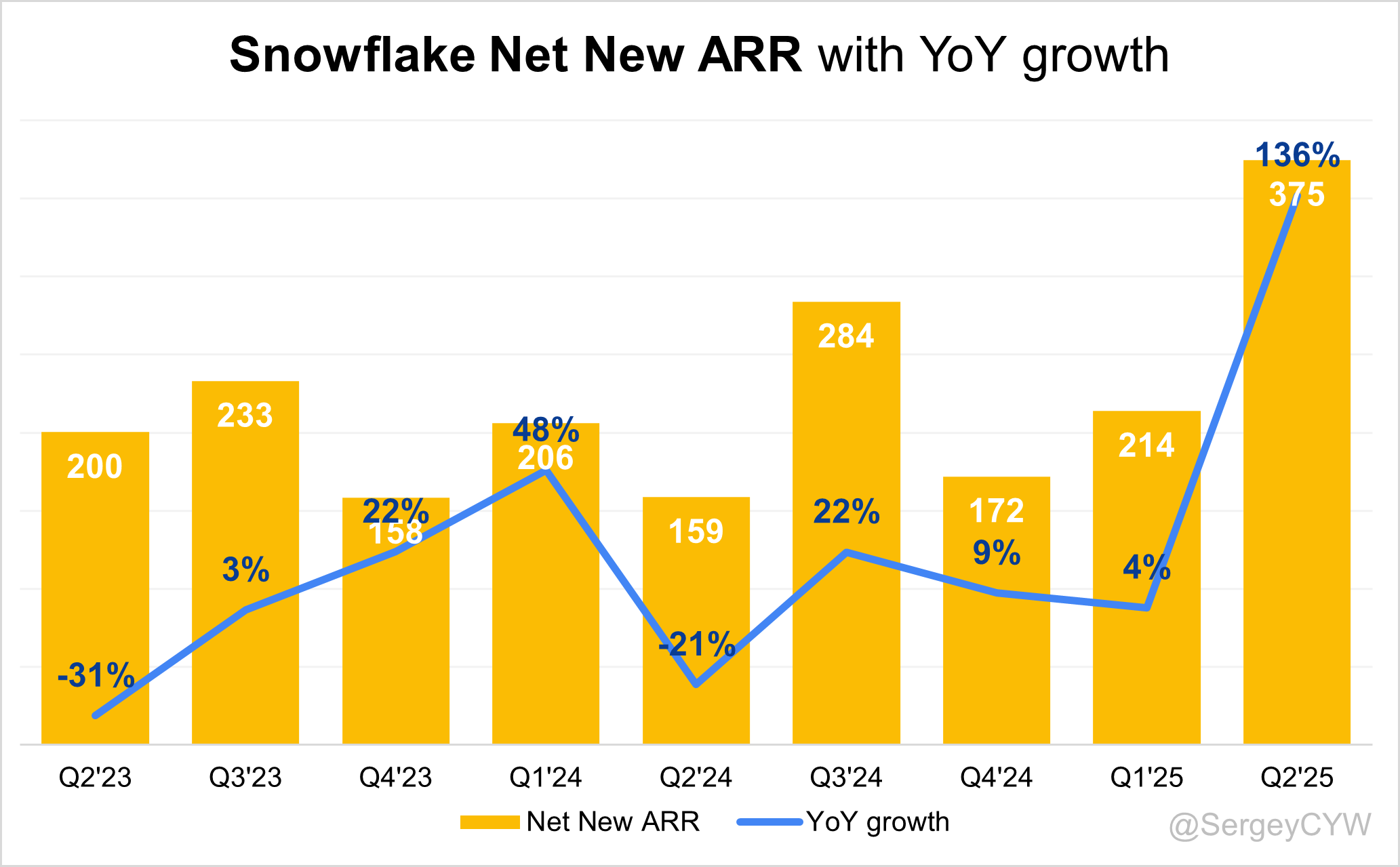

Net new ARR

$SNOW Snowflake added $375 million in net new ARR, reflecting a +136% increase YoY. Net new ARR addition in Q2 was a record for the company.

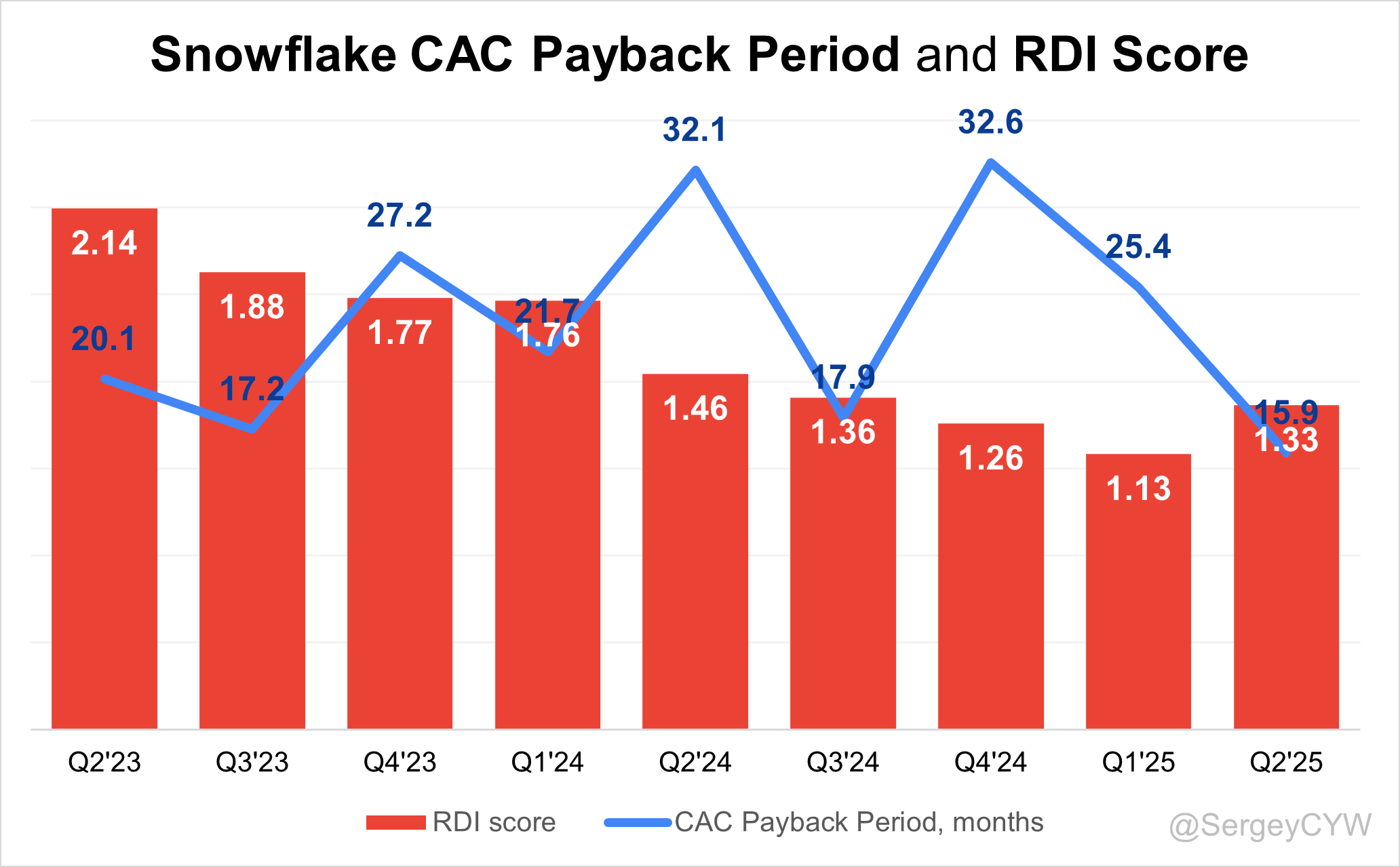

CAC Payback Period and RDI Score

$SNOW Snowflake’s return on S&M spending is 15.9, significant improvement compared to the previous quarter.

Snowflake isn’t a pure SaaS company—it runs on a consumption-based model, which makes metrics like CAC Payback Period and net new ARR more volatile than those of traditional SaaS businesses.

The R&D Index (RDI Score) for Q2 came in at 1.33, above the median of 1.2 for the SaaS companies I track, but still solid and well above the industry median of 0.7. Snowflake has increased its R&D spending, which has temporarily lowered the RDI Score—though this is expected, as the impact of those investments should be reflected in future revenue growth.

An RDI Score above 1.4 is considered best-in-class, while the industry median of 0.7 highlights the importance of efficient R&D investment.

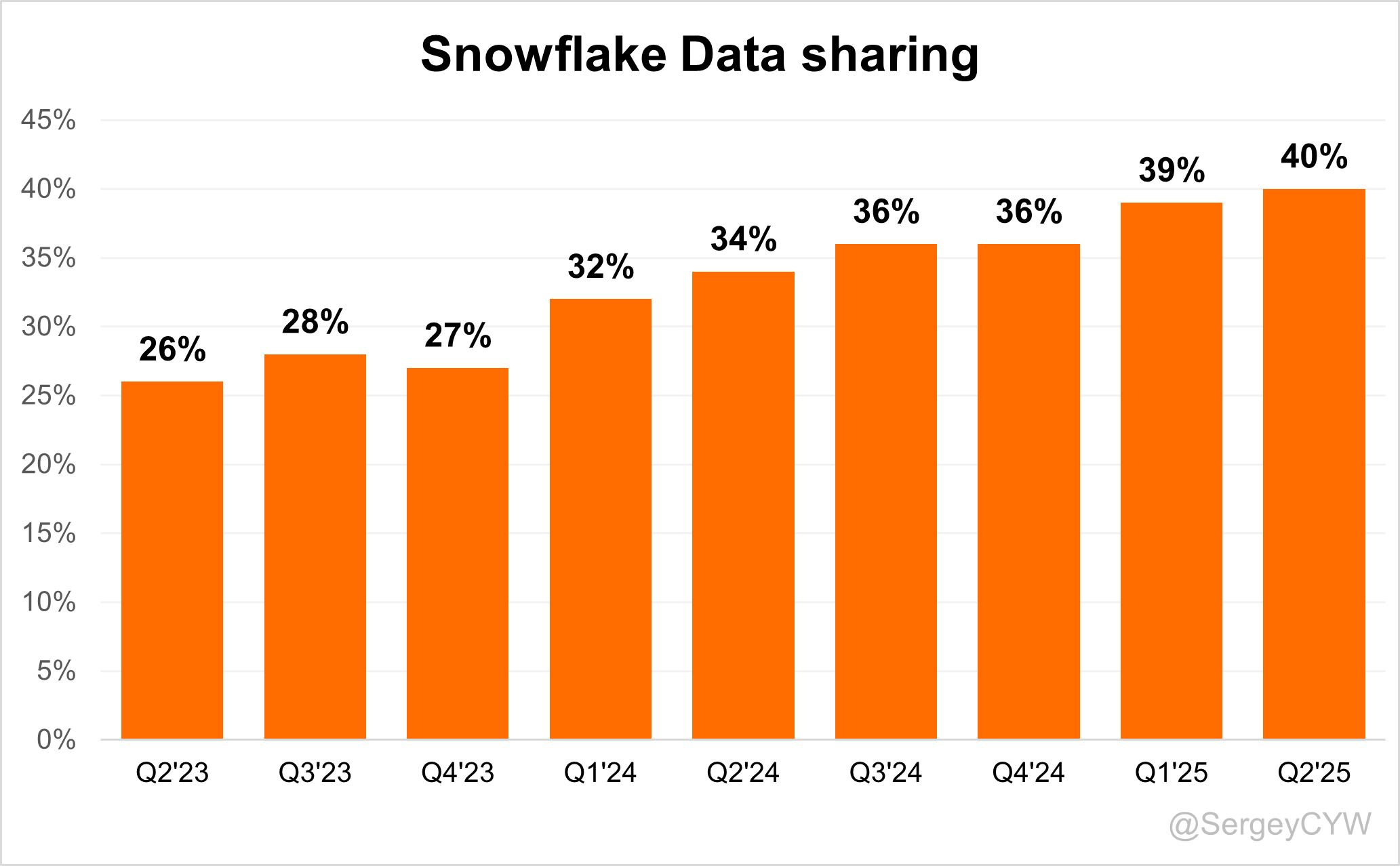

Two key components of $SNOW Snowflake’s economic moat are high switching costs and strong network effects.

Data sharing has steadily grown from 26% two years ago to 40% in Q2 2025, reflecting sustained engagement.

This metric is crucial in highlighting Snowflake’s network effect, as higher data sharing enhances platform utility, attracting more customers and reinforcing Snowflake’s competitive edge.

Data sharing remains Snowflake’s structural moat. Dentsu and CloudZero use live data connections to collaborate across networks and eliminate third-party tools.

Snowflake’s Data Clean Room supports secure, privacy-preserving sharing—critical for industries like advertising and finance.

$SNOW added 302 new listings to its Marketplace in Q2 2025, a +21% YoY increase. After a weak Q1 with only 54 new listings, Q2 marked a record addition for the company.

Management had previously stated that Marketplace activity was expected to reaccelerate in H2 FY2025 as AI adoption scaled — which indeed happened in Q2.

This metric still reflects the strength of Snowflake’s expanding ecosystem and the growing traction of its data-sharing platform.

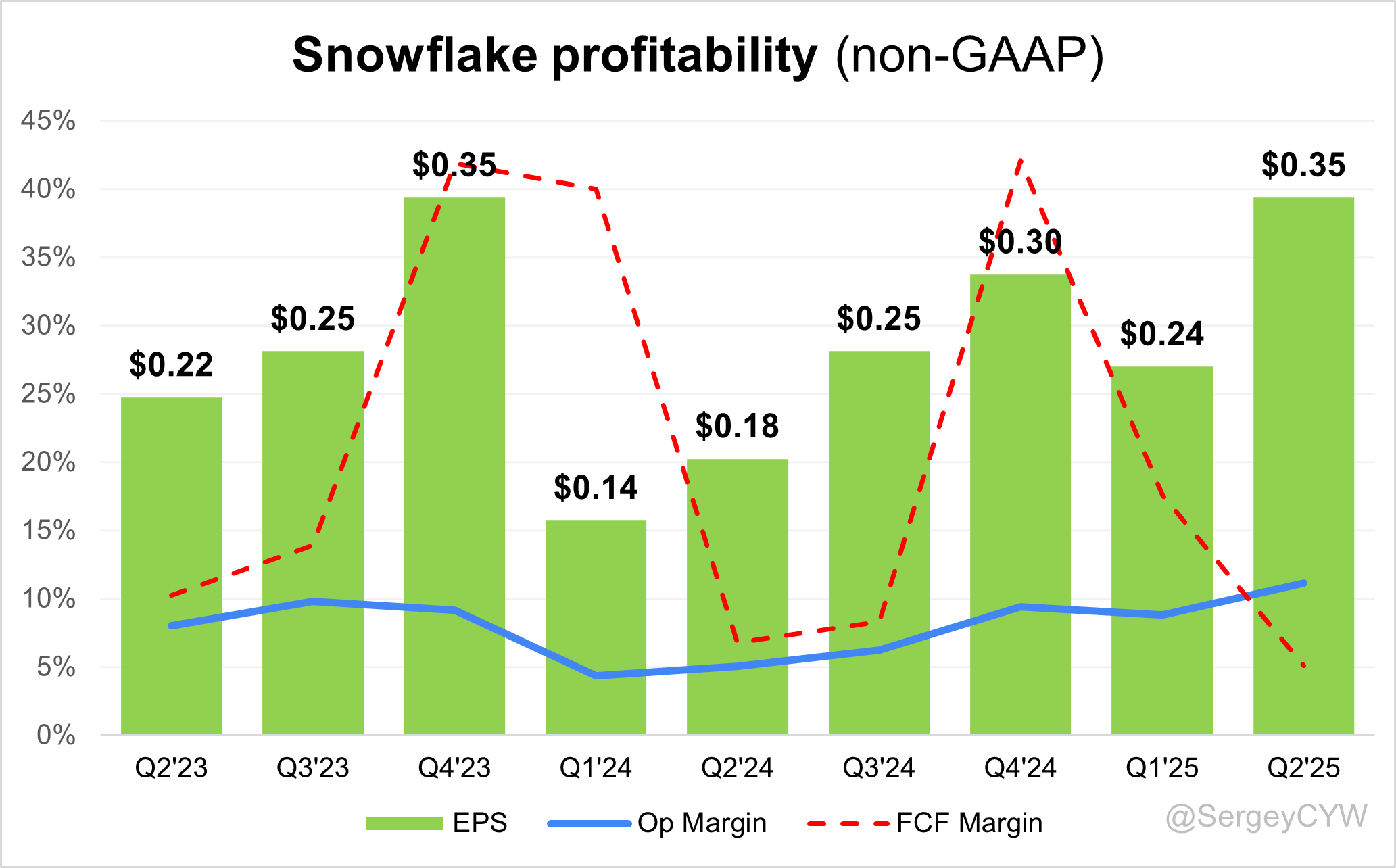

Profitability

Over the past year, $SNOW Snowflake’s margins have changed:

• Gross Margin slightly declined from 73.2% to 72.9%.

• Operating Margin increased from 5.0% to 11.1%.

• FCF Margin slightly declined from 6.7% to 5.1%.

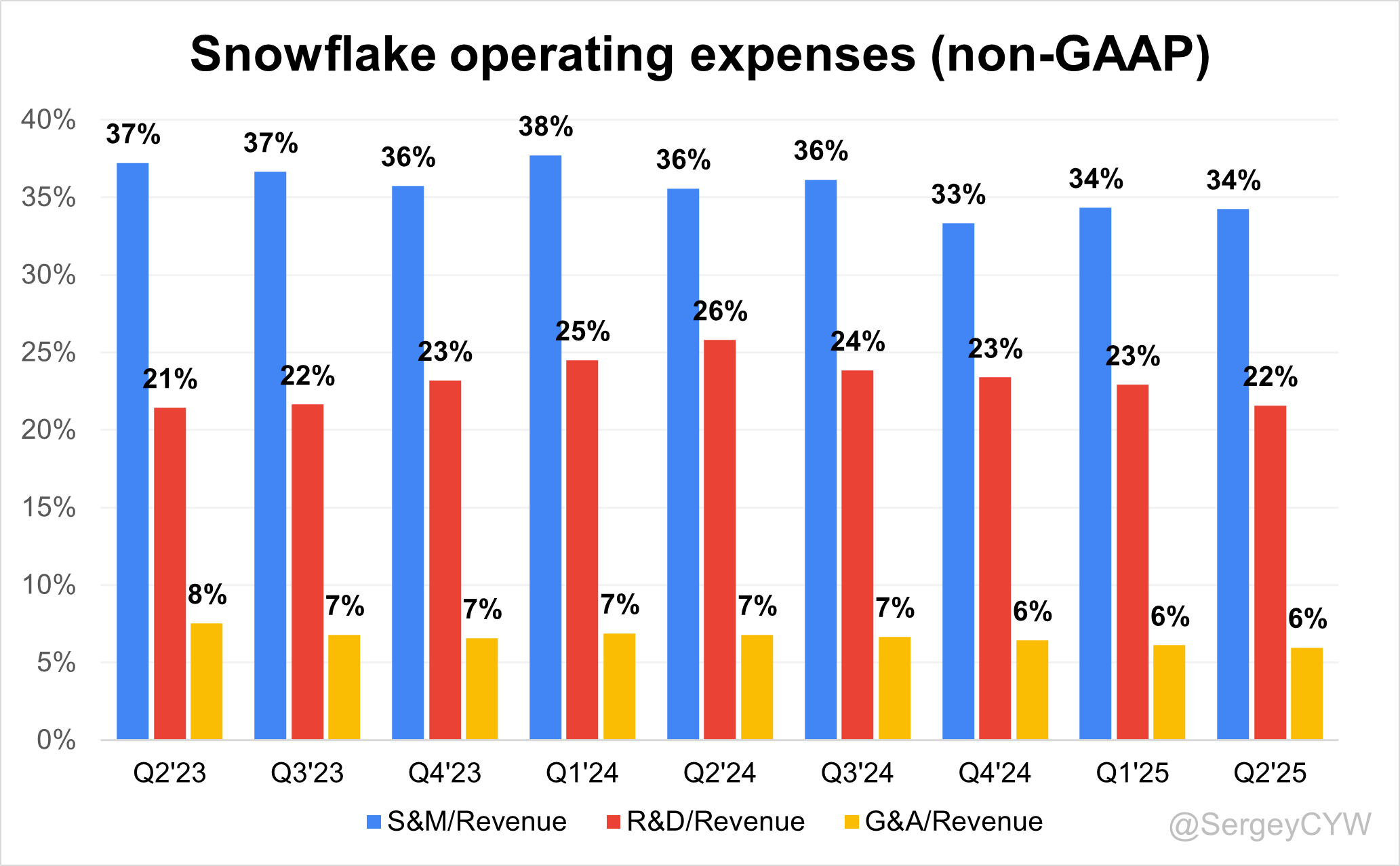

Operating expenses

Over the past two years, $SNOW Snowflake has reduced operating expenses, with a significant decline in the last quarter driven by lower S&M and G&A spending. S&M expenses dropped from 37% in Q2 2023 to 34%, while G&A decreased from 8% to 6%. Meanwhile, R&D spending increased and remained high at 22% of revenue, reflecting the company’s commitment to reinvesting in product development.

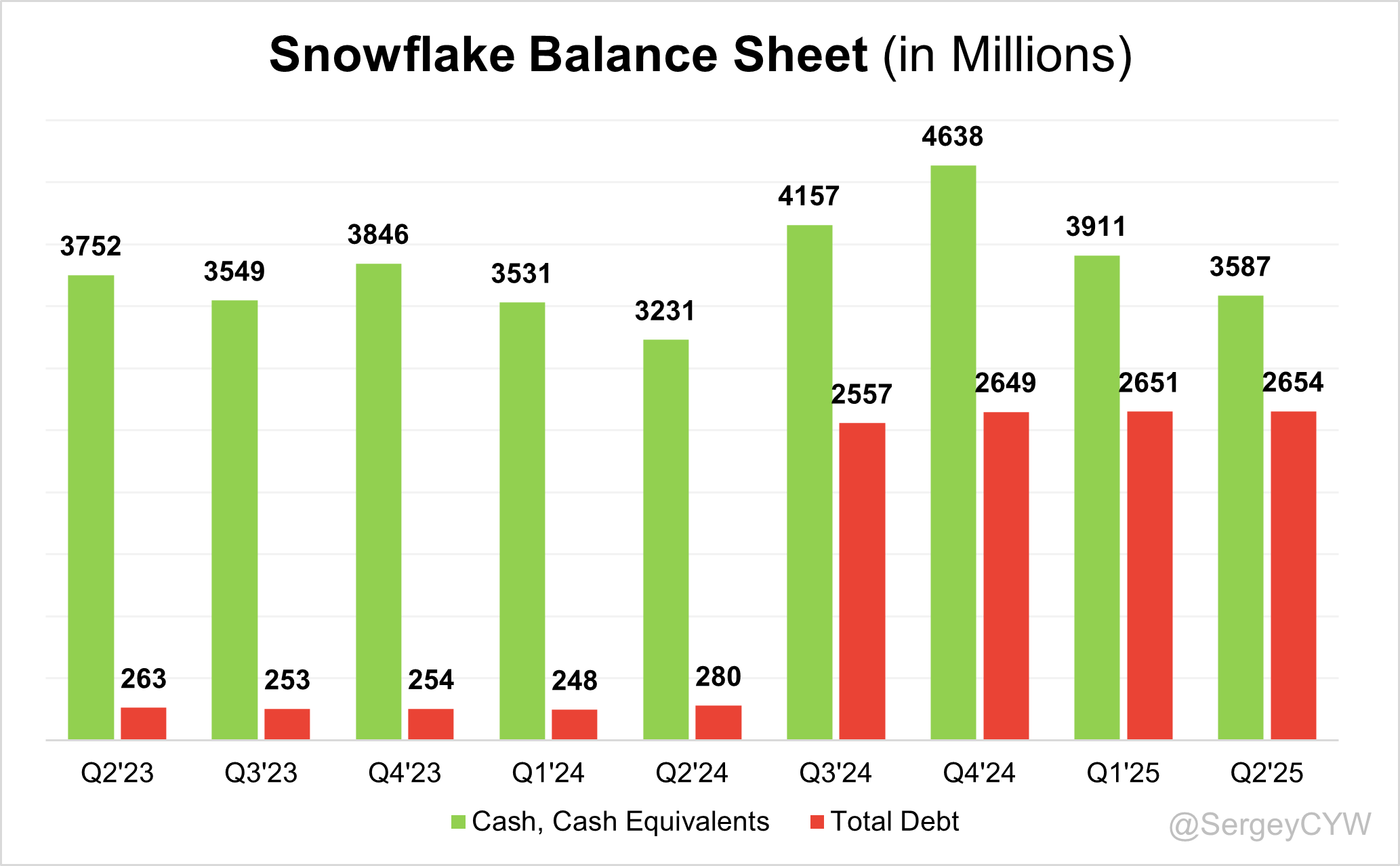

Balance Sheet

$SNOW Balance Sheet: Total debt stands at $2,654M. The company's debt increased in Q3 2024 due to the issuance of $2.3 billion in 0% convertible senior notes, split into $1.15 billion due in 2027 and $1.15 billion due in 2029. However, Snowflake holds $3,587M in cash and cash equivalents, keeping the balance sheet stable.

Snowflake recently announced acquisitions:

In late 2024, it acquired Datavolo, a platform for managing multimodal data pipelines powered by Apache NiFi. The deal expands Snowflake into the $17B data integration market and is expected to accelerate growth in the public sector, where Datavolo already has strong adoption.

On June 1, 2025, Snowflake acquired Crunchy Data for about $250M. Crunchy generates $30M+ annualized revenue and is known for secure, enterprise-ready PostgreSQL. The acquisition supports the launch of Snowflake Postgres, aimed at developers building AI-driven applications.

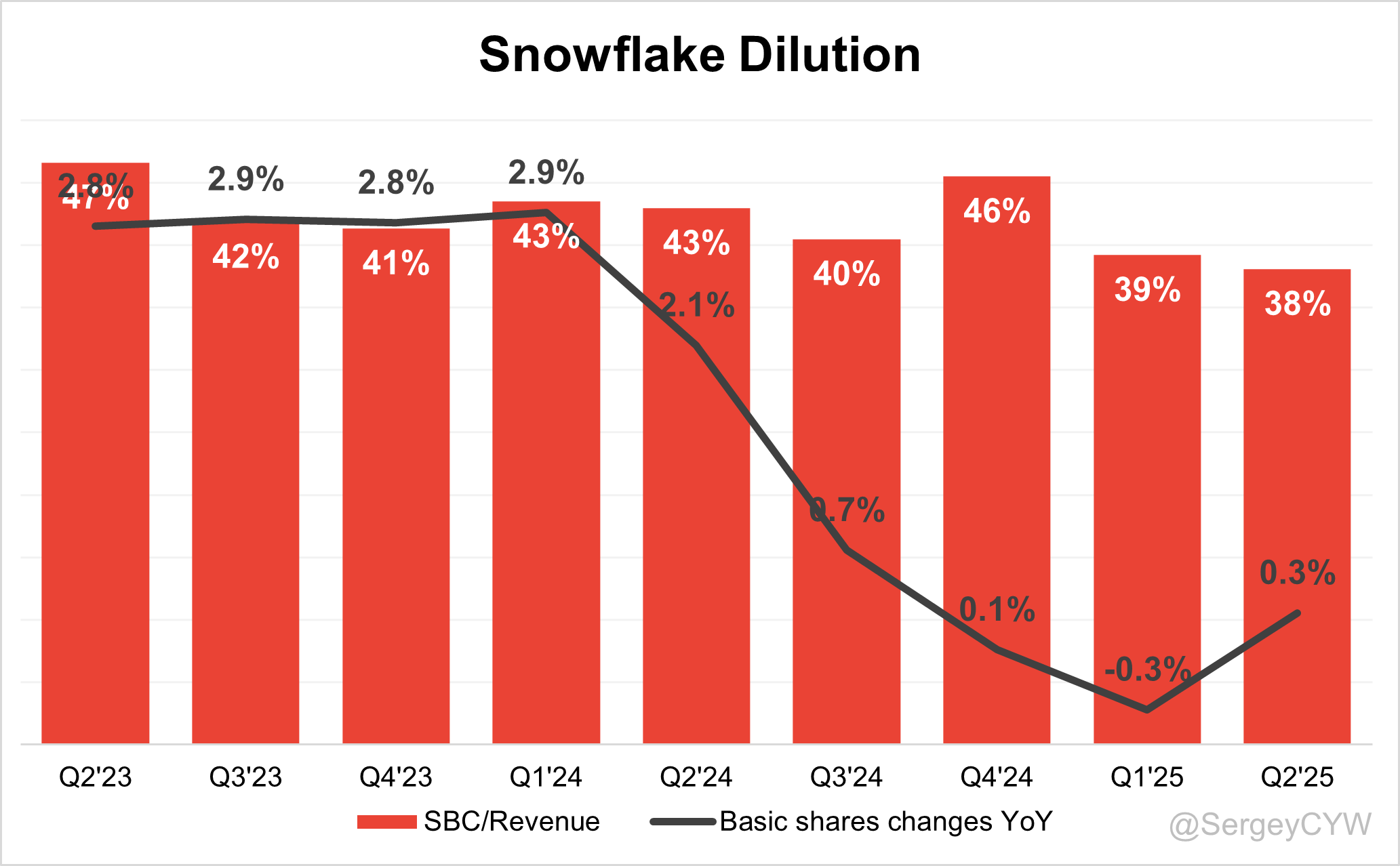

Dilution

$SNOW Shareholder Dilution: Snowflake's stock-based compensation (SBC) expenses were previously at very high levels but declined in the last quarter to 38% of revenue, which is still relatively high.

Snowflake did not repurchase shares in Q2, but during the first quarter of fiscal year 2026, Snowflake allocated $491 million to repurchase 3.2 million shares at an average price of $152.63 per share. $1.5B remains available under authorization through March 2027. Weighted-average number of common shares outstanding increased just 0.3% YoY.

9. Conclusion

$SNOW delivered a very strong Q2. Snowflake is strengthening its competitive position through major new products and innovations.

Key launches included Cortex AI SQL, which unifies analytics and AI inside the platform, Gen 2 Warehouse delivering up to 2× faster performance with auto-optimization at no added cost, and the acquisition of Crunchy, bringing enterprise-grade Postgres into the AI Data Cloud.

Innovation has accelerated under CEO Sridhar Ramaswamy, reflected in a substantial increase in R&D spending — a move I view as the right strategy. Snowflake’s total addressable market is ~$170B today, growing at a 16% CAGR.

Leading Indicators

• RPO and cRPO growth of +32.5%, outpacing revenue growth

• Billings growth at +41.4%, faster than revenue growth

• Record net new ARR added in Q2, up +136% YoY

• Record large enterprise customer additions

Key Indicators

• Net Dollar Retention at 125%, up +1pp QoQ

• CAC Payback Period improved at 15.9 month

• RDI Score is up 1PPs QoQ, at 1.33, well above SaaS peers

Snowflake’s economic moat — high switching costs and strong network effects — continues to strengthen. Data sharing now accounts for 40% of platform usage, up from 26% two years ago. Marketplace activity also hit a record, with 302 new listings in Q2.

Snowflake reduced S&M and G&A expenses while reinvesting heavily in R&D, reinforcing long-term advantages. Revenue growth has reaccelerated under Ramaswamy’s leadership, supported by aggressive hiring: 529 new employees in Q2, including 364 in sales — more than the past two years combined in the first half alone.

Forward EV/Sales ratio looks undervalued compared to other big data peers. While SBC as a percentage of revenue remains high, it has declined meaningfully, showing management is actively controlling it.

CEO Sridhar Ramaswamy:

“Snowflake is at the center of today’s enterprise AI revolution. We continue to execute at scale, as evidenced by our product revenue growth and strong outlook. We see a long runway of durable high growth and continued margin expansion ahead.”

$SNOW is one of the largest positions in my portfolio, now representing 10.2% of total holdings.

Thank you for reading!

Follow me for more frequent updates on X/Twitter and Threads, and on LinkedIn. For visual infographics, check out Instagram, and for portfolio changes, follow me on SavvyTrader.

Disclaimer: This earnings review is for informational purposes only and does not constitute financial, investment, or trading advice.