Shopify: Scalable E-Commerce Leader with Massive Growth Potential

Deep Dive into $SHOP: Valuation, Segment Growth, Key Metrics, Profitability, Expenses, Product Launches, Customer Acquisition, Financial Stability, SBC/Revenue, and Shareholder Dilution.

Shopify: Company overview

About Shopify

Shopify is a leading e-commerce platform founded in 2006 by Tobias Lütke and Scott Lake. Headquartered in Ottawa, Canada, the company enables businesses to build and manage online stores, process payments, and handle shipping. As of today, Shopify powers over 4.6 million active websites worldwide. Since going public in 2015, it has expanded into point-of-sale systems, fulfillment services, and merchant financing.

Company Mission

Shopify’s mission is “To make commerce better for everyone.” The company focuses on helping businesses of all sizes succeed online by offering intuitive tools that reduce technical complexity and enhance merchant focus on product and customer experience.

Sector

Shopify operates in the e-commerce technology sector. As of 2025, it holds a 10.32% share of the global e-commerce software market and a commanding 29% share in the U.S. e-commerce platform market. Its platform supports multiple industries, with retail making up 11% of its customer base.

Competitive Advantage

Shopify’s edge lies in its scalable solutions, extensive partner ecosystem, and focus on small to mid-sized businesses. Its integrated services, such as Shopify Payments, simplify operations for merchants. The company continually improves the platform through regular feature updates and empowers brands to go direct-to-consumer, bypassing traditional retail channels.

Total Addressable Market (TAM)

Shopify’s global TAM is estimated at $849 billion, covering e-commerce, B2B, offline retail, and merchant services. The retail e-commerce market alone is valued at $7.29 trillion in 2025, projected to grow to $15.62 trillion by 2032, representing a 12.6% CAGR.

International markets now account for 30% of revenue, growing 30%+ for two consecutive years.

Enterprise penetration through Shopify Plus has brought in larger merchants like Reebok and Barnes & Noble.

Despite the progress, Shopify has captured less than 1% of its total addressable market, highlighting the vast growth potential that still lies ahead.

Valuation

$SHOP Shopify is trading at a Forward EV/Sales multiple of 11.5, which is in line with the median of 11.2 and close to valuation levels based on multiples from 2019.

$SHOP Shopify is trading at a Forward P/E multiple of 67.6, with revenue growth of +31.2% YoY in the most recent quarter.

The EPS growth forecast for 2026 is 26%, with a P/E of 66.1, resulting in a 2026 PEG ratio of 2.5.

For 2027, EPS growth is projected at 40%, with a P/E of 52.0 and a 2027 PEG ratio of 1.3.

The PEG (Price/Earnings to Growth) ratio is a key tool for evaluating growth stocks, introduced by Peter Lynch.

PEG < 1: Undervalued – A ratio below 1 suggests the stock is undervalued. For example, if the P/E is 15 and earnings are expected to grow by 20%, the PEG would be 0.75, indicating a good buying opportunity.

PEG = 1: Fair Value – A PEG of 1 means the stock price matches its growth expectations, representing fair value.

PEG > 1: Overvalued – A PEG above 1 indicates the stock may be overvalued, as its price is higher than its projected growth rate, making it riskier.

Valuation comparison

Analysts forecast $SHOP revenue growth of +25.5% in 2025 and +20.9% in 2026. Based on this outlook, the valuation using the P/S multiple appears to be trading at a premium compared to other companies in the e-commerce sector.

Analysts expect strong revenue growth, so let's examine the key metrics to determine whether these expectations are justified.

We'll evaluate the company's economic moat, which supports long-term revenue growth, analyze revenue trends and the forecast for next quarter, and identify key factors that could help the company exceed expectations and sustain future growth.

We'll assess the performance of key segments, the launch of new products and updates, customer acquisition growth, key financial metrics, financial stability, and margin trends.

Additionally, we'll review the SBC/Revenue ratio, shareholder dilution, and finally, draw conclusions on the company's outlook.

Economic Moat

Shopify benefits from strong economies of scale, a very strong network effect driven by its 8,000+ app ecosystem, and a recognized brand with 29% U.S. market share. Its proprietary tech, like Shop Pay, offers some IP advantage, though the patent portfolio is moderate. Switching costs are very high, with deep integration and 90%+ retention among large merchants.

Economies of Scale

Shopify benefits from significant economies of scale as one of the largest e-commerce platforms globally, serving over 4.6 million active websites worldwide. This scale allows Shopify to spread fixed costs across a massive merchant base, enabling more competitive pricing while maintaining profitability. The company's R&D investments reportedly dwarf those of competitors, resulting in an unrivaled array of features that keep Shopify at the cutting edge of e-commerce technology. As Shopify continues to grow, particularly in the enterprise sector through Shopify Plus, these scale advantages strengthen, allowing the company to offer increasingly competitive pricing while maintaining healthy margins.

Network Effect

Shopify possesses a strong network effect that creates a self-reinforcing ecosystem. As more merchants join the platform, it attracts more developers, creating a virtuous cycle. The Shopify App Store now features over 8,000 apps, making the platform increasingly valuable to merchants who benefit from this extensive ecosystem. This network effect extends to Shopify's fulfillment network, where increased merchant adoption leads to faster shipping, lower costs, and ultimately better performance for Shopify stores compared to competitors. The B2B segment has experienced six consecutive quarters of over 100% year-over-year GMV growth, further strengthening this network effect as more wholesale businesses join the platform.

Brand

Shopify has established a powerful brand identity synonymous with reliable, user-friendly e-commerce solutions. The company's reputation for enabling merchant success has made it the go-to platform for businesses looking to establish an online presence. This brand strength is particularly evident in Shopify's ability to attract larger merchants like Reebok and Barnes & Noble to its Shopify Plus offering. The brand's value proposition of empowering businesses of all sizes has resonated strongly in the market, with Shopify now commanding approximately 10% of the global e-commerce software market and an impressive 29% of the e-commerce platform market in the United States.

Intellectual Property

While Shopify's intellectual property moat is not as strong as its other competitive advantages, the company has developed valuable proprietary technology that powers its platform. Shopify's continuous innovation in areas such as payment processing (Shop Pay), which outpaces competition by up to 36% in conversion rates, represents significant intellectual property value. The company's development of AI-powered tools for personalized shopping experiences, inventory management, and merchant insights creates additional proprietary assets that competitors cannot easily replicate. However, compared to other tech giants, Shopify's patent portfolio is less extensive, making this a moderate rather than strong moat.

Switching Costs

Shopify has created exceptionally high switching costs for merchants, perhaps its strongest moat. Merchants invest substantial time and resources into setting up their Shopify stores, integrating third-party apps, and customizing their sites. As Shopify serves as an all-in-one solution handling everything from inventory management to payment processing, marketing, and analytics, it becomes deeply embedded in merchants' operations. These multiple touchpoints across an organization make switching to another provider extremely difficult, costly, and time-consuming. For larger merchants, these switching costs are even higher, resulting in retention rates that reportedly exceed 90% according to some investment research.

Revenue growth

Revenue growth for $SHOP Shopify accelerated to +31% YoY in Q4. Based on the forecast for the next quarter, if the company exceeds its guidance by 0.8%, as it did in Q4, Q1 growth would reach 26.8%. This would indicate a slowdown in revenue growth, though still higher than the growth rate in Q3 2024.

Segments and Main Products

Shopify serves a wide range of customers, including small businesses, mid-sized companies, enterprise clients, dropshippers, and service providers. The platform supports entrepreneurs building their first online store, scaling brands expanding digital operations, and large enterprises managing complex e-commerce infrastructures.

The core product is Shopify’s e-commerce platform, built on a SaaS model. Merchants can launch and manage online stores without coding, using customizable templates and drag-and-drop tools.

Merchant services form another key revenue stream. Tools like Shopify Payments handle transactions, while Shopify Shipping supports order fulfillment. Merchants manage operations from a single dashboard, increasing efficiency.

Shopify Plus targets high-volume merchants, offering greater customization, automation, and integration with social media platforms. It serves brands needing advanced e-commerce capabilities at scale.

The Shopify App Store includes over 13,000 third-party applications, enabling merchants to add features for inventory, marketing, and customer support. This ecosystem strengthens Shopify’s network effect and platform stickiness.

B2B commerce tools are a fast-growing segment. Shopify now supports wholesale experiences with custom pricing, discount structures, and flexible payment terms tailored to business buyers.

Shopify’s Point of Sale (POS) system enables merchants to operate across both online and physical stores, ensuring a unified commerce experience across all customer touchpoints.

Main Products Performance in the Last Quarter

$SHOP Shopify revenue breakdown by segment: Merchant Solutions accounts for 76% of total revenue, while Subscription Solutions makes up 24%.

Merchant Solutions revenue grew by +32.6% YoY. The gross margin for this segment was 38.2%, slightly down from 39.2% a year earlier.

More importantly, Subscription Solutions revenue grew +26.9% YoY, a bit slower than overall revenue growth. However, this segment is highly profitable, with a gross margin of 79.9%, down from 81.5% in the same quarter last year.

Subscription Solutions

Revenue grew +27% YoY in Q4, driven by merchant growth, higher platform fees, and the impact of pricing changes. MRR rose +24%, with Plus still accounting for 33%. Growth was seen across Standard, Plus, and Offline. A headwind in Q4 was the transition from 1-month to 3-month paid trials, which reduced short-term MRR but improves merchant durability and GMV over time. Despite the slower near-term revenue from this change, Shopify expects better long-term outcomes from stronger merchant engagement.

Merchant Solutions

Q4 revenue increased +33% YoY, supported by +26% GMV growth and expanding payments adoption. Gross payments volume (GPV) hit $61 billion, up 35% YoY, with Shopify Payments penetration reaching 64%. Strength came from the adoption of value-added services like Capital, Tax, and Markets. International growth was also a key factor, especially in EMEA (+37%). Merchant Solutions take rate outperformance was supported by scale in enterprise and increased GPV from Shop Pay. Gross margin was impacted slightly by lower non-cash revenue from partnerships and expanded PayPal integration.

Shop Pay

GMV processed through Shop Pay reached $27 billion in Q4, up +50% YoY, and now makes up 41% of GPV. It processed 2x more GMV than the next leading accelerated checkout. Growth was fueled by adoption from major brands like Crocs and GameStop. The Shop Pay Commerce Component saw 20x YoY GMV growth, acting as a strong entry point for enterprise brands. Conversion improvements and widespread buyer trust are reinforcing Shop Pay as a competitive moat.

Shopify App Store

The App Store grew significantly, adding over 3,000 new apps in 2024, with more than 16,000 apps total by year-end. 675+ apps were part of the Built for Shopify program. Shopify paid $1 billion to partners in 2024, emphasizing the ecosystem's scale. The integration of partners like Roblox, Oracle, YouTube, and PayPal further deepened the App Store’s reach. The store continues to be a critical growth and retention lever, particularly for scaling mid-market and enterprise merchants.

Product Innovation and New Features

In 2024, Shopify introduced major updates across all merchant segments. Variant limits were raised to 2,000 for complex catalogs. Shopify Balance for Plus brought next-day payouts and improved credit products. Shopify Tax expanded to the U.K. and EU. Tap to Pay and enhanced order management features were introduced in Offline. Shop App added cart syncing and personalized feeds, driving +84% native GMV YoY.

AI played a growing role. Sidekick, Shopify’s AI assistant, along with semantic search and AI-enhanced support tools, improved merchant productivity. Internally, AI enabled more efficient customer support and development.

Offline POS expanded to 8 new countries and Shopify Payments integrated Klarna in Europe. POS now supports up to 1,000 retail locations, a milestone for enterprise.

Market Leader

$SHOP is a Gartner Leader, recognized for its seamless connectivity, integrating with custom code and third-party systems. It offers flexibility, supporting full-stack, headless, and composable commerce. Shopify continues to drive innovation with cutting-edge commerce technology. Its cost efficiency stands out, providing more native capabilities at lower costs compared to BigCommerce Enterprise.

Customers

Large Customer Wins

Enterprise momentum accelerated in Q4, with major global brands choosing Shopify for unified commerce. New wins included Reebok, Champion, BarkBox, and Westwing, which launched on the platform during the quarter. Shopify expanded into the luxury fashion segment with the onboarding of Karl Lagerfeld, which will run over 70 POS locations globally on Shopify.

In the footwear segment, three major brands—ALDO, Sperry, and Call It Spring—signed agreements to move both their online and offline operations to Shopify, representing over 400 physical locations. Initially drawn in via the Shop Pay commerce component, these brands later opted for full platform integration, reflecting the growing success of Shopify’s land-and-expand strategy.

Enterprise retailers such as Warner Music Group, David’s Bridal, Dooney & Bourke, and Uncommon Goods also joined in Q4. Each reflects broader industry confidence in Shopify’s product maturity and value proposition. This traction was visible across geographies, with new additions in the Asia-Pacific region and Europe, and across verticals, including health, beauty, apparel, and entertainment.

Shopify's continued adoption by top-tier sports franchises was highlighted by FC Barcelona’s expansion beyond online to unified commerce and POS. Shopify now powers global teams such as Real Madrid, LA Lakers, Miami Heat, Red Bull Racing, and Team Liquid, establishing brand authority in high-visibility markets.

Customer Success Stories

Enterprise brands that initially adopted a single Shopify component are scaling into full-stack adoption. Everlane, which began with Shop Pay 15 months ago, expanded its relationship by transitioning more of its business to Shopify’s broader ecosystem in Q4. The shift demonstrates increasing confidence in Shopify’s scalability and performance at higher volumes.

The Shop Pay commerce component is proving effective in opening doors to enterprise. Crocs and GameStop adopted the component during Q4. In many cases, the component serves as a wedge to deeper engagement with the full platform, creating a long-term conversion path for high-GMV retailers.

In the offline retail space, Shopify supported the launch of SKIMS’s first NYC store and Beams’ first pop-up store. A new Ernst & Young report confirmed Shopify POS reduces total cost of ownership by 22% and implementation time by 20%, a value proposition that continues to attract enterprise retailers with multi-location footprints.

In B2B, GMV grew +132% YoY in Q4, marking the sixth straight quarter of 100%+ YoY growth. November 2024 recorded the highest monthly B2B GMV ever. Shopify’s inclusion in the Forrester Wave for B2B solutions further reinforces credibility and positions it to serve wholesale alongside DTC from a unified platform.

Across online, offline, and B2B, Shopify is building a platform that enterprises trust for rapid deployment, strong ROI, and long-term scalability. The Q4 customer momentum shows that Shopify is no longer just a solution for startups—it's becoming an operating system for commerce at scale.

Key Metrics

$SHOP Shopify Company Metrics Explained: GMV, GPV, MRR, and Attach Rate. Starting with GMV—Gross Merchandise Volume is a key metric for Shopify, representing the total dollar value of merchandise sold through its platform over a given period. GMV growth indicates rising adoption of Shopify by merchants and overall expansion in e-commerce activity across its user base.

GMV growth accelerated from +10% YoY in Q3 2022 to +26% in Q4 2024.

Next, let's look at GPV for $SHOP Shopify. Gross Payments Volume (GPV) measures the total dollar value of transactions processed through Shopify Payments. This service enables merchants to accept credit cards and other payment methods directly on their Shopify stores.

GPV is a key indicator of the adoption and effectiveness of Shopify’s integrated payment solutions, as it reflects the volume of commerce processed on the platform that generates transaction-based revenue.

GPV growth accelerated from +30% YoY in Q2 2024 to +32% in Q4 2024.

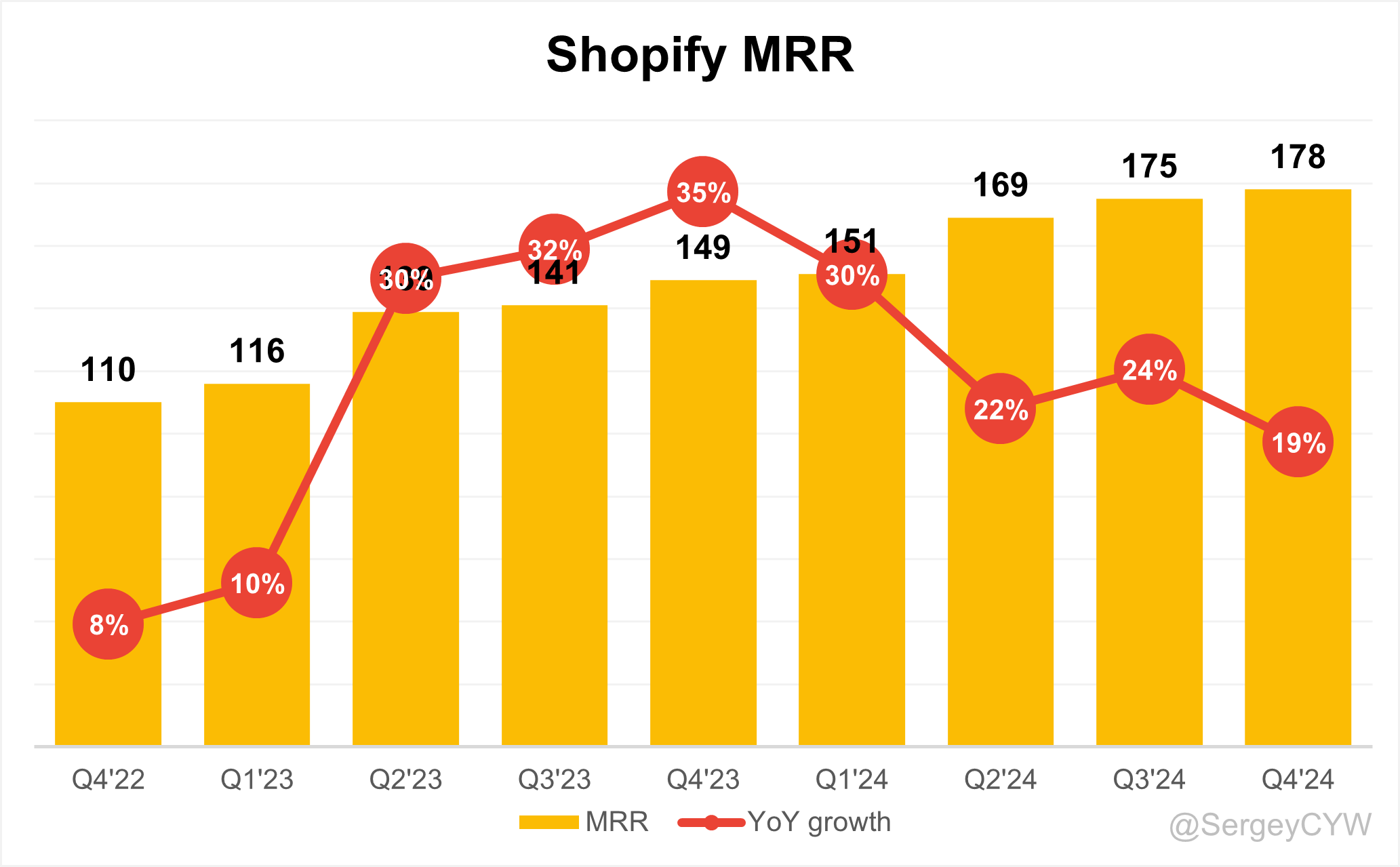

Now, let's look at MRR for $SHOP Shopify. Monthly Recurring Revenue (MRR) is a key metric for Shopify’s Subscription Solutions, reflecting the total recurring revenue generated from subscription plans on a monthly basis. MRR is important for assessing the stability and predictability of Shopify’s revenue from its tiered subscription offerings.

MRR growth signals an increasing number of merchants subscribing and maintaining their plans, contributing to a consistent revenue stream.

MRR growth accelerated from +8% YoY in Q3 2022 to +35% in Q4 2023, but slowed to +19% YoY in Q4 2024.

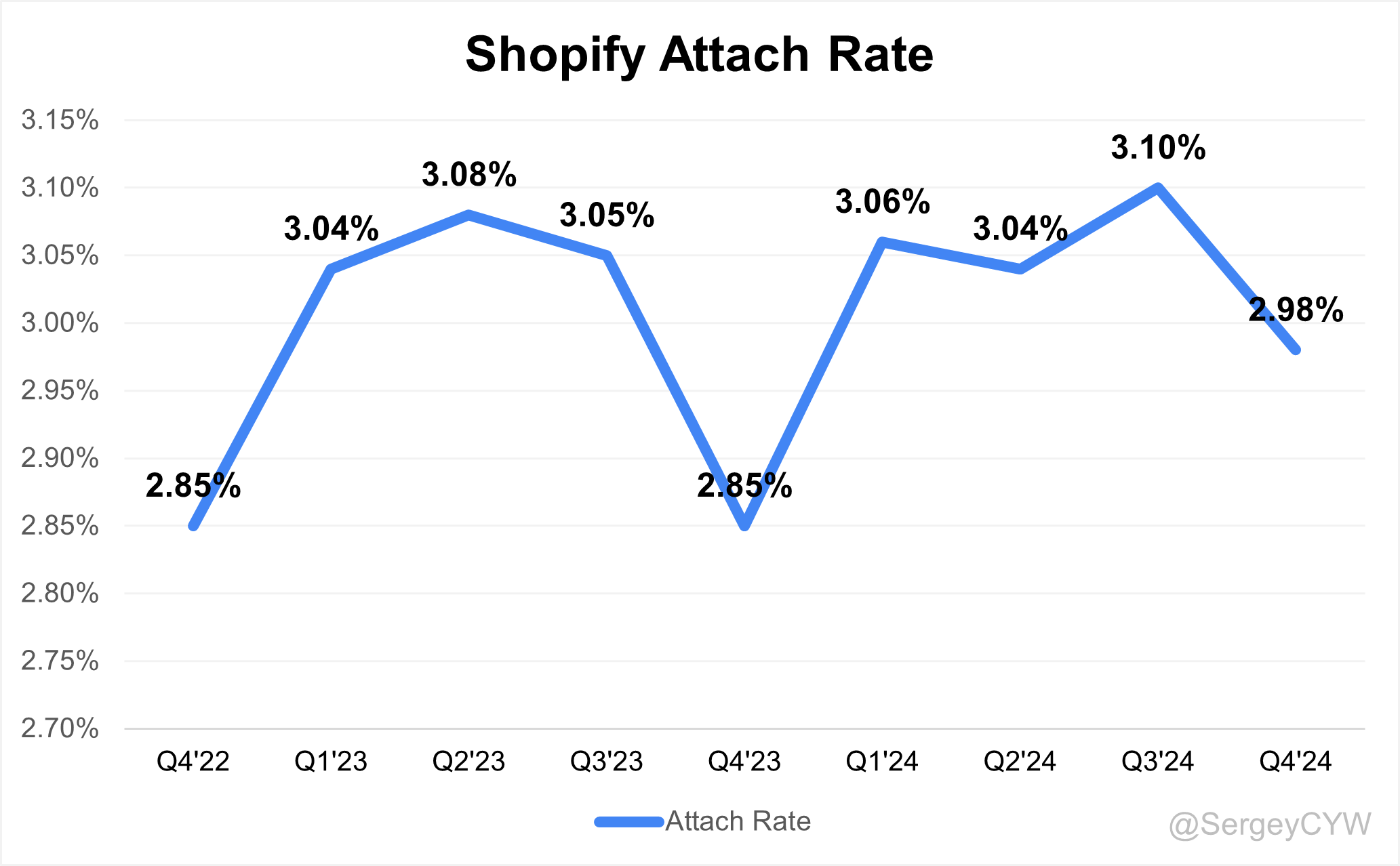

Lastly, let's consider the attach rate for $SHOP Shopify. The attach rate refers to the percentage of Shopify merchants who adopt additional services beyond the basic subscription. This includes Shopify Payments, Shopify Shipping, Shopify Capital, and advanced apps.

It’s a key indicator of product adoption and monetization depth. The attach rate is currently at a strong level of 2.98%, up from 2.85% in Q4 2023 and Q4 2022, Q4 - seasonally weaker quarter.

Profitability

Over the past year, $SHOP Shopify's margins have shifted:

· Gross Margin decreased from 49.7% to 48.1%.

· Operating Margin increased from 18.5% to 20.8%.

· Free Cash Flow (FCF) Margin improved from 20.8% to 21.7%.

The company also achieved GAAP profitability in Q2 2024.

Operating expenses

$SHOP non-GAAP operating expenses have gradually decreased, driven by reductions in S&M, R&D, and G&A spending. Sales & Marketing (S&M) expenses declined from 16% two years ago to 12%.

R&D expenses also dropped from 19% to 10% over the same period, but remain at a relatively high level, enabling continuous product innovation.

General & Administrative (G&A) expenses have decreased to 3%.

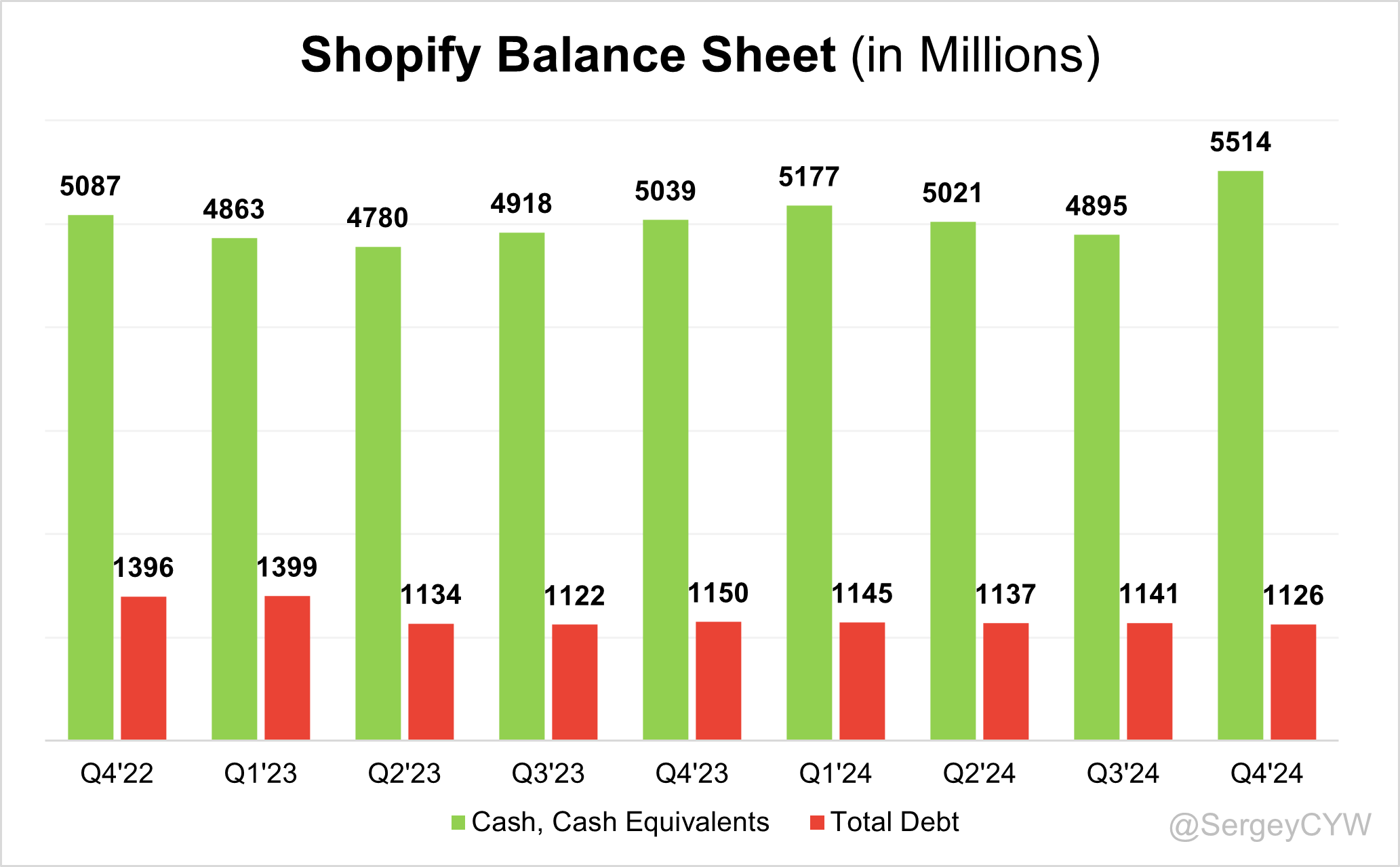

Balance Sheet

$SHOP Balance Sheet: Total debt stands at $1,126 million, while Shopify holds $5,514 million in cash and cash equivalents, far exceeding its liabilities and reflecting a healthy balance sheet.

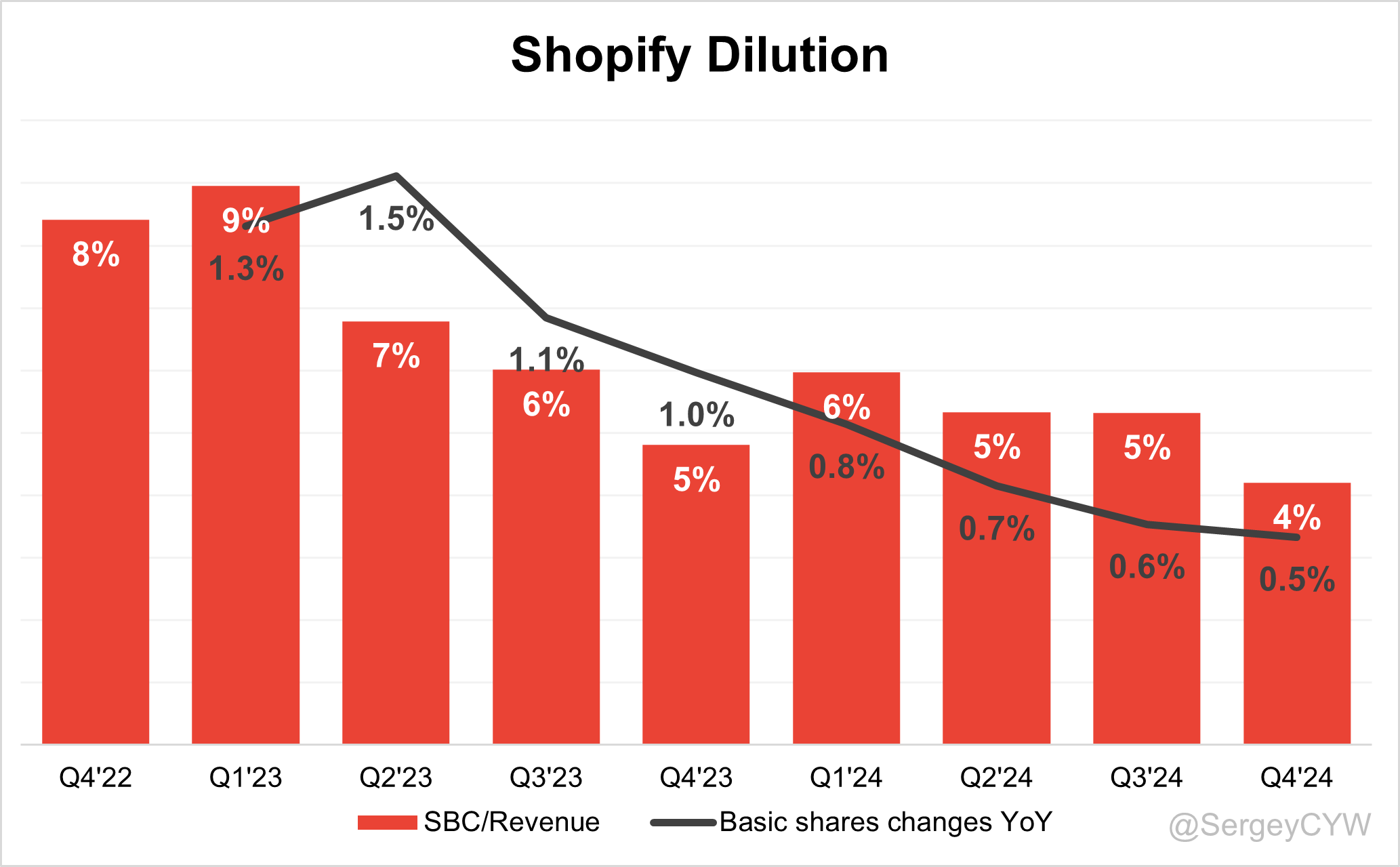

Dilution

$SHOP Shareholder Dilution: Shopify’s stock-based compensation (SBC) expenses have declined to 4% of revenue, which is a low level for SaaS companies.

However, shareholder dilution remains well-controlled, with the weighted-average number of basic common shares outstanding increasing by just 0.5% YoY.

Conclusion

$SHOP has been highly innovative and is strengthening its position through increased investment in R&D.

The company’s margins are improving, supported by strong growth in Merchant Solutions and continued expansion in the high-margin Subscription Solutions segment. Growth in Merchant Solutions has also accelerated.

Key Performance Indicators (KPIs) show positive momentum. GMV (Gross Merchandise Volume) and GPV (Gross Payment Volume) accelerated in the last quarter and remain strong. MRR (Monthly Recurring Revenue) growth slightly slowed in Q4 but remains at a high level. The Attach Rate is elevated, indicating that Shopify is increasing its competitive edge.

The revenue growth forecast for the next quarter suggests a slight decline compared to Q4 but remains above Q3 2024 levels and continues to reflect strong performance.

Shopify trades at a premium valuation based on Forward EV/Sales and Forward P/E multiples, but its competitive advantage and strong management justify the pricing.

The company has exited its low-margin logistics operations and is now focused on high-margin subscription solutions, where gross margins are rising and their contribution to total revenue is increasing.

In January 2025, after valuation multiples normalized, I slightly increased my position. $SHOP now represents 7.8% of my portfolio.