Shopify Q1 2025 Earnings Analysis

Dive into $SHOP Shopify’s Q1 2025 earnings with review of financial performance, key metrics, operating expenses, dilution, customer growth, future outlook

Financial Results:

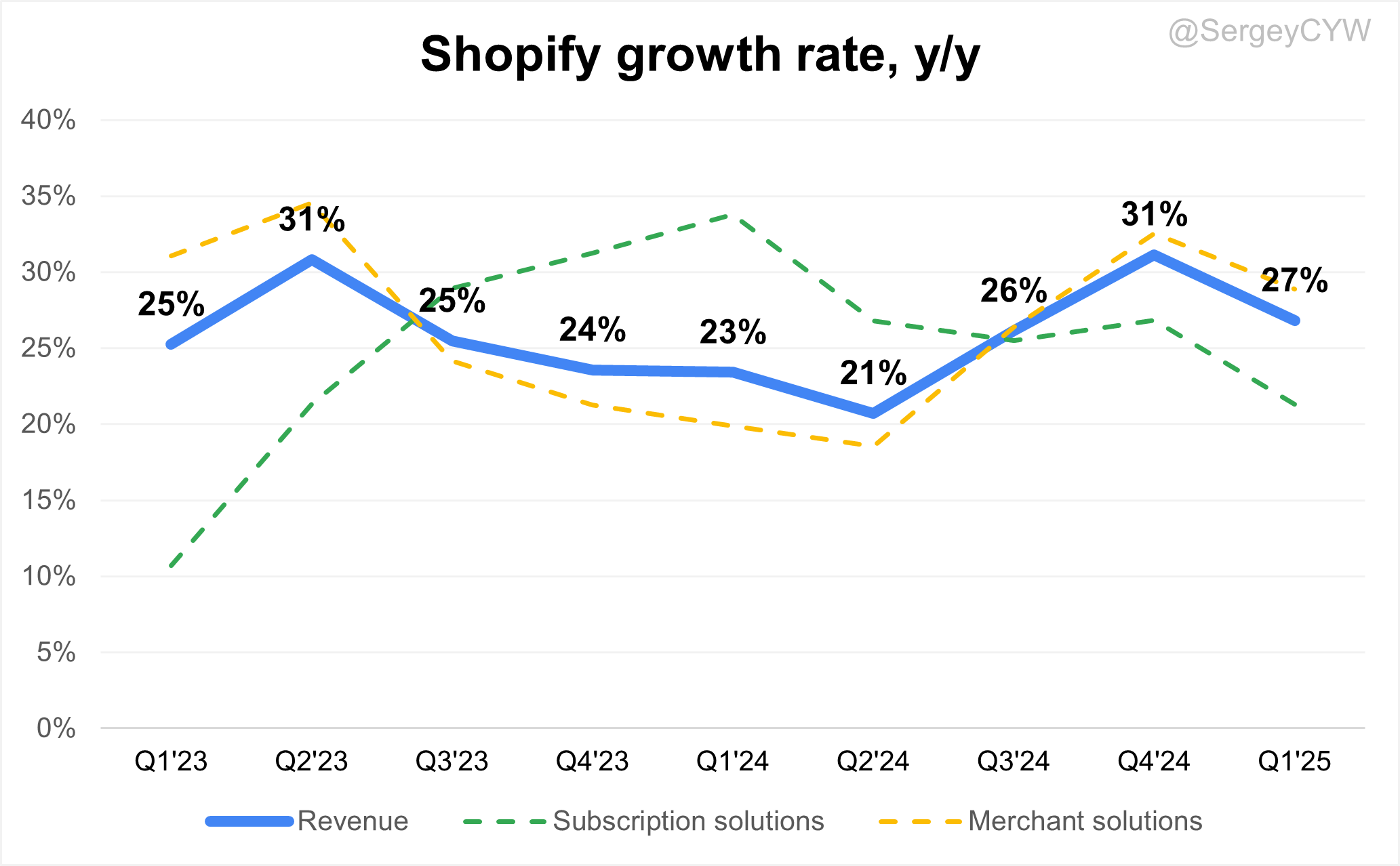

↗️$2,360.0M rev (+26.8% YoY, +31.2% LQ) beat est by 1.2%

↘️GM* (49.5%, -2.2 PPs YoY)🟡

➡️Operating Margin* (13.9%, +3.1 PPs YoY)

➡️FCF Margin (15.4%, +2.9 PPs YoY)

↘️Net Margin (-28.9%, -14.2 PPs YoY)🟡

↘️EPS* $0.25 missed est by -3.8%

*non-GAAP

Segment Revenue

➡️Subscription solutions $620M rev (+21.3% YoY, 80.2% Gross Margin)🟡

↗️Merchant solutions $1,740M rev (+28.9% YoY, 38.6% Gross Margin)

Key Metrics

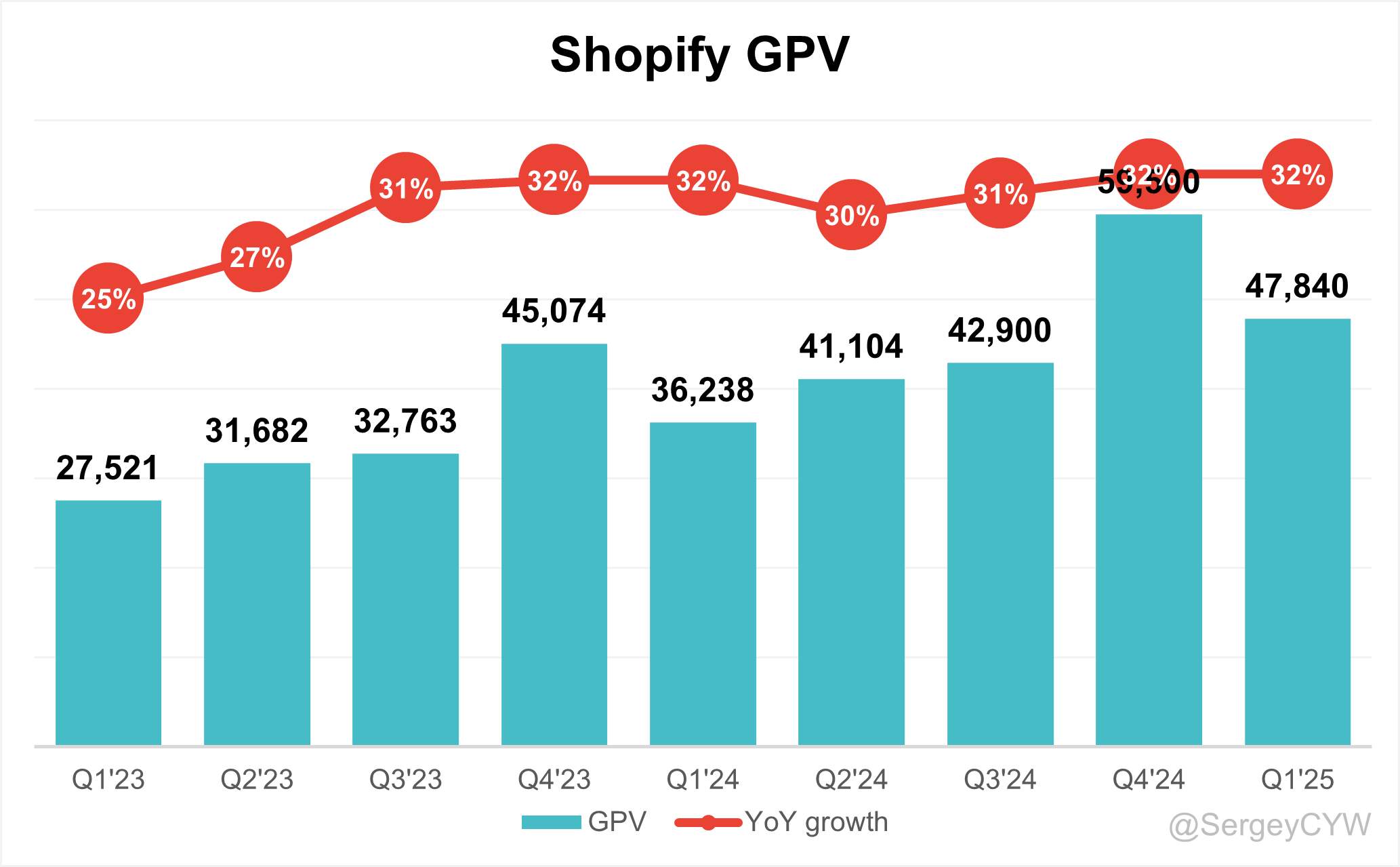

➡️GMV $74.75B (+22.8% YoY)🟡

↗️GPV $47.84B (+32.0% YoY, 64.0%% of GMV)🟢

➡️MRR 182B (+20.5% YoY)🟡

Operating expenses

↘️S&M*/Revenue 16.6% (-2.1 PPs YoY)

↘️R&D*/Revenue 12.4% (-1.7 PPs YoY)

↘️G&A*/Revenue 3.6% (-1.7 PPs YoY)

Dilution

↗️SBC/rev 5%, +1.0 PPs QoQ

↗️Basic shares up 0.6% YoY, +0.1 PPs QoQ🟢

↗️Diluted shares up 0.6% YoY, +0.0 PPs QoQ🟢

Guidance

↗️Q2'25 $2,540.0 - $2,570.0M guide (+24.9% YoY) beat est by 1.9%

Key points from Shopify’s First Quarter 2025 Earnings Call:

Financial Performance

Shopify reported a strong Q1 2025 with revenue up +26.8% YoY to $2.36B, beating estimates by 1.2%. Gross profit reached $1.17B (+22% YoY), while free cash flow was $363M, representing 15% of revenue. Operating income grew to $203M (9% margin), up from 5% a year ago, showing improved leverage. GMV was $74.8B (+23% YoY), driven by strong same-store sales, merchant growth, and international momentum. It was Shopify’s eighth consecutive quarter with revenue growth above 25% and seventh straight quarter of GMV growth over 20%.

Subscription Solutions

Subscription revenue grew +21% YoY, supported by new merchant additions and Shopify Plus pricing changes implemented in February for new customers. Monthly Recurring Revenue (MRR) rose +21%, with Plus plans contributing 34% of total MRR. Most existing Plus merchants locked in three-year contracts at legacy pricing, delaying full monetization.

The shift from one-month to three-month trials created near-term MRR comparison complexity but improved retention and long-term GMV. Gross margin remained near 80%, slightly compressed by higher infrastructure costs tied to usage and international scaling. AI investment had no material impact on Q1 gross margin, though efficiencies are expected over time.

Merchant Solutions

Revenue from Merchant Solutions rose +29% YoY, outpacing Subscription Solutions. Growth was driven by GMV expansion and deeper Shopify Payments penetration, which hit 64%. This was supported by international rollout, rising Shopify Plus usage, and partnerships with PayPal and Klarna.

Gross margin declined to 38.6% from 40.1% YoY, due to the increased mix of lower-margin payment revenue, the expiration of non-cash revenue from prior partnerships, and accounting impacts from PayPal. Adjacent services such as tax, FX, and capital saw continued growth. B2B GMV expanded triple digits YoY, indicating successful traction in the segment.

Shop Pay

Shop Pay processed $22B in GMV, growing +57% YoY, with strong adoption across SMB and enterprise. New customers included Birkenstock, Johnny Was, Purple, and Lily Pulitzer. Expansion into Tapestry’s portfolio (Coach, Kate Spade) reinforced its value as a conversion driver. Shop Pay Installments launched in Canada, with further global rollout planned.

Shop App

Native GMV through the Shop App grew +94% YoY, accelerating from +84% in Q4 2024. Shopify launched a “buy local” filter in response to tariff concerns, rolled out in under one week, generating hundreds of thousands of user sessions. Early integration of Shop Pay Installments also began during Q1. The app continues to drive buyer engagement and support merchant adaptation during trade uncertainty.

Product Innovation

Shopify responded rapidly to tariff shifts with new tools. It cut duties calculation pricing to 0.5%, doubling adoption between January and March. Introduced duty-inclusive pricing, allowing for transparent international checkout. Released TariffGuide.ai, an AI tool that calculates duty rates by product description and origin. Added prepaid DDP shipping labels and expanded 3PL access through the Fulfillment Network app.

Offline and B2B Growth

Offline GMV rose +23% YoY, led by multi-location brands such as FAO Schwarz, Grand Seiko, and Just Cozy. Same-day delivery was launched for Alo Yoga via integration with Uber and DoorDash. B2B GMV posted triple-digit YoY growth, highlighting strong early traction in business commerce.

Enterprise Adoption

Enterprise growth accelerated as Shopify continued displacing legacy and in-house platforms. VF Corp signed to onboard 8 brands, including JanSport, Dickies, and Kipling. Follett Higher Education, managing 1,000+ college stores, joined amid tariff uncertainty.

In Europe, Caring Beauty (part of Kering, which owns Alexander McQueen and Creed) adopted Shopify to unify B2C, B2B, and POS. Other new launches included JW Anderson (LVMH), Paper Source, Therabody, Away, Kent Automotive, and Life is Good.

Enterprise success was supported by Shop Pay and POS adoption, with additional tools layered over time. Existing clients like BarkBox, Brilliant Earth, and Toys R Us contributed to offline GMV strength.

International Growth

International GMV grew +31% YoY, with Europe up +36%, led by the UK, Germany, and Netherlands. Shopify Payments expanded from 23 to 39 countries, nearly doubling market coverage. Multi-currency payouts launched across 20 European markets, enhancing merchant flexibility and FX efficiency.

Gross Margin Compression

Total gross margin declined to 49.5% from 51.4% YoY, due to mix shift toward lower-margin Merchant Solutions, PayPal-related accounting, and increased infrastructure costs. Subscription Solutions maintained margin stability near 80%, with slight pressure from cloud and hosting scale. Shopify reiterated margin consistency across a five-year horizon, with no major AI-related drag in Q1.

Tariff Exposure

Only ~1% of GMV was tied to China imports previously covered by U.S. de minimis exemptions. Shopify reported no material impact on GMV post-expiration. Strong performance continued through April and early May, supported by a buyer base in which over 50% of U.S. consumers earn more than $100K, offering insulation from price sensitivity.

Outlook

For Q2 2025, Shopify expects revenue growth in the mid-20s% YoY, with gross profit dollar growth in the high teens. Free cash flow margin is projected to remain in the mid-teens, and operating expenses to be 39–40% of revenue, reflecting continued leverage.

The company will continue prioritizing AI, global expansion, B2B features, and enterprise scaling while maintaining strict discipline in marketing and hiring.

Management comments on the earnings call.

Product Innovations

Harley Finkelstein, President

“We rolled out the Shop App filter in less than a week and the duties calculation checkout update over a weekend. Literally, the weekend after the tariff changes were announced, the team got to work. And by Sunday evening, we were testing it for production.”

“Our obsession with unlocking every opportunity and filling every important gap in the system to give our merchants the best chance of success is one of our superpowers.”

Jeff Hoffmeister, Chief Financial Officer

“This acquisition is one piece of a broader strategy to ensure that our merchants are able to continue meeting buyers regardless of where they’re shopping or discovering great products.” (on the acquisition of Vantage Discovery to enhance AI-powered search)

Subscription Solutions

Jeff Hoffmeister, Chief Financial Officer

“Over the past five years, the gross margin for Subscription Solutions has centered around 80%, plus or minus a couple hundred basis points in any given quarter, and we do not anticipate that trend changing in the near term.”

“As I mentioned on our last call, we expect our Subscription Solutions growth to normalize to a rate lower than Merchant Solutions in 2025, given the benefits from the Plus pricing changes tapering off and the lengthening of the paid trials.”

Merchant Solutions

Jeff Hoffmeister, Chief Financial Officer

“Merchant Solutions revenue increased 29%, driven by the same factors as Q4, including continued strength in GMV and increased penetration of Shopify Payments, which reached 64% for the quarter.”

“We did have a little bit of impact from the falloff of the non-cash revenue. One of those did roll off in Q4. That would be a one-time or just Q4 to Q1 adjustment.”

Shop Pay

Harley Finkelstein, President

“One of the biggest advantages to our merchants is access to Shop Pay. And in Q1, Shop Pay GMV was up 57% from last year, processing over $22 billion in GMV.”

“This is more than just a passing trend. It is becoming an increasingly compelling pathway for large merchants to come to Shopify.”

Enterprise & Large Customers

Harley Finkelstein, President

“Many legacy commerce platforms are actually being exposed as pretty slow and pretty restrictive. Some of these older systems can’t even handle basic tasks like price updates or loyalty changes.”

“Large retailers and brands with custom-built or in-house platforms are realizing those platforms are just as brittle and slow… so as a result, brands are moving to Shopify at even higher clip.”

“We’ve had some of the most iconic retailers and brands on the planet come to Shopify in the last quarter, and that pipeline has not slowed down at all.”

International Growth

Jeff Hoffmeister, Chief Financial Officer

“Within Europe, we are outperforming the market by an even wider margin at even higher multiples of e-commerce growth. We’ve seen robust greater than 30% GMV growth now for eight consecutive quarters.”

Harley Finkelstein, President

“Adding more products in more markets remains a key driver of our international growth. And with these country launches, even more merchants can process payments seamlessly in their home countries.”

Challenges

Harley Finkelstein, President

“We have merchants everywhere of all sizes across pretty much every geography and pretty much every vertical… exposure really does vary by merchant, but net-net, we’re not seeing any meaningful impact on GMV.”

Jeff Hoffmeister, Chief Financial Officer

“The recent expiration of the de minimis exemption for goods from China is not expected to have a meaningful impact on Shopify in the near term, as only 1% of our overall GMV is related to imports from China that were subject to the exemption.”

“While some merchants have raised prices, we haven’t seen broad-based price increases yet.”

Future Outlook

Jeff Hoffmeister, Chief Financial Officer

“Our expectations for the second quarter of 2025 factor in the strength of our Q1 and what we are seeing quarter to date for Q2.”

“We expect Q2 revenue growth in the mid-twenties year over year… We expect Q2 free cash flow margin to be in the mid-teens, similar to Q1.”

Harley Finkelstein, President

“It is quite simple. Our success boils down to three key principles. First, everything we do is merchant first. Second, we’ve demonstrated an incredible ability to pivot. Third, our operating discipline provides the flexibility we need to deliver unmatched value while balancing profitability and long-term growth.”

“I think these days for us are just like anything else. And our objective in these times is to shoulder complexity so our merchants don’t have to.”

Thoughts on Shopify Earnings Report $SHOP:

🟢 Positive

Revenue grew +26.8% YoY to $2.36B, beating estimates by 1.2%

Free cash flow margin reached 15.4% (+2.9pp YoY), maintaining profitability

Operating margin expanded to 13.9% (+3.1pp YoY)

GPV rose +32.0% YoY to $47.84B, reaching 64% of GMV

Merchant Solutions revenue increased +28.9% YoY to $1.74B

Shop Pay GMV hit $22B (+57% YoY), with growing enterprise adoption

Shop App native GMV surged +94% YoY, up from +84% in Q4

B2B GMV posted triple-digit YoY growth

International GMV grew +31% YoY, with Europe up +36%

Q2 revenue guidance of $2.54B–$2.57B implies +24.9% YoY, 1.9% above consensus

🟡 Neutral

Subscription Solutions revenue up +21.3% YoY to $620M, with stable 80.2% gross margin

MRR grew +20.5% YoY, with 34% from Plus plans

Operating expenses as % of revenue declined: S&M to 16.6%, R&D to 12.4%, G&A to 3.6%

SBC/revenue increased to 5% (+1pp QoQ), but dilution remained minimal

Product innovation and AI use expanding, but impact on cost structure not yet material

Dilution slightly increased: basic shares up 0.6% YoY, +0.1pp QoQ

Merchant Solutions gross margin fell to 38.6% from 40.1% YoY, but up QoQ

🔴 Negative

Gross margin declined to 49.5% (-2.2pp YoY) due to mix shift to lower-margin services

Net margin was -28.9% (-14.2pp YoY) despite strong top-line growth

EPS missed estimates at $0.25 (-3.8%)

Thank you for reading!

Follow me for more frequent updates on X/Twitter and Threads, and on LinkedIn. For visual infographics, check out Instagram, and for portfolio changes, follow me on SavvyTrader.

Disclaimer: This earnings review is for informational purposes only and does not constitute financial, investment, or trading advice.

Absolutely love what you are doing. Thank you so much. You are awesome.