SentinelOne Q4 2024 Earnings Analysis

Dive into $S SentinelOne’s Q4 2024 earnings with review of financial performance, key metrics, operating expenses, dilution, customer growth, future outlook

Financial Results:

↗️$226M rev (+29.4% YoY, +28.3% LQ) beat est by 1.6%

↗️GM* (79.3%, +1.2 PPs YoY)

↗️Operating Margin* (1.2%, +10.3 PPs YoY)🟢

↗️FCF Margin (-3.9%, +2.2 PPs YoY)

↗️Net Margin (-31.4%, +9.9 PPs YoY)🟢

↗️EPS* $0.04 beat est by 300.0%🟢

*non-GAAP

Key Metrics

➡️DBNR 110%

↗️RPO $1.20B (+33.9% YoY)🟢

➡️Billings $300M (+12.6% YoY)🟡

➡️ARR $0.92B (+27.0% YoY, +60 net new ARR)🟡

Customers

↗️1,411 $100k+ customers (+24.5% YoY, +101)

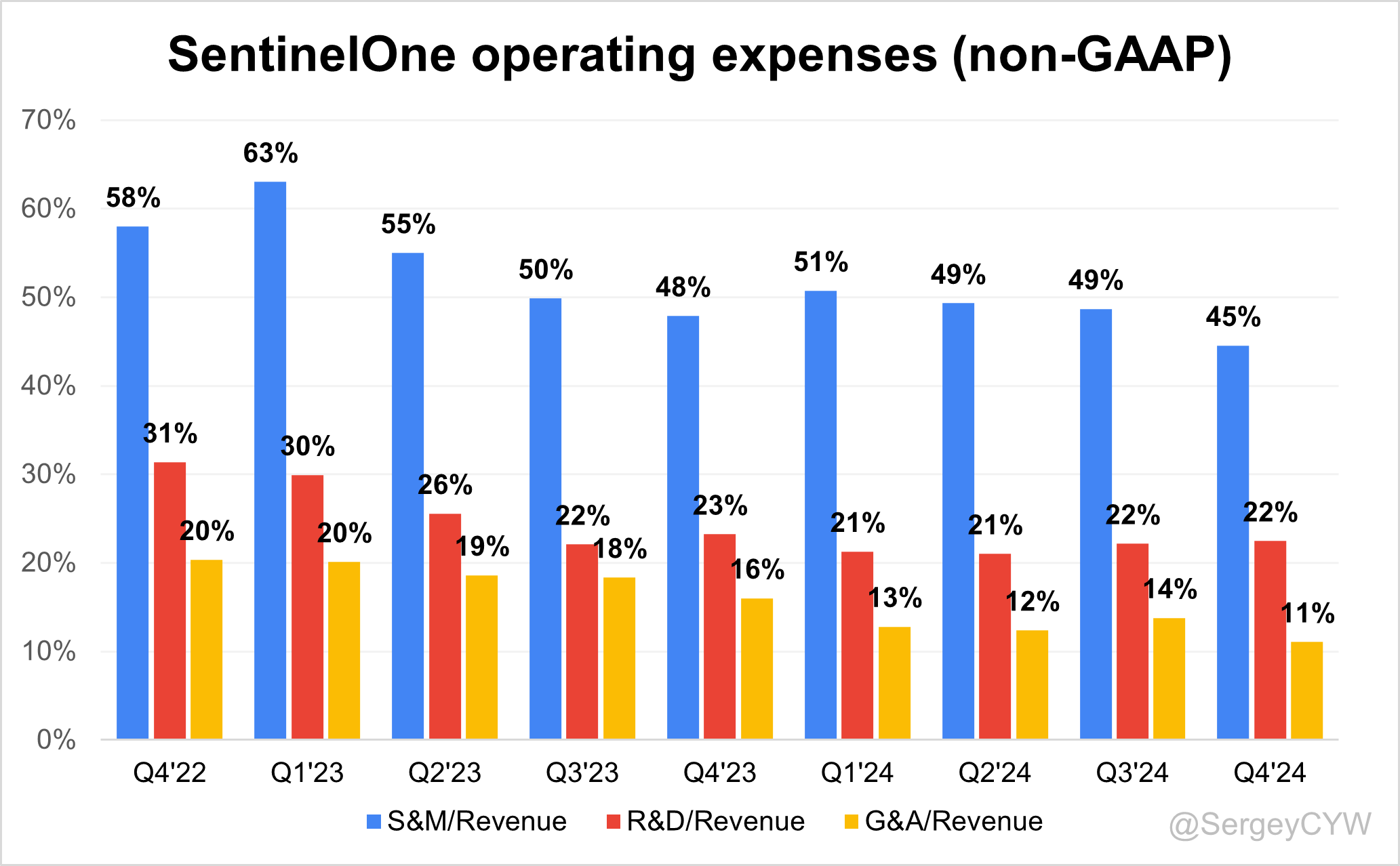

Operating expenses

↘️S&M*/Revenue 44.5% (-3.3 PPs YoY)

↘️R&D*/Revenue 22.5% (-0.8 PPs YoY)

↘️G&A*/Revenue 11.1% (-5.0 PPs YoY)

Quarterly Performance Highlights

↘️Net New ARR $60M (-0.2% YoY)

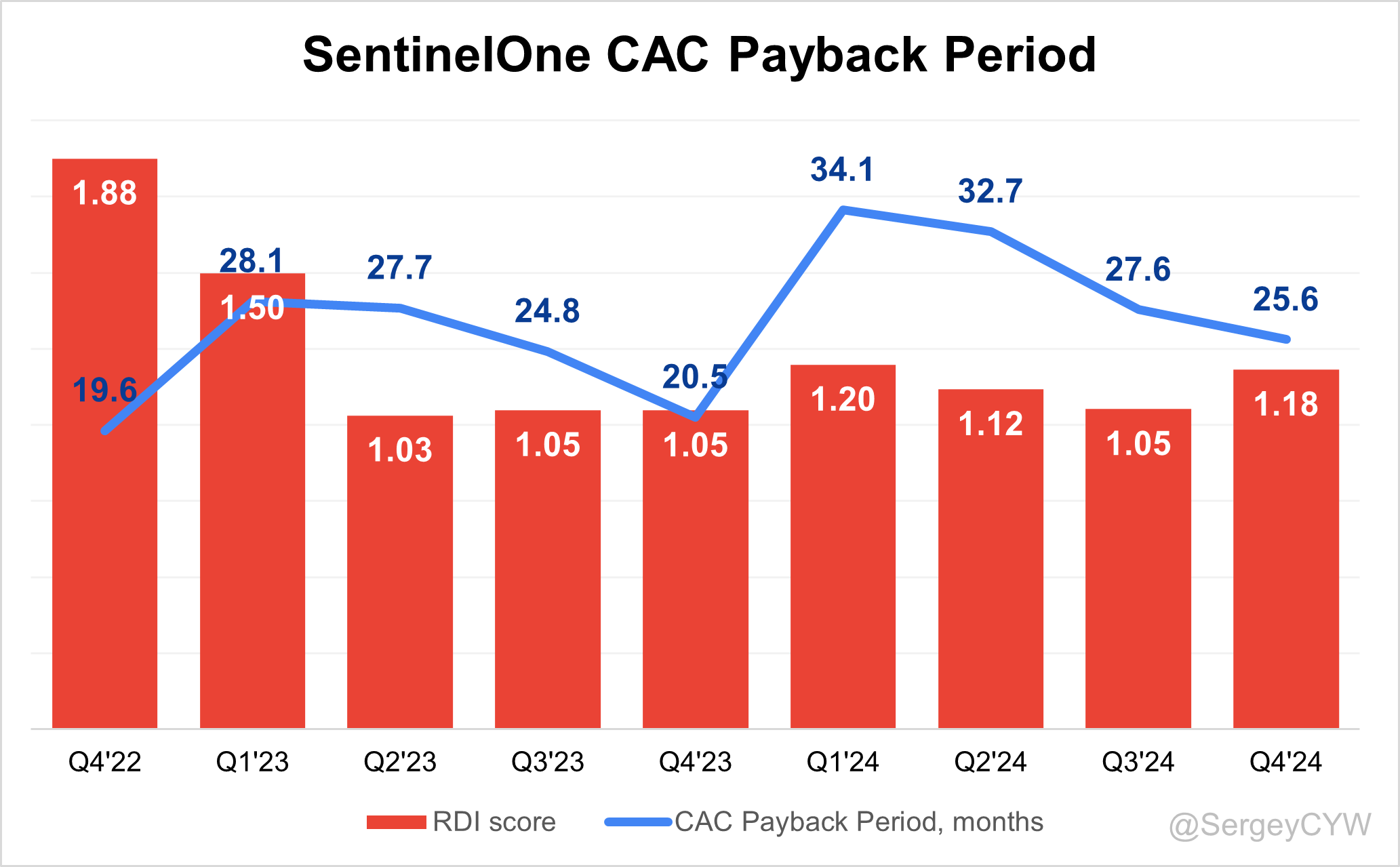

↗️CAC* Payback Period 25.6 Months (+5.1 YoY)🟡

↗️R&D* Index (RDI) 1.18 (+0.13 YoY)🟢

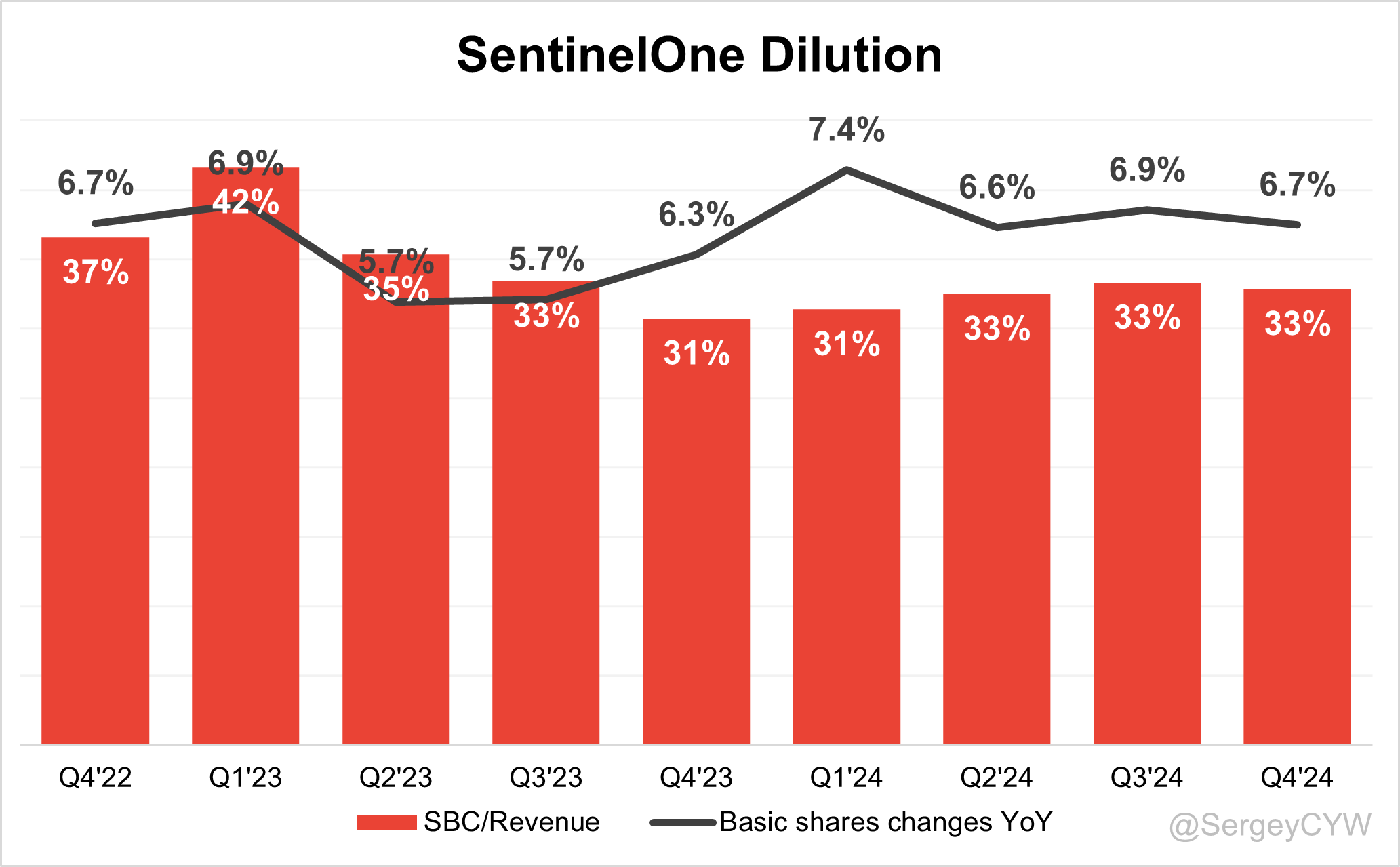

Dilution

↘️SBC/rev 33%, -0.5 PPs QoQ

↘️Basic shares up 6.7% YoY, -0.2 PPs QoQ🔴

↘️Diluted shares up 12.5% YoY, -0.5 PPs QoQ🔴

Guidance

↘️Q1'25 $228.0M guide (+22.3% YoY) missed est by -3.3%🔴

↘️$1,007.0 - $1,012.0M FY guide (+22.9% YoY) missed est by -2.0%🔴

Key points from SentinelOne Fourth Quarter 2024 Earnings Call:

Financial Performance

SentinelOne closed FY25 with $821M in revenue, up 32% YoY. Q4 revenue reached $226M, growing 29% YoY, exceeding expectations. ARR grew 27% YoY to $920M, with $60M in Q4 net new ARR.

Gross margin hit a new high, and operating margin improved 16 percentage points YoY. SentinelOne reported its first full-year positive net income and free cash flow, achieving positive operating income in Q4 ahead of expectations.

RPO increased 30% YoY, hitting $1.2B, signaling strong future revenue. International revenue accounted for 37% of Q4 revenue, up 36% YoY. FY26 operating margin is projected to improve by 650+ bps, targeting 3-4% positive margin.

Singularity Platform

More than 50% of FY25 bookings came from non-endpoint security solutions, reflecting increased demand for cloud security, AI-driven analytics, and identity protection. The modular platform approach led to broader customer adoption, with three+ solution deployments tripling and four+ solution deployments quadrupling.

The platform’s AI-driven automation, real-time processing, and scalability address complex cybersecurity threats. Seamless integrations with Microsoft, Palo Alto Networks, and Zscaler enhance enterprise security.

The largest CNAP deal in SentinelOne history was secured in Q4, strengthening its cloud security presence. The platform earned 2024 Gartner Peer Insights Customer Choice recognition, with 98% customer recommendations.

Purple AI

SentinelOne became the first cybersecurity company to embed generative AI across all security solutions by default. More than 300 AI deployments in Q4 highlight demand for autonomous security.

Purple AI automates threat detection, response, and security operations, improving efficiency while reducing analyst workload. The AI-native approach provides a competitive edge over traditional security vendors.

AI SIEM

Organizations are replacing high-cost, legacy SIEM solutions with SentinelOne’s AI SIEM, which delivers real-time analytics, automation, and cost-efficient security operations.

Q4 saw several major AI SIEM displacements:

Global financial institution replaced Splunk, increasing SentinelOne’s footprint 5x while reducing costs.

Multinational retailer transitioned to AI SIEM, saving $1M annually and cutting incident response time by 12 hours.

Major APAC enterprise closed an eight-figure deal, consolidating endpoint, cloud, and AI SIEM security.

Cost savings and advanced automation continue to drive adoption, reinforcing SentinelOne’s leadership in AI-driven security.

Customer Growth

Direct customers surpassed 14,000, excluding MSSP-served businesses. Customer expansion was driven by enterprise adoption, competitive displacements, and platform expansion.

International revenue grew 36% YoY, contributing 37% of Q4 revenue.

Large Wins

Fortune 100 Airline replaced its incumbent endpoint security vendor after a six-month evaluation, adopting Singularity AI.

Financial institution transitioned from Splunk to AI SIEM, expanding SentinelOne’s footprint 5x and lowering costs.

Retailer replaced a legacy security provider, saving $1M annually and accelerating incident response by 12 hours.

Major APAC enterprise consolidated endpoint, cloud, and AI SIEM under an eight-figure agreement.

Go-to-Market

SentinelOne refined pricing structures to enhance flexibility, increasing multi-module security suite adoption.

SentinelOne strengthened multi-year MSSP contracts, securing higher retention rates and long-term revenue visibility.

Market Share Gains

SentinelOne continued to displace CrowdStrike, Splunk, and other incumbents, capitalizing on AI-native automation and lower total cost of ownership.

Key performance highlights:

MITRE ATT&CK Evaluations: 100% detection for the fifth consecutive year.

Noise Reduction & Speed: 88% fewer alerts than competitors, zero detection delays.

Strategic Partnerships

Multi-year Lenovo partnership expected to scale in future years with increased on-device security adoption.

Expanded integrations with Zscaler, Okta, Palo Alto Networks, and Microsoft broaden SentinelOne’s ecosystem reach.

Macro & Challenges

SentinelOne remains cautious about enterprise spending constraints, citing:

Economic uncertainty & political volatility affecting security budgets.

Federal spending slowdowns prolonging sales cycles.

Delays in AI-driven security transformation initiatives.

FY26 revenue guidance of $1.07B–$1.012B (+23% YoY) accounts for deal timing uncertainties. SentinelOne retired its Deception product, impacting $10M in ARR churn, with half affecting Q1 FY26.

Future Outlook

SentinelOne is set to surpass $1B in revenue and ARR in FY26, fueled by:

AI-powered cybersecurity growth led by Purple AI and AI SIEM.

Platform consolidation, increasing multi-module adoption.

Margin expansion through operating leverage and cost discipline.

Federal, financial services, and large-scale cloud security penetration.

With continued innovation, enterprise expansion, and AI-driven transformation, SentinelOne is positioned for sustained profitable growth in FY26 and beyond.

Management comments on the earnings call.

Product Innovations

Tomer Weingarten, Chief Executive Officer

"Our AI-native autonomous security is fundamentally redefining how cybersecurity challenges are addressed, setting us apart in the industry. We believe every customer should be able to leverage generative AI’s foundational abilities for security applications. The inclusion of Purple AI across our Singularity platform marks a major step forward in transforming cybersecurity with advanced automation."

Barbara Larson, Chief Financial Officer

"We are sharpening our innovation focus toward AI-native data and security solutions. Our disciplined investment strategy ensures that we remain at the forefront of cybersecurity innovation while maintaining strong financial performance."

Singularity Platform

Tomer Weingarten, Chief Executive Officer

"We have successfully transformed our business from an endpoint-focused model to a comprehensive AI-native cybersecurity platform. With more than 50% of our bookings coming from non-endpoint solutions, we have demonstrated our ability to disrupt large markets and redefine security for enterprises."

"Our unified AI security platform integrates endpoint, cloud, identity, and data solutions to deliver real-time protection, automation, and a lower total cost of ownership. This approach allows enterprises to consolidate security operations while gaining best-in-class threat detection capabilities."

Purple AI

Tomer Weingarten, Chief Executive Officer

"Purple AI is already the first and only scaled agentic AI for cybersecurity. By embedding generative AI into every solution by default, we are setting a new standard for security automation. This technology enhances analysts’ capabilities, reduces manual workload, and improves security outcomes in ways that traditional approaches cannot match."

"We are extending the power of Purple AI across a wider range of security data, adding support for third-party solutions including Zscaler, Okta, Palo Alto Networks, Fortinet, and Microsoft. By breaking data silos, we are enabling customers to unleash the full potential of AI-driven security operations."

Competitors

Tomer Weingarten, Chief Executive Officer

"We are seeing customers migrate away from legacy SIEM solutions and modernize their security infrastructure with our AI SIEM. The performance improvements and cost savings we provide are compelling, and enterprises are recognizing the limitations of outdated security architectures."

"Our competitive win rates were strong in Q4, and we continue to take market share from both incumbents and next-gen vendors. The momentum behind our AI-powered platform is driving strategic enterprise engagements and increasing awareness of our differentiated approach to cybersecurity."

Customers

Tomer Weingarten, Chief Executive Officer

"Our customers are choosing us because of our ability to provide real-time, autonomous security that adapts to evolving threats. In Q4, we saw one of our strongest quarters of competitive displacements, including enterprises moving away from legacy endpoint and SIEM vendors."

"A Fortune 100 airline selected us to replace their incumbent security provider, a major financial institution switched from Splunk to AI SIEM, and a global retailer reduced their security costs by over $1 million annually by adopting our platform. These examples illustrate how our AI-driven security approach simplifies operations and delivers measurable value."

Strategic Partnerships

Tomer Weingarten, Chief Executive Officer

"Our long-standing partnerships with managed service providers are built on collaboration and innovation. MSSPs are doubling down on SentinelOne, embracing more of our platform and establishing longer-term contracts. This gives us and our partners greater visibility and predictability into future growth."

"We are also seeing increased interest from managed security, incident response, and insurance providers for our broader platform solutions. More than a dozen large partners adopted AI SIEM, Purple AI, and CNAP in Q4 alone, further validating the value of our platform in the cybersecurity ecosystem."

International Growth

Barbara Larson, Chief Financial Officer

"Revenue from international markets grew 36% year-over-year in Q4 and represented 37% of our total revenue. The demand for our AI-driven security solutions is accelerating globally, and we see continued opportunity for expansion in key international markets."

Macro & Challenges

Tomer Weingarten, Chief Executive Officer

"AI is upending what we know about software and security, and we are evolving as a company to lead in this future. However, we remain mindful of macroeconomic conditions, deal timing, and federal spending uncertainty, which continue to impact enterprise security budgets."

Barbara Larson, Chief Financial Officer

"While the macro environment remains volatile, we believe we have positioned SentinelOne for sustained growth by aligning our investments with high-value areas such as AI, data, and cloud security. Our ability to deliver strong revenue growth and margin expansion despite these headwinds is a testament to the strength of our execution."

Future Outlook

Tomer Weingarten, Chief Executive Officer

"We expect to surpass $1 billion in both ARR and revenue this year—an important milestone in our growth journey. At the same time, we will achieve full-year operating income profitability while continuing to invest in our platform and future opportunities."

"We are leading the next wave of AI-driven cybersecurity, and our investments in AI SIEM, Purple AI, and cloud security are positioning us for long-term success. The opportunity ahead is immense, and we are focused on delivering sustainable, profitable growth while redefining the future of enterprise security."

Thoughts on SentinelOne Earnings Report $S:

🟢 Positive

Revenue: $226M (+29.4% YoY), beating estimates by 1.6%.

Gross Margin: 79.3% (+1.2 PPs YoY).

Operating Margin (Non-GAAP): 1.2% (+10.3 PPs YoY).

EPS (Non-GAAP): $0.04, exceeding estimates by 300%.

RPO: $1.2B (+33.9% YoY), outpacing revenue growth.

$100K+ customers: 1,411 (+24.5% YoY, +101 new customers), the highest addition in the past two years.

Customer wins: Major deals secured, including a Fortune 100 airline, a global financial institution (+5x expansion), and a multinational retailer ($1M annual savings, 12-hour faster detection).

AI Expansion: 300+ Purple AI deployments in Q4.

Market leadership: 100% detection rate in MITRE ATT&CK for the 5th consecutive year, 88% fewer alerts than competitors, zero detection delays.

🟡 Neutral

DBNR: 110%, indicating stable expansion within the customer base.

Net Margin (Non-GAAP): -31.4% (+9.9 PPs YoY), improving but still generating significant losses.

Billings: $300M (+12.6% YoY), growing at a slower pace than revenue.

ARR: $920M (+27% YoY, +$60M Net New ARR), lagging behind revenue growth.

Net New ARR: $60M, down 0.2% YoY.

R&D Spend: 22.5% of revenue, a 0.8 PP YoY decline, showing cost efficiency but lower investment in innovation.

🔴 Negative

FY26 Revenue Guidance: $1.007B–$1.012B (+22.9% YoY), missing estimates by -2.0%.

Q1'25 Revenue Guidance: $228M (+22.3% YoY), -3.3% below estimates.

Customer Acquisition Cost (CAC) Payback: 25.6 months, up +5.1 months YoY, indicating longer ROI on new customers.

Free Cash Flow (FCF) Margin: -3.9%, improving +2.2 PPs YoY but still negative.

Stock-Based Compensation (SBC): 33% of revenue, only -0.5 PPs QoQ reduction.

Share Dilution: Basic shares +6.7% YoY, diluted shares +12.5% YoY.

Deception Product Retirement: $10M ARR churn, with half impacting Q1 FY26.

Nice write up. Do you own it and what are you doing after earnings ? Others holding on after earnings ?