Palo Alto Networks Q4 2023 Earnings Review

$PANW Q4'23 Results:

Financial Results:

⬆️$2,015.2M rev (+21.8% YoY, 20.1% LQ) beat est by 2.3%

⬆️GM* (76.4%, +1.0%pp YoY)

⬆️Operating Margin* (28.0%, +5.2%pp YoY)

↘️FCF Margin 32.5%, -7.2%pp YoY)

⬆️EPS* $1.46 beat est by 12.3%🟢

*non-GAAP

Revenue By Type

Product

➡️$390.7M rev (+10.7% YoY, 3.4% LQ) 🟡

⬆️GM* (78.3%, +5.8%pp YoY)

Subscription and support

➡️$1,584.4M rev (+21.7% YoY, +24.6% LQ) 🟡

⬆️GM* (77.9%, +1.7%pp YoY)

Key Metrics

⬆️RPO $10.80B (+23.0% YoY)

➡️Billings $2,347M (+16.0% YoY)🟡

⬆️NGS ARR $3,490M (+50.0% YoY)

Operating expenses

↘️S&M*/Revenue 29.1% (30.4% LQ)

↘️R&D*/Revenue 15.0% (15.2% LQ)

⬆️G&A*/Revenue 4.4% (4.2% LQ)

↘️Net New ARR $260M ($280 LQ)

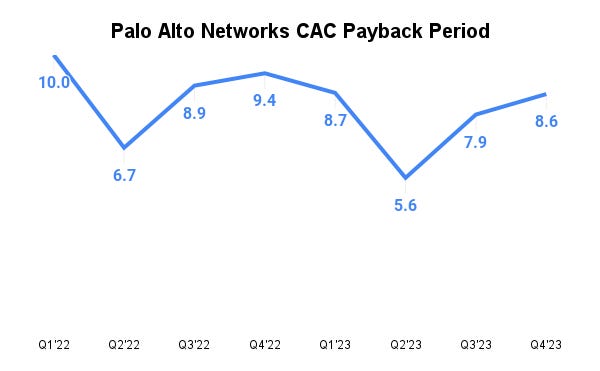

⬆️CAC* Payback Period 8.6 Months (7.9 LQ)

Dilution

↘️SBC/rev 15%, -0.6%pp QoQ

⬆️Dilution at 5.7% YoY, +2.3%pp QoQ🔴

Guidance

↘️Q1'24 $1,980.0M guide (+15.1% YoY) missed est by -2.9%🔴

↘️$8,000M FY guide (+11.0% YoY) lowered by -2.4%🔴

Key points from Palo Alto Networks Fourth Quarter 2023 Earnings Call:

Guidance Cut and Future Expectations:

The company expects a period of 12 to 18 months of pressure on top-line growth rates, notably billings, due to platformization efforts and programs that effectively provide customers a period of the contract for free as part of their commitment.

Despite the short-term impact on billings and revenue growth, Palo Alto Networks is aiming for sustained higher growth beyond this period, with an aspiration to reach $15 billion of Next-Generation Security (NGS) ARR by fiscal year 2030.

The company maintains its free cash flow and EPS guidance for fiscal year 2024, indicating confidence in managing through the strategy shift in a financially prudent manner.

Platformization Strategy:

Palo Alto Networks is accelerating its platformization strategy to consolidate cybersecurity solutions and drive faster adoption of its integrated platforms, aiming to streamline customer security operations and improve total cost of ownership (TCO).

XSIAM Traction:

The company highlighted the continued traction and success of its XSIAM product, noting significant displacement of legacy SIM vendors and emphasizing XSIAM as a key catalyst for growth and consolidation in the security operations center (SOC) space.

Demand and Market Trends:

Demand for cybersecurity solutions remains strong, driven by the increasing scale and sophistication of cyber attacks. Palo Alto Networks aims to address customer spend fatigue by offering more value and efficiency through its platformization efforts.

Go-to-Market and Channel Strategy:

The company is aligning its go-to-market and channel strategies to support its platformization effort, emphasizing total contract value (TCV) to motivate sales and channel partners, and leveraging strategic partnerships with system integrators (SIs) for broader platform adoption.

Investment in AI and Innovation:

AI is seen as a significant growth driver for cybersecurity, with Palo Alto Networks actively investing in AI capabilities across its product lines. The company is optimistic about the potential of AI to expand the total addressable market in cybersecurity and reinforce its leadership position.

Competitors and Market Dynamics:

There is an acknowledgment of competitive pressures, but Palo Alto Networks believes its strategy of platformization and offering bundled solutions will avoid price wars and create more value for customers, leading to larger deal sizes and stronger customer commitments.

Management comments on the earnings call.

Guidance Cut:

Dipak Golechha: "We expect a period of 12 to 18 months of pressure on our top line growth rates, notably billings... Beyond this period, we expect we can sustain higher growth than we provided in these targets in August."

Nikesh Arora: "Our guidance is not a consequence of a change in the demand outlook out there. Our guidance is a consequence of us driving a shift in our strategy in wanting to accelerate both our platformization and consolidation and activating our AI leadership."

Customers and Competitive Pressures:

Nikesh Arora: "The demand story is no different from prior quarters and on the margin, continues to get stronger... However, we're beginning to notice customers are facing spending fatigue in cybersecurity."

Nikesh Arora: "We intend to accelerate that opportunity. Along with the incremental focus on ROI and TCO with single product vendors having challenges and articulating compelling value, they're also forced to have platformization narrative."

Competitors:

"We've already displaced 19 different SIM vendors to date, and with the confidence under our belt, we're now looking systematically on how we can accelerate this legacy SIM displacement."

"We see the share shift happening in our favor because we see customers consolidating into our zero trust platforms."

Customers:

"Our 10 highest spending customers in Q2 increased their spend with us by 36% of the period."

"Additionally, more than 30% of our new SASE customers we signed in the second quarter were new to Palo Alto Networks, showing that we can win head-to-head in the market when leading with SASE."

Product Innovations:

"In our network security business, we continue to see progress driving ARR growth in our SASE business. Q2 was our fifth consecutive quarter of 50% ARR growth."

"In Prisma Cloud, we have made significant investments in the first half of the year to drive new customers and saw this pay off in Q2 with our highest new ACV growth in five quarters."

"In Cortex, XSIAM continues to be a significant catalyst for large transactions and growth across the business."

AI:

Nikesh Arora: "We have been working on AI for a long time as a company, however, we did accelerate our efforts with the arrival of generative AI... We see three discrete opportunities to drive additional growth in cybersecurity through AI."

Leadership:

"With several leadership positions awarded in second quarter, including our addition as a leader of the Gartner Endpoint Protection Magic Quadrant, we're now a recognized leader in 21 different categories across our three platforms."

"Our success over the last five years has been driven by the shift to platformization. We're committed to investing in innovation to extend our industry leadership position and platform."

Go-to-Market:

Nikesh Arora: "We are putting a lot of attention and focus on it. And we're positively enthused about the traction we're getting with the SI. To think about it, the SIs are new to this business over the last three to five years... So they are a critical part of this platformization approach."

Challenges:

"We did see softness in the US federal government's market. We were positioned well for several large projects where we had requisite certifications and won technical selection, but these deals did not close."