Palo Alto Networks Q1 2024 Earnings Review

$PANW Q1'24 Results:

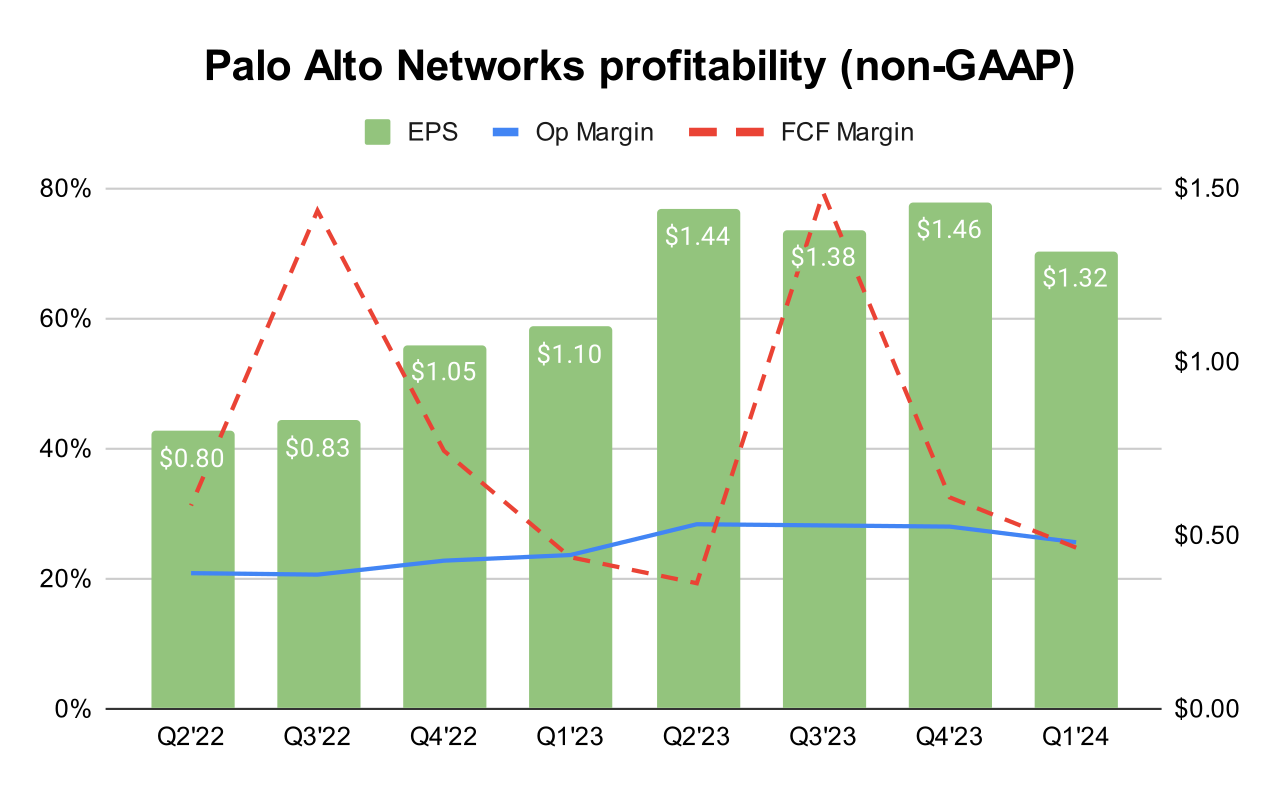

Financial Results:

↗️$1,984.8M rev (15.3% YoY, +21.8% LQ) beat est by 0.8%

↗️GM* (77.6%, +1.5%pp YoY)

↗️Operating Margin* (25.6%, +2.0%pp YoY)

↗️FCF Margin (24.8%, +1.5%pp YoY)

↗️EPS* $1.32 beat est by 5.6%

*non-GAAP

Revenue By Type

Product

➡️$391.0M rev (+0.7% YoY, +10.7% LQ) 🟡

↗️GM* (81.0%, +4.1%pp YoY)🟢

Subscription and support

➡️$1,593.8M rev (+19.6% YoY, +21.7% LQ)

↗️GM* (76.8%, +0.9%pp YoY)

Key Metrics

↗️RPO $11.30B (+23.0% YoY)🟢

➡️Billings $2,334M (+3.0% YoY)🟡

↗️NGS ARR $4,000M (+56.0% YoY)🟢

Operating expenses

↗️S&M*/Revenue 31.8% (29.1% LQ)

↗️R&D*/Revenue 16.1% (15.0% LQ)

↘️G&A*/Revenue 4.1% (4.4% LQ)

↗️Net New ARR $510M ($260 LQ)

↘️CAC* Payback Period 4.4 Months (8.6 LQ)

Dilution

↘️SBC/rev 15%, -0.1%pp QoQ

↗️Basic shares up 6.3% YoY, +0.5%pp QoQ🔴

↘️Diluted shares up 2.9% YoY, -4.9%pp QoQ

Guidance

➡️Q2'24 $2,150.0 - $2,170.0M guide (+10.6% YoY) in line with est

↗️$7,990.0 - $8,010.0M FY guide (+5.7% YoY) raised by 0.1% beat est by 0.3%

Key points from Palo Alto’s First Quarter 2024 Earnings Call:

Product Innovations:

AI Security Innovations: Palo Alto Networks announced a comprehensive suite of AI security offerings, which is expected to be the first in the market with capabilities to protect customers' AI security needs.

The suite includes:

AI Access Security: Ensures safe AI usage for employees and enterprises.

AI Security Posture Management (SPM): Monitors and manages the security posture for AI applications.

AI Runtime Security: Protects against vulnerabilities during the runtime phase of AI applications.

These products are designed to enable safe AI usage across enterprises, a response to the rapid adoption and integration of AI technologies which introduce new security threats.

Platform Enhancements (SASE 3.0):

The launch of SASE 3.0 marked a significant update, introducing unique industry-defining capabilities aimed at enhancing security and performance:

Secure Enterprise Browser: Integrated within the SASE framework to protect against AI threats and improve security for contractors and mobile devices.

AI-Powered Data Security: Features the industry's first LLM-powered data classification system, increasing accuracy and reliability in data handling.

Application Acceleration: Optimizes performance for enterprise SaaS and cloud applications, enhancing user experience significantly.

Prisma Cloud Updates:

Continued enhancements in Prisma Cloud include the rollout of data security posture management, incorporating advancements from the acquisition of Dig Security.

The introduction of support for over 100 new APIs across major cloud providers, ensuring that Prisma Cloud stays ahead in securing emerging cloud services.

Cortex Developments:

The ongoing expansion of the Cortex platform, particularly with the XSIAM system (Extended Security Information and Event Management), which has significantly grown in customer acceptance and has accumulated $400 million in bookings.

New capabilities such as Cloud Detection and Response (CDR) and Cloud Discovery and Exposure Management (CDEM) leverage Cortex Xpanse technology to provide a unified view of security from cloud to endpoint.

Platformization Strategy:

Palo Alto Networks is actively pursuing a platformization strategy aimed at consolidating cybersecurity solutions across three main platforms. The strategy has involved initiating deeper conversations with customers about integrating multiple security solutions into unified platforms, with the goal of enhancing security effectiveness and operational efficiency.

Feedback on the platformization approach has been largely positive, with a 30% increase in meetings focused on platform opportunities. This indicates robust demand and alignment with customer needs.

Billings and Revenue Impact:

Impact of Deferred Billing: The company has observed a shift in customer preferences towards annual billing plans, impacting the billings metric. This shift is attributed to the higher cost of money and changes in payment terms, which are now more spread out over time.

Bookings vs. Billings: Despite fluctuations in billings, the underlying business strength is suggested to be better reflected in bookings and the Remaining Performance Obligation (RPO), which saw significant growth. This aligns with the company's focus on high-quality bookings that contribute to long-term contractual commitments.

Customer Engagement and Growth:

Significant Deals and Contracts: Palo Alto Networks reported several large transactions in Q3, which underscore the efficacy of its platform approach. Notable deals include a seven-figure transaction with a U.S. county agency and an eight-figure deal with a U.S. financial services company.

Platformization Metrics: Approximately 900 of the top 5,000 customers have completed platformization, with ongoing efforts to increase this number. This strategy has resulted in higher average ARR (Annual Recurring Revenue) per fully platformized customer.

IBM Partnership: A significant new partnership with IBM was announced, involving the migration of QRadar customers to Palo Alto's XSIAM platform. This partnership is viewed as a strategic move to accelerate market penetration and enhance platformization efforts.

Future Outlook:

The company has set an ambitious target of achieving $15 billion in next-generation security ARR by fiscal year 2030, supported by incremental platformization sales and ongoing customer base expansion.

Continued investments in AI and cybersecurity innovations are planned, alongside strategic partnerships like the one with IBM to migrate QRadar customers to Palo Alto's XSIAM platform. This partnership is expected to accelerate platform adoption and enhance the company's market position.

Management comments on the earnings call.

Product Innovations

Nikesh Arora, Chairman & CEO: "In early May, we announced our comprehensive suite of AI security offerings and believe we will be first to market the capabilities to protect the range of our customers' AI security needs. We rolled out three products to safely enable the use of AI from employees using AI to enterprises building AI into their applications."

Customers

Nikesh Arora, Chairman & CEO: "As I mentioned in our prepared remarks, we have been reviewing all of our customers. We have been through 500 of them with the account teams. And every customer, there is an opportunity. There's an opportunity to deliver a platform, there's an opportunity to consolidate."

Platformization Strategy

Nikesh Arora, Chairman & CEO: "This drove us to accelerate the rollout of our platformization strategy at the end of the last quarter, following successful pilots earlier in the year. We created interest in the market, we started conversation with customers looking to begin their platformization journey, and spurring existing sales cycles to a more strategic outcome."

Billings

Dipak Golechha, CFO: "We reported Q3 billings within the range we guided, although as Nikesh and I have noted several times in the past few quarters, we continue to focus less on this metric. We saw an increase quarter-over-quarter in business transacted with deferred billings, which was also higher than we forecasted."

Future Outlook

Nikesh Arora, Chairman & CEO: "As we look forward, we have significant pipeline heading into our largest quarter of the year. We're just beginning to see the benefits of platformization accrue to our business. We will continue to make further investments here while balancing delivering profitable growth and have chartered a path with conviction towards being a $15 billion NGS ARR company."