Netflix Q1 2025 Earnings Analysis

Dive into $NFLX Netflix’s Q1 2025 earnings with review of financial performance, key metrics, operating expenses, dilution, customer growth, future outlook

Financial Results:

↗️$10.543B rev (+12.5% YoY, +16.0% LQ) beat est by 0.4%

↗️GM (50.1%, +3.2 PPs YoY)🟢

↗️EBIT Margin (31.7%, +3.6 PPs YoY)🟢

↗️FCF Margin (25.2%, +2.4 PPs YoY)

↗️Net Margin (27.4%, +2.5 PPs YoY)🟢

↗️EPS $6.61 beat est by 15.4%🟢

KPI

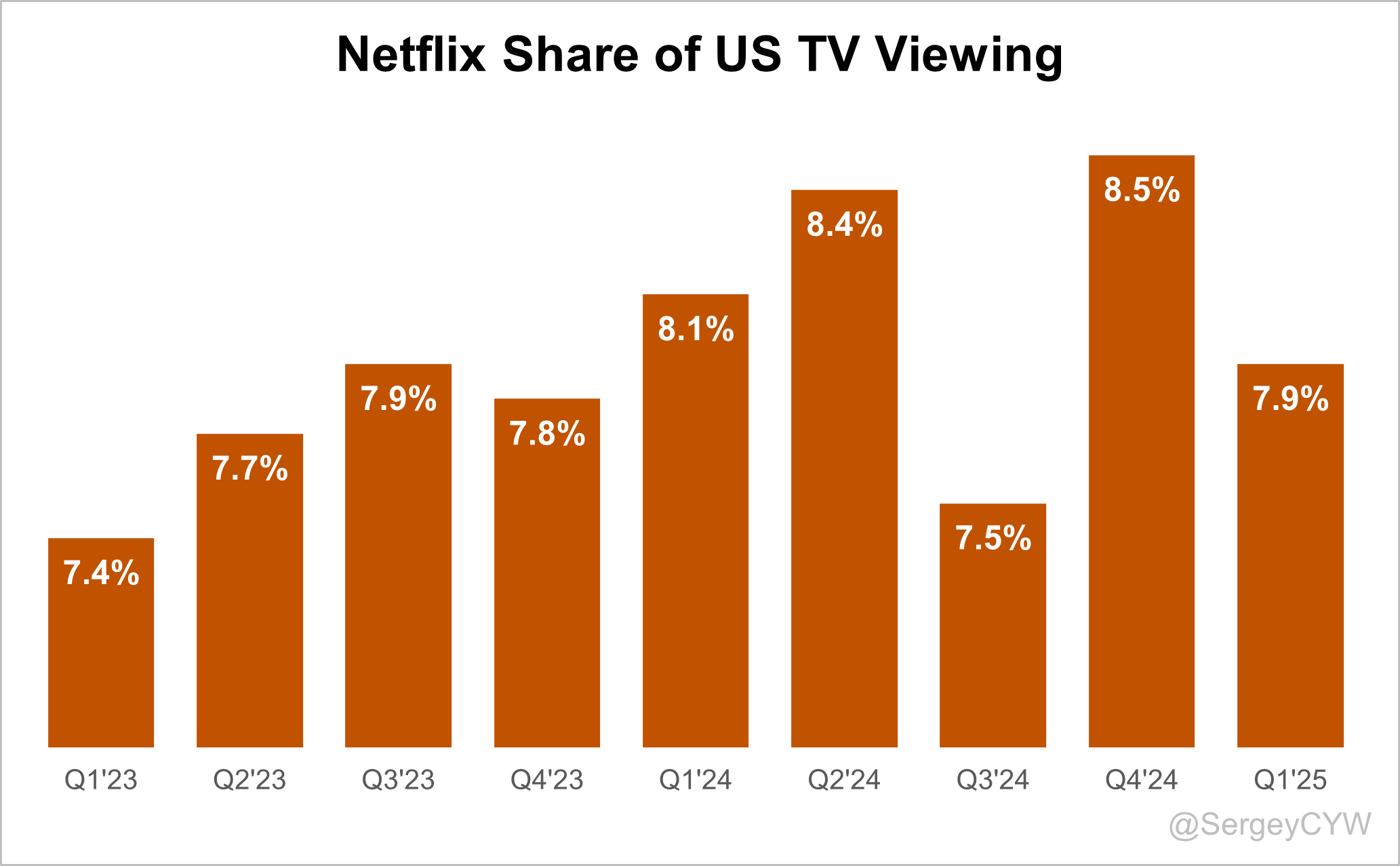

↘️7.9% Share of US TV Viewing (-0 PPs YoY)

Regional Breakdown

UCAN ↘️$4.617B rev (+9.3% YoY, 44% of Rev)

EMEA ↗️$3.405B rev (+15.1% YoY, 32% of Rev)

LATAM ↘️$1.262B rev (+8.3% YoY, 12% of Rev)

APAC ↗️$1.259B rev (+23.1% YoY, 12% of Rev)

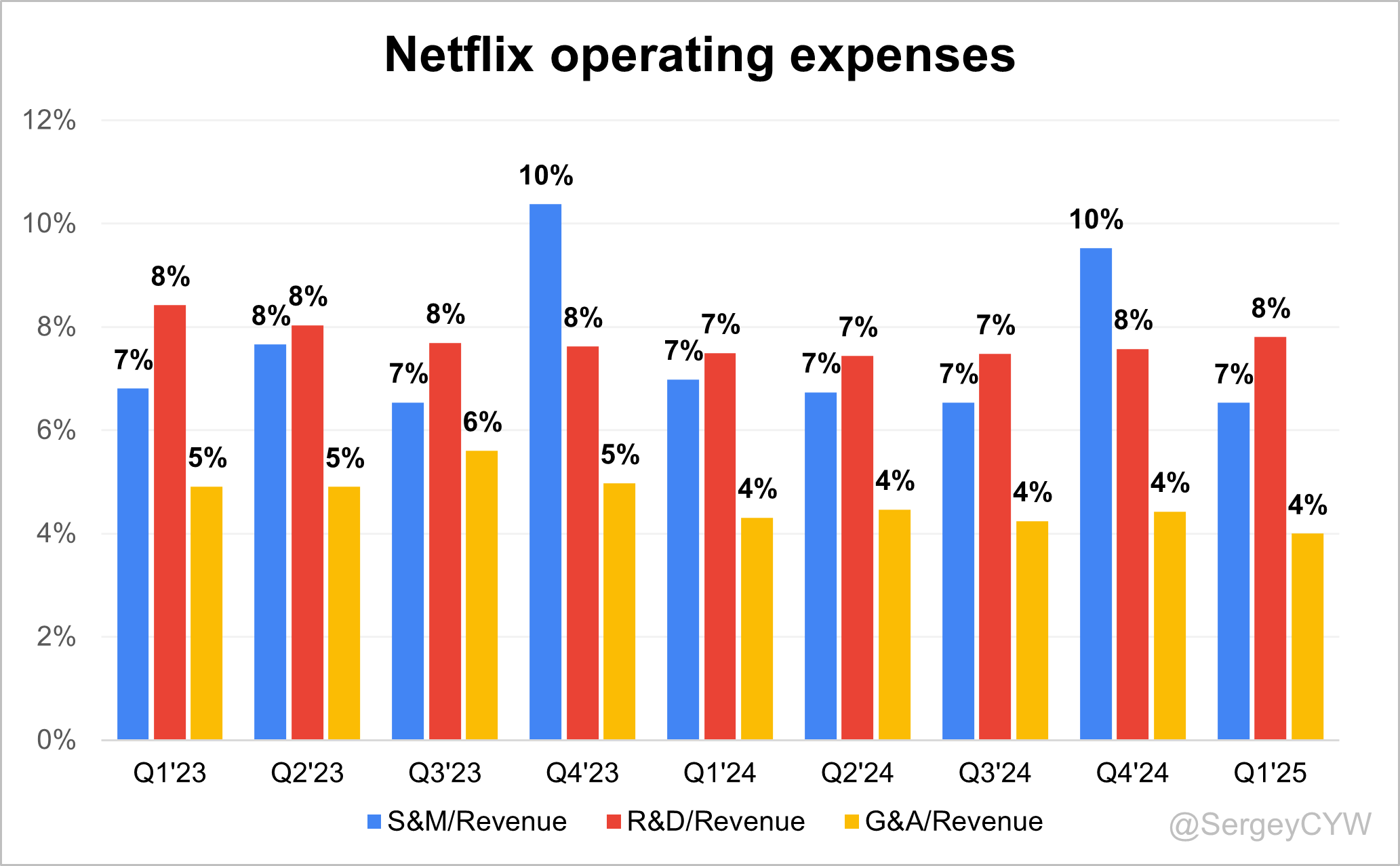

Operating expenses

↘️S&M/Revenue 6.5% (-0.5 PPs YoY)

↗️R&D/Revenue 7.8% (+0.3 PPs YoY)

↘️G&A/Revenue 4.0% (-0.3 PPs YoY)

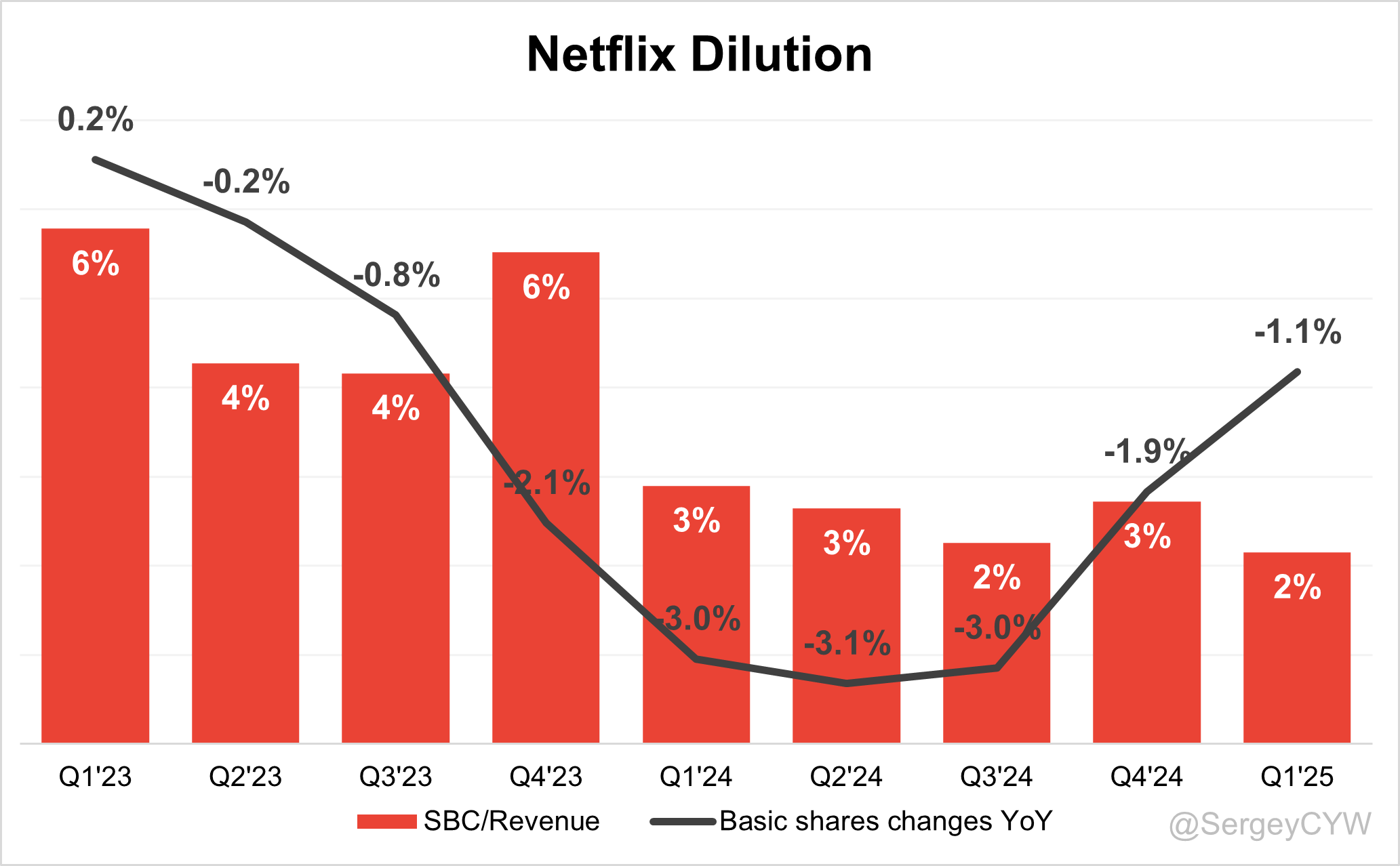

Dilution

↘️SBC/rev 2%, -0.6 PPs QoQ

↗️Basic shares down -1.1% YoY, +0.8 PPs QoQ🟢

↗️Diluted shares down -1.1% YoY, +0.4 PPs QoQ🟢

Guidance

↗️Q2'25 $11.035B guide (+15.4% YoY) beat est by 1.2%

Key points from Netflix’s First Quarter 2025 Earnings Call:

Financial Performance

Netflix reported Q1 revenue of $10.543B, up +12.5% YoY and +16.0% QoQ, exceeding expectations by 0.4%. Operating margin expanded to 31.7%, a +3.6 pp YoY increase, demonstrating strong operating leverage. EPS reached $6.61, beating estimates by +15.4%.

Free cash flow reached $3.5B with a 25.2% margin, up +2.4 pp YoY. Despite strong Q1, full-year margin guidance remains at 29%, with expected H2 pressure from increased content amortization and higher sales and marketing spend.

Streaming Platform

Netflix continues to grow steadily across global markets. Q1 2025 saw healthy net additions with no decline in retention or engagement. Churn remained stable, and retention of Q4 cohorts, including those acquired during major events, remained in line with historical patterns.

Netflix is redesigning its TV home interface—the first major overhaul in over 10 years. Testing indicates improved discovery and navigation. Rollout is expected by late 2025.

The platform is also developing generative AI-powered search to enhance personalization. Even the most-viewed titles represent <1% of total watch time, reinforcing the need for effective content surfacing.

Live Events and Sports

Live content accounts for a small portion of view hours but delivers outsized value in acquisition and engagement. NFL games aired on Christmas Day 2024 drove both subscriber and ad revenue upside. Netflix will host two NFL games in December 2025.

The Taylor vs. Serrano rematch in July 2025 follows the most-viewed women’s sporting event in US history. Netflix remains selective, pursuing live content only when economically viable.

Live operations are expanding internationally, positioning Netflix for broader global reach in event distribution.

Advertising

Netflix projects ad revenue will double in 2025, supported by the launch of its first-party ad tech platform, live in the US and Canada. Rollout to 10 additional markets is ongoing.

The proprietary stack enables expanded targeting based on life stage, mood, and modeled audiences, along with enhanced programmatic capabilities. Advertisers can now activate campaigns using onboarded customer lists and third-party segments.

Strong demand from Upfront buyers signals momentum. Full benefits of platform control are expected by 2026–2027, including ML-based optimization, advanced measurement, and new formats. The $7.99 ad-supported plan continues to drive subscriber diversification and monetization flexibility.

Netflix Originals and IP

In 2024, 9 of the top 10 most-streamed movies were animated. Titles like Leo, Sea Beast, and Pinocchio (Oscar-winner) led viewership. Netflix plans exclusive animated originals through 2027, with In Your Dreams debuting in Q4 2025.

Output deals with Universal, Illumination, and Sony expand licensed content. Netflix is also scaling creator-led shows such as Miss Rachel, Kill Tony, and Sidemen, all of which consistently chart in the top 10.

Video Games

Netflix views gaming as a $140B TAM opportunity (ex-China/Russia). Investment remains modest but focused. Four categories define the strategy:

Narrative IP games (Squid Game: Unleashed, Thronglets)

Franchise ports (GTA Trilogy)

Ad-free children’s games (Peppa Pig)

Social/party games (interactive multiplayer)

Early signals from GTA Trilogy and Thronglets suggest growing engagement. Investment will scale with improved confidence in the segment’s contribution to subscriber retention and engagement.

Key priorities for 2025–2026 include onboarding improvements and content library expansion.

Product Innovation

Netflix is enhancing platform utility with interactive search, redesigned UI, and broader content formats including video podcasts and creator-driven IP. Properties like Kill Tony and Sidemen: Pop the Balloon highlight diversification beyond scripted formats.

Game development is proceeding with a measured approach, investing in four pillars—IP games, ports, kid-safe experiences, and party formats—while tracking engagement metrics for scalable execution.

Content Strategy

Live content is used strategically for spikes in engagement. NFL will return with two games on December 25, 2025, after 2024’s success. The Taylor vs. Serrano event is also expected to generate strong acquisition momentum.

Animation is central to the strategy. Internal titles are being expanded, and Netflix’s in-house team is building a content pipeline through 2027. Licensing deals with major studios ensure a broad mix of originals and acquired content.

AI in Production

Netflix is integrating AI to improve content quality and cost-efficiency. Pedro Páramo used AI-based de-aging, achieving comparable effects to The Irishman at a fraction of the cost. The entire film budget equaled the VFX cost of The Irishman alone.

AI is used for pre-visualization, shot planning, and VFX sequencing, democratizing high-end effects for lower-budget productions. Management sees greater ROI in making content 10% better, rather than just cheaper.

Subscriber Growth

Q1 2025 saw strong net additions, extending Q4’s momentum. Growth was not dependent on high-profile events, which accounted for only a small share of additions. Netflix now serves 300M+ paid households, or ~700M individuals globally.

Netflix remains early in market penetration, with <10% of TV time and ~6% of consumer media spend in its markets. Continued growth is expected from content quality, price range flexibility, and international expansion.

Retention and Engagement

Churn remains low and stable. New cohorts, including those acquired during major live events, exhibit strong retention similar to traditional content-based acquisitions. Engagement levels remain high across tiers.

Recent price adjustments have not impacted churn, underscoring pricing power and value delivery. Content discovery remains critical, as top titles account for <1% of total watch time.

Global Expansion

Netflix now produces content in 50+ countries. Recent commitments include $1B in Mexico and $2.5B in Korea. The company continues to expand UK operations and build global live event capabilities.

Local production enhances cultural relevance while reducing cost structures. Netflix complies with local tax and content regulations, strengthening resilience in the face of international policy changes.

The extra member feature, which allows for paid sharing, is seeing solid adoption and retention, particularly in markets where multi-household sharing is common.

Macro Stability

Netflix sees no macro-driven deterioration in KPIs. Retention, plan mix, and engagement remain steady. Historical data supports home entertainment’s resilience in recessions. Management sees minimal exposure to geopolitical or regulatory disruption due to localized operations and compliance.

Competitive Positioning

Netflix is focused on the 80% of TV time not yet claimed by itself or YouTube. It offers stronger monetization to premium storytellers, positioning itself as the preferred platform for professional-grade creators. Shows from Miss Rachel and Sidemen illustrate this crossover.

Capital Allocation

Netflix expects $8B in FCF for FY25, with no major M&A planned. Capital allocation strategy remains unchanged: reinvest for growth, maintain liquidity, and return excess cash via share buybacks.

Outlook

Long-term aspiration includes doubling revenue and tripling operating income by 2030, though this is not official guidance. In the near term, Netflix expects:

Q2 UCAN revenue reacceleration

H2 margin contraction due to content and S&M ramp

Ongoing buildout of advertising and gaming

Product improvement via AI-powered discovery tools

Execution remains focused on innovation with capital discipline.

Management comments on the earnings call.

Product Innovations

Greg Peters, Co-CEO

“We began testing a new, simpler, more intuitive TV homepage. This is something that we hadn't made big structural changes to in over a decade, and we believe that will significantly improve the discovery experience.”

Greg Peters, Co-CEO

“We're also building out interactive search based on generative technologies. We expect that will improve that aspect of discovery for members.”

Ted Sarandos, Co-CEO

“We're constantly looking at all different types of content and content creators. As the popularity of video podcasts grow, I suspect you'll see some of them find their way to the platform.”

Streaming Platform

Spence Neumann, Chief Financial Officer

“Retention characteristics for the members that came in for big events like NFL or Squid Game were similar to members that joined for other big titles. So really no meaningful changes to our retention story.”

Greg Peters, Co-CEO

“We've got a pretty good business today—over $40 billion in revenue, 300 million paid households. But we still think we are a minority of our addressable market across all key measures.”

AI

Ted Sarandos, Co-CEO

“Our talent today is using AI tools to do set references, previs, VFX sequence prep, shot planning—all kinds of things that make the process better.”

Ted Sarandos, Co-CEO

“Rodrigo Prieto is directing Pedro Páramo. Using AI-powered tools, he was able to deliver de-aging VFX for a fraction of what it cost on The Irishman. The entire budget of the film was about equal to the VFX cost on The Irishman alone.”

Ted Sarandos, Co-CEO

“I remain convinced there's an even bigger opportunity if you can make movies 10% better using AI, not just cheaper.”

Competitors

Greg Peters, Co-CEO

“We believe we are a more competitive, better service for a certain class of creators and types of storytelling. Most importantly, we lead monetization for those kinds of titles.”

Ted Sarandos, Co-CEO

“Creators today have tools that were unimaginable a decade ago. We think we can help them reach an audience and support more ambitious efforts unlike the typical UGC models.”

International Growth

Ted Sarandos, Co-CEO

“When we produce in these countries, we create and support employment, training, and we help export local stories and cultures around the world.”

Spence Neumann, Chief Financial Officer

“We produce original content in 50 countries around the world. We’re a net contributor to many of those economies and cultures.”

Ted Sarandos, Co-CEO

“In 2023, we announced we’re committing $2.5 billion to Korean content, and recently, a $1 billion production investment in Mexico.”

Challenges

Greg Peters, Co-CEO

“Entertainment has been historically resilient in tougher economic times. And we haven’t seen any significant changes in retention or engagement, even with price adjustments.”

Spence Neumann, Chief Financial Officer

“There’s still a long way to go in the year, and a good bit of macro uncertainty out there. But this remains our best estimate for the full-year outlook.”

Future Outlook

Greg Peters, Co-CEO

“We don’t have a five-year forecast or guidance, but you can assume we are long-range thinking. We’re working hard every day to build the most loved and valued entertainment company.”

Spence Neumann, Chief Financial Officer

“Our capital allocation strategy hasn’t changed. In the absence of meaningful M&A, we expect growing free cash flow to be redeployed to share repurchase.”

Thoughts on Netflix Earnings Report $NFLX:

🟢 Positive

$10.543B revenue, up +12.5% YoY and +16.0% QoQ, beat by 0.4%

EPS $6.61, beat by +15.4%

31.7% EBIT margin, up +3.6 pp YoY

25.2% FCF margin, up +2.4 pp YoY, with $3.5B FCF

Net margin 27.4%, up +2.5 pp YoY

Q2'25 guidance $11.035B, up +15.4% YoY, beat by 1.2%

Ad revenue to double in 2025, supported by first-party ad tech rollout

Basic shares down -1.1% YoY, dilution offset via buybacks

APAC revenue +23.1% YoY, strongest regional growth

S&M spend down, 6.5% of revenue, improved efficiency

Stable churn, strong retention across all cohorts

AI-driven production cut costs, increased quality

Live sports (NFL, boxing) driving acquisition and engagement

300M+ paid households, ~700M viewers, still underpenetrated

$8B FCF projected for FY25, most redirected to buybacks

🟡 Neutral

7.9% share of US TV viewing, flat YoY

EMEA revenue +15.1% YoY, in line with regional trend

LATAM revenue +8.3% YoY, moderate growth

R&D expense rose to 7.8% of revenue, up +0.3 pp YoY

Content amortization and S&M spend to rise in H2, impacting margin

Interactive UI and AI-powered search expected by late 2025

Gaming strategy early-stage, with promising engagement but small revenue base

Share of TV time still <10%, signals room for growth but low current saturation

SBC/revenue 2%, but improved -0.6 pp QoQ

🔴 Negative

UCAN revenue +9.3% YoY, decelerated from previous quarter

Global content and marketing ramp in H2 to pressure operating margin

Net additions not materially driven by major events, raises bar for future catalysts

Video games segment not yet delivering material financial contribution

Thank you for reading!

Follow me for more frequent updates on X/Twitter and Threads, and on LinkedIn. For visual infographics, check out Instagram, and for portfolio changes, follow me on SavvyTrader.

Disclaimer: This earnings review is for informational purposes only and does not constitute financial, investment, or trading advice.