My Stock Portfolio Review, August 2024

Portfolio Review

Holdings:

Monthly Allocations:

* green (added), orange (trimmed)

Performance (TWR):

Historical performance (TWR):

2020: +110.2%(since 15.04.2020)

2021: +23.7%

2022: -59.6%

2023: +57.3%

Cumulative: +72.6%

A recap of my portfolio in 2024

January:

⬇️ Trim $ZS $CRWD $NET

⬆️Add $TSLA $TTD $MDB $AXON

March:

⬇️ Trim $NET $MNDY

✅ New position $GTLB ~3.1% (after -23% on ER)

May:

⬇️ Trim $CRWD $MNDY $DDOG $TTD

⬆️ Add $AXON

✅ New position $SHOP ~3.2%

June:

⬇️ Trim $CRWD $MNDY $MDB

⬆️ Add $NET $SNOW $TSLA $AXON $SHOP $GTLB

July:

⬇️ Trim $NET $MDB

⬆️ Add $CRWD

Commentary on my holdings:

Cloudflare NET 0.00%↑

The company reported its second quarter of 2024 results.

Thoughts on Cloudflare ER $NET:

🟢Pros:

+ Revenue rose by +30.0% YoY; according to Q3 guidance, revenue growth will slightly decrease to 28.4% YoY

+ RPOs are growing +42% YoY faster than revenue

+ Company increasing margins and profitability

+ Gross margin in record level

+ Record number of total customers added: +13,028

+ 168 new $100k+ customers added

+ Visible results from changes in GTM (Go-To-Market) strategy, with CAC Payback Period decreasing to 26 months from 34 last quarter

+ SASE platform secured several strong contracts

+ Beat revenue guidance by 1.6%.

+ FY revenue growth guidance increased by 0.4%

🔴Cons:

- Diluted shares count rose by 3.8% YoY

🟡Neutral:

+- DBNR decrease to 112%

+- SBC/rev 22%

+- Billings growth at 23% YoY, slower than revenue

Good quarter for Cloudflare; the company slightly raised its full-year forecast. A record number of total clients were added this quarter, RPO growth accelerated to 42%, significantly outpacing revenue growth. A downside was the decrease in DBNR to 112%, which I will continue to monitor closely.

MercadoLibre MELI 0.00%↑

The company reported its second quarter of 2024 results.

Thoughts on MercadoLibre Earnings Report $MELI:

🟢 Pros:

+ MercadoLibre remains the preeminent e-commerce and fintech player in Latin America.

+ Revenue increased by +48.6% YoY, accelerating from the previous quarter's +42.7%.

+ Company increasing margins and profitability.

+ Both commerce and fintech revenues showed acceleration.

+ The take rates for commerce and fintech increased from the previous quarter.

+ The fintech segment experienced strong growth in monthly active users.

+ Non-performing loans (NPL) for credits over 15 days are declining.

+ GMV growth stabilizing at +20% YoY.

+ The number of successful items sold on the Mercado Libre marketplace increased by 9% QoQ and accelerates to +30% YoY.

+ Strong number of Unique Marketplace Buyers added.

+ Risks associated with inflation in Argentina are decreasing, with expected improvements in e-commerce due to legislative changes.

🟡 Neutral:

+- Dilution at 1.1% YoY.

+- Gross margin slightly decreased from Q2 2023 due to higher rates.

+- The percentage of Credits NPL >90 slightly increased relative to the previous quarter but significantly decreased compared to last year.

Market Reaction to Earnings Release: The stock price rose by 6% following the earnings release.

The quarterly report from the company was truly outstanding, with no significant negatives to highlight. MercadoLibre is a market leader in Latin America, showing improvements across all metrics. It's important to note that the gross margin decreased as the company began counting the sales of goods from merchants on its E-commerce platform as its own revenue, which should be considered when evaluating revenue growth. For assessing the growth of the commercial segment, it is crucial to evaluate the growth of GMV, which has stabilized at +20% YoY.

Axon AXON 0.00%↑

The company reported its second quarter of 2024 results.

Thoughts on Axon Enterprise ER $AXON:

🟢 Pros:

+ Revenue accelerates to +34.6% YoY.

+ FY 2024 guidance increased by 3.0%.

+ Axon Cloud revenue growth rate +46.8% YoY.

+ Dollar-Based Net Retention (DBNR) is stabilizing at 122%.

+ Annual Recurring Revenue (ARR) is growing +44.1% faster than revenue.

+ Total company future contracted revenue is growing +41% faster than revenue.

+ The company is increasing margins and profitability.

+ Non-GAAP Gross Margin strong at 62.5%, up from Q2 last year 62.4%.

+ TASER 10 has shown robust demand.

+ Management noted that the customer response to Draft One is better than anything in the company’s history.

🔴Cons:

- Weak number of +25 net new ARR added, -36% YoY.

🟡 Neutral:

+- SBC/rev at 15% decreased from 16% in the last quarter.

+- Weighted-average number of common shares up 2.3% YoY.

Market Reaction to Earnings Release: The stock price increased by 12% following the earnings release.

The quarterly report was outstanding. The new TASER 10 product has shown robust demand. The company significantly increased its FY 2024 guidance by 3.0%. Axon Cloud revenue is growing at a high rate of +46.8% YoY. It's worth noting management's statement on Draft One: "The customer response to Draft One is better than anything in the company’s history."

Shopify SHOP 0.00%↑

The company reported its second quarter of 2024 results.

Thoughts on Shopify ER $SHOP :

🟢 Pros:

+ Revenue growth rate at 20.7% YoY. If the company beats the forecast similarly to this quarter by 1.4%, growth could accelerate to 24.3% next quarter.

+ The company is increasing margins and profitability on YoY basics.

+ Beat Q2 revenue guidance by 1.4%.

+ GMV growing at 22% YoY and GPV is growing 30% YoY, faster than revenue.

+ Subscription solutions revenue growing at 27%, with a record gross margin of 83%.

🟡 Neutral:

+- SBC/rev is 5%.

+- Diluted shares are up 1.5% YoY.

+- Attach Rate decreased -4 bps y/y

Market Reaction to Earnings Release: The stock price rose by 19% following the earnings release.

The quarterly report was outstanding. The company exceeded its Q2 forecast by 1.7% and surpassed analysts' expectations for Q3 by 1.4%. The forecast for the next quarter suggests an acceleration in revenue growth. The only negative noted was a decrease in the Attach Rate by 0.04 percentage points YoY, but this metric remains at a high level of 3.04%.

Datadog DDOG 0.00%↑

Yanbing Li has joined Datadog as Chief Product Officer, bringing over 25 years of experience from notable companies such as Aurora, Google, and VMware. With her deep expertise in AI, machine learning, and cloud infrastructure, Li is set to enhance Datadog's product portfolio and drive innovation in observability and security, aligning with the company's goals to meet global customer needs.

Datadog has been recognized as a Leader in the Gartner Magic Quadrant for Observability Platforms for the fourth consecutive year, underscoring its consistent execution and visionary approach in the rapidly growing observability market. This accolade reflects Datadog's ability to innovate and adapt to customer needs, offering robust monitoring and analytics capabilities that enhance operational efficiency and performance tracking across various sectors.

The company reported its second quarter of 2024 results.

Thoughts on Datadog ER $DDOG :

🟢Pros:

+ Revenue growth stabilizing at +26.7% YoY.

+ Dollar-Based Net Retention (DBNR) remains strong at ~115%.

+ Billings are growing 28.4% YoY, and Remaining Performance Obligations (RPO) grew by +43% YoY, faster than revenue.

+ The company is increasing margins and profitability on a YoY basis.

+ Beat revenue guidance by 3.4%.

+ The percentage of customers using 2+, 4+, 6+, and 8+ products increased from the last quarter.

+ Net New ARR is growing 22.6% YoY.

+ Investment in R&D is bigger than in S&M; the company pays great attention to the development of new products.

+ A large number of new and updated products were introduced.

+ The management team was strengthened.

🔴Cons:

- Diluted shares up 10.7% YoY.

- Weak customer growth (+50 >$100K customers); the share of >$100K customers is now 87%. Since the company is focused on attracting large customers, the more important metric is the use of 6+ and 8+ products by customers.

🟡Neutral:

+- Stock-Based Compensation (SBC)/revenue is 21%.

+- 700 new total customers added, the same as in Q1 2024.

Market Reaction to Earnings Release: The stock price rose by 6.5% following the earnings release.

The quarterly report was strong. The forecast for the next quarter suggests revenue growth will stabilize. Despite the weak addition of new customers, this is not currently a critical metric for the company, as it is focused on attracting larger clients. Clients contributing more than $100k ARR are no longer the primary focus; instead, it is important to observe customers' usage of multiple modules, where the company is performing well. Customers are using an increasing number of modules.

Trade Desk TTD 0.00%↑

The company reported its second quarter of 2024 results.

Thoughts on Trade Desk ER $TTD :

🟢 Pros:

+ Customer retention remains above 95% for 9 consecutive years.

+ Revenue growth rate accelerating to 26.1% YoY. If the company beats its forecast by 1.7% similar to this quarter, next quarter's growth will be 27.5%.

+ The company is increasing margins and profitability.

+ Beat Q2 revenue guidance by 1.7%.

+ Diluted shares down 0.1% YoY.

+ The company is actively pursuing global expansion, with international growth outpacing North American growth for the sixth consecutive quarter.

+ This political season is expected to generate substantial advertising revenue.

+ The Trade Desk has strengthened its partnerships with major CTV platforms and content providers: Netflix, Roku, and FOX.

+ AI-driven platform, Kokai, has received significant enhancements.

🟡 Neutral:

+- SBC/rev is 22%.

+- FCF margin declined to 9.7% but remains healthy.

Market Reaction to Earnings Release: The stock price increased by 2% following the earnings release.

The company has strengthened its partnerships with major CTV platforms and content providers. The forecast for the next quarter suggests accelerated revenue growth. The company continues its international expansion, with international growth outpacing North American growth for the sixth consecutive quarter. Management's comments during the earnings call were very positive.

Monday MNDY 0.00%↑

The company reported its second quarter of 2024 results.

Thoughts on Monday.com ER $MNDY :

🟢Pros:

+ Revenue accelerates to +34.4% YoY growth rate; if the company similarly beats its forecast by 2.7%, next quarter's revenue growth will stabilize at 34%.

+ Dollar-Based Net Retention (DBNR) for $50k+ customers is stable at 114%, for $100k+ customers at 114%; increased by 1 PPs sequentially.

+ Record number of $100k+ and $50k+ customers added.

+ Record growth in CRM and development accounts.

+ Record net new ARR added.

+ Strong FCF margin 21.5%.

+ Non-GAAP gross margin at a record level 90.7%.

+ Beat Q2 revenue guidance by 2.7%.

+ FY 2024 guidance increased by 1.4%.

+ New Pricing Model starts well.

🔴Cons:

- Diluted shares up 8.3% YoY.

🟡Neutral:

+- SBC/rev at 15.5%, increased 3.3 PPs sequentially.

+- Billings growing at 29.3%, slower than revenue.

Market Reaction to Earnings Release: The stock price rose by 10% following the earnings release.

The quarterly report was very strong. The company significantly exceeded the Q2 forecast and raised its full-year 2024 guidance. Management noted that the new pricing model has started well, confirmed by a record addition of large clients. Record growth was noted in CRM and development accounts in new business areas.

Snowflake SNOW 0.00%↑

The company reported its second quarter of 2024 results.

Thoughts on Snowflake ER $SNOW:

🟢Pros:

+ Revenue rose by +28.9% YoY.

+ Strong DBNR at 127%, with a minor decline of -1PP sequentially.

+ FY guidance increased by 1.7%.

+ RPO growth increased to 48% YoY, growing faster than revenue. cRPO is growing at 29.6%. Some major clients pay monthly, which suggests that the actual cRPO growth could be higher.

+ Strong number of new customers added (+427), more than last year (+370).

+ The company is implementing new products and increasing R&D spending; R&D expenses now account for 25.8% of revenue as the company invests in future growth.

+ Record number of Marketplace Listings added +237.

+ Data sharing 34%, up 2 PPs sequentially.

🔴Cons:

- Net New ARR growth declined by -21% YoY.

- If the company beats its forecast for the next quarter by a similar 2.4%, revenue growth will continue to slow down to +25% YoY.

🟡Neutral:

+- SBC/rev at 43%, basic shares up 2.1% YoY.

+- Beat Q2 revenue estimates by 2.4%; significantly less than the 5.3% beat in the previous quarter.

+- The company announced an additional $2.5 billion share buyback.

+- Product Gross Margin down 1.5PPs YoY, but consistent with the previous quarter; the decline was attributed to GPU-related costs which improve the company’s AI functionalities.

+- Margins and profitability declined due to increases in operating expenses.

+- Total calculated billings growth accelerated to +22.7% but is still growing slower than revenue.

+- Weak number: +26 $1M+ ARR customers added.

Market Reaction to Earnings Release: The stock price fell by 9.7% following the earnings release.

The company's quarterly report was weak. Although management noted that the forecast was conservative, the company exceeded the Q2 forecast by 2.4%, whereas the "conservatism" of the forecast implied an outperformance similar to the 5.3% in Q1. Considering the forecast for the next quarter, revenue growth will continue to slow. The company is actively investing in new product development and increasing R&D expenses, which is positive in the long term, but leads to a reduction in operating margins in the short term. Positively, DBNRR has stabilized, there is good growth in total customers, and a record addition of 237 marketplace listings. Data sharing grew to 34%, up 2 percentage points sequentially, indicating a widening network effect moat. Management notes that revenue growth from new products is expected in two quarters. I have not yet reduced my position, but am considering it.

Crowdstrike CRWD 0.00%↑

CrowdStrike has expanded its cybersecurity measures by integrating support for NVIDIA NIM Agent Blueprints within its AI-native Falcon platform. This partnership enhances the security framework for developers building enterprise generative AI applications, leveraging NVIDIA’s comprehensive AI toolset. By providing robust security solutions, CrowdStrike and NVIDIA are facilitating the secure and efficient development of generative AI applications across various industries, including customer service and drug discovery.

CrowdStrike has been recognized as a Leader in the 2024 Frost Radar: Global Cloud Workload Protection Platform (CWPP) for the second year in a row, highlighting its innovation and growth in cloud security. The company's Falcon Cloud Security platform offers comprehensive protection from cloud breaches through a unified approach that includes threat intelligence, managed detection and response, and robust visibility across cloud environments.

The company reported its second quarter of 2024 results.

Thoughts on CrowdStrike ER $CRWD :

🟢 Pros:

+ Revenue rose by +31.8% YoY.

+ ARR grew by +32% and RPO by +36%, both outpacing revenue growth.

+ Strong Net New ARR added (+217M, +11% YoY).

+ Customers are using more modules (6+, and 7+ modules +1pp QoQ).

+ Usage of 8+ modules + 66% YoY.

+ Company increasing margins and profitability.

+ Beat Q2 revenue guidance by 0.3%, despite the recent incident.

+ Management emphasized that deals delayed due to the incident are not canceled but postponed to the next quarter and remain under consideration.

🟡 Neutral:

+- SBC/rev at 20.8%. Diluted shares up 3.8% YoY.

+- FY revenue growth forecast adjusted to 27.5%, a reduction of 2.7%, with the incident estimated to impact net new ARR by $60 million.

+- Total calculated billings growing +18,3% YoY slower than revenue.

+- Company doesn’t provide DNBR numbers (“our dollar based gross and net retention rates were consistent with our expectations” - supposedly at 120%).

Market Reaction to Earnings Release: The stock price rose by 2% following the earnings release.

The report was solid, considering the recent incident on July 19th. The next quarter will provide more details, but the current quarter's competitor earnings reports show that there was no significant customer migration from CrowdStrike to competitors following the incident. Management reported discounts provided to customers and an expected impact on ARR of $60M ($30M in Q3 and Q4), and it was noted that some deals are delayed in signing, but customers are not leaving and deals are expected to be signed in the next quarter. The percentage of customers using more modules is increasing, which is the most critical metric for the company.

MongoDB MDB 0.00%↑

MongoDB announced that Iron Mountain $IRM is using MongoDB's Atlas platform for their new Iron Mountain InSight Digital Experience Platform (DXP).

This platform, built on MongoDB Atlas, integrates and manages both physical and digital information across various industries, featuring AI-driven tools for process automation and data accessibility. It offers customizable solutions like Digital Auto Lending and Health Information Exchange, supported by MongoDB’s flexible architecture and strong security features.

Iron Mountain, established in 1951, is a global leader in information management, serving over 240,000 customers worldwide.

The company reported its second quarter of 2024 results.

Thoughts on MongoDB ER $MDB:

🟢 Pros:

+ Revenue rose by +12.8% YoY, with next quarter's revenue growth forecast accelerating to +18.3% YoY if it beats the forecast by 3.0%

+ Atlas revenue grew +27% YoY (71% of total revenue), comparable to Snowflake +29 % growing at the same rate.

+ Total calculated billings growth slightly decreased to 21.3% YoY, but is still growing faster than revenue.

+ Net ARR Expansion remains above 119%, slightly down from 120% last quarter.

+ R&D expenses remain high, with reductions in S&M and G&A expenses as the company invests in new product development.

+ MongoDB raised full-year guidance by 1.6%.

+ MongoDB exceeded its Q2 revenue forecast by 3%.

+ MongoDB has launched the MongoDB AI Applications Program (MAP) to support customers in building and deploying AI applications, which could drive future revenue growth.

🔴 Cons:

- Weak number of new customers $100k+ added, only +52.

🟡 Neutral:

+- SBC/rev is 26%, dilution at 3.8% YoY.

+- Non-GAAP gross margin recovered to 75.5% from last quarter but is still below last year's 77.6%.

+- Atlas Net New ARR added declined by -13%, but overall, it’s not bad, given the forecast that Atlas Net New ARR growth will accelerate next quarter.

+- Slightly more total customers added compared to last quarter.

Market Reaction to Earnings Release: The stock price rose by 18% following the earnings release.

The company's quarterly report was quite good, despite the weak addition of large clients, with only +52 $100k+ customers added. The forecast for the next quarter suggests an acceleration of revenue growth, and importantly, an acceleration of Atlas revenue growth, which will grow faster than Snowflake's revenue.

GitLab GTLB 0.00%↑

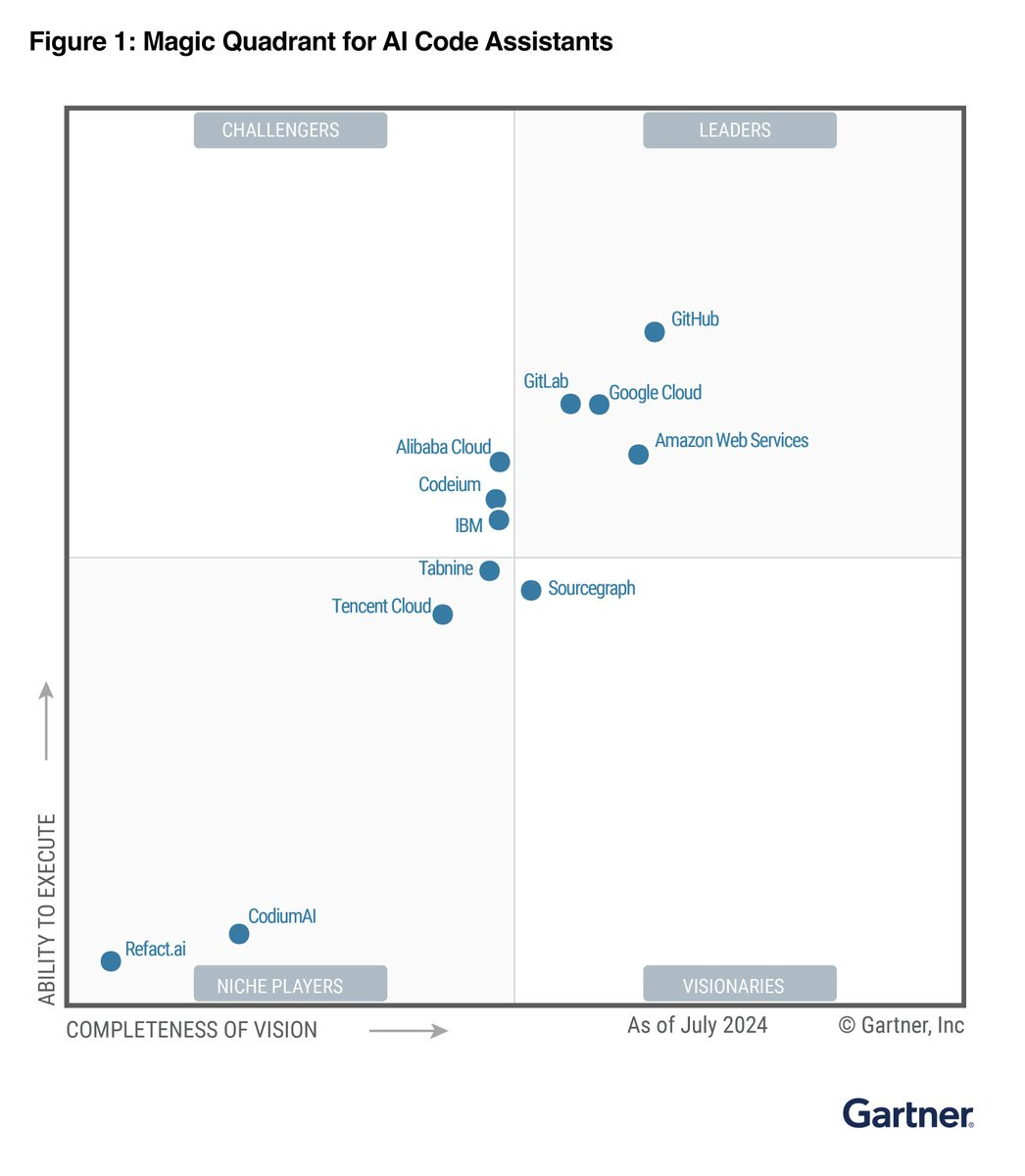

GitLab has been named a Leader in the inaugural 2024 Gartner Magic Quadrant for AI Code Assistants. This recognition is based on its comprehensive AI-powered DevSecOps platform, which excels in enhancing developer productivity, code quality, and security throughout the software development lifecycle (SDLC). Gartner highlights GitLab's deep market understanding, continuous innovation with advanced AI models, robust ecosystem through third-party integrations, and strong security measures.

This is a very important direction for the company as its competitor, GitHub, reported a 40% revenue increase last quarter, primarily due to the implementation of AI Code Assistants. I expect that GitLab will also begin to see additional revenue growth from the deployment of AI Code Assistants in the near future.