HubSpot Q4 2024 Earnings Analysis

Dive into $HUBS HubSpot’s Q4 2024 earnings with review of financial performance, key metrics, operating expenses, dilution, customer growth, future outlook

Financial Results:

↗️$703.2M rev (+20.8% YoY, +20.1% LQ) beat est by 4.4%

↗️GM (85.3%, +0.5 PPs YoY)🟢

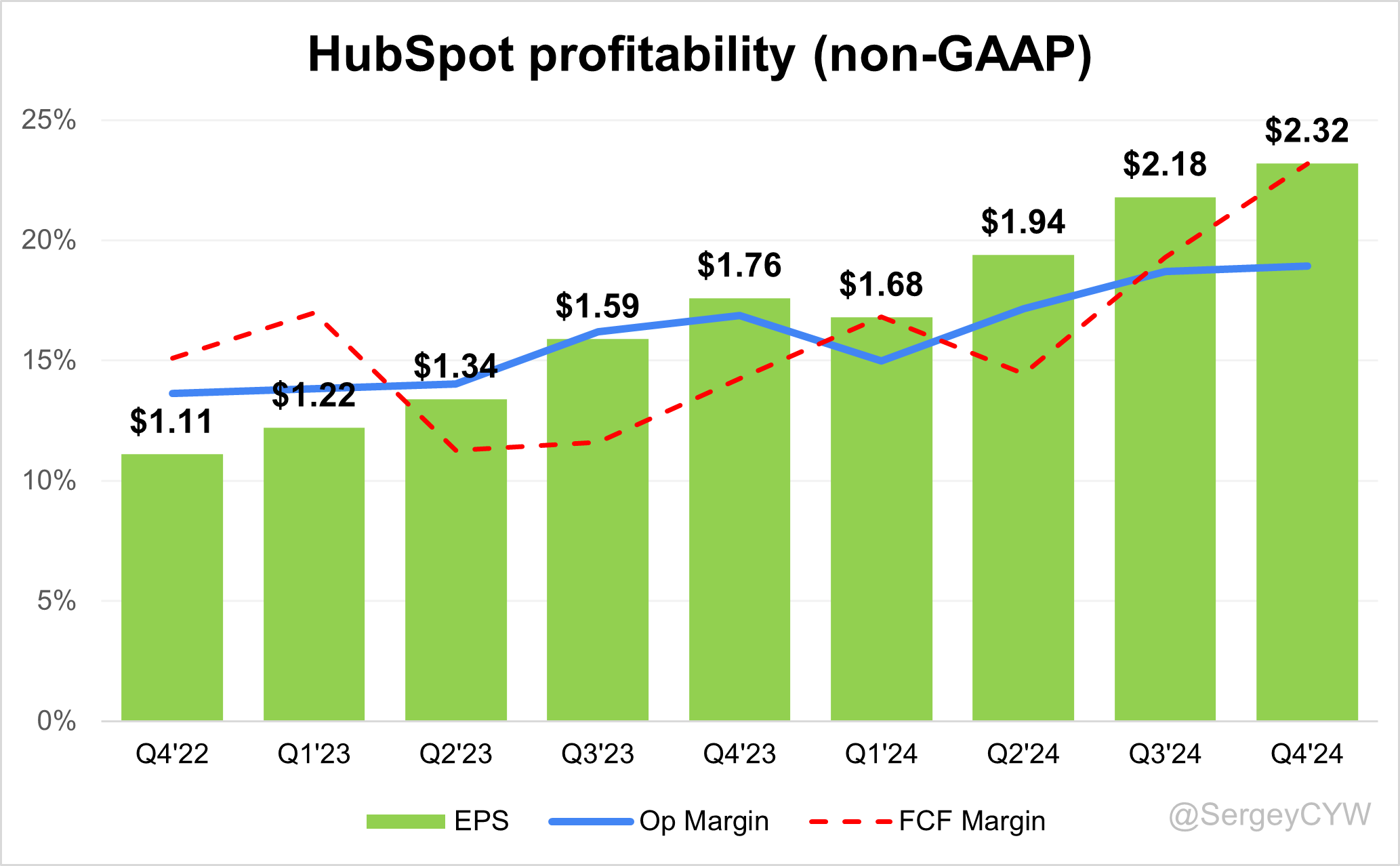

↗️Operating Margin* (18.9%, +2.1 PPs YoY)🟢

↗️FCF Margin (23.2%, +8.9 PPs YoY)🟢

↗️Net Margin (0.7%, +3.0 PPs YoY)

↗️EPS* $2.32 beat est by 5.9%🟢

*non-GAAP

Subscription

➡️$687.3M Subscription rev (+20.5% YoY); 97.7% of Rev🟡

↗️GM* (88.0%, +0.3pp YoY)

Key Metrics

➡️Deferred Revenue $788.21M (+16.3% YoY)🟡

↗️RPO $1,000.00M (+23.9% YoY)

➡️Billings $768M (+13.3% YoY)🟡

↘️Average Rev Per Customer $11,312 (-0.5% YoY)

Customers

➡️247,939 customers (+20.9% YoY, +9811)

Operating expenses

↗️S&M*/Revenue 39.6% (+0.3 PPs YoY)

↘️R&D*/Revenue 21.5% (-0.2 PPs YoY)

↗️G&A*/Revenue 8.4% (+0.5 PPs YoY)

Quarterly Performance Highlights

↗️Net New ARR $130M (+33.5% YoY)

↘️CAC* Payback Period 28.8 Months (-5.6 YoY)🟢

↘️R&D* Index (RDI) 1.04 (-0.19 YoY)🟡

Dilution

↘️SBC/rev 19%, -0.3 PPs QoQ

↘️Basic shares up 2.6% YoY, -0.0 PPs QoQ

↗️Diluted shares up 2.4% YoY, +0.7 PPs QoQ

Guidance

↘️Q1'25 $697.0 - $699.0M guide (+13.1% YoY) missed est by -1.3%🔴

↘️$2,985.0 - $2,995.0M FY guide (+13.8% YoY) missed est by -0.4%🔴

Key points from HubSpot’s Fourth Quarter 2024 Earnings Call:

Financial Performance

HubSpot reported Q4 2024 revenue growth of 20% YoY in constant currency and 21% for the full year. Subscription revenue increased 21% YoY, while services and other revenue saw a 36% increase in Q4.

Operating margin expanded to 19% in Q4 and 17.5% for the full year, up 200 basis points from 2023. Free cash flow reached $488 million, representing 19% of revenue, with Q4 free cash flow at $163 million (23% of revenue).

The company ended 2024 with 248,000 customers, adding 9,800 net new customers in Q4, a 21% YoY increase. Net revenue retention improved to 104%, up two points sequentially, driven by seat upgrades from the new pricing model. Average revenue per customer (ARPC) remained stable at $11,300.

AI and Product Innovations

HubSpot embedded 80+ AI-powered features across its platform. AI Co-Pilot assists marketing, sales, and service teams, while AI Agents automate workflows.

AI Support Bot now handles 35% of support tickets, aiming for 50% in 2025. AI Sales Bot resolves 80% of website chat inquiries, improving lead conversion. AI-driven sales prospecting automation generated 10,000+ meetings in Q4, accelerating pipeline growth.

The Frame.ai acquisition enhanced real-time analysis of structured and unstructured data, improving customer insights. 80% of business data is unstructured, including calls, emails, and transcripts. Integrating structured records with this data enhances sales and marketing strategies.

Agent.ai Expansion

HubSpot’s Agent.ai platform is driving AI adoption. The user base surged from 50,000 to 900,000 in six months, with 7,000 builders developing AI agents.

AI agents collaborate with human teams, aligning with HubSpot’s vision of a hybrid workforce. The company is embedding automation across the customer lifecycle, positioning itself as a leader in AI-driven CRM.

Content Hub Growth

Content Hub became the fastest-growing product in 2024. AI-powered Content Remix increased Marketing Hub’s attach rate from 13% to 54% over the year.

New AI capabilities, including multi-input remixing, podcast generation, and automated case study creation, enhanced adoption. AI-driven content marketing is improving productivity by reducing manual effort and streamlining workflows.

Service Hub Expansion

Service Hub saw 100% QoQ growth in enterprise portal adoption, with 54% YoY growth in customers with 100+ seats.

AI-powered features like call and ticket summaries, reply recommendations, and predictive support routing are key differentiators. Customer Agent AI is used by 1,340+ customers, achieving a 42% resolution rate.

Retention and revenue expansion remain priorities. Enterprises are adopting AI-driven support, but some are still assessing long-term deployment. HubSpot is refining its AI monetization strategy, introducing usage-based AI pricing while ensuring seamless enterprise integration.

Commerce Hub and Pricing Model Shift

HubSpot transitioned to a hybrid pricing model, combining seat-based and usage-based pricing. This shift drove strong seat expansion and multi-hub adoption, improving net revenue retention.

Commerce Hub integrates AI-driven billing, payment automation, and renewal forecasting. Migration to the new pricing model will be completed in 2025, with 50-60% of ARR undergoing a 5% price increase upon renewal.

Challenges remain in AI monetization. Customers remain cost-focused, and broader AI adoption is still developing. AI-powered automated workflows will drive gradual revenue growth as more businesses transition.

Customer Retention and Expansion

Customer retention remained strong, driven by multi-hub adoption, AI automation, and improved onboarding. 35% of Pro+ customers now use four or more hubs, up 7% YoY.

Co-selling with partners increased 68% YoY, reflecting growing ecosystem-driven customer acquisition. HubSpot removed minimum seat requirements for Professional and Enterprise tiers, making it easier for businesses to scale.

The enterprise segment saw 21% YoY growth in large deals, with customers consolidating sales, marketing, and service operations onto HubSpot’s platform.

Customer Success Stories

AI-powered automation is delivering measurable results. AI Support Bot now resolves 35% of support tickets, targeting 50% by 2025, reducing costs while maintaining customer satisfaction.

Transcribe, a HubSpot customer, automated its service operations using AI, reducing response times and improving efficiency. Businesses using Content Hub for AI-driven content creation now publish 80% of their blogs using AI, streamlining workflows and enhancing output.

Enterprise Wins and Strategic Partnerships

HubSpot’s Service Hub expanded in the enterprise market, with 54% YoY growth in customers with 100+ seats. AI-powered service capabilities like automated ticketing, call summaries, and predictive insights drove adoption.

Product advancements, including sensitive data support, UI extensions, and CRM development tools, fueled 21% YoY growth in large deals.

HubSpot’s partner ecosystem strengthened, with co-selling increasing 68% YoY. More partners are selling multi-hub solutions and AI-first offerings, expanding HubSpot’s enterprise presence.

Challenges and Market Conditions

HubSpot faces macroeconomic and operational challenges. The strengthening US dollar created a 200 bps foreign exchange headwind. The wind-down of Clearbit will impact revenue growth by less than 1% in 2025.

SMB sentiment is improving, but purchasing decisions remain value-driven, committee-based, and influenced at the C-suite level.

Seasonal softness is expected in Q1 2025, with revenue growth likely reaching its lowest point before accelerating later in the year.

Future Outlook and Growth Strategy

HubSpot forecasts 2025 revenue of $2.985B to $2.995B, reflecting 16% YoY growth in constant currency. Non-GAAP operating margin is expected at 18%, reflecting ongoing efficiency improvements and AI-driven automation.

Growth levers for 2025 include:

Seat-based expansion and pricing model migration, driving ARR uplift.

AI-driven product adoption, increasing multi-hub usage and retention.

Enterprise growth, driving larger deal sizes and revenue expansion.

Investment in AI-driven automation, reducing costs and improving go-to-market execution.

HubSpot is strengthening its AI-powered CRM leadership, embedding automation across marketing, sales, and service. With growing AI adoption and a structured pricing transition, the company expects long-term revenue and margin expansion.

Management comments on the earnings call.

Product Innovations

Yamini Rangan, Chief Executive Officer

"We are committed to becoming an AI-first customer platform by embedding AI into every hub and across the entire platform. To deliver on this vision, we launched a co-pilot that gives every customer-facing employee a digital assistant to work with, AI agents that handle context-sensitive tasks out of the box, and 80-plus AI features embedded within our hubs."

Dharmesh Shah, Chief Technology Officer

"We are building an ecosystem where structured and unstructured data come together, giving businesses a deeper understanding of their customers. Our AI-powered automation is enabling users to extract real-time insights and streamline processes in ways that were previously impossible."

AI Integration

Yamini Rangan, Chief Executive Officer

"2024 was a transformative year as we reimagined our products, platform, and entire company with AI. The momentum we are building with AI is exciting, and we are just at the beginning of unlocking its full potential."

Dharmesh Shah, Chief Technology Officer

"We’ve seen a dramatic reduction in AI infrastructure costs, and with new reasoning models, we are expanding the range of problems AI can solve. These advancements allow us to build smarter agents that work alongside teams, making businesses more efficient and productive."

Agent.ai Ecosystem

Yamini Rangan, Chief Executive Officer

"We believe the future is about hybrid teams—people and AI agents working together. That’s why we have been incubating Agent.ai, which has grown from 50,000 users to 900,000 in just six months, with over 7,000 builders creating agents using our low-code tool."

Dharmesh Shah, Chief Technology Officer

"Our strategy is clear: we are building a network where AI agents can collaborate, discover each other, and work towards higher-order goals. With the rapid adoption of Agent.ai, we are shaping a future where businesses can harness AI automation at scale."

Content Hub Growth

Yamini Rangan, Chief Executive Officer

"Content Hub has been our fastest-growing hub, and its success is driven by AI. We improved its attach rate to Marketing Hub from 13% to 54% in one year, and we continue to expand its capabilities with AI-driven content remixing, podcast generation, and case study automation."

Customer Growth and Retention

Kate Bueker, Chief Financial Officer

"Net revenue retention increased two points sequentially to 104%, reflecting the continued momentum in seat expansion from customers adopting our new seat-based pricing model. We remain focused on retention by delivering more product value and improving the customer experience."

Yamini Rangan, Chief Executive Officer

"Customers are consolidating their sales, marketing, and service operations on our platform. Over 35% of our Pro+ customers now use four or more hubs, up 7% year-over-year, which underscores the increasing value of our unified customer platform."

Strategic Partnerships

Yamini Rangan, Chief Executive Officer

"We have been investing heavily in our partner ecosystem to drive growth. Co-selling with partners grew 68% year-over-year, a clear sign that our ecosystem strategy is working. Our partners are now engaged in multi-hub selling and AI-first solutions, which strengthens our market position."

Challenges and Market Conditions

Kate Bueker, Chief Financial Officer

"While we are encouraged by improving customer sentiment, purchasing decisions remain value-driven, committee-based, and influenced at the C-suite level. We are assuming that these customer buying patterns will persist throughout 2025."

Future Outlook

Yamini Rangan, Chief Executive Officer

"We are entering this year with more clarity on strategy, more alignment on outcomes, and more urgency in execution than ever before. Our focus remains on making our products easy, fast, unified, and AI-first."

Kate Bueker, Chief Financial Officer

"We expect a step down in our Q1 2025 growth rate, but we anticipate revenue acceleration throughout the year. Our pricing model transition, AI-driven expansion, and upmarket momentum will be key drivers of long-term growth."

Thoughts on HubSpot Earnings Report $HUBS:

🟢 Positive

Revenue: $703.2M (+20.8% YoY, +20.1% QoQ) beat estimates by 4.4%.

Profitability: Operating margin at 18.9% (+2.1pp YoY), Free cash flow margin at 23.2% (+8.9pp YoY).

EPS: $2.32 beat estimates by 5.9%.

Net New ARR: $130M (+33.5% YoY), showing strong revenue expansion.

Customer Growth: 247,939 customers (+20.9% YoY, +9,811 net adds).

Agent.ai Growth: Users surged from 50,000 to 900,000 in six months.

Service Hub Expansion: 100% QoQ growth in enterprise portal adoption, 54% YoY growth in 100+ seat customers.

AI Automation Impact: AI-powered Support Bot now resolves 35% of support tickets, targeting 50% in 2025.

Retention Improvement: Net revenue retention increased to 104%, up 2pp sequentially.

🟡 Neutral

Subscription Revenue: $687.3M (+20.5% YoY), making up 97.7% of total revenue.

Deferred Revenue: $788.2M (+16.3% YoY), showing strong contract value but slower growth.

Billings: $768M (+13.3% YoY), lagging revenue growth, indicating potential future slowdown.

Sales Efficiency: CAC Payback Period dropped to 28.8 months (-5.6 months YoY), but still at a high level.

Average Revenue Per Customer: $11,312, down 0.5% YoY, reflecting smaller deal sizes or pricing pressure.

Commerce Hub: Transition to a hybrid pricing model in progress, with 50-60% ARR renewals expected at a 5% increase.

🔴 Negative

Q1 2025 Guidance Miss: Revenue guide of $697M - $699M (+13.1% YoY) missed estimates by 1.3%.

FY 2025 Guidance Miss: $2.985B - $2.995B (+13.8% YoY) missed estimates by 0.4%.

Strengthening US Dollar Impact: 200bps FX headwind, reducing international revenue contribution.

Clearbit Wind-Down: Expected to reduce revenue growth by <1% in 2025.

Seasonal Weakness in Q1 2025: Revenue growth expected to slow before accelerating later in the year.