HubSpot: A Scalable CRM Leader in a Rapidly Expanding Market

Deep Dive into $HUBS: Valuation, Segment Growth, Key Metrics, Profitability, Expenses, Product Launches, Customer Acquisition, Financial Stability, SBC/Revenue, and Shareholder Dilution.

HubSpot: Company overview

About HubSpot

HubSpot, Inc. is a cloud-based CRM platform provider founded in 2005 and headquartered in Cambridge, Massachusetts. It went public on October 9, 2014, and trades on the NYSE under the ticker HUBS. HubSpot delivers an integrated CRM platform through six hubs: Marketing, Sales, Service, Content, Operations, and Commerce. Each hub supports specific functions, from automation and analytics to customer service and B2B commerce. The company employs 8,246 full-time staff and is led by CEO Yamini Rangan. HubSpot primarily serves mid-market B2B companies across Americas, Europe, and Asia Pacific, offering both software and professional services to drive adoption and success.

Company Mission

HubSpot’s mission is “to help millions of organizations grow better”. As of 2023, the company served 194,737 customers across 120+ countries, generating $2.24 billion in total revenue. Key metrics include a customer acquisition cost of $42, retention rate of 81.3%, and a product adoption rate of 73.6%. The company's vision focuses on enabling global digital transformation through a customer-centric technology ecosystem, aiming for an average customer retention rate of 85%.

Sector and Market Position

Operating in the Technology sector under the Software–Application industry, HubSpot has become a notable CRM platform. Its annual recurring revenue (ARR) reached $2.12 billion by Q4 2023. The stock has been volatile, with a 52-week trading range between $434.84 and $881.13. It currently trades below its 50-day ($648.09) and 200-day ($608.90) moving averages.

Competitive Advantage

HubSpot’s edge lies in offering a unified CRM platform rather than fragmented point solutions. This creates high switching costs and improves long-term retention. The company’s differentiation strategy emphasizes product quality and customer loyalty, while its focus strategy targets mid-market B2B firms with tailored capabilities. Its modular platform enables continuous expansion through new hubs, increasing revenue per customer and lifetime value.

Total Addressable Market (TAM)

HubSpot is positioned within a rapidly expanding CRM market. Depending on the source, the global CRM market was valued at:

$73.40 billion in 2024 (Grand View Research)

$101.41 billion in 2024 (Fortune Business Insights)

$254.89 billion in 2024 (The Business Research Company)

Forecasts indicate strong growth:

Grand View Research projects a CAGR of 14.6%, reaching $163.16 billion by 2030

Fortune Business Insights forecasts a CAGR of 12.8%, with the market growing to $262.74 billion by 2032

The Business Research Company estimates a CAGR of 17.1%, reaching $561.17 billion by 2029

This growth underscores the large opportunity HubSpot has within the evolving CRM landscape.

Valuation

$HUBS HubSpot is trading at a Forward EV/Sales multiple of 9.1, approximately in line with its median of 8.9. The company's current Forward EV/Sales multiple is at low levels compared to the valuation lows in 2019 and 2024.

$HUBS HubSpot trades at a Forward P/E of 59.2, with revenue growth of +21% YoY in the most recent quarter.

The EPS growth forecast for 2026 is 16.4%, with a P/E of 57.8, resulting in a 2026 PEG ratio of 3.5.

The PEG (Price/Earnings to Growth) ratio is a key tool for evaluating growth stocks, introduced by Peter Lynch.

PEG < 1: Undervalued – A ratio below 1 suggests the stock is undervalued. For example, if the P/E is 15 and earnings are expected to grow by 20%, the PEG would be 0.75, indicating a good buying opportunity.

PEG = 1: Fair Value – A PEG of 1 means the stock price matches its growth expectations, representing fair value.

PEG > 1: Overvalued – A PEG above 1 indicates the stock may be overvalued, as its price is higher than its projected growth rate, making it riskier.

Valuation comparison

Analysts forecast 16.4% revenue growth for $HUBS HubSpot in 2025 and 16.3% in 2026. Based on these projections, the company’s P/S multiple suggests it is fairly valued compared to companies in the CRM sector.

Analysts expect solid revenue growth, so let's examine the key metrics to determine whether these expectations are justified.

We'll evaluate the company's economic moat, which supports long-term revenue growth, analyze revenue trends and the forecast for next quarter, and identify key factors that could help the company exceed expectations and sustain future growth.

We'll assess the performance of key segments, the launch of new products and updates, customer acquisition growth, key financial metrics, financial stability, and margin trends.

Additionally, we'll review the SBC/Revenue ratio, shareholder dilution, and finally, draw conclusions on the company's outlook.

Economic Moat

HubSpot has established several economic moats that protect its competitive position in the CRM market. These moats vary in strength and contribute differently to the company's ability to maintain pricing power and market share. Let's examine each type of economic moat HubSpot has developed.

Switching Costs

HubSpot has developed exceptionally strong switching costs by integrating deeply into customers’ operations across marketing, sales, service, and operations. Migrating to a competitor involves high disruption and financial cost, creating economic "lock-in" and allowing HubSpot to maintain pricing power with low churn. Customers rely on the platform for storing critical business data, workflows, and processes, which increases friction over time for switching providers. HubSpot’s customer retention rate of 81.3% reflects the strength of this moat. Because of the interconnected nature of its hubs, replacing one component affects the performance of the entire system, discouraging partial transitions.

Network Effect

HubSpot benefits from a moderate network effect, which grows as more users, partners, and developers join its ecosystem. Its App Marketplace includes over 1,400 integrations, adding utility and stickiness to the platform. As adoption grows, more integrations are developed, creating a reinforcing loop that enhances value for all users. However, this effect is concentrated in the B2B mid-market, limiting its scale compared to broader consumer platforms.

Brand

HubSpot has established a strong brand moat by pioneering the concept of inbound marketing and aligning its identity with this strategy. It is widely recognized as the original and authoritative voice in inbound CRM. Educational resources, certification programs, and the annual INBOUND conference reinforce its brand leadership and deepen engagement. Even with feature parity from competitors, HubSpot remains the default choice for inbound-focused businesses.

Intellectual Property

HubSpot maintains a moderate intellectual property moat, grounded in its proprietary methods for CRM, marketing automation, and engagement workflows. While not heavily patent-protected, the company’s edge comes from continuous innovation in areas like AI, predictive analytics, and customer journey mapping. These tools create real differentiation, although the ease of replication in software limits long-term defensibility.

Economies of Scale

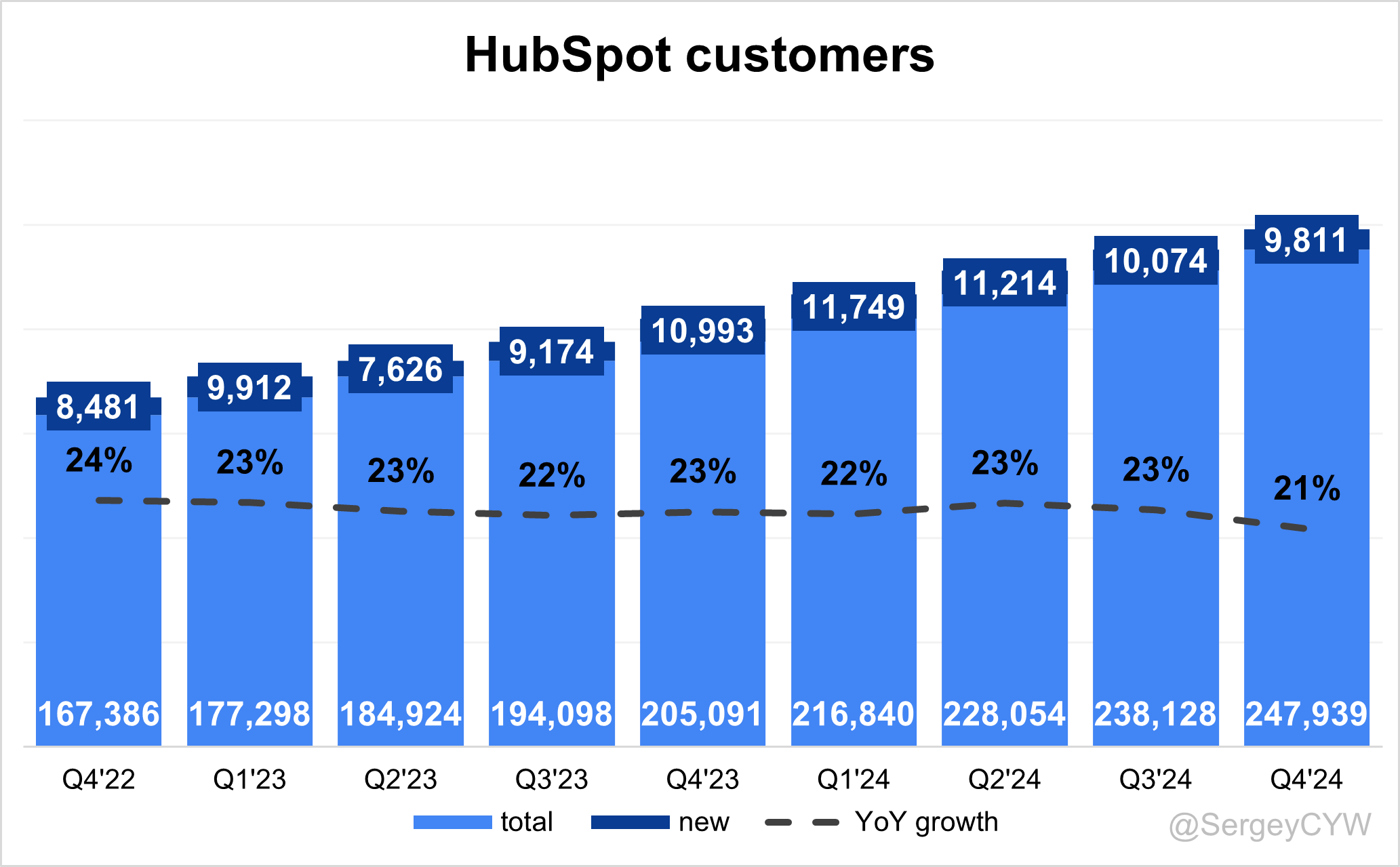

With $2.63 billion in revenue and 247,939 customers, HubSpot is leveraging economies of scale effectively. Spreading fixed costs, especially R&D, across a wide customer base enables higher investment in innovation without sacrificing margin. As the company scales, cost per customer for support, infrastructure, and development decreases. This dynamic allows for better pricing flexibility or improved profitability. However, compared to giants like Salesforce, HubSpot’s relative scale advantage remains constrained.

HubSpot's overall economic moat is most powerful in its switching costs and brand recognition, with complementary strength from its growing scale, network effects, and intellectual property. The combination of these moats creates a formidable competitive position that has enabled HubSpot to maintain strong growth and pricing power in the competitive CRM market.

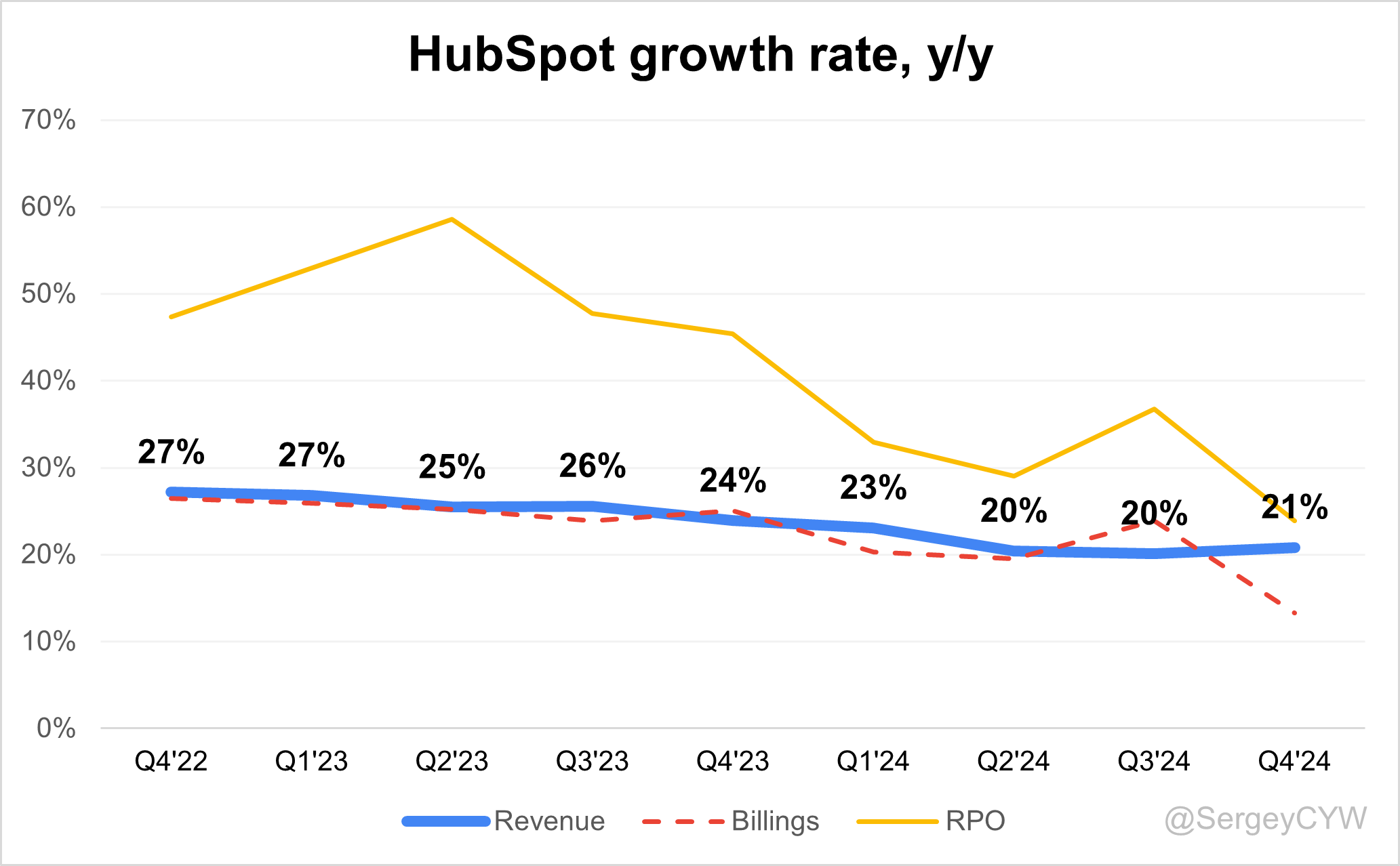

Revenue growth

$HUBS HubSpot's revenue growth slightly accelerated from +20.1% YoY in Q3 2024 to +20.8% YoY in Q4. Based on the forecast for the next quarter, if the company beats its guidance by 4.3%, as it did in Q4, Q1 revenue growth would reach +18.1%, indicating a potential significant deceleration in growth.

RPO growth slowed notably to +23.9% YoY, but remains above revenue growth. Billings growth also decelerated to +13.3% YoY, falling below the pace of revenue growth.

Segments and Main Products

HubSpot operates as a comprehensive CRM platform provider focused primarily on mid-market B2B companies. Its product suite is structured into integrated hubs, each targeting a specific component of customer relationship management.

Marketing Hub is the foundation of the platform. It enables businesses to drive inbound strategies through content creation, SEO optimization, and social media campaigns. Built-in AI tools power lead scoring and dynamic automation workflows. Real-time adaptive email templates increase engagement. Inbound marketing generates 3x more leads than traditional outbound methods, positioning Marketing Hub as a core driver of organic growth.

Sales Hub equips sales teams with automation tools, meeting scheduling, and pipeline tracking. It provides real-time visibility into the buyer journey, enabling prioritization and efficient closing. Reporting dashboards offer granular insights into deal performance. 73% of top-performing sales teams rely on analytics, emphasizing the role of Sales Hub in data-informed sales execution.

Service Hub streamlines customer support using ticketing systems, feedback loops, and knowledge base management. Integrated NPS surveys and satisfaction scoring tools support service quality improvement. Businesses using robust support tools report a 2.5x increase in revenue growth, highlighting Service Hub’s influence on customer retention and lifetime value.

Content Hub, introduced in 2024, allows businesses to build and manage web content. Integrated directly into the platform’s global navigation, it provides seamless access and collaboration across CRM workflows. It enables unified content strategy execution across all customer touchpoints.

Operations Hub offers data automation and RevOps-aligned process management. It connects marketing, sales, and service operations into a unified analytics environment. This ensures data consistency, removes silos, and accelerates decision-making across the funnel.

Commerce Hub delivers B2B commerce functionality, including subscription management and automated billing journeys. In 2025, HubSpot will enable native checkout capabilities within the platform, eliminating reliance on third-party tools and synchronizing commerce with marketing and CRM workflows.

AI capabilities are now embedded across all Hubs. In 2025, HubSpot’s AI tools support content generation, audience segmentation, and predictive analytics. Campaigns adapt in real time to user behavior. AI-powered automation increases marketing scale without compromising personalization, while dynamic segmentation ensures higher targeting precision.

HubSpot's modular and intelligent platform structure enables businesses to scale efficiently while keeping all operations synchronized under a single ecosystem.

Main Products Performance in the Last Quarter

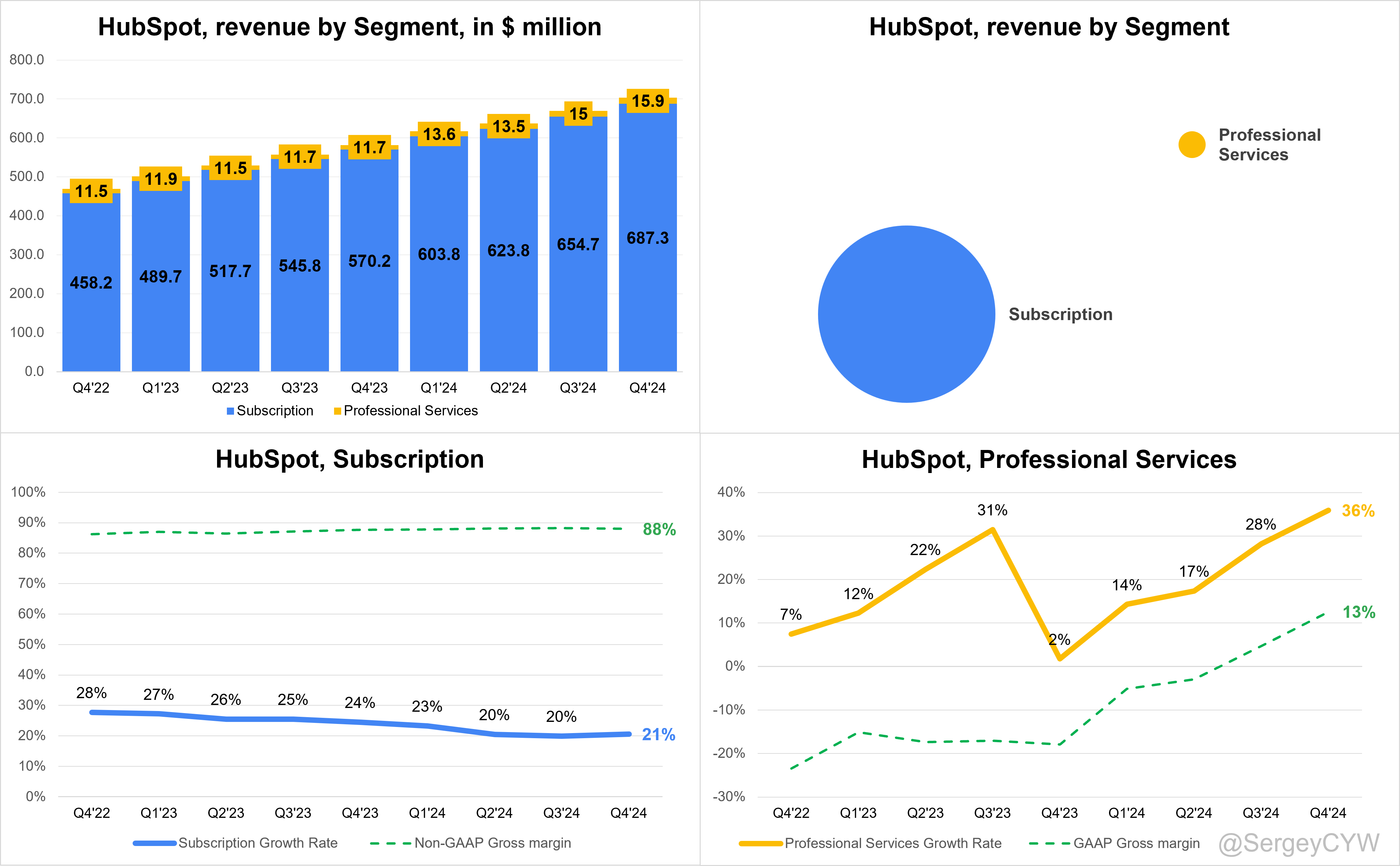

$HUBS Revenue by Segment: 97.7% of the company’s revenue comes from subscriptions. Professional services revenue accounts for the remaining 2.3%.

Subscription revenue growth remained strong at +20.5% YoY in Q4. Non-GAAP gross margin reached 88%, increasing by +0.3 percentage points YoY.

Professional services revenue grew by +36% YoY, and GAAP gross margin turned positive at 13%.

Marketing Hub

Marketing Hub saw strong expansion, particularly in conjunction with Content Hub. The two are increasingly adopted together, with Content Hub’s attach rate to Marketing Hub increasing from 13% to 54% over the year. AI-driven tools like Content Remix and newer features like multi-input remix, podcast remix, and case study remix have significantly accelerated content production and improved campaign efficiency. This dynamic is directly enhancing cross-sell momentum and driving broader platform adoption. Marketing Hub adoption remains strong. Breeze Intelligence, launched in January 2025, is driving early demand in marketing workflows. Early usage is centered on campaign managers and channel designers. HubSpot sees high engagement from marketers using AI for prospect identification and intent signal detection.

Sales Hub

Sales Hub is benefiting from internal adoption of AI prospecting tools. Over 10,000 meetings were generated in Q4 through AI-powered automated communications. The company is applying generative AI to automate discovery, research, follow-ups, and improve personalization across the sales journey. However, there’s no explicit mention of net new accounts tied solely to Sales Hub. The focus remains on AI transforming existing sales workflows, rather than major new customer acquisition in this segment.

Service Hub

Service Hub is experiencing rapid upmarket growth, particularly among larger teams. New enterprise portals grew +100% QoQ in Q4, while customers with 100+ seats grew +54% YoY. Key drivers include AI-based tools like call summaries, ticket summaries, and reply recommendations embedded into help desk and customer success workspaces. The company is positioning Service Hub as a platform for enterprise-grade customer experience. One agent, the Customer Agent, is already achieving a 42% resolution rate with over 1,340 customers.

Content Hub

Content Hub was the fastest-growing hub of 2024. The attach rate to Marketing Hub rose from 13% to 54%, supported by the widespread adoption of AI features. The most popular feature, Content Remix, has seen increasing usage, with many customers now producing over 80% of their blogs using AI-generated content. This hub has become the main entry point for new content workflows and is enabling faster scale-up of campaigns across segments.

Commerce Hub

Commerce Hub is being strengthened through M&A. The cash flow acquisition is enabling native CPQ capabilities, which are now being rebuilt inside HubSpot’s core platform. This will enhance the Commerce Hub’s ability to serve small and medium-sized businesses with integrated quoting and revenue workflows.

Agent.AI

Agent.AI is rapidly scaling. Users grew from 50K at Inbound to 500K, and as of the latest update, surpassed 900K users. The platform now has 7,000+ builders using low-code tools to create agents. The system is being positioned as the control tower for AI-driven workflows in the SMB market. AI agents like Customer Agent and Content Agent are early in monetization but are already proving value. AI support bots now handle 35% of tickets and are targeted to reach 50% in 2025, while the AI sales bot resolves 80% of website inquiries.

Product Innovations

AI is now fully embedded across the HubSpot platform. Breeze Copilot has surpassed 75,000 weekly active users, signaling growing adoption across customer teams. The acquisition of Frame.AI unlocked real-time insights from unstructured data sources like calls, emails, and transcripts. HubSpot is building a contextual knowledge layer on top of both structured and unstructured data to deliver more personalized, efficient workflows. Usage-based pricing for AI is planned once repeatable value is established at scale.

Over the past two years, HubSpot has embedded 100+ AI features into the platform. Every hub now includes native AI functionality. The company operates under a platform-first architecture built on three core layers: data, context, and AI intelligence. Frame.AI is central to the context layer, aligning workflows to each company’s brand, tone, and ideal customer profile.

Breeze Intelligence, powered by Clearbit, expands HubSpot’s reach into the data enrichment and intent signal market, a multi-billion-dollar TAM adjacent to CRM. The product helps customers identify better-fit prospects, capture purchase intent, and accelerate conversions—all embedded directly into the CRM experience.

Due to the accelerated pace of product development, HubSpot now splits major launches across two flagship events per year—Spring Spotlight in April and Inbound in September. Both events will showcase new AI agents and deeper AI platform capabilities.

In 2024, the company introduced a revamped pricing model. Seat prices were lowered, seat minimums for Pro and Enterprise tiers were removed, and a core seat model was introduced requiring payment to edit CRM records. The result is a smoother upgrade path and more precise customer value alignment. Legacy customers will begin migrating into this model across 2025–2026, with up to a 5% pricing uplift expected during the transition.

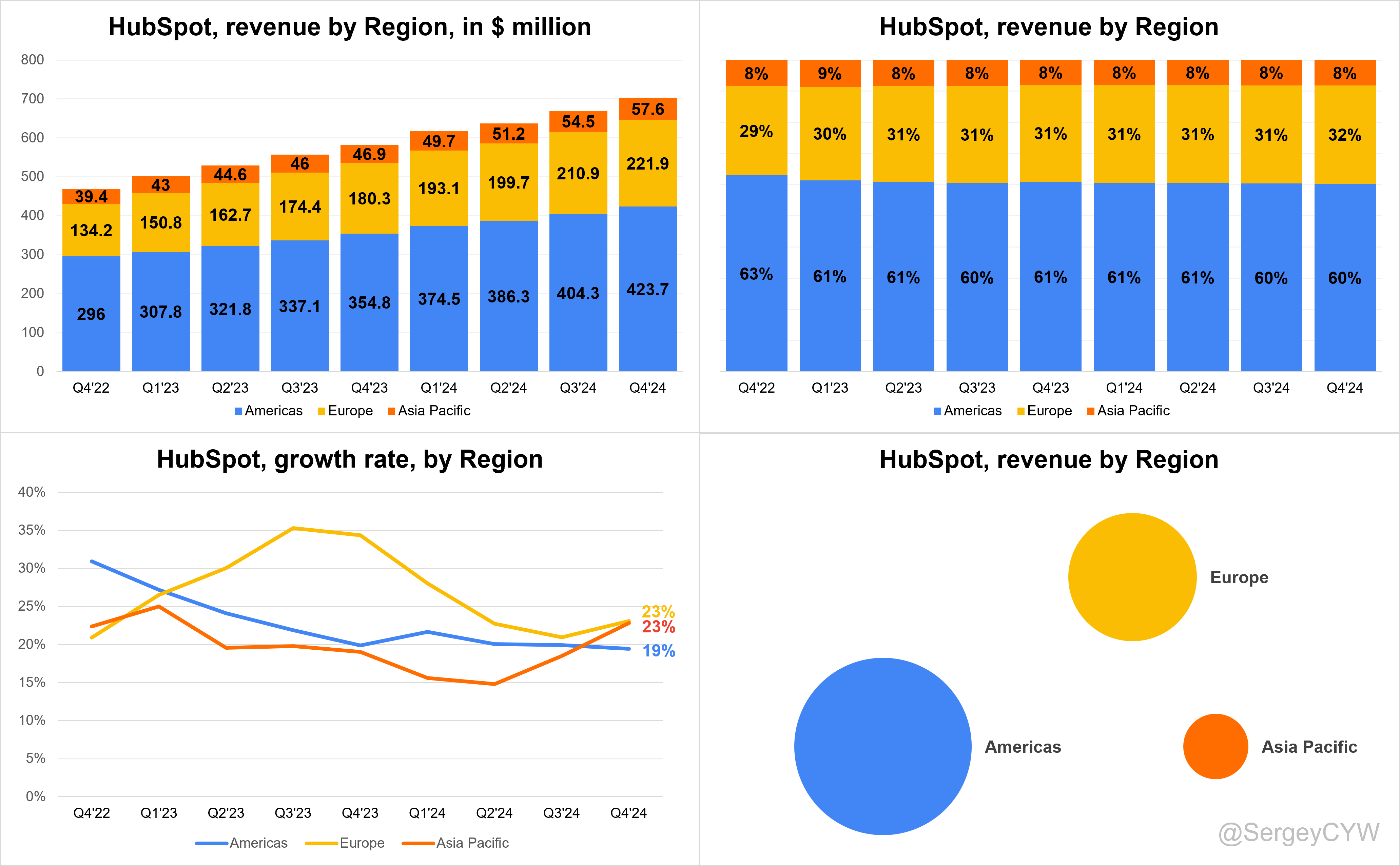

Revenue by Region

The Americas account for 60% of total revenue, making it HubSpot’s $HUBS largest market, with revenue growing +19% YoY in Q4.

Europe represents 32% of total revenue, also holding a significant share, and is growing at a faster pace of +23% YoY.

Asia Pacific contributes 8% of total revenue and is also growing as fast or faster than total revenue, at +23% YoY.

Market Leaders

Content Marketing Platforms

In March 2025, Gartner named $HUBS HubSpot a Leader in the Magic Quadrant for Content Marketing Platforms. This recognition positions HubSpot among vendors who "execute well against their current vision and are well positioned for tomorrow". The report, published on March 10, 2025, highlights HubSpot's broad ecosystem of technology partners, successful sales across multiple industries, and demonstrated ability to support enterprise-scale customers globally.

HubSpot's AI-powered innovations like Content Remix and Content Agent enable marketers to create personalized experiences at scale while demonstrating clear ROI.

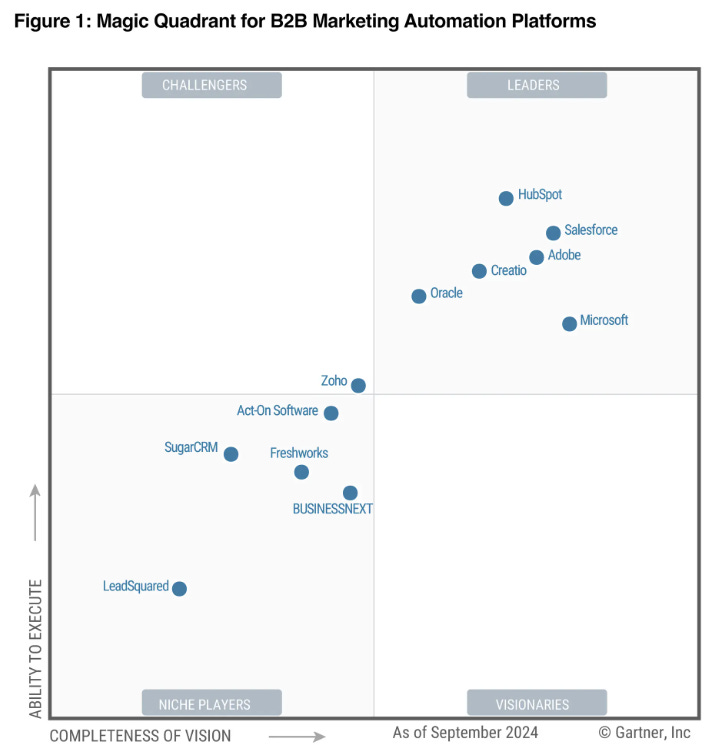

B2B Marketing Automation Platforms

$HUBS HubSpot has maintained its leadership position in the Gartner Magic Quadrant for B2B Marketing Automation Platforms for four consecutive years as of September 2024. This consistent recognition reflects HubSpot's sustained excellence and continuous product innovation in the marketing automation space.

Marketing Hub was evaluated based on Completeness of Vision and Ability to Execute. According to Nicholas Holland, VP of Product, evolving customer behavior demands connected tools and unified data for marketers to operate effectively. HubSpot’s strategy focuses on enabling growth through AI-powered features, including social and content agents, dynamic forms, and real-time marketing insights.

Customers

$HUBS HubSpot added 9,811 customers, with growth slowing to +21% YoY. While this addition is lower than the same period last year, customer growth remains solid and in line with revenue growth.

Customer Success Stories

HubSpot’s platform transformation through AI is driving measurable outcomes for its users. One notable example is the customer Transcribe, which highlighted the operational shift achieved by implementing the Customer Agent. Manual, time-intensive service workflows were replaced with streamlined, AI-driven processes. The agent now automates support tasks and achieves an average resolution rate of 42%, accelerating service efficiency while reducing team workload. This early traction validates the utility of embedded agents across customer-facing teams.

Content creation is another area of demonstrated success. Companies using Content Agent are publishing over 80% of their blog content with AI assistance. This enables faster, more cost-effective content marketing, particularly for SMBs scaling output without expanding headcount. Use of multi-input remix, podcast remix, and case study remix tools has led to meaningful improvements in publishing velocity and workflow optimization.

AI automation also delivered tangible impact in sales. AI-powered prospecting generated over 10,000 meetings for HubSpot’s internal sales teams in Q4 alone. Customers benefit from the same automation capabilities built into the Sales Hub and Breeze Copilot.

Internally, HubSpot is also acting as a case study for its own tools. The company’s AI support bot now resolves 35% of support tickets, maintaining high satisfaction while lowering cost to serve. Chat automation is even more efficient, handling 80% of website inquiries. These internal outcomes are now guiding customer implementations across mid-market and enterprise use cases.

Large Customer Wins

HubSpot continues to scale successfully upmarket. During Q4, the company recorded significant expansion in its enterprise-tier user base. Service Hub enterprise portals grew +100% QoQ, while customers with 100+ seats increased by 54% YoY. This reflects accelerating adoption among larger customers seeking AI-powered service operations.

Enterprise growth was supported by feature releases targeted at complex organizations, including support for sensitive data, UI extensions, and custom CRM development tools. These product investments directly contributed to a +21% YoY increase in large deals. The traction indicates growing acceptance of HubSpot’s unified platform among organizations previously limited by point solutions.

Awareness of HubSpot as a comprehensive customer platform increased +7 points globally. Co-selling with partners was a core driver of large deal activity, rising +68% YoY. The partner ecosystem, now more aligned with HubSpot’s upmarket strategy, played a crucial role in joint sales motions and implementation delivery.

The company also noted stronger multi-hub adoption, with 35% of Pro+ customers by ARR now using 4+ hubs, up from 28% a year earlier. This is a direct indicator of platform consolidation, higher ACV per account, and long-term stickiness across large-scale deployments.

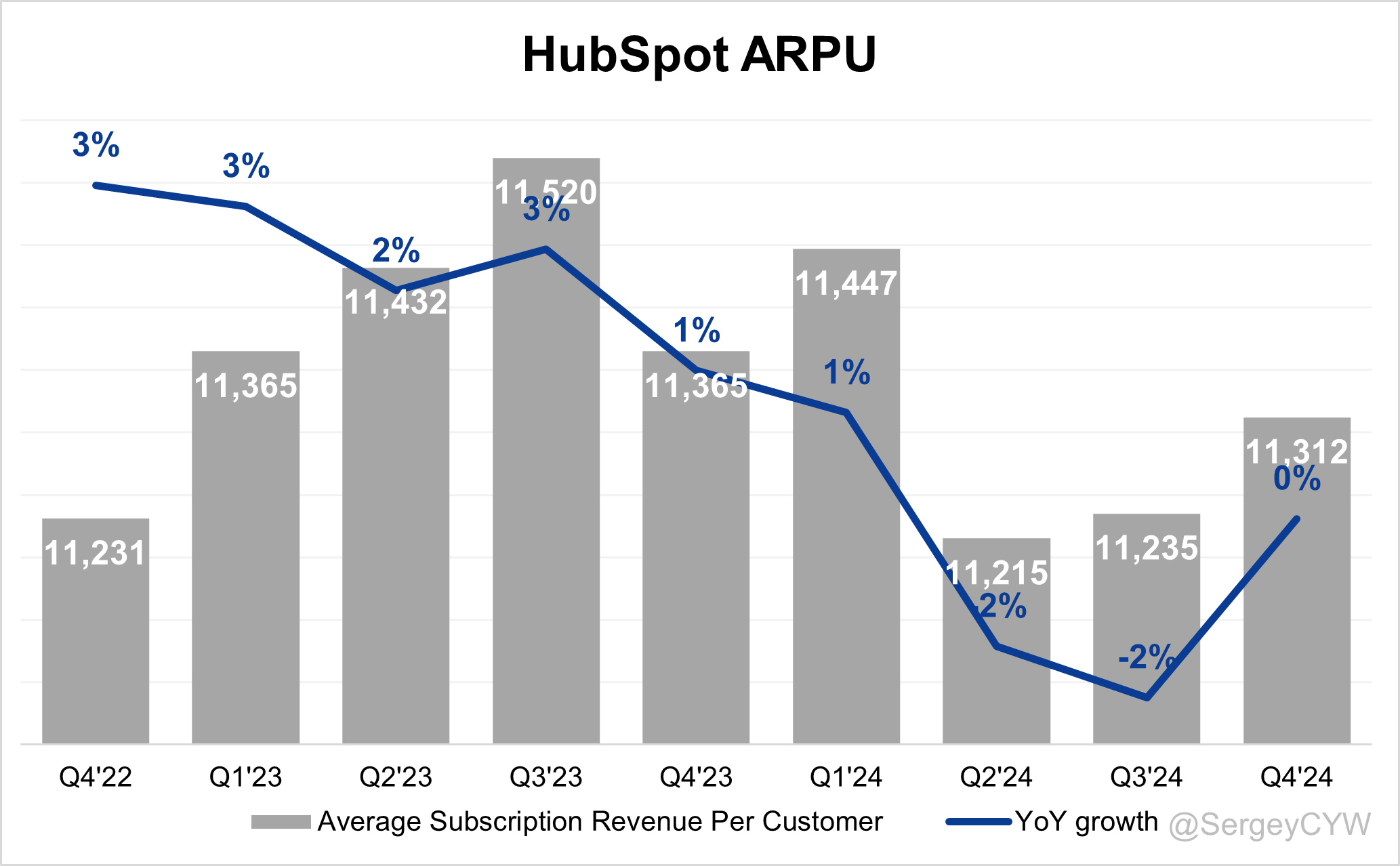

ARPU

$HUBS HubSpot's Average Subscription Revenue Per Customer was $11,312, which is in line with Q4 2023.

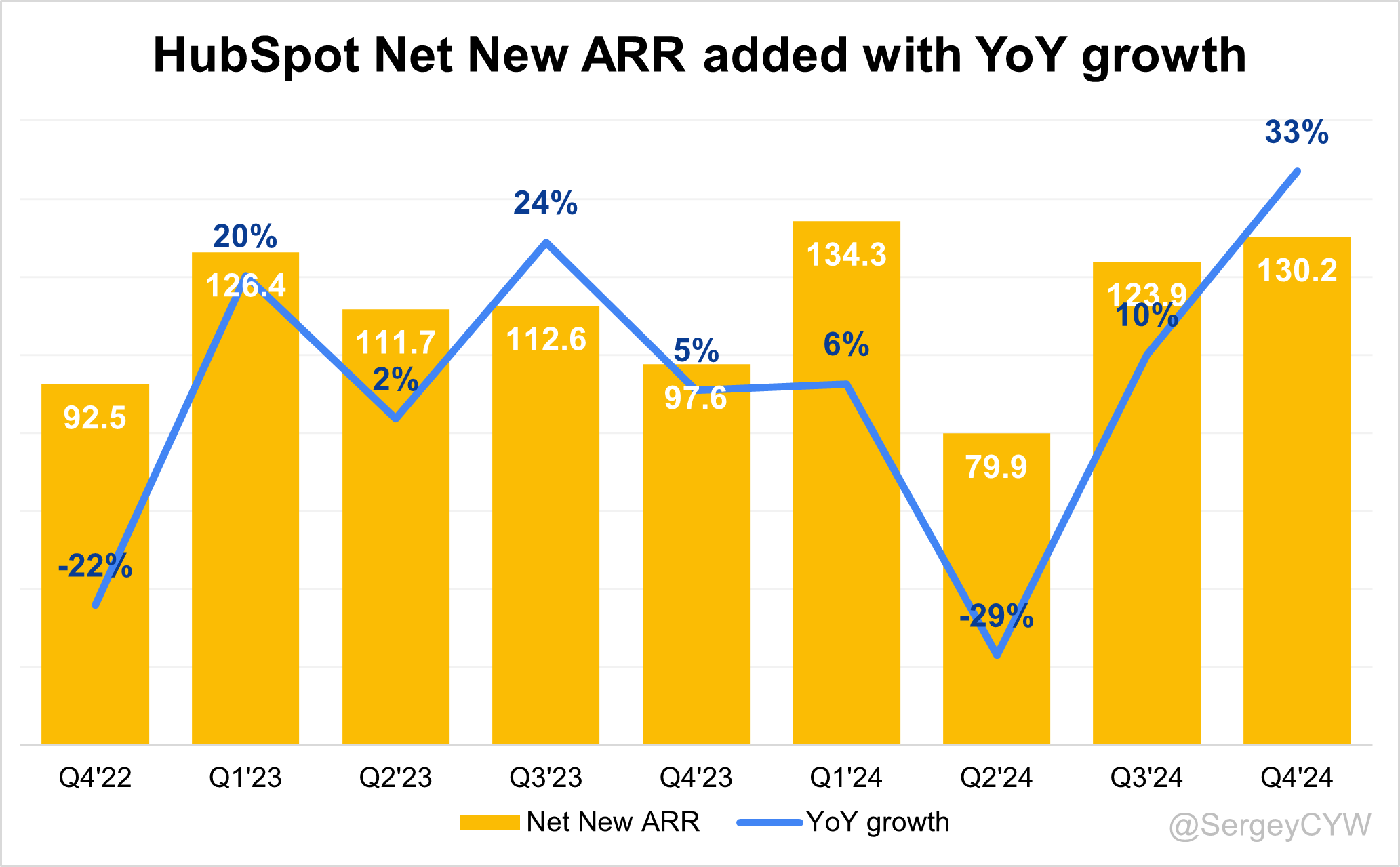

Net new ARR

$HUBS HubSpot added $130.2 million in net new ARR in Q4 2024, representing +33% year-over-year growth. This net new ARR addition was at a record level.

CAC Payback Period and RDI Score

$HUBS HubSpot's return on Sales & Marketing (S&M) spending stands at 28.8, with a CAC Payback Period worse than the SaaS average (the median for the SaaS companies I track is 20.8 months).

The R&D Index (RDI Score) for Q4 is 1.04, which is below the 1.2 median of the SaaS companies I monitor but still above the broader industry median of 0.7, indicating a healthy level of R&D investment.

An RDI Score above 1.4 is considered best-in-class, underscoring the importance of efficient R&D allocation.

Profitability

Over the past year, $HUBS HubSpot has experienced changes in its margins:

Gross Margin increased from 84.7% to 85.3%.

Operating Margin slightly improved from 16.8% to 18.9%.

Free Cash Flow (FCF) Margin significantly improved from 14.2% to 23.2%.

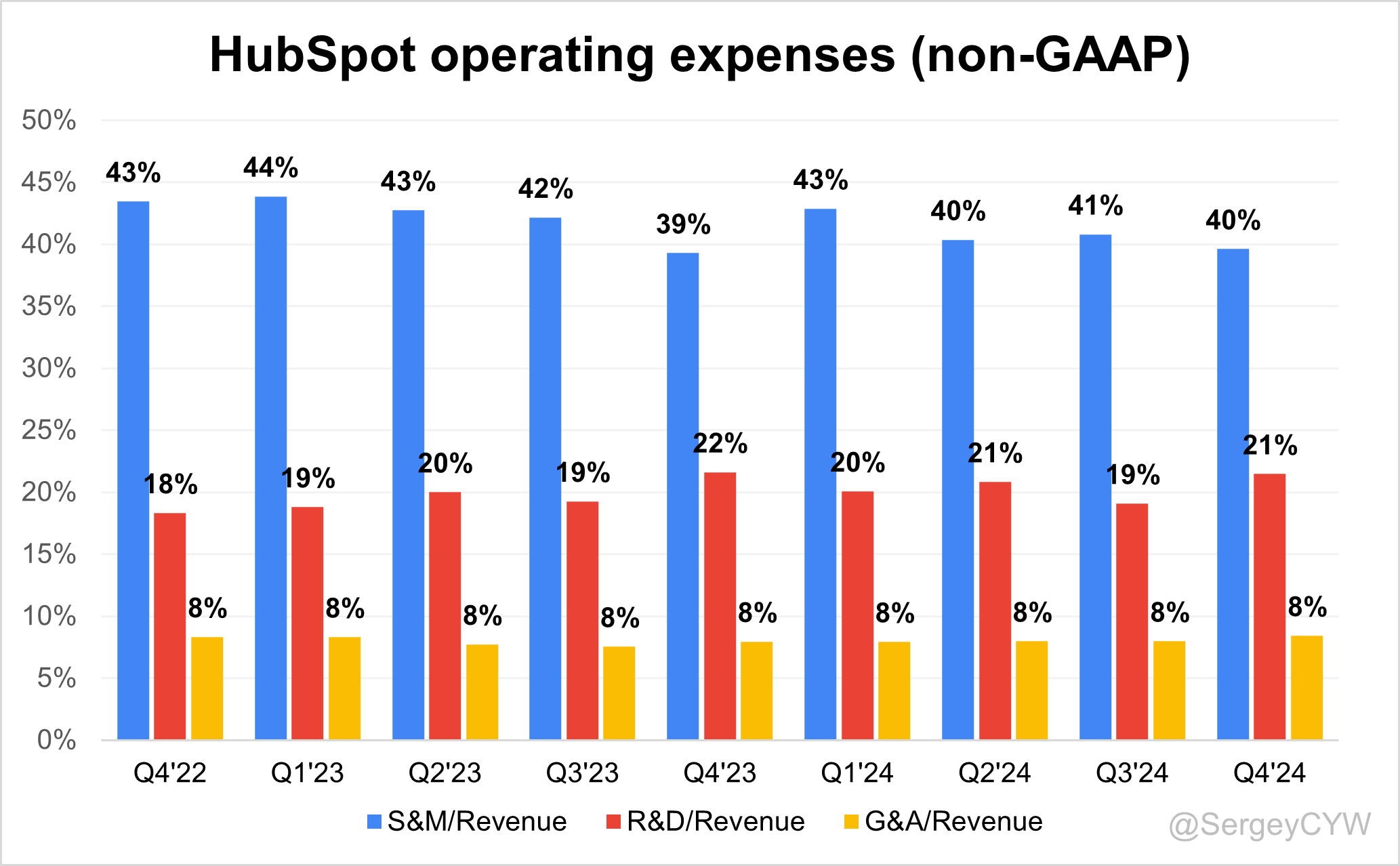

Operating expenses

$HUBS HubSpot's non-GAAP operating expenses have slightly decreased, driven by reduced Sales & Marketing (S&M) spending. S&M expenses have declined from 43% two years ago to 40%.

R&D expenses increased from 18% to 21%. The R&D share remains high at 21%, reflecting the company’s continued investment in future growth through platform enhancements and updates.

General & Administrative (G&A) expenses remained unchanged at 8%.

Balance Sheet

$HUBS Balance Sheet: Total debt stands at $781 million, while HubSpot holds $1,235 million in cash and cash equivalents, far exceeding its liabilities and reflecting a healthy balance sheet.

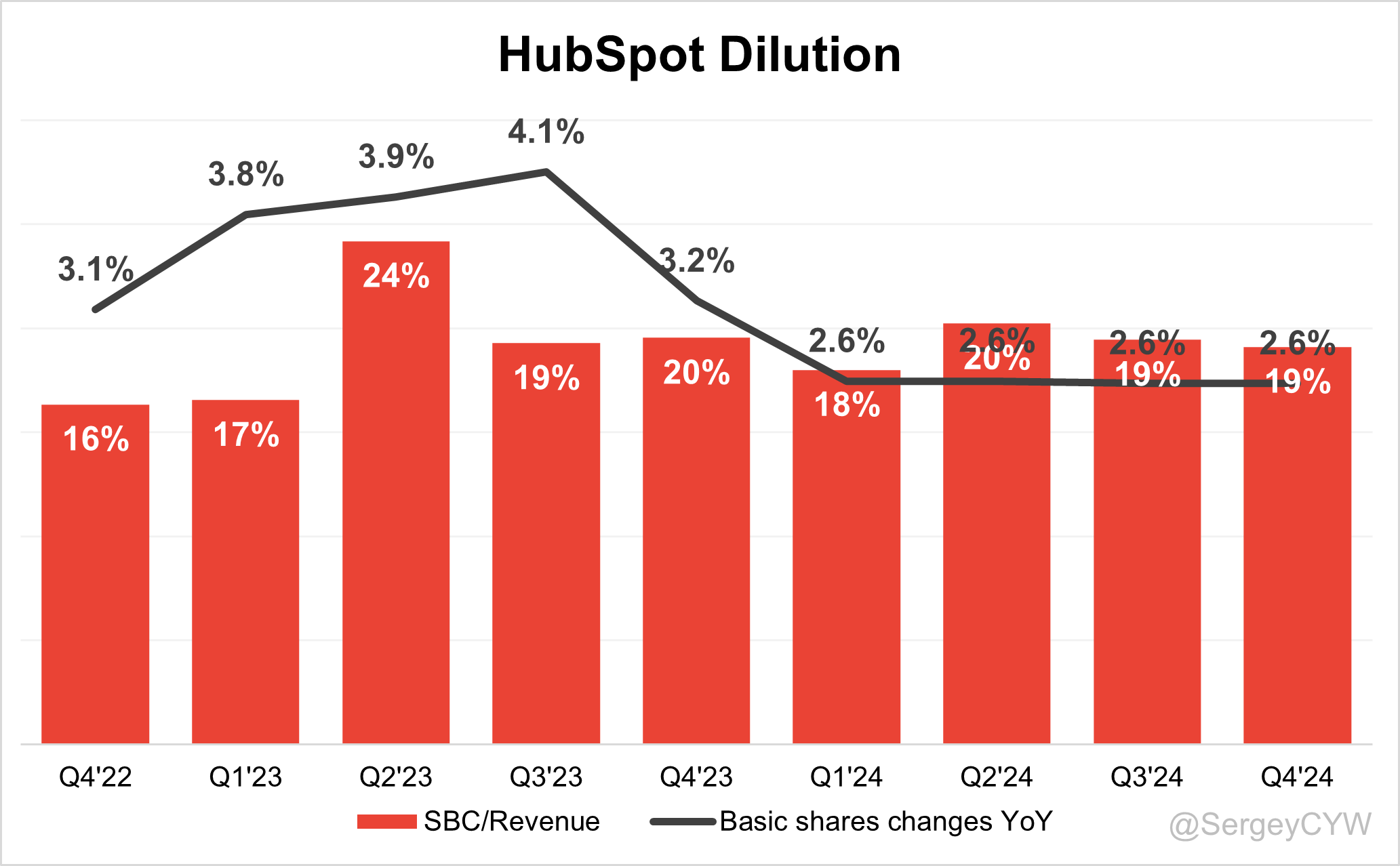

Dilution

$HUBS Shareholder Dilution: HubSpot’s stock-based compensation (SBC) expenses remain at 19% of revenue, approximately in line with the SaaS sector median.

Shareholder dilution is at a moderate level, with the weighted-average number of basic common shares outstanding increasing by 2.6% YoY.

Conclusion

$HUBS HubSpot is a strong player in the CRM sector. Gartner recognizes HubSpot’s leadership in the Magic Quadrant for Content Marketing Platforms, and the company has maintained its leadership position in the Magic Quadrant for B2B Marketing Automation Platforms for four consecutive years.

The company’s TAM is large, estimated at $101.41 billion in 2024 according to Fortune Business Insights, with a projected 13% CAGR. HubSpot's economic moat is built on high switching costs, driven by deep integration across marketing, sales, service, and operations. The company is actively adopting AI across its platform.

Leading Indicators:

• RPO growth of +23.9% is slightly above revenue growth.

• Billings growth significantly slowed to +13.3%, falling below revenue growth.

• Net new ARR additions reached a record level, up +33% YoY.

• Customer additions remained solid, though slightly lower than in the previous four quarters.

Key Indicators:

• Average Subscription Revenue Per Customer was $11,312, in line with last year.

• CAC Payback Period worsened to 28.8 months, which is significantly higher than the SaaS median.

• RDI Score came in at 1.04, also below the SaaS median.

The weak guidance for the next quarter raises some concerns. The forecasted deceleration in revenue growth could weigh on sentiment. However, healthy customer additions, RPO growth outpacing revenue, and strong net new ARR additions may offer some support for continued growth.

Valuation appears fair relative to revenue growth forecasts and in comparison with peers in the CRM sector.

I continue to keep $HUBS on my watchlist as a strong, well-positioned CRM platform.

Thank you for reading!

Follow me for more frequent updates on X/Twitter and Threads, and on LinkedIn. For visual infographics, check out Instagram, and for portfolio changes, follow me on SavvyTrader.

Disclaimer: This deep dive is for informational purposes only and does not constitute financial, investment, or trading advice.