Datadog: Leading Cloud Observability & Security

Deep Dive into $DDOG: Valuation, Segment Growth, Key Metrics, Profitability, Expenses, Product Launches, Customer Acquisition, Financial Stability, SBC/Revenue, and Shareholder Dilution.

Datadog: Company overview

About Datadog

Founded in 2010 and headquartered in New York City, Datadog provides a cloud observability and security platform. Its software solutions cover infrastructure monitoring, APM, log management, digital experience monitoring, database monitoring, network monitoring, and cloud security. Datadog went public on NASDAQ on September 19, 2019, with an IPO price of $27 per share.

Mission

Datadog enables organizations to monitor, optimize, and secure their entire technology stack. Its real-time insights empower businesses to make data-driven decisions and improve user experiences.

Sector

Datadog operates in the Technology sector under Software - Application. It serves a rapidly growing market of enterprise and mid-market customers demanding cloud-based observability and security solutions.

Competitive Advantage

Datadog’s unified observability platform integrates infrastructure monitoring, APM, log management, and cloud security into a single solution. It offers over 800 built-in integrations, more than any competitor, ensuring comprehensive system visibility. With an 81.7% non-GAAP gross margin and 30,000 global customers, including 3,610+ customers generating over $100K in ARR, Datadog maintains a 119% net revenue retention rate. Its AI-driven analytics, real-time insights, and scalability further solidify its leadership in cloud observability.

Total Addressable Market (TAM)

Datadog’s Total Addressable Market (TAM) has expanded significantly. Initially estimated at $35 billion, projections suggest it could reach $175 billion by 2034 at a 17.5% CAGR. The observability market is expected to hit $62 billion by 2026 with a 10.9% CAGR, while the Application Performance Monitoring (APM) market is forecasted to grow to $11.1 billion by 2027 at an 8.3% CAGR.

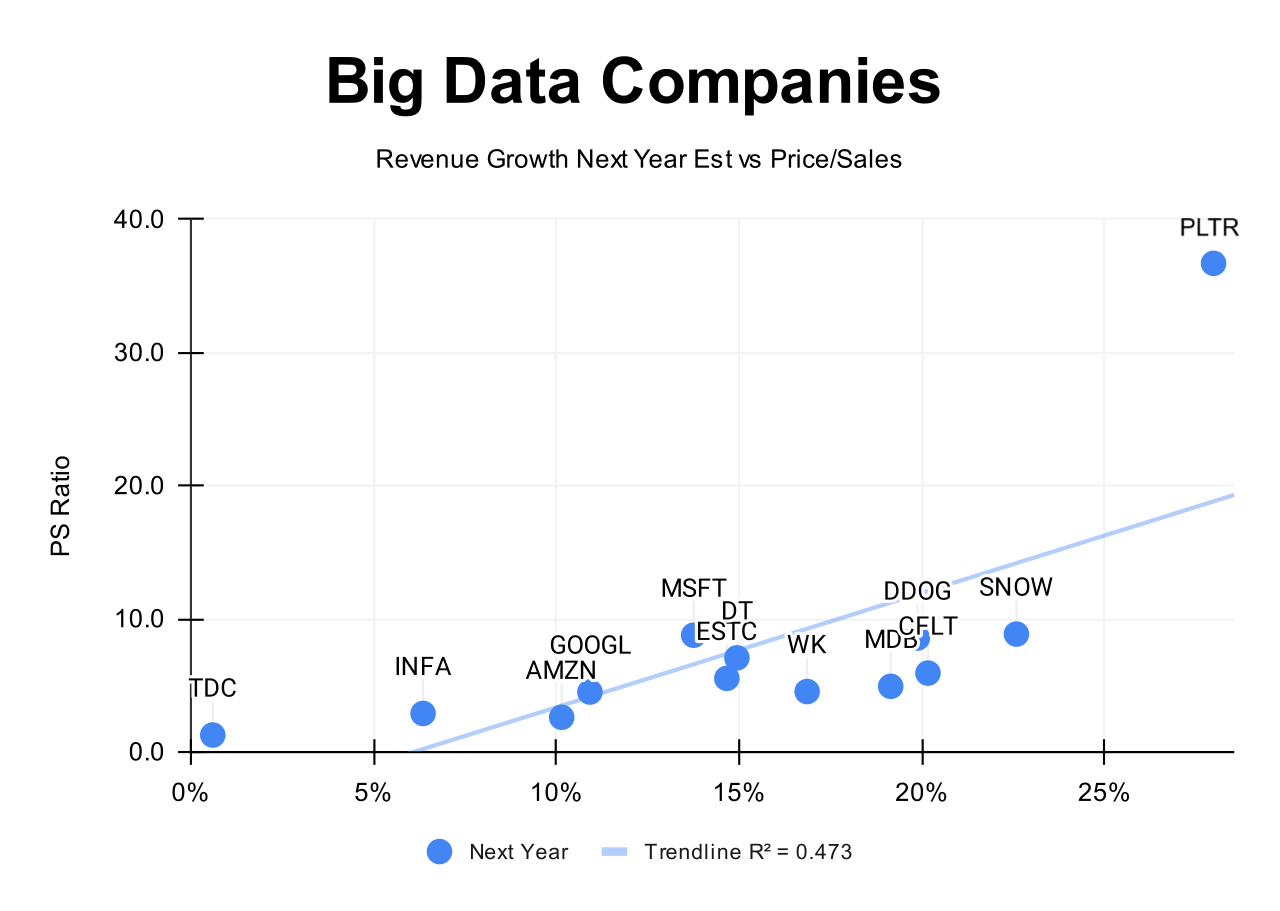

Valuation

$DDOG Datadog is trading at a Forward EV/Sales multiple of 10.3, significantly below the average of 16.8 and near its lowest valuation levels based on multiples from 2020.

$DDOG Datadog trades at a Forward P/E of 60.8.

The EPS growth forecast for 2026 is 22.8% (while revenue growth is projected at +19.9%), and P/E of 57.7 resulting in a 2026 PEG ratio of 2.5. Datadog is in the early stages of growth and reinvests most of its profits into further expansion through investments in R&D and S&M.

The PEG (Price/Earnings to Growth) ratio is a key tool for evaluating growth stocks, introduced by Peter Lynch.

PEG < 1: Undervalued – A ratio below 1 suggests the stock is undervalued. For example, if the P/E is 15 and earnings are expected to grow by 20%, the PEG would be 0.75, indicating a good buying opportunity.

PEG = 1: Fair Value – A PEG of 1 means the stock price matches its growth expectations, representing fair value.

PEG > 1: Overvalued – A PEG above 1 indicates the stock may be overvalued, as its price is higher than its projected growth rate, making it riskier.

Valuation comparison

Analysts forecast revenue growth of +19.9% for $DDOG next year, making it one of the highest projected growth rates in the segment, following $SNOW and $PLTR.

Considering the projected revenue growth for next year, the valuation based on the P/S multiple appears fair.

Analysts expect strong revenue growth, so let's examine the key metrics to determine whether these expectations are justified.

We'll evaluate the company's economic moat, which supports long-term revenue growth, analyze revenue trends and the forecast for next quarter, and identify key factors that could help the company exceed expectations and sustain future growth.

We'll assess the performance of key segments, the launch of new products and updates, customer acquisition growth, key financial metrics, financial stability, and margin trends.

Additionally, we'll review the SBC/Revenue ratio, shareholder dilution, and finally, draw conclusions on the company's outlook.

Economic Moat

Datadog has built a durable competitive advantage in cloud monitoring through economies of scale, network effects, brand strength, intellectual property, and high switching costs.

Economies of Scale

With a customer base exceeding 20,000 organizations, Datadog spreads fixed costs across a growing revenue base, reducing cost per user while maintaining competitive pricing. Its cloud-native architecture and subscription model drive operational efficiency and scalability.

Network Effect

More users generate more data, enhancing monitoring accuracy and analytics capabilities. Each additional customer increases platform value, reinforcing adoption and continuous improvement.

Brand Strength

Recognized as a leader in observability, Datadog is known for reliability and innovation. Its strong reputation attracts enterprise customers and fosters long-term loyalty.

Intellectual Property

Proprietary technologies enable seamless integration and advanced analytics, differentiating Datadog from competitors. Continuous AI-driven innovation positions the company for future market expansion.

High Switching Costs

Enterprises deeply integrated into Datadog’s platform face significant costs in downtime, retraining, and system reconfiguration, making transitions to competitors costly and complex. Strong customer retention reinforces recurring revenue stability.

Datadog’s moat strengthens its leadership in cloud observability, ensuring long-term competitive positioning and sustained growth.

Revenue growth

$DDOG Datadog's revenue growth has stabilized since Q2 2023 at around 25%. RPO growth stands at 23.4% YoY, slightly below revenue growth, with mid-30s% normalized growth.

Billing growth has significantly accelerated to +25.7% YoY, exceeding revenue growth. Since revenue recognition is usage-based, billings growth does not immediately impact revenue.

Based on the next quarter's forecast, if the company exceeds its projection by 3.5%, as it did in Q4, Q1 revenue growth would reach 25.4%, indicating a slight acceleration in growth.

It's worth noting that Datadog operates on a usage-based model, which makes RPO growth more volatile compared to companies with a subscription-based model.

Segments and Main Products.

Segments

Datadog operates primarily in six segments: Infrastructure Monitoring, Application Performance Monitoring (APM), Log Management, Security Monitoring, Synthetic Monitoring, and Network Performance Monitoring. Infrastructure Monitoring provides real-time visibility into IT infrastructure health, including servers, databases, and cloud services. Application Performance Monitoring (APM) traces application requests across distributed systems to identify bottlenecks and optimize performance. Log Management collects and analyzes log data for troubleshooting and integrates seamlessly with monitoring services. Security Monitoring detects and responds to security threats in real-time, including threat detection, compliance monitoring, and incident response. Synthetic Monitoring simulates user interactions to assess web application uptime and API performance from user perspectives. Network Performance Monitoring tracks network traffic across cloud and on-premises environments to identify latency issues.

Main Products

Datadog's key products include Datadog Agent, Real User Monitoring (RUM), Dashboards & Visualization tools, Incident Management, and extensive Integrations. Datadog Agent is a lightweight collector gathering metrics, logs, and events from infrastructure components. Real User Monitoring (RUM) captures client-side performance metrics and errors to improve user experience. Dashboards & Visualization tools offer customizable real-time visualization of metrics across applications and infrastructure. Incident Management consolidates alerts for effective incident resolution. Datadog supports over 800 integrations with third-party services including AWS, Azure, GCP, CI/CD tools, and collaboration platforms.

Security & SIEM

Datadog's Security & Cloud SIEM solution integrates observability with security by providing real-time threat detection, automated responses, and extensive visualization capabilities. It ingests security logs from over 750 integrations, normalizes data for centralized analysis, and provides historical data retention exceeding 15 months for detailed investigations. Security teams benefit from automated workflows (300+ actions) aligned with MITRE ATT&CK framework standards and customizable detection rules (400+ detections) maintained by Datadog's dedicated Security Research team.

Multi-Cloud Monitoring

Datadog's Multi-Cloud Monitoring unifies metrics, logs, traces, and security data from multiple cloud environments (AWS, Azure, GCP, Alibaba Cloud) into one integrated platform. It offers synchronized dashboards for consistent monitoring across clouds, host and container visualizations for simplified management of dynamic environments, and comprehensive monitoring of serverless functions. This unified approach enables organizations to effectively manage complex multi-cloud infrastructures from a single interface.

Main Products Performance in the Last Quarter

Infrastructure Monitoring

Revenue from infrastructure monitoring exceeded $1.25 billion in ARR. Growth driven by enterprise adoption and expansions. 45% of Fortune 500 now Datadog customers, up from 42% last year. Mid-market and SMB adoption steady. New customer wins include a Fortune 100 oil and gas company migrating from on-prem to cloud, replacing two legacy monitoring tools. Competition remains in legacy on-prem solutions, but cloud adoption drives growth.

Application Performance Monitoring (APM)

APM and related products surpassed $750 million in ARR. Customers using Datadog for end-to-end application visibility grew. Error Tracking launched, allowing users to track errors across logs, applications, and user sessions. Expansion in Database Monitoring, Continuous Profiler, and Real User Monitoring strengthens the offering. Increased enterprise adoption but still a significant opportunity as more than half of customers do not use all three observability pillars.

Log Management

Log management surpassed $750 million in ARR, driven by Flex Logs adoption. Strong demand from enterprises looking for cost-effective long-term log storage and analytics. Seven-figure deals closed with a U.S. financial institution and a federal health insurer migrating to Flex Logs for cost savings. Security SIEM adoption also expanding, with more integrations and migration tools developed to displace legacy providers.

Security Monitoring & SIEM

Security product adoption accelerating. 7,000+ customers now use at least one Datadog security product. Demand for Cloud SIEM increasing, driven by cost and efficiency concerns from enterprises. Launched Code Security, Kubernetes Security Posture Management, and Agentless Scanning. Key win: high six-figure deal with a federal health insurer replacing a costly SIEM. Opportunity remains in displacing entrenched security tools.

Synthetic Monitoring

Launched mobile app testing for iOS and Android on real devices. Expansion into session replay to help customers investigate mobile performance issues. Product analytics in early stages but gaining interest. Large Brazilian retail company adopted Datadog to improve customer experience, leading to higher app store ratings. Growing enterprise demand for unified front-end and back-end monitoring.

Network Performance Monitoring

Demand increasing as enterprises move workloads to the cloud. Expanded deep insights for Amazon SQS and MongoDB monitoring. Strong push for cloud-native network observability to displace traditional tools. New customer growth from enterprises migrating from legacy network monitoring to unified observability. Enterprise deals highlight cost savings and operational efficiency.

Multi-Cloud Monitoring

New integrations expanding coverage across AWS, Azure, GCP, and Oracle Cloud Infrastructure (OCI). Datadog now offers unified monitoring for OCI stacks, enhancing visibility for multi-cloud enterprises. More than 850 integrations now available, up from previous quarters. Growing need for AI observability, with 3,500+ customers sending AI/ML usage data into Datadog.

Product Innovations & Updates

Over 400 new features released in 2024, reinforcing Datadog’s leadership in observability. Bits AI expanded for incident management and autonomous investigations. LLM Observability now in general availability, helping customers monitor AI model performance. Datadog OnCall launched, solving modern incident response challenges. Flex Logs now in GA, offering high-volume, long-term log retention at lower costs. Kubernetes Autoscaling introduced, optimizing cloud resources dynamically. Strong focus on security posture management, observability pipelines, and software delivery improvements.

Market Leader

$DDOG Datadog has been recognized as a Leader in the Gartner Magic Quadrant for Observability Platforms for the fourth consecutive year, underscoring its consistent execution and visionary approach in the rapidly growing observability market. This accolade reflects Datadog's ability to innovate and adapt to customer needs, offering robust monitoring and analytics capabilities that enhance operational efficiency and performance tracking across various sectors.

Datadog has been named a Leader in the inaugural Gartner Magic Quadrant for Digital Experience Monitoring (DEM), recognizing its comprehensive DEM solution, which includes Synthetic Monitoring, Real User Monitoring (RUM), Product Analytics, Session Replay, and Error Tracking for browser and mobile applications.

Customers

$DDOG Datadog added +120 new customers spending >$100K in Q4 2024, which is in line with the average over the past two years, with a growth rate of 13% YoY.

However, it’s important to note that this cohort now constitutes 87% of the total and is no longer classified as large customers. Datadog is currently focusing on targeting even larger customers by expanding the number of products available on its platform.

Large Customer Wins

U.S. Financial Institution

Signed a 7-figure annualized deal to replace costly legacy logging tools. Moved to Datadog Flex Logs and Observability Pipelines to reduce expenses and reallocate savings toward broader observability transformation. Started with four Datadog products, replacing four legacy solutions.

Brazilian Retail Company

Landed a 7-figure annualized contract to improve application performance and digital customer experience. Previous open-source observability tools failed to provide visibility into customer journeys. Higher app store ratings and better user confidence achieved through Datadog’s platform. Started with five Datadog products.

American Entertainment Company

Secured a 6-figure deal to improve customer experience tracking across in-store kiosks and mobile apps. Deployed Datadog’s unified platform for front-end and back-end correlation, improving service reliability. Displaced two commercial observability and analytics tools.

U.S. Federal Health Insurer

Signed a high 6-figure deal to replace an expensive and underutilized SIEM tool. Datadog Flex Logs and Cloud SIEM within GovCloud deployed for better compliance and cost reduction. Expected to save over $1 million per year while improving security.

Fortune 100 Oil & Gas Company

Signed a 7-figure expansion deal to migrate thousands of on-prem hosts to the cloud. Replaced two legacy infrastructure and network monitoring tools, leading to estimated $1 million in operational cost savings. Company expanded to 14 Datadog products, reducing incident-related losses by over $10 million per year.

Leading Security Software Company

Secured a 7-figure expansion deal to replace an inefficient homegrown log management system. Datadog Flex Logs deployed, cutting costs, reducing mean time to resolution, and increasing user productivity. Expected over $1 million in savings per year, expanded to eight Datadog products.

Customer Success Stories

AI-Native Customers Driving Growth

AI-native companies now contribute 6% of Datadog’s ARR, up from 3% a year ago. These customers account for 5 percentage points of Q4 revenue growth, underscoring AI’s growing impact on observability demand.

Enterprise Expansion in Fortune 500

45% of Fortune 500 companies now use Datadog, up from 42% in 2023. Median ARR per Fortune 500 customer remains below $500K, indicating substantial room for expansion.

Cross-Sell & Product Adoption Growth

Customer adoption of multiple products continues to rise. 83% use two or more products, 50% use four or more, and 12% use eight or more. Growth driven by APM, Log Management, Flex Logs, Security, and AI monitoring solutions.

Record Bookings & Customer Expansion

Q4 achieved record bookings exceeding $1 billion, reflecting strong land-and-expand strategies. Net revenue retention remains in the high 110s, driven by increased usage and adoption of new Datadog products.

Security Product Growth in Large Enterprises

More than 7,000 customers now use Datadog’s security products. Security-related customer wins highlight increasing demand for cloud-native security solutions alongside observability.

Customers adoption

$DDOG Datadog is focusing on large customers by expanding the number of products available on its platform. A key metric for evaluating customer adoption of new products is the usage of 2+, 4+, 6+, and 8+ products.

Over the last quarter, the percentage of customers using 4+ products increased by 1 percentage point, while the other cohorts remained at the same level.

The growth in customers using 8+ products was 47% YoY, and the growth in customers using 6+ products was 30% YoY, both outpacing revenue growth. However, the addition of new customers in these cohorts has slowed when recalculated based on the total customer base.

Retention

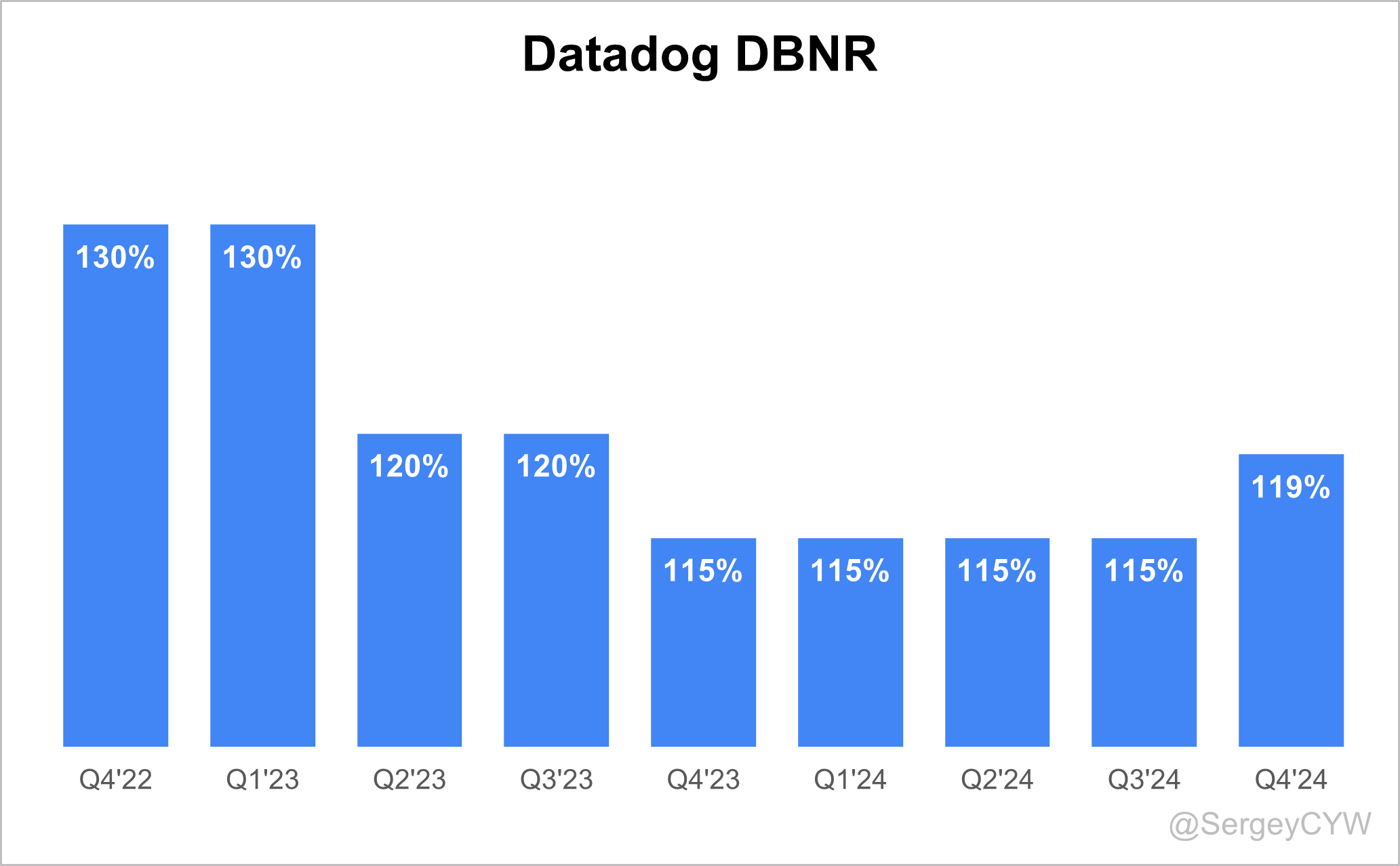

$DDOG Datadog's Dollar-Based Net Retention Rate (DBNRR) for the last quarter grew to 119% and remains at a high level, slightly above the 117% median for the SaaS companies I monitor.

Net new ARR

$DDOG Datadog added $191M in net new ARR in Q4 2024, representing 13% YoY growth—the highest net new ARR addition in the last three years. Net new ARR growth has recovered following the slowdown experienced at the end of 2022 and the beginning of 2023.

CAC Payback Period and RDI Score

$DDOG Datadog's return on Sales & Marketing (S&M) spending is 12. The Customer Acquisition Cost (CAC) Payback Period is at a high level among SaaS companies, with the median for the SaaS companies I track being 20.8.

Datadog is typically a market leader in terms of CAC Payback Period, as the company allocates a higher percentage of its spending to Research & Development (R&D) than to S&M. The company prioritizes innovation and new product launches.

The R&D Index (RDI Score) for Q4 stands at 0.85, below the median of 1.2 for the SaaS companies I monitor, but still a strong value, above the industry median of 0.7. Datadog attracts customers through high R&D spending, focused on product improvements and new module launches. Increased R&D expenditures lower the RDI Score but enhance the company’s competitive advantage.

An RDI Score above 1.4 is considered best-in-class performance. The industry median of 0.7 highlights the importance of efficient R&D investment.

Profitability

Over the past year, $DDOG Datadog's margins have changed as follows:

Gross Margin decreased from 83.4% to 81.7%.

Operating Margin slightly decreased from 28.3% to 24.3%.

Free Cash Flow (FCF) Margin slightly decreased from 34.1% to 32.6%.

The company has been profitable under GAAP net income for the past six quarters.

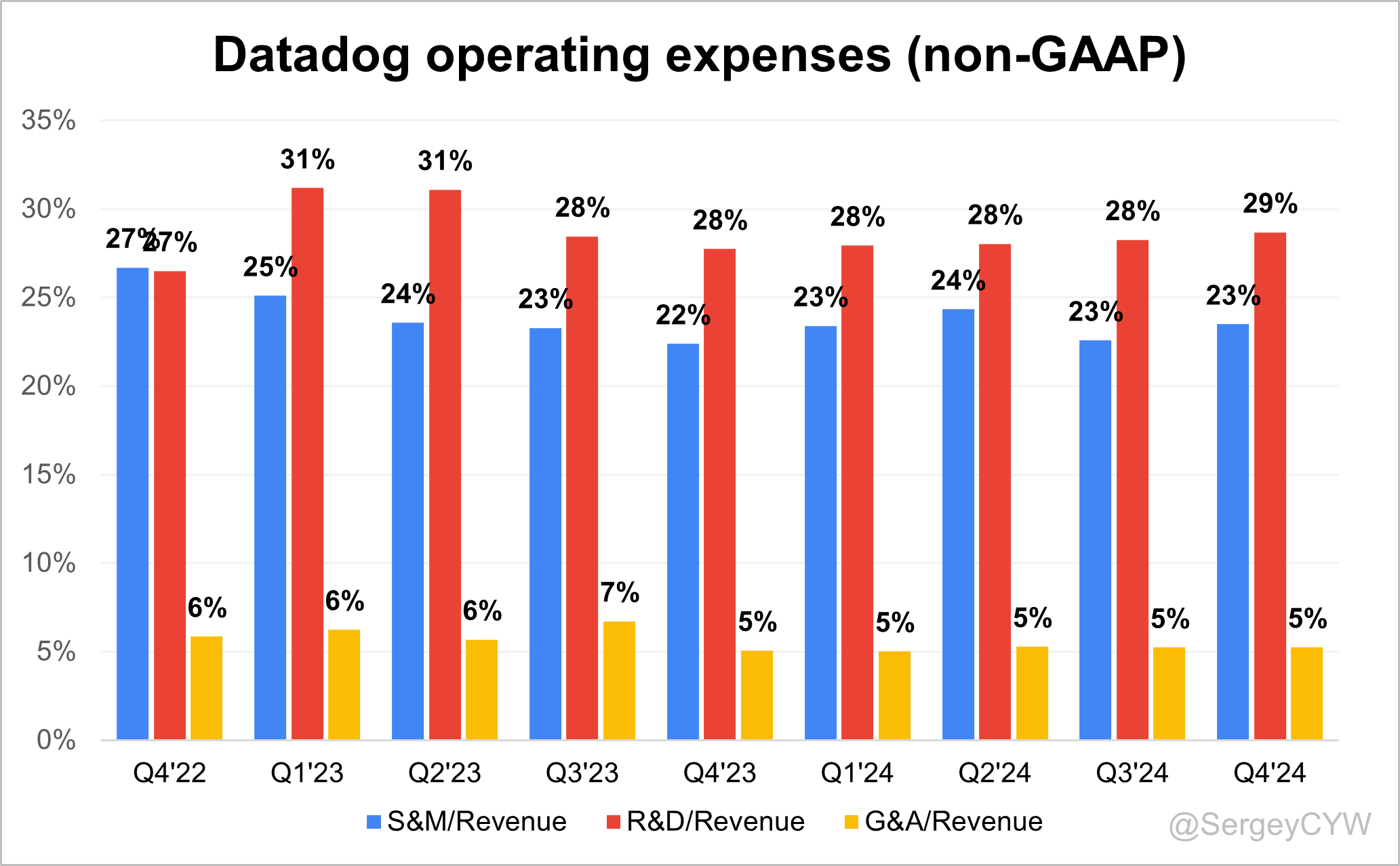

Operating expenses

$DDOG Non-GAAP Operating Expenses: Datadog's non-GAAP operating expenses have gradually decreased due to lower spending on S&M and G&A. R&D expenses have remained at a high level and have even increased slightly.

It is noteworthy that Datadog is one of the few companies that spends more on R&D than on S&M, allowing it to continuously enhance its product and release new modules, expanding its platform. G&A expenses have decreased and are now at 5%.

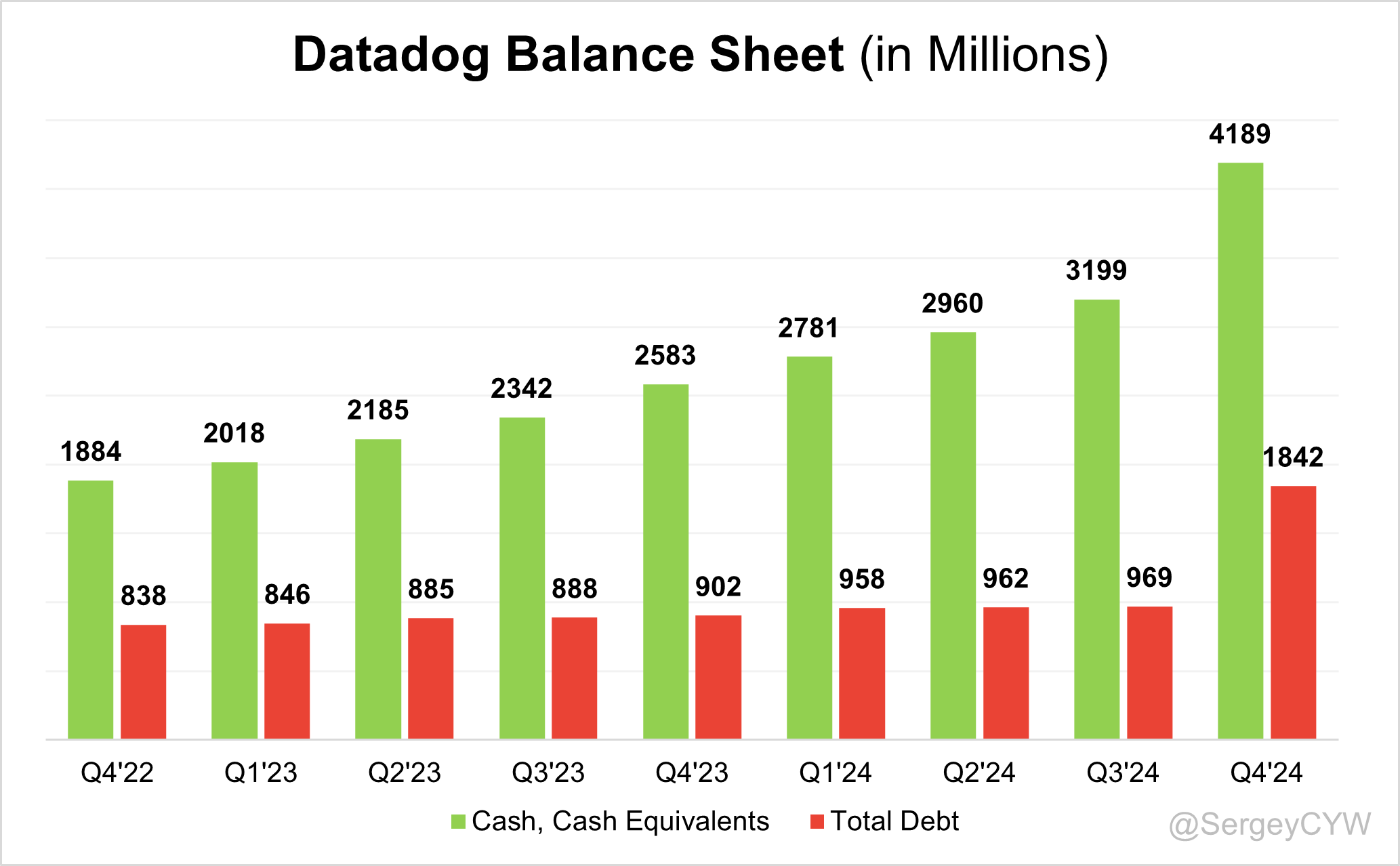

Balance Sheet

$DDOG Balance Sheet: Total debt stands at $1,842M, while Datadog holds $1,856M in cash and cash equivalents, exceeding total debt and ensuring a healthy balance sheet.

Dilution

$DDOG Shareholder Dilution: Datadog's stock-based compensation (SBC) expenses decreased in the last quarter to 21% of revenue.

Shareholder dilution remains under control, with the weighted-average number of basic common shares outstanding increasing by 3.5% YoY, although it is worth noting that dilution has increased from 1.8% in the previous year.

Conclusion

$DDOG Datadog continues to drive innovation, launching multiple new products and updates. The company prioritizes R&D, with R&D expenses exceeding S&M expenses, demonstrating the effectiveness of its investments as customers increasingly adopt more of its products.

Leading Indicators

RPO growth of +23.4% exceeded revenue growth, with mid-30s% normalized growth.

Billings growth accelerated to +25.7%, outpacing revenue growth.

Adoption of 4+ modules increased by +1 percentage point QoQ, while other cohorts remained stable.

Key Indicators

Net Dollar Retention (NDR) increased to 119%.

CAC Payback Period improved to 12.0 months, one of the best among SaaS companies.

RDI Score stood at 0.85, below the median compared to other SaaS companies I track, but Datadog’s strategy focuses on high R&D investments and growth through innovation.

The next quarter forecast suggests a slight acceleration in revenue growth to +25.4%. Strong leading indicators such as adjusted RPO and Billings growth support continued revenue expansion. However, new customer additions and adoption were not particularly strong in Q4, and I expect improved customer adoption next quarter.

The valuation based on Forward EV/Sales multiples appears reasonable. The company recently entered the security cloud SIEM market and announced LLM Observability, now in general availability. Additionally, Datadog OnCall and Flex Logs are now in GA, offering high-volume, long-term log retention at lower costs. Kubernetes Autoscaling was also introduced, optimizing cloud resources dynamically, unlocking further growth opportunities.

Datadog continues to strengthen its competitive advantage, consistently launching new products and updates. Its leadership is reaffirmed by Gartner's quadrants.

$DDOG is one of my top ten portfolio holdings. In January 2025, following a strong quarterly report, I slightly increased my position, which now stands at 7.3%.

Hi I had a few questions regarding your CAC calculations. You mentioned in another post it was previous quarter's S&M expenses / net new ARR added in the current period * Gross Margin

1) Where did you get net new ARR of $191M? I found S&M of last quarter of $188M and gross margin of roughly 80% but could not find ARR, unless you calculated yourself.

2) Even so, when I make the calculation, it comes out to 188/(191*.80) = 1.23 which is not anywhere close to the 12 you calculated.

3) On a separate note I saw Brian another person on Finx post his CAC for DDOG with a negative trend - https://x.com/Brian_Stoffel_/status/1903098385785118828

"How long it takes (in subscription gross profit) for a new customer to payback the cost to get them (via sales and marketing)"

I'm aware everyone has their own interpretation of how best to calculate, but curious if you had any thoughts?