CrowdStrike, GitLab Q4 2025 Earnings

$CRWD, $GTLB Earnings analysis with review of financial performance, key metrics, operating expenses, dilution, customer growth, future outlook

Table of Contents

Detailed Earnings Analysis:

CrowdStrike CRWD 0.00%↑ , GitLab GTLB 0.00%↑ .

CrowdStrike

Financial Results:

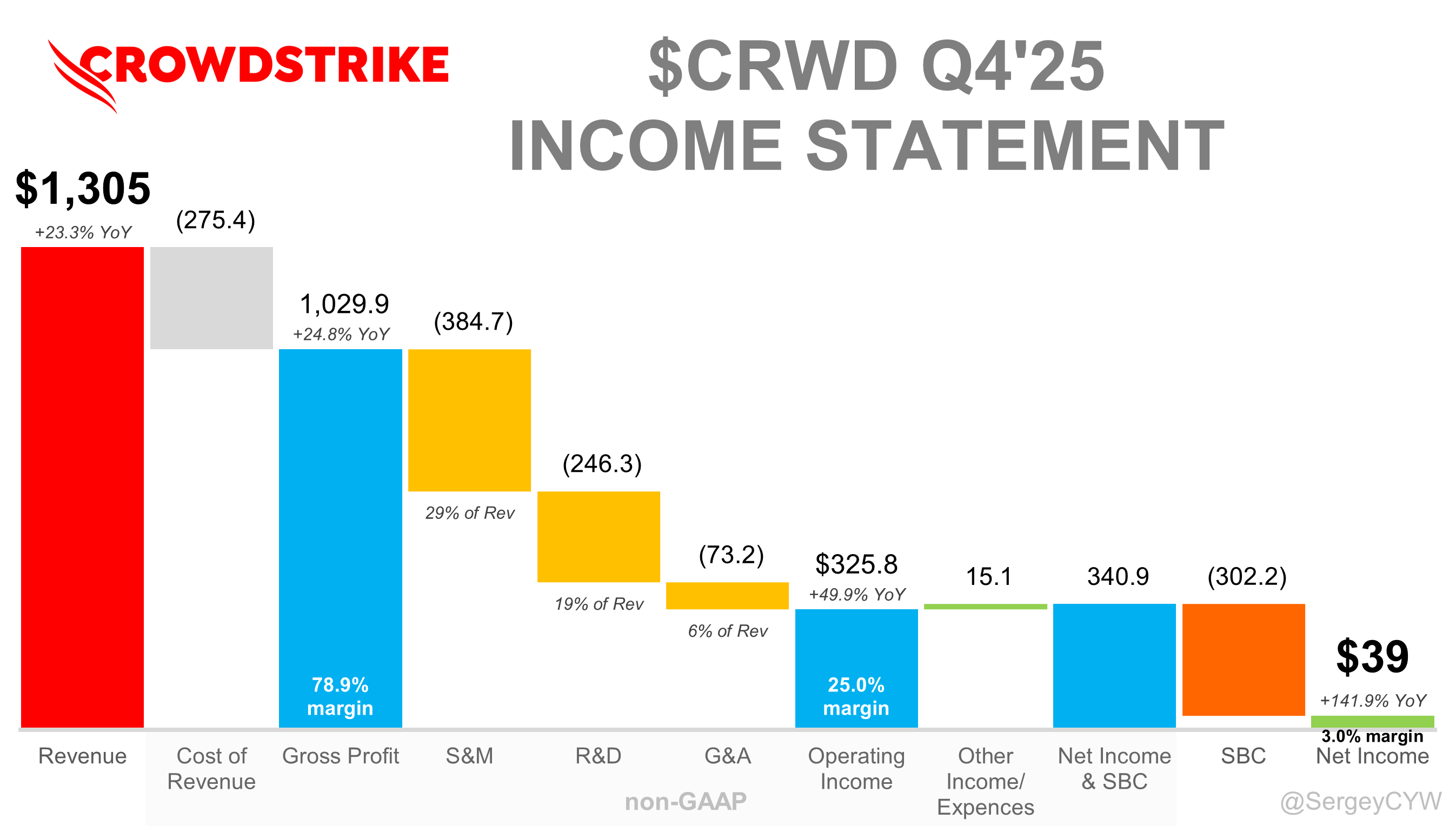

↗️$1,305M rev (+23.3% YoY, +5.8% QoQ) beat est by 0.7%

↗️GM* (78.9%, +1.0 PPs YoY)🟢

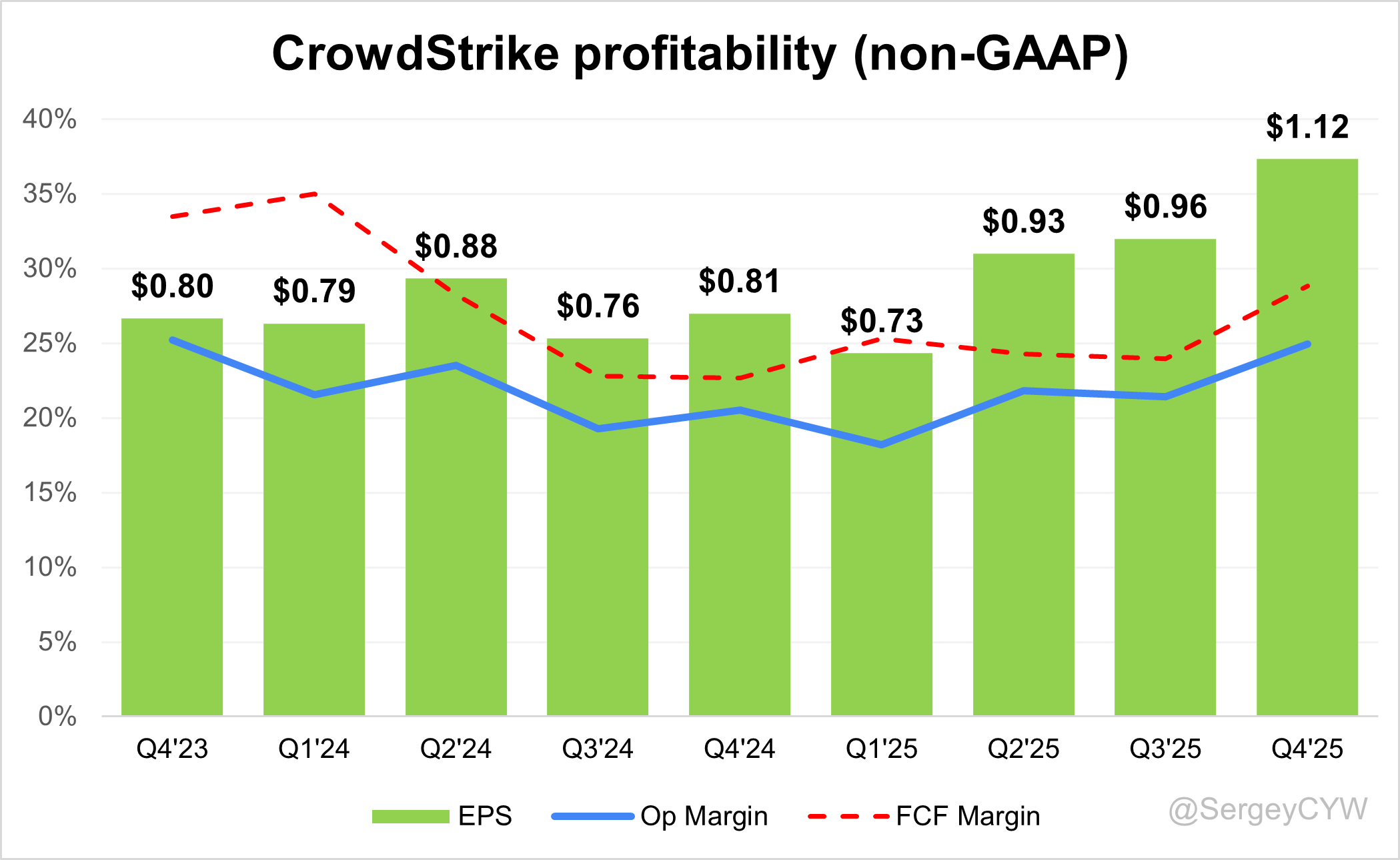

↗️Operating Margin* (25.0%, +4.4 PPs YoY)

↗️FCF Margin (28.8%, +6.2 PPs YoY)

↗️Net Margin (3.0%, +11.7 PPs YoY)

↗️EPS* $1.12 beat est by 1.8%🟢

*non-GAAP

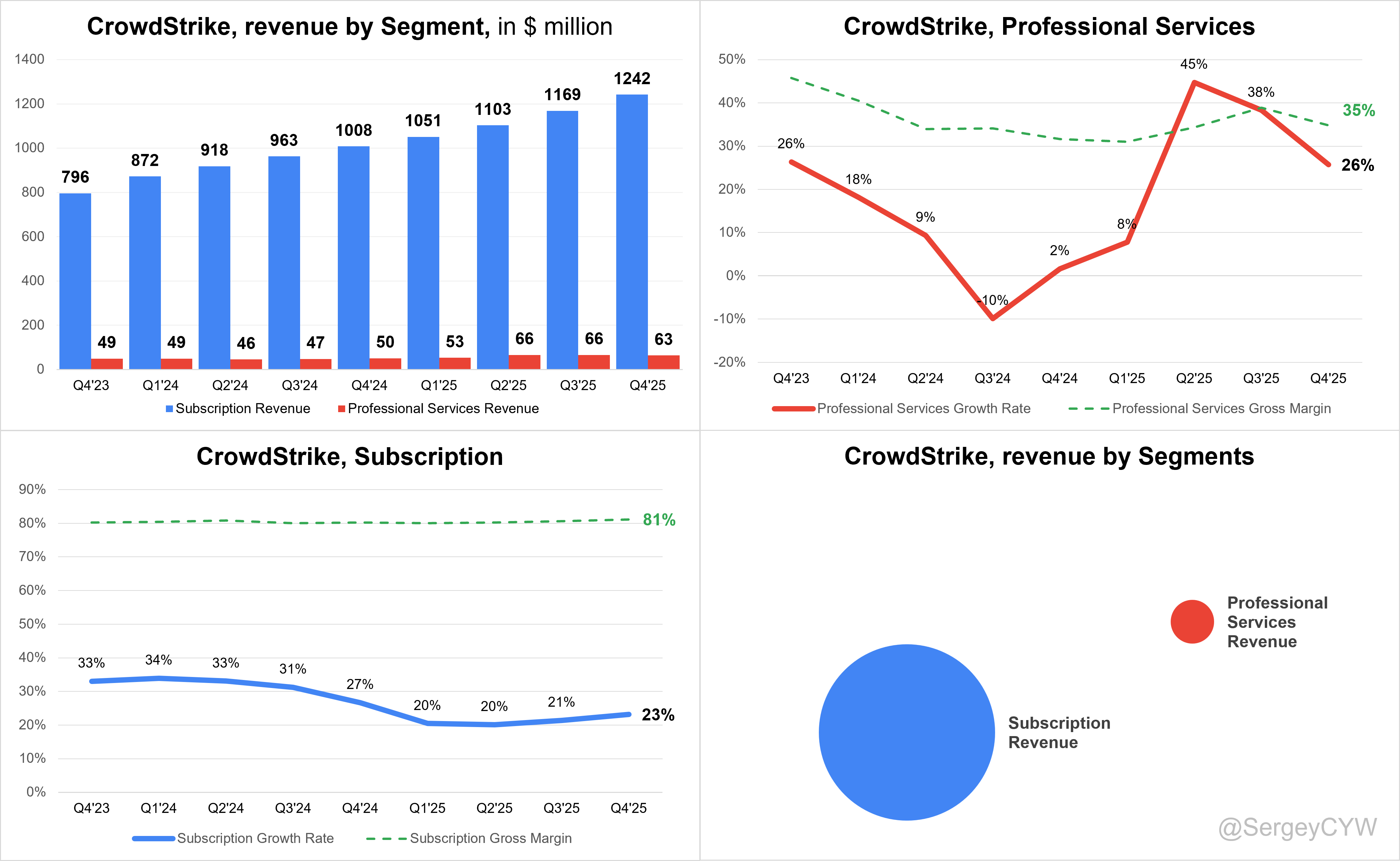

Revenue By Segments

Subscription

➡️Subscription Revenue $1,242M (+23.2% YoY)🟡

↗️GM* (81.1%, +0.9 PPs YoY)🟢

Professional Services

↗️Professional Services Revenue $63M (+25.7% YoY)

↗️GM* (34.8%, +3.2 PPs YoY)

Key Metrics

↗️DBNR Net Retention Rate 115%

➡️DBGR Gross Retention Rate 97%

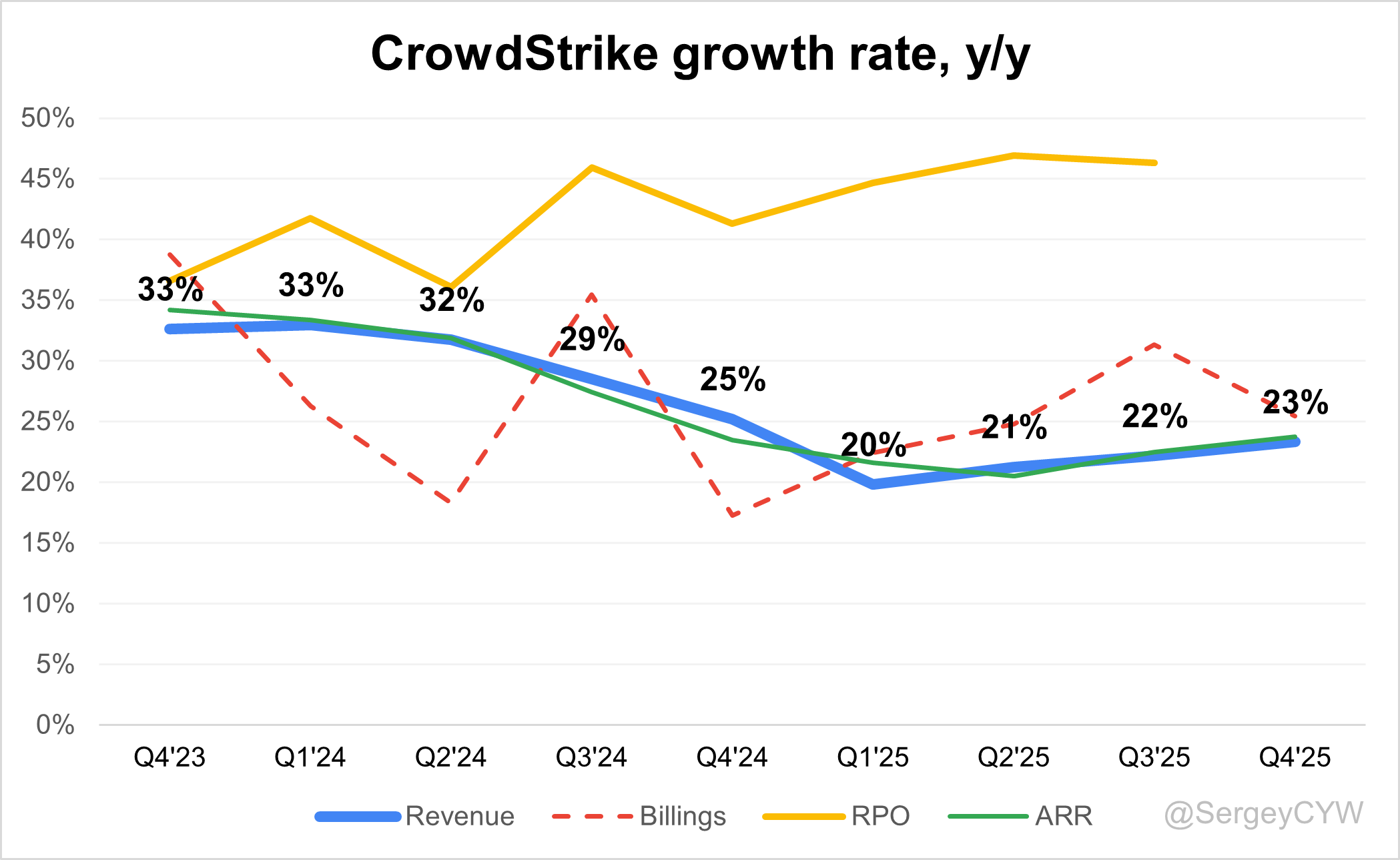

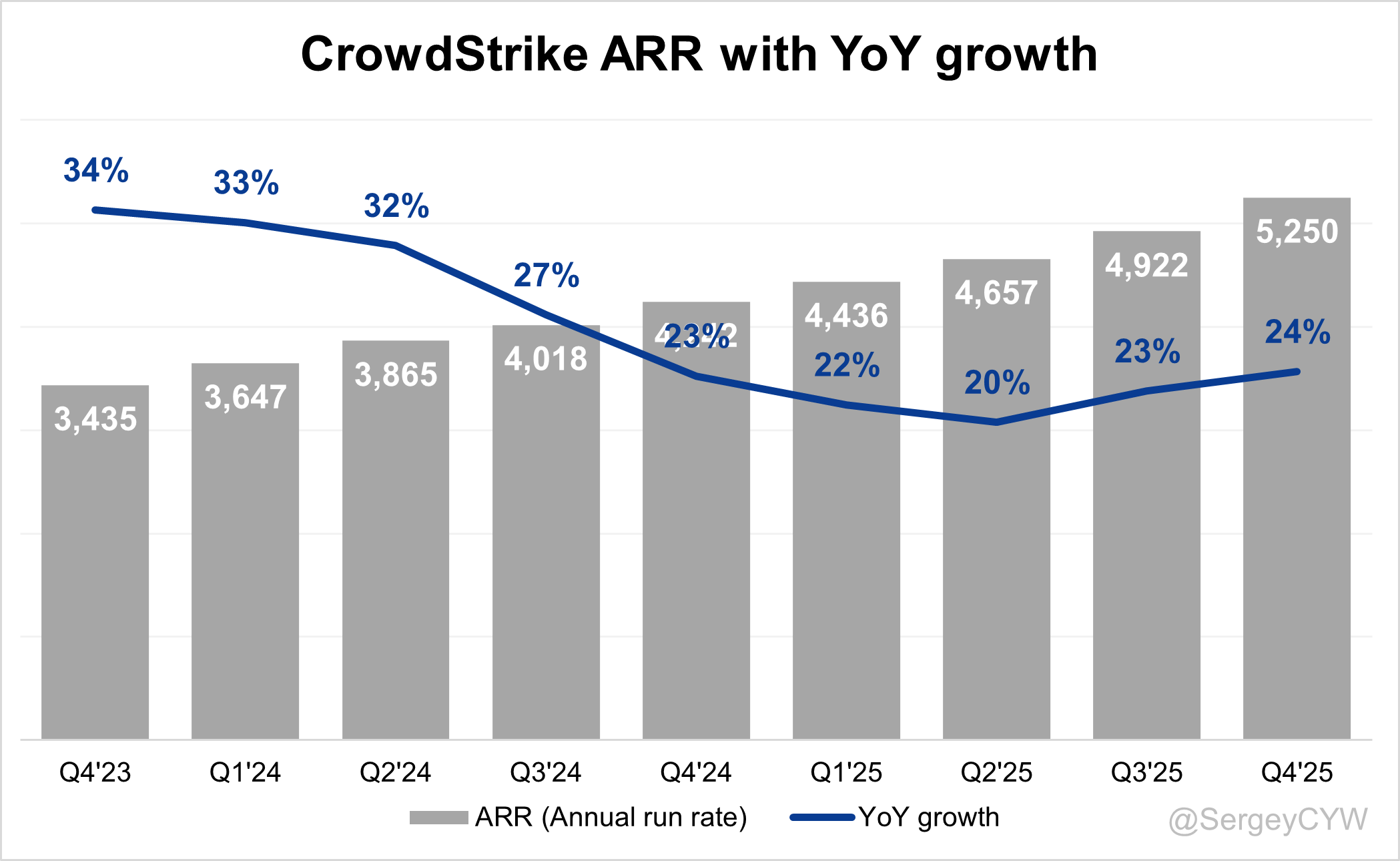

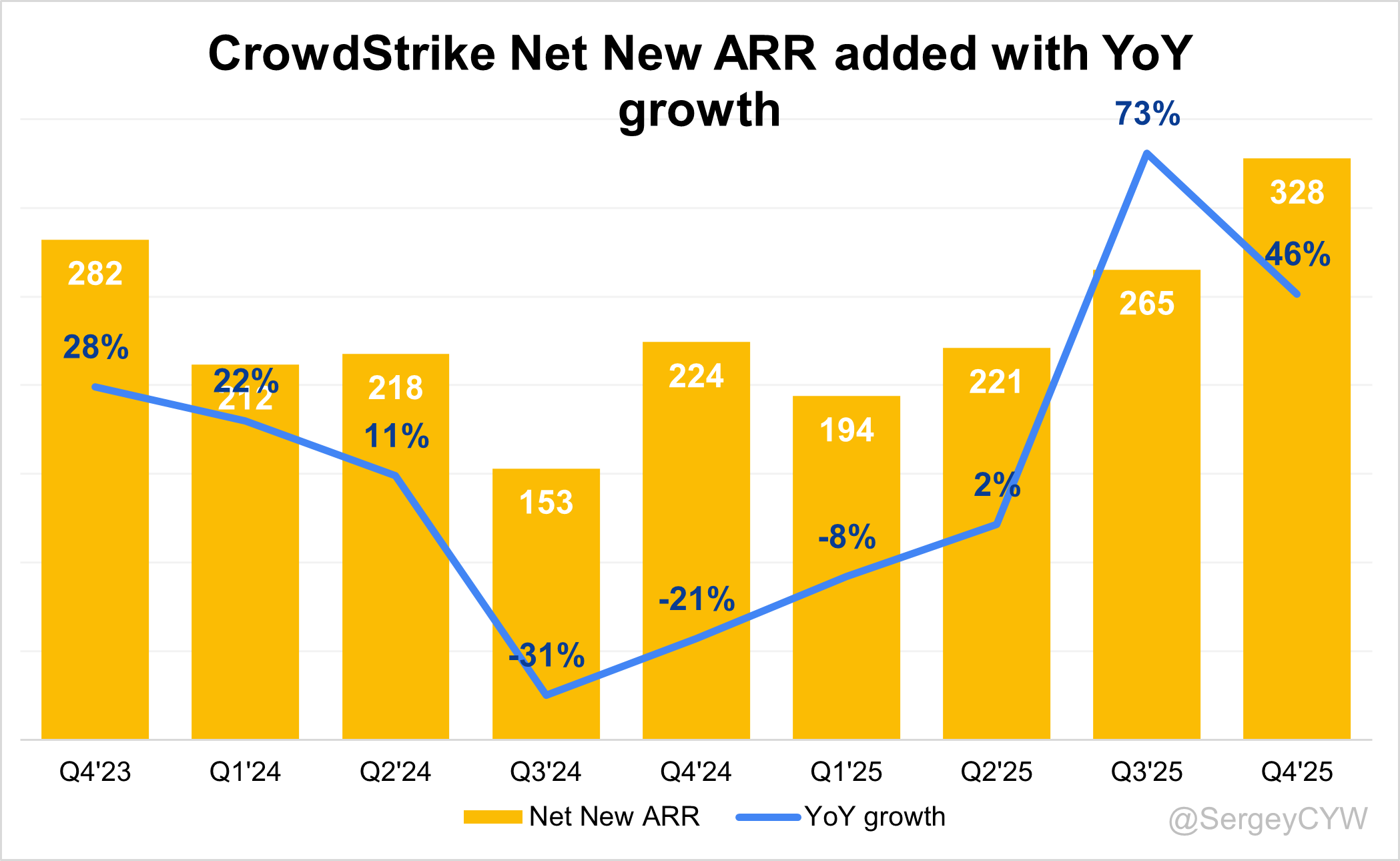

↗️ARR $5.25B (+23.8% YoY, +328 net new ARR)

↗️Billings $1,996M (+25.5% YoY)

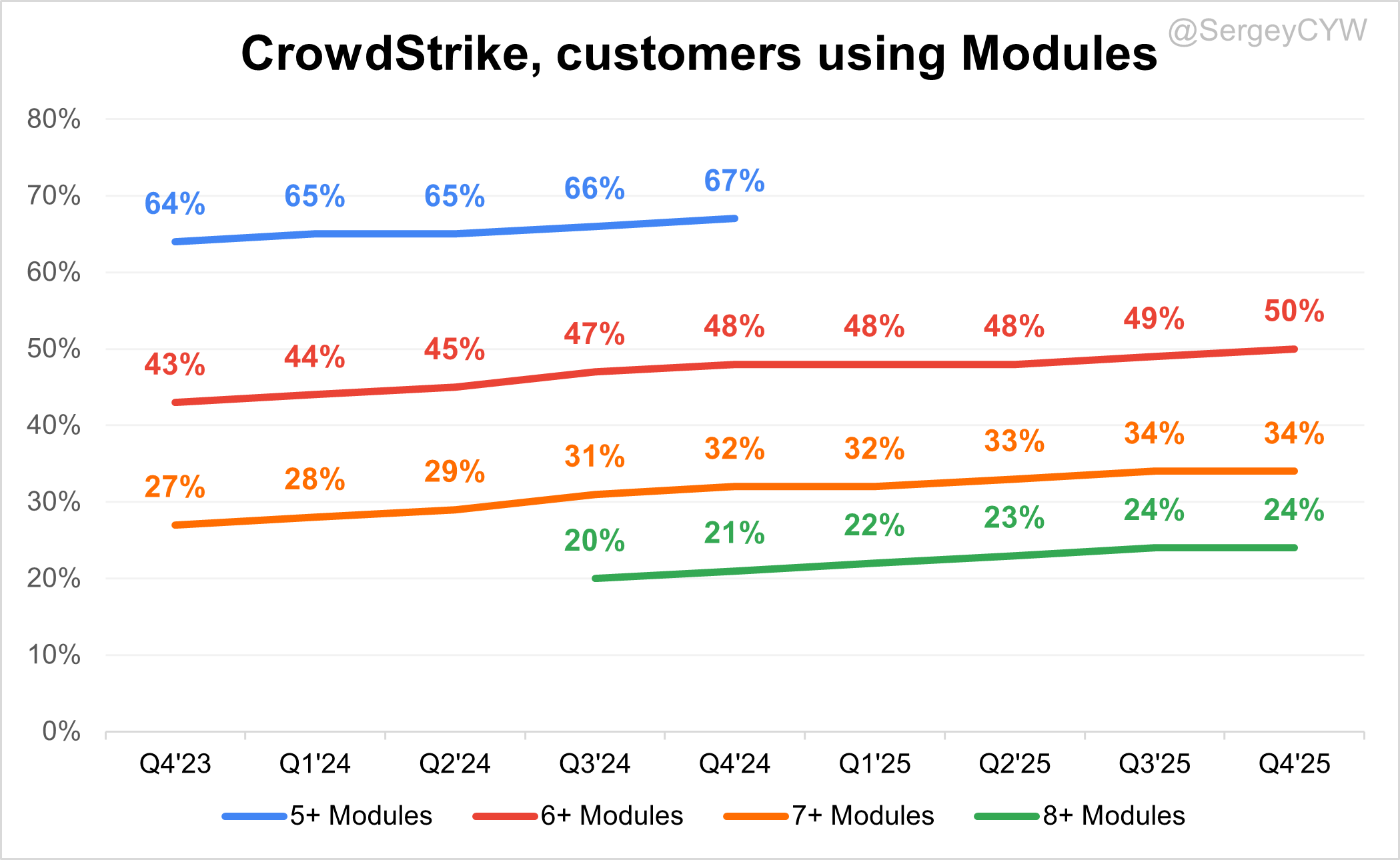

Customer Engagement with Multiple Modules

↗️% of customers using 6+ Modules (50%, 49% LQ)

➡️% of customers using 7+ Modules (34%, 34% LQ)

➡️% of customers using 8+ Modules (24%, 24% LQ)

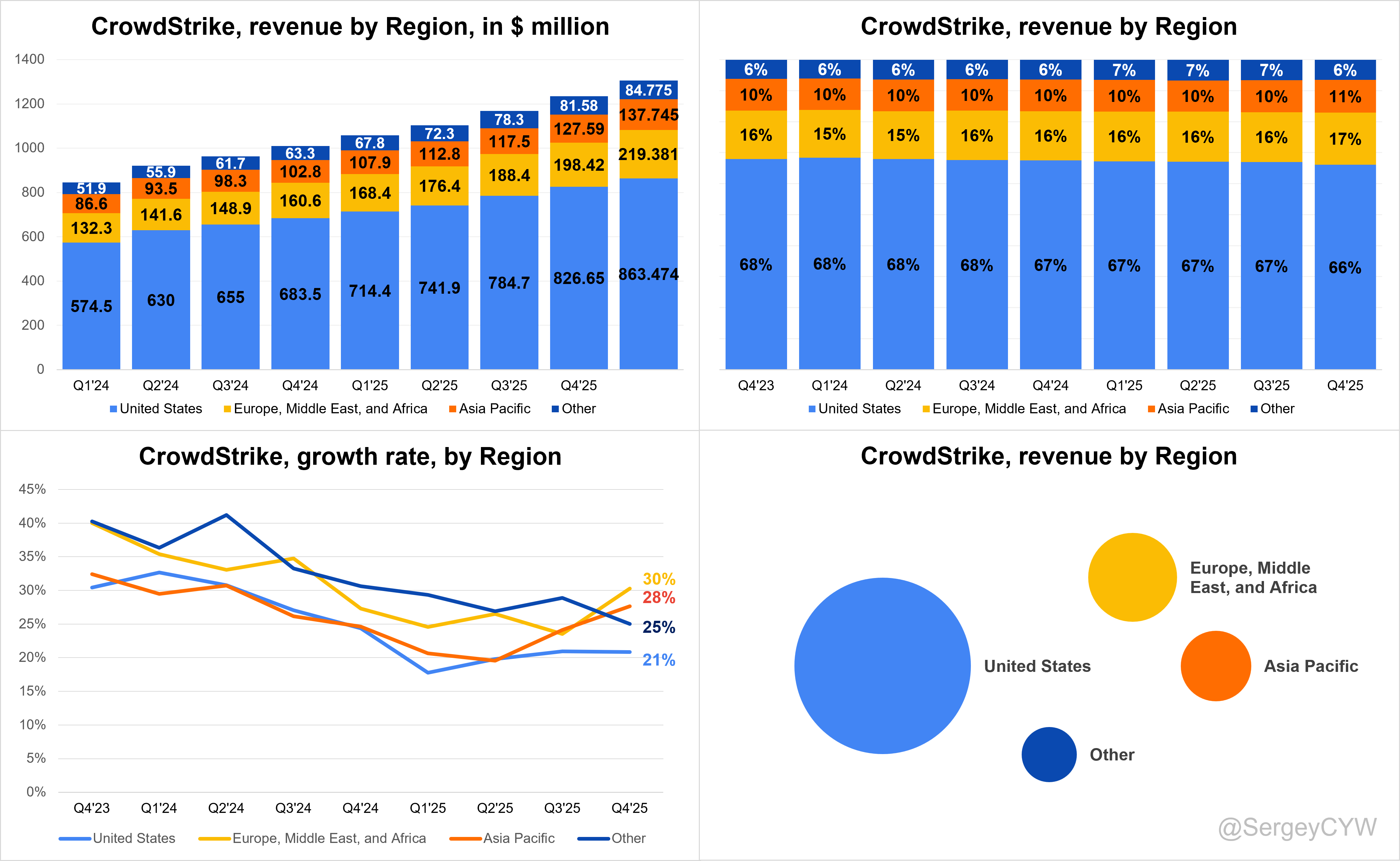

Regional Breakdown

↘️United States $863.5M rev (+20.9% YoY, 66% of Rev)

↗️Europe, Middle East, and Africa $219.4M rev (+30.3% YoY, 17% of Rev)

↗️Asia Pacific $137.7M rev (+27.7% YoY, 11% of Rev)

↗️Other $84.8M rev (+25.0% YoY, 6% of Rev)

Operating expenses

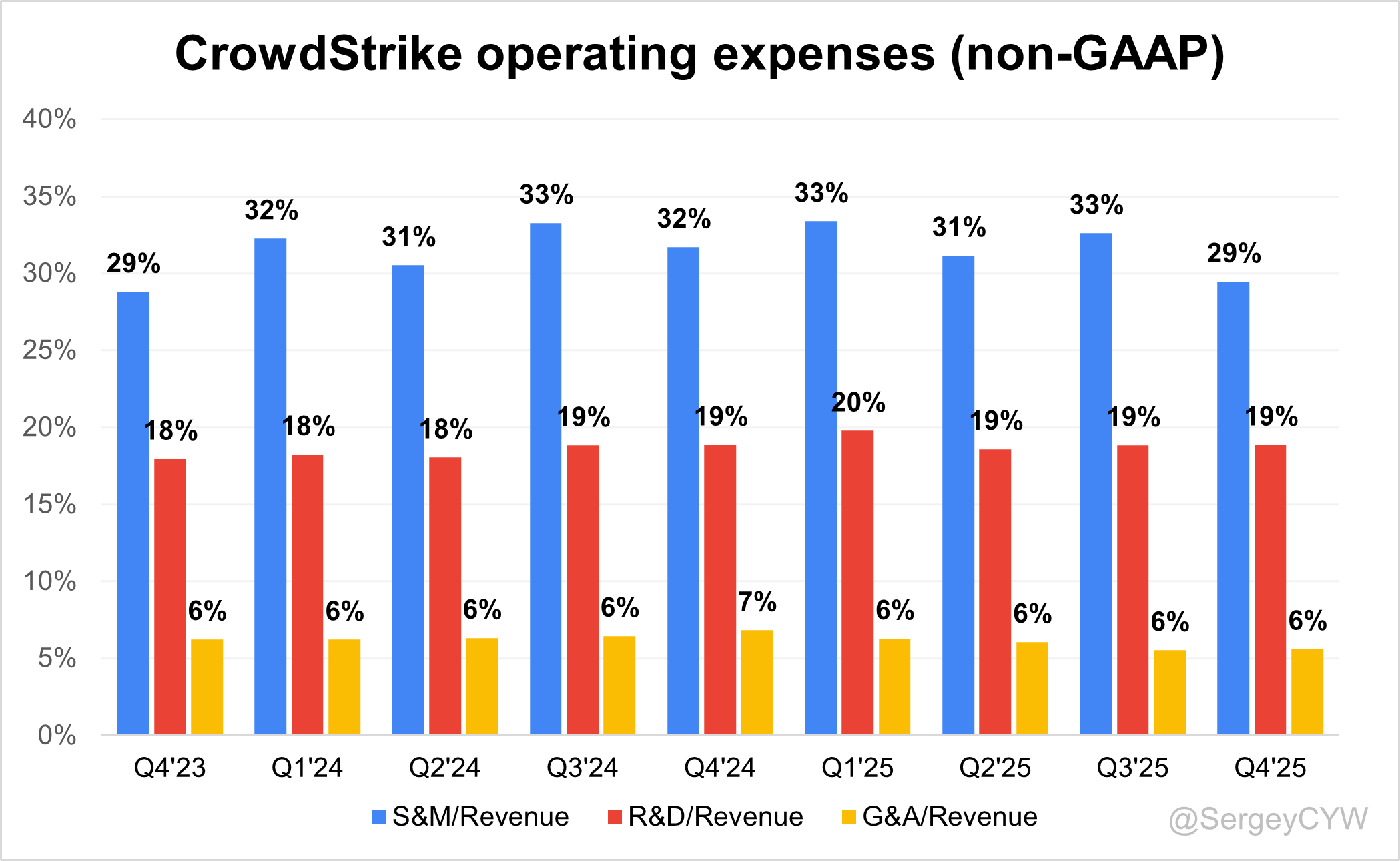

↘️S&M*/Revenue 29.5% (-2.2 PPs YoY)

↗️R&D*/Revenue 18.9% (+0.0 PPs YoY)

↘️G&A*/Revenue 5.6% (-1.2 PPs YoY)

Quarterly Performance Highlights

↗️Net New ARR $328M (+46.2% YoY)

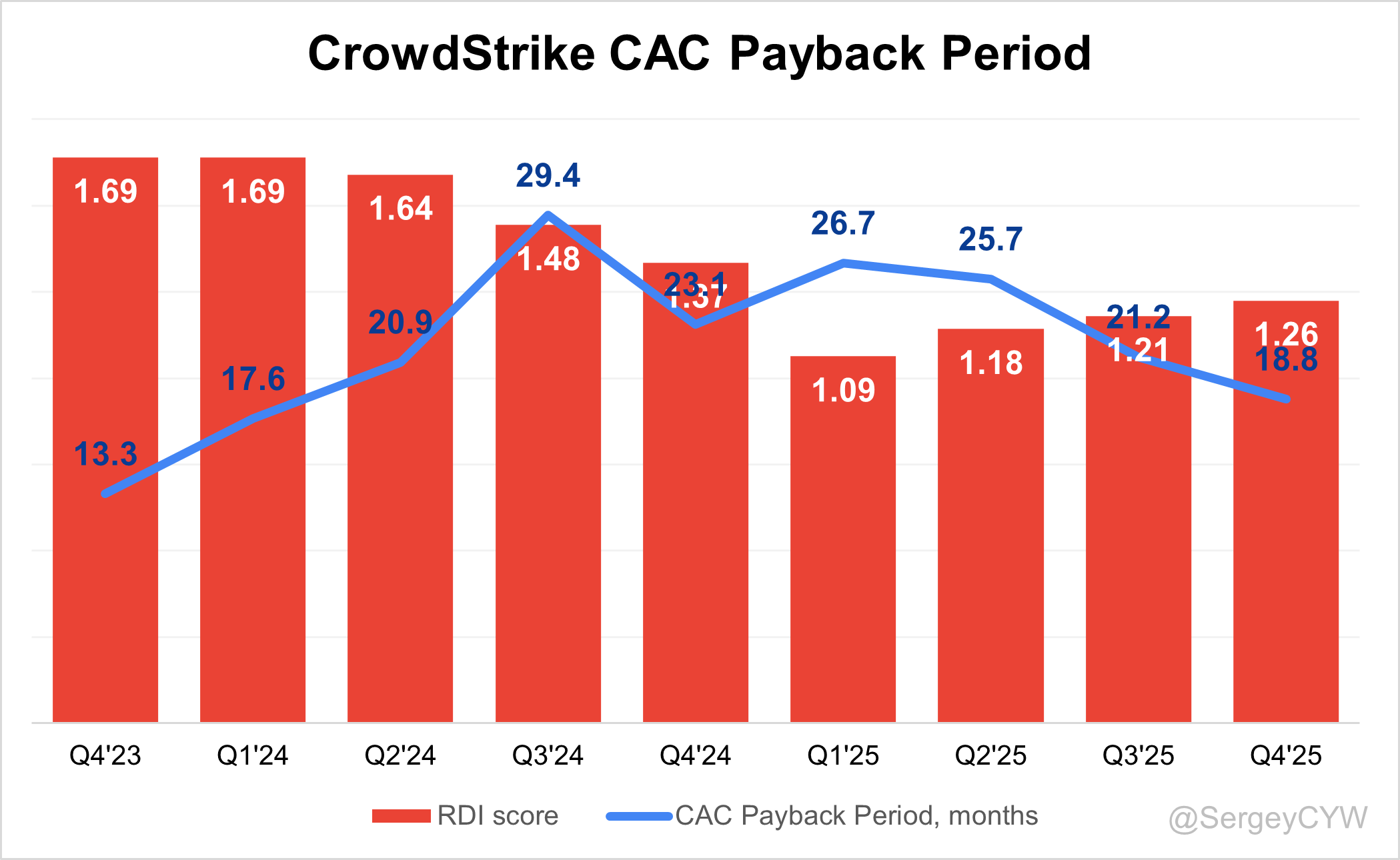

↘️CAC* Payback Period 18.8 Months (-4.3 YoY)🟢

↘️R&D* Index (RDI) 1.26 (-0.11 YoY)🟡

Dilution

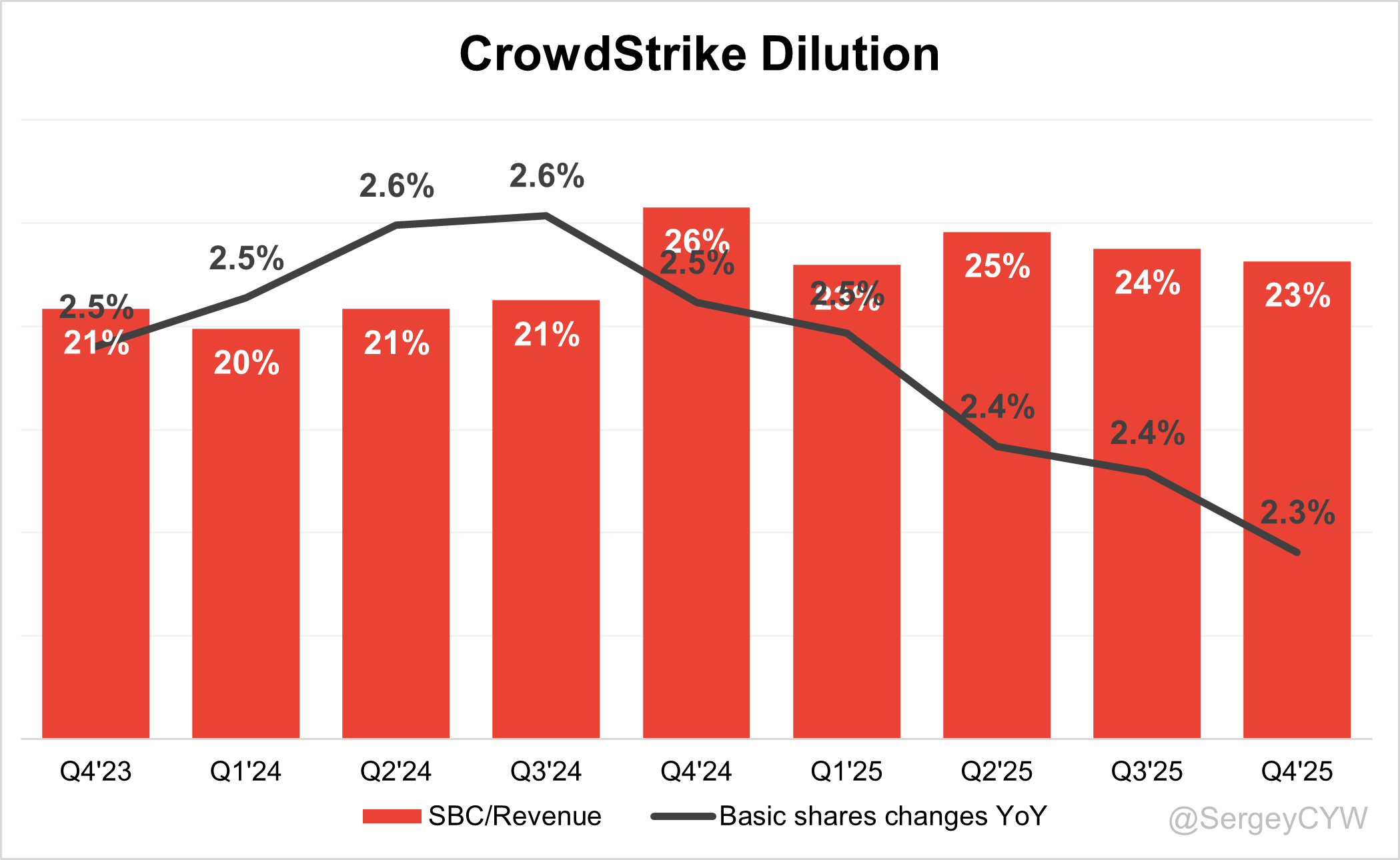

↘️SBC/rev 23%, -0.6 PPs QoQ

↘️Basic shares up 2.3% YoY, -0.1 PPs QoQ

↘️Diluted shares up 1.9% YoY, -0.4 PPs QoQ

Guidance

↗️Q1’26 $1,360.0 - $1,364.0M guide (+23.4% YoY) beat est by 0.6%

↗️$5,867.6 - $5,927.6M FY guide (+22.6% YoY) beat est by 0.8%

Key points from CrowdStrike’s Fourth Quarter 2025 Earnings Call:

Financial Performance

CrowdStrike delivered strong fiscal FY2026 results. Q4 net new ARR reached $331 million, growing 47% year over year and representing the company’s largest quarterly ARR expansion. Full-year net new ARR totaled $1.01 billion, increasing 25% and marking the first time annual additions exceeded $1 billion.

Ending ARR rose to $5.25 billion, a 24% increase, making CrowdStrike the first pure-play cybersecurity vendor to surpass the $5 billion ARR threshold. Q4 revenue reached $1.31 billion, growing 23%, including $1.24 billion in subscription revenue and $63.1 million in professional services revenue, which increased 26%.

Profitability improved alongside revenue. Q4 operating income reached $326 million, equal to 25% of revenue, marking the third consecutive quarterly record. Full-year operating income surpassed $1.05 billion, representing 22% of revenue.

Cash generation remained strong. Q4 free cash flow reached $376 million, or 29% of revenue, while full-year free cash flow totaled $1.24 billion, equal to 26% of revenue. Cash and equivalents ended the quarter at $5.23 billion, providing capital for acquisitions, platform investment, and share repurchases.

Burt Podbere, Chief Financial Officer

“The combination of growth, scale, profitability, and cash flow puts CrowdStrike in rare air.”

Falcon Platform

Falcon remains the company’s core platform, integrating endpoint protection, identity security, cloud security, data pipelines, and AI automation. Platform adoption continues to expand as enterprises consolidate cybersecurity tools.

Module usage increased significantly. By Q4 FY2026, 50% of customers used six or more modules, 34% used seven or more, and 24% used eight or more. Rising module adoption increases platform stickiness and customer lifetime value.

Falcon operates one of the largest security telemetry systems in the industry. Threat Graph processes over 1 trillion security events daily, correlating activity across approximately 2 trillion vertices and analyzing more than 15 petabytes of telemetry data.

Large-scale telemetry improves threat detection accuracy and strengthens AI models embedded across Falcon. Growing demand stems from expanding cyber threats, multi-cloud infrastructure, and enterprise AI adoption. Platform expansion also increases operational complexity as new modules and acquisitions must integrate seamlessly.

George Kurtz, Chief Executive Officer and Founder

“CrowdStrike is durable, mission-critical infrastructure for both securing AI and accelerating global AI adoption.”

George Kurtz, Chief Executive Officer and Founder

“Falcon is a vertically integrated net data creator and third-party data aggregator, generating real-time data from customer environments and world-class threat intelligence.”

Falcon Flex

Falcon Flex transformed CrowdStrike’s sales model by allowing customers to purchase platform access rather than individual modules. Organizations activate modules gradually as security requirements expand.

More than 1,600 customers adopted Falcon Flex by FY2026 year-end. Q4 alone added over 350 Flex customers, averaging nearly four per day. Flex accounts generated $1.69 billion in ARR, growing more than 120% year over year. Average Flex customers now generate over $1 million in ARR.

Flex expansion occurs through the Reflex model, where customers increase contract value after deploying additional modules. During FY2026, 380 Flex customers executed Reflex expansions, representing 23% of the Flex base, compared with 5% earlier in the year.

Reflex expansions typically occur within seven months and increase ARR by 26% on average. Nearly 100 customers completed multiple Reflex expansions, generating an additional 48% ARR uplift beyond the original contract.

One enterprise software company expanded from a single module and low six-figure spend to 25 Falcon modules and an $86 million contract value after adopting Flex. Forecasting module activation patterns remains a challenge, although high Reflex rates indicate strong platform usage.

George Kurtz, Chief Executive Officer and Founder

“Falcon Flex unlocks never-seen-before adoption for customers. Flex is now how we go to market.”

George Kurtz, Chief Executive Officer and Founder

“Flex is creating its own flywheel — demand drives use, use drives more demand.”

Falcon Cloud Security

Falcon Cloud Security expanded rapidly as enterprises strengthened cloud and AI infrastructure protection. ARR surpassed $800 million, growing more than 35% year over year and accelerating for a second consecutive quarter.

Platform capabilities include CSPM, CIEM, Cloud Detection and Response, and runtime threat protection. Runtime protection focuses on blocking attacks rather than only identifying configuration vulnerabilities.

A large enterprise data platform provider replaced its previous vendor after a detailed evaluation. Deployment occurred through a multi-year eight-figure Flex contract and reduced mean time to detect and respond by 90%.

Growing cloud complexity, multi-cloud adoption, and AI infrastructure deployment drive demand. Competition remains intense due to overlapping offerings from cybersecurity vendors and hyperscale cloud providers.

George Kurtz, Chief Executive Officer and Founder

“Our unique ability to operate in runtime at scale continues to set us apart from the rest of the market.”

George Kurtz, Chief Executive Officer and Founder

“Customers are realizing that identifying exposures alone is not enough — they need protection that stops the breach.”

Falcon Shield

Falcon Shield protects SaaS environments and application identities. Following the acquisition of Adaptive Shield, ARR increased more than 300% year over year and expanded over fivefold since integration.

SaaS applications represent a rapidly growing attack surface as organizations deploy collaboration tools, enterprise applications, and AI platforms. Falcon Shield provides visibility and policy enforcement across SaaS identities, permissions, and configurations.

Integration with Falcon identity security enables monitoring of both human users and machine identities. SaaS security requires continuous updates due to the expanding ecosystem of enterprise SaaS tools.

George Kurtz, Chief Executive Officer and Founder

“The browser has become the front door for AI applications, and protecting that surface is essential as enterprises adopt agentic workflows.”

Falcon Identity Protection

Identity security has become a major growth driver. Approximately 80% of modern breaches involve compromised credentials rather than malware.

Falcon Identity Protection generated more than $520 million in ARR, growing over 34% year over year. Demand comes from rising identity complexity across hybrid environments and regulatory compliance requirements.

Privileged Access Management emerged as a key driver, growing over 170% sequentially. PAM protects high-privilege accounts frequently targeted by attackers.

Acquisition of SGNL introduced Zero Standing Privilege, replacing static permissions with dynamic, context-based authorization. Dynamic access control reduces identity attack surfaces as enterprises deploy automation and AI agents.

A major department store chain replaced its previous identity vendor with CrowdStrike’s ITDR and PAM platform through a seven-figure Falcon Flex deployment.

George Kurtz, Chief Executive Officer and Founder

“Identity is one of the biggest threat vectors today. Nearly 80% of breaches are non-malware based and centered on identity compromise.”

George Kurtz, Chief Executive Officer and Founder

“Access should no longer be static — it should be always-on, granular, and dynamic.”

Charlotte AI

Charlotte AI functions as the platform’s AI security assistant, supporting investigation, automation, and incident response within security operations centers.

Charlotte usage increased more than sixfold year over year, while ARR related to Charlotte deployments more than tripled. Platform capabilities expanded beyond one AI assistant to include ten specialized AI agents performing tasks such as threat investigation, correlation, and remediation.

A leading enterprise cloud software company adopted Charlotte alongside Falcon Next-Gen SIEM in an eight-figure Reflex expansion. Initial deployment improved mean time to respond by three times within 30 days.

Competition in AI-driven security automation continues to increase. CrowdStrike differentiates Charlotte through integration with proprietary telemetry and threat intelligence.

George Kurtz, Chief Executive Officer and Founder

“Charlotte is our flagship agent and the foundation of an agentic SOC workforce.”

George Kurtz, Chief Executive Officer and Founder

“Using domain-specific AI trained on security data, Charlotte accelerates and democratizes security outcomes.”

Next-Generation SIEM

CrowdStrike’s Next-Gen SIEM business grew rapidly, reaching over $585 million in ARR with 75% year-over-year growth. Platform design replaces traditional SIEM systems that often suffer from high infrastructure costs and slow analytics.

Integration with the Falcon architecture enables unified analysis of telemetry from endpoints, cloud workloads, identities, and external data sources.

Introduction of Falcon Onum, a native data pipeline, simplified ingestion and analysis of security data across distributed environments.

A Fortune 500 retail company replaced its legacy SIEM platform through a seven-figure contract. Deployment delivered 80% faster query performance and enabled automated security workflows.

Competition remains strong from legacy SIEM vendors and new AI-driven analytics platforms. Platform integration and cost efficiency provide a key competitive advantage.

George Kurtz, Chief Executive Officer and Founder

“Next-Gen SIEM has proven itself a scaled market disruptor, delivering performance and cost advantages over legacy platforms.”

Product Innovations

CrowdStrike launched AI-DR (AI Detection and Response) to monitor enterprise AI usage and identify risks associated with AI models, prompts, and data exposure.

Adoption accelerated quickly. Demand increased more than fivefold quarter over quarter shortly after launch.

CrowdStrike sensors identified over 1,800 AI applications running on enterprise devices, representing approximately 160 million unique AI application instances across customer environments.

George Kurtz, Chief Executive Officer and Founder

“AI is driving elevated demand for the Falcon platform while also accelerating the sophistication of cyber adversaries.”

Data Advantage

CrowdStrike maintains a significant data advantage through Falcon telemetry. Threat Graph analyzes more than 1 trillion security events daily across roughly 2 trillion interconnected vertices.

Data originates from endpoint sensors, cloud workloads, identity systems, and incident response activities across 176 countries.

Large volumes of expert-labeled security data produced by analysts and threat hunters strengthen detection models and automation capabilities. Proprietary operational data provides an advantage not easily replicated by general AI models trained on public datasets.

George Kurtz, Chief Executive Officer and Founder

“Our data does not come from internet text — it comes from stopping real breaches in real time.”

Customers and Adoption

Customer retention remains among the strongest in enterprise software. Gross retention reached 97%, while dollar-based net retention reached 115%, indicating consistent expansion within existing accounts.

Organizations increasingly consolidate multiple security tools onto the Falcon platform. Consolidation reduces infrastructure complexity and lowers total cost of ownership while improving threat detection.

CrowdStrike’s Managed Security Service Provider ecosystem expanded significantly, growing from under $100 million ARR three years ago to over $1.3 billion. Key partners include Kroll, Pax8, and NinjaOne.

George Kurtz, Chief Executive Officer and Founder

“Customers are consolidating their security needs on Falcon because they want better outcomes at lower total cost of ownership.”

Partnerships

Strategic partnerships expanded across cloud providers and infrastructure vendors. CrowdStrike generated nearly $1.5 billion in contract value through the AWS Marketplace, representing almost 50% growth year over year.

Customers can now purchase Falcon through the Microsoft Azure Marketplace using existing cloud consumption commitments.

Technology partnerships include NVIDIA, AMD, Intel, Dell, HPE, and Supermicro, supporting security for AI infrastructure environments.

Consulting and integration firms such as EY, Accenture, Deloitte, Wipro, HCL, Infosys, and KPMG continue building cybersecurity practices around Falcon deployments and SIEM migrations.

George Kurtz, Chief Executive Officer and Founder

“We didn’t just have a great partner year — we built an ecosystem to win the next decade.”

Challenges

CrowdStrike operates in a highly competitive cybersecurity market that includes hyperscalers and emerging AI-driven security vendors.

Industry analysts raised concerns about potential commoditization of security analytics due to large language models. Management argues real-time threat prevention requires telemetry, sensors, and deterministic response systems rather than probabilistic AI outputs.

Rapid expansion of AI attack surfaces also increases system complexity. AI agents, automated workflows, and browser-based AI tools create additional vectors that security platforms must monitor.

George Kurtz, Chief Executive Officer and Founder

“In cybersecurity you cannot have hallucinations — prevention must be first-time final.”

Outlook

CrowdStrike expects continued growth in FY2027, supported by a record pipeline entering Q1 that increased 49% year over year.

Projected ARR ranges between $6.47 billion and $6.52 billion, representing 23–24% growth. Revenue guidance ranges from $5.87 billion to $5.93 billion, or 22–23% growth.

Operating income is expected to reach $1.42 billion to $1.46 billion. Free cash flow margins are projected to remain above 30%.

Management continues to target long-term ARR milestones of $10 billion and eventually $20 billion, supported by demand for AI security, cloud protection, identity security, and cybersecurity platform consolidation.

Burt Podbere, Chief Financial Officer

“Our record pipeline gives us strong conviction in our ability to deliver profitable growth.”

George Kurtz, Chief Executive Officer and Founder

“As AI adoption accelerates, every enterprise deploying AI will require an independent protection layer for visibility, compliance, and enforcement.”

Thoughts on CrowdStrike Earnings Report $CRWD:

🟢Positive

• Revenue reached $1.31B, growing 23.3% YoY, while EPS $1.12 exceeded estimates and operating margin expanded to 25% (+4.4 pps YoY), reflecting strong operating leverage.

• ARR increased to $5.25B (+23.8% YoY) with $328M net new ARR (+46% YoY), marking the company’s largest quarterly ARR addition.

• Free cash flow margin improved to 28.8% (+6.2 pps YoY) with full-year free cash flow of $1.24B, reinforcing strong cash generation.

• Subscription revenue reached $1.24B (+23.2% YoY) with subscription gross margin of 81.1%, supporting scalable profitability.

• Falcon Flex adoption accelerated, reaching 1,600+ customers and $1.69B ARR (+120% YoY), with expansions delivering 26% ARR uplift on average.

• Falcon Cloud Security ARR exceeded $800M (+35% YoY), supported by enterprise wins and strong demand for AI and multi-cloud protection.

• Next-Gen SIEM ARR surpassed $585M (+75% YoY), driven by platform consolidation and performance advantages.

• Charlotte AI adoption expanded rapidly, with usage up 6× YoY and multiple enterprise deployments accelerating SOC automation.

• Customer metrics remain strong with 97% gross retention and 115% net retention (up from 112% year ago), indicating continued expansion within the installed base.

• Ecosystem growth strengthened through $1.5B AWS marketplace contract value (+~50% YoY) and new Microsoft Azure marketplace integration.

🟡Neutral

• U.S. revenue growth slowed to 20.9% YoY, while international regions grew faster (EMEA +30.3%, APAC +27.7%), shifting geographic growth dynamics.

• Customer adoption of additional modules stabilized, with 50% using 6+ modules, 34% using 7+, and 24% using 8+.

• R&D intensity remained steady at 18.9% of revenue, reflecting continued product investment without major efficiency gains.

• Share dilution remained moderate with SBC at 23% of revenue and diluted shares increasing 1.9% YoY.

• Guidance implies continued strong growth, with FY revenue expected at $5.87B–$5.93B (+~22–23% YoY).

• Expanding AI attack surfaces and agent-based workflows increase security complexity and require continuous platform development.

🔴Negative

• Competitive pressure continues across cloud security, SIEM, and AI-driven security automation, particularly from hyperscalers and emerging AI vendors.

• Forecasting usage patterns under the Falcon Flex consumption model remains challenging due to variable module activation timing.

GitLab

Financial Results:

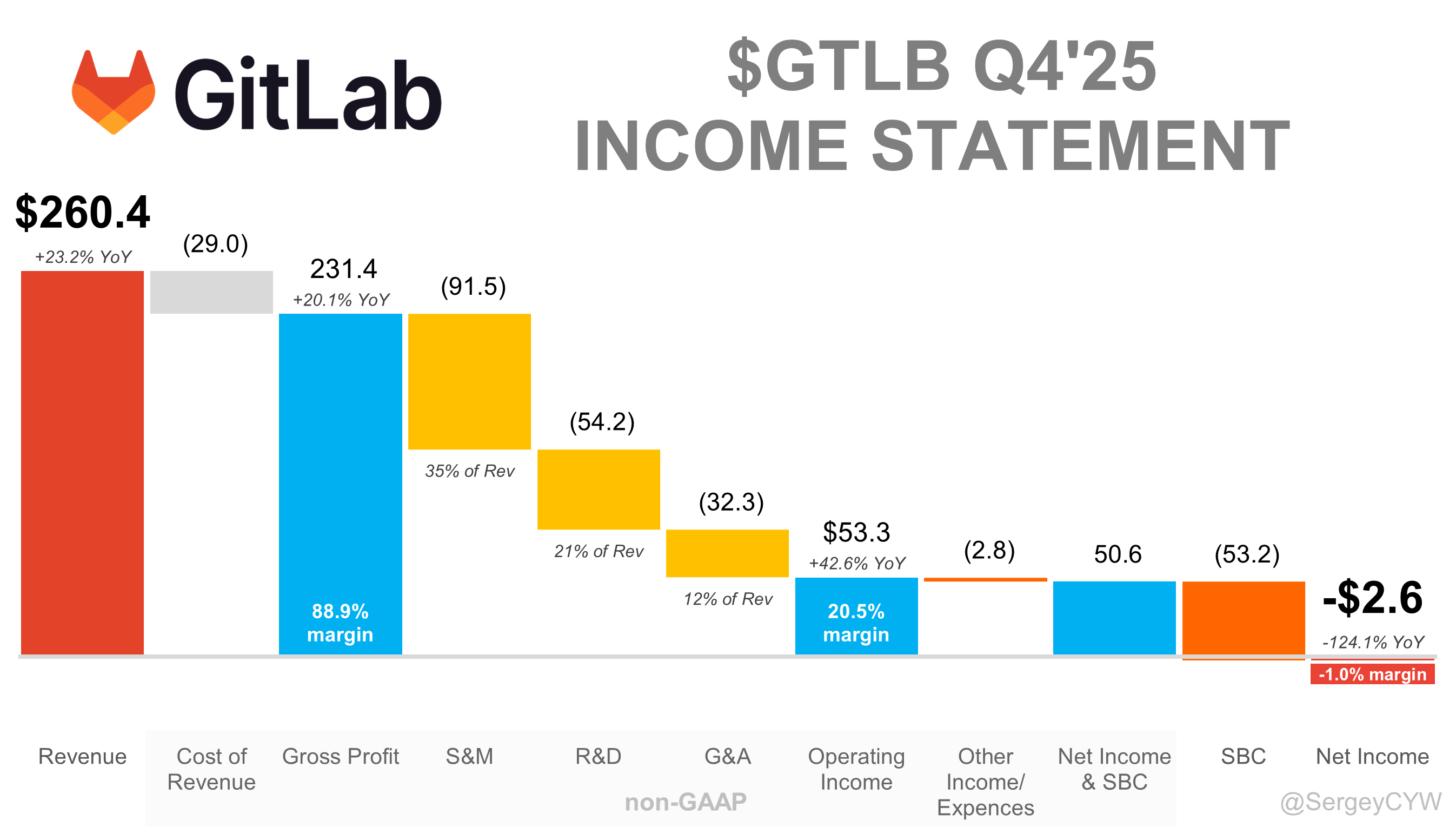

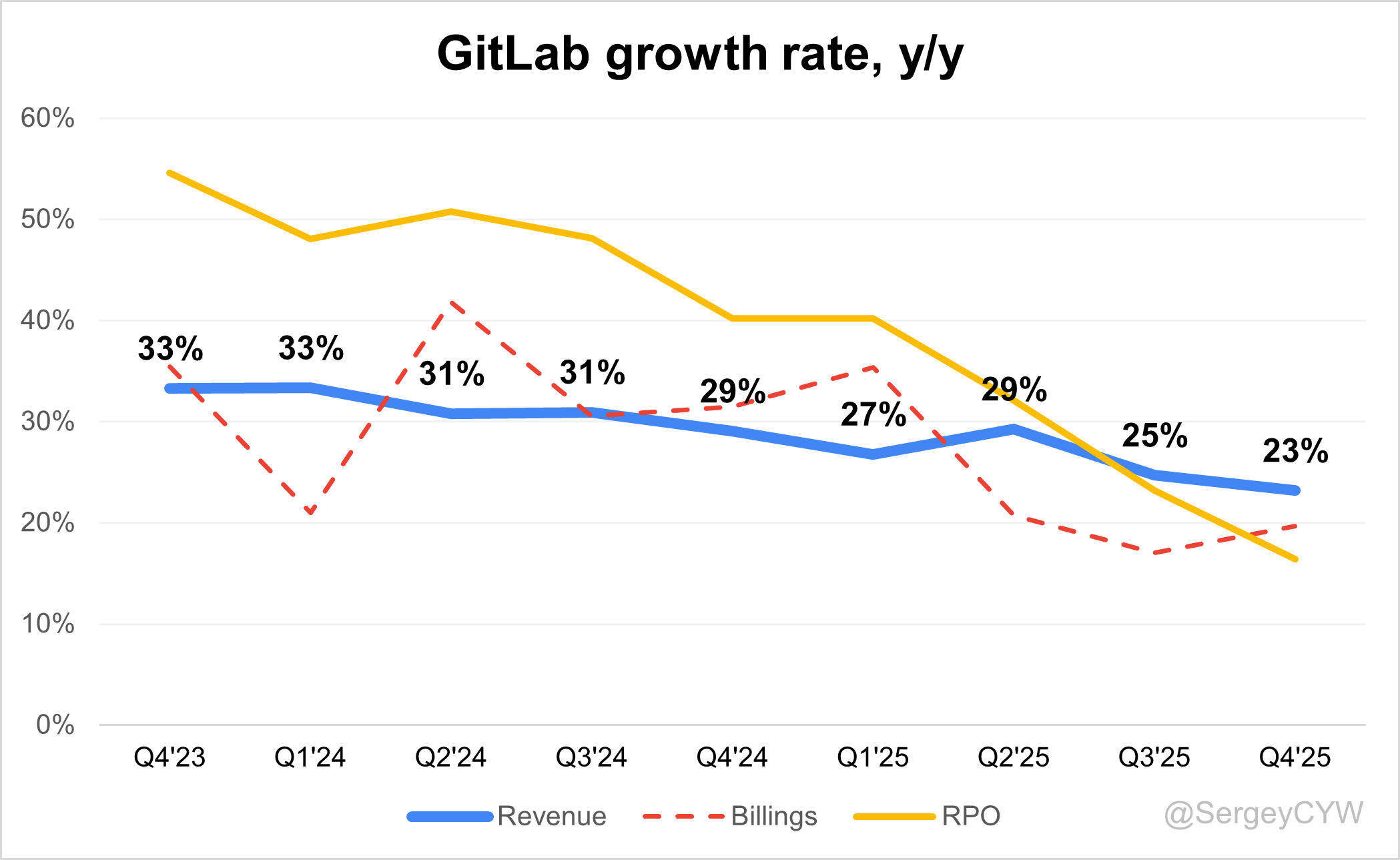

↗️$260.4M rev (+23.2% YoY, +6.5% QoQ) beat est by 3.5%

↘️GM* (88.9%, -2.3 PPs YoY)🟡

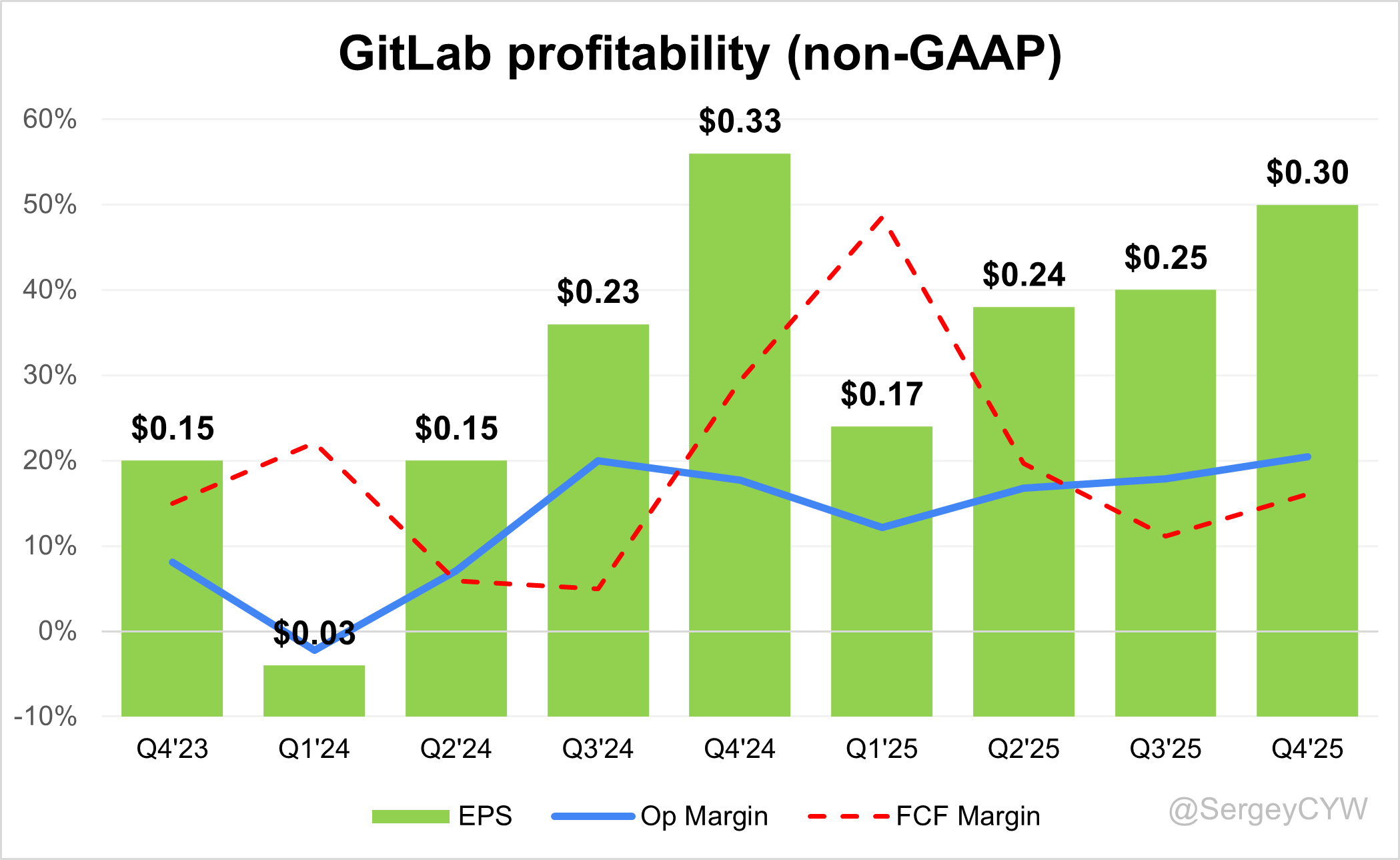

↗️Operating Margin* (20.5%, +2.8 PPs YoY)🟢

↘️FCF Margin (16.0%, -13.3 PPs YoY)🟡

↗️EPS* $0.30 beat est by 30.4%

*non-GAAP

Key Metrics

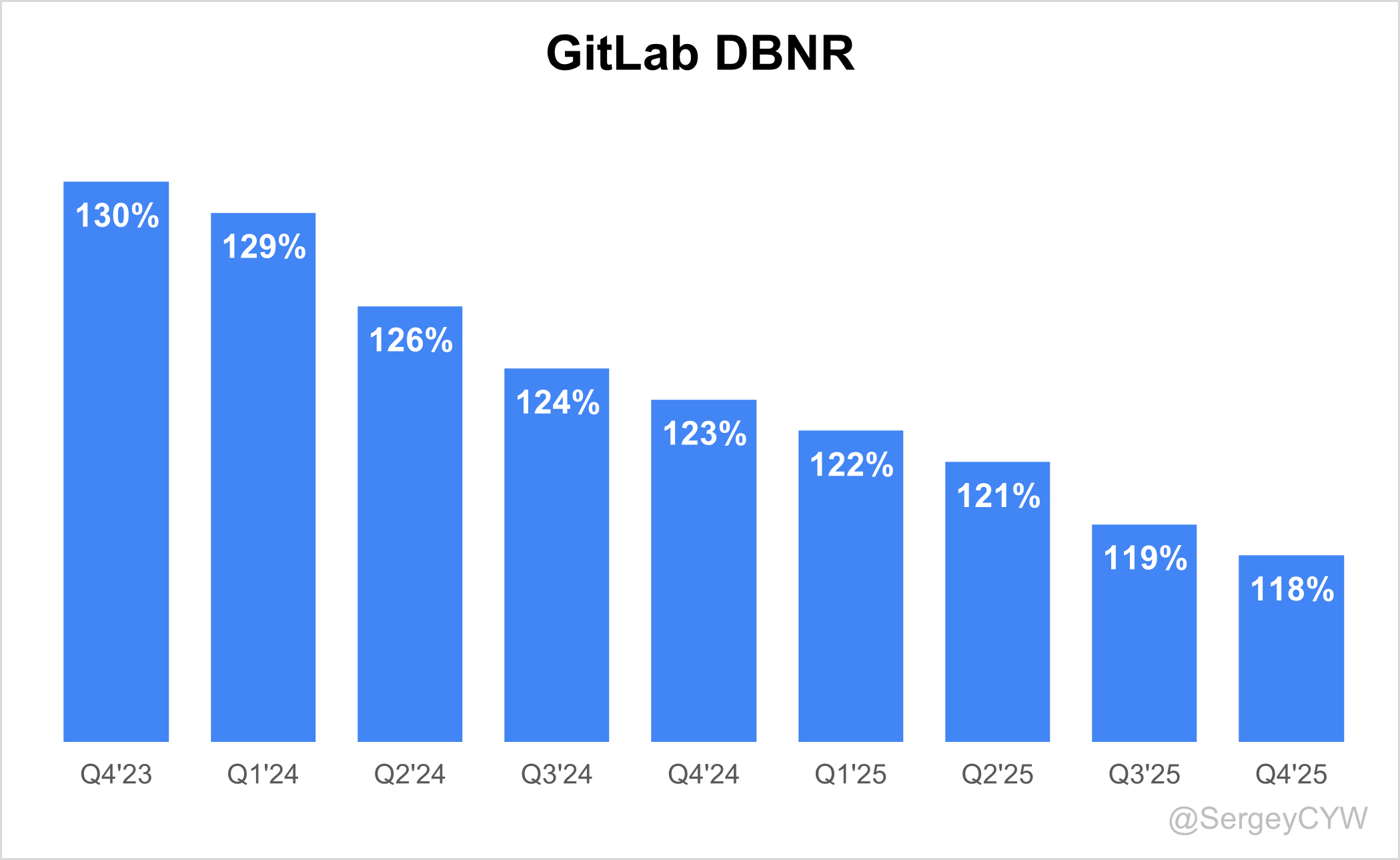

↘️DBNR 118% (119% LQ)

➡️RPO $1.10B (+16.4% YoY)🟡

➡️Billings $339M (+19.7% YoY)🟡

Customers

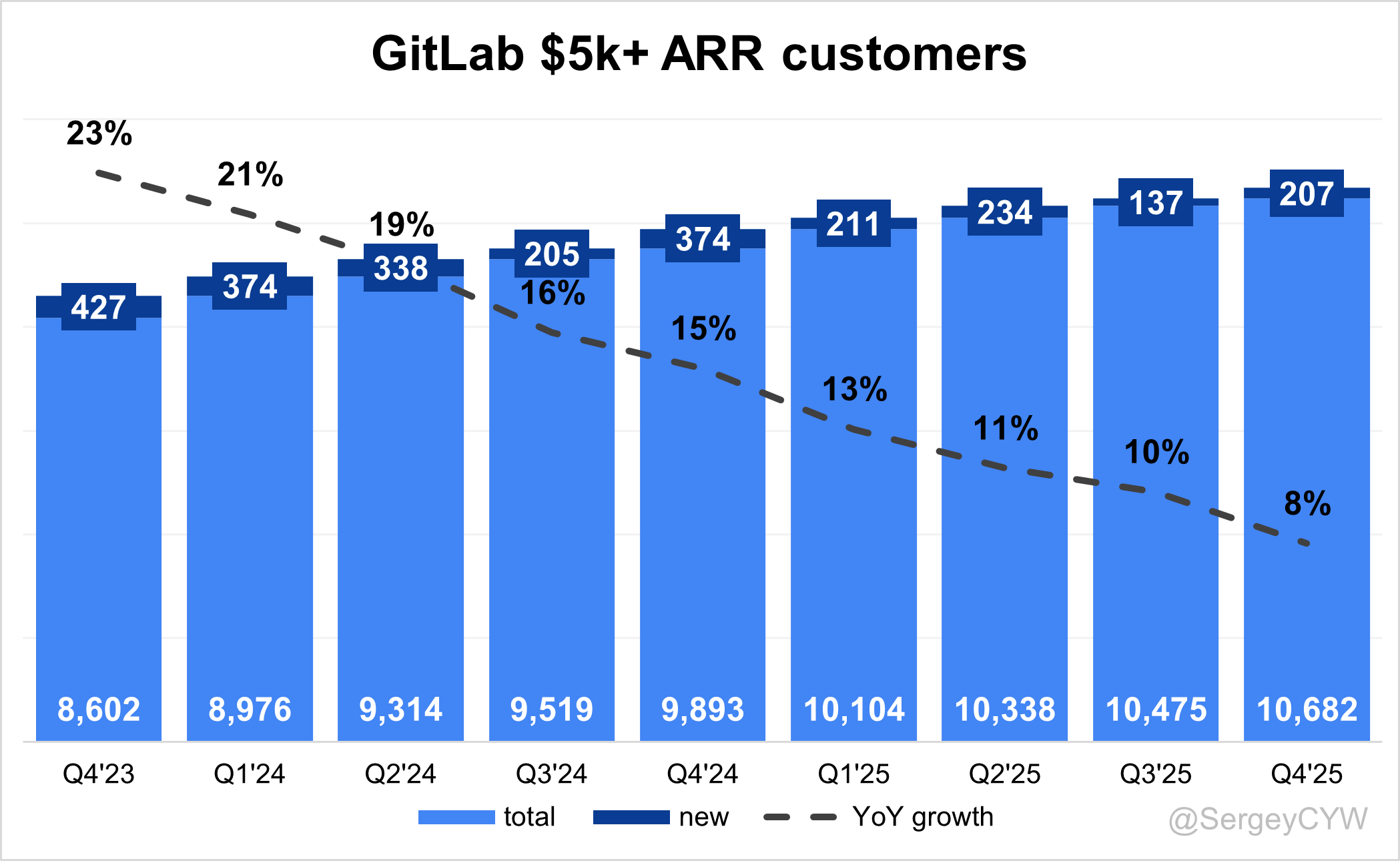

➡️10,682 customers (+8.0% YoY, +207)

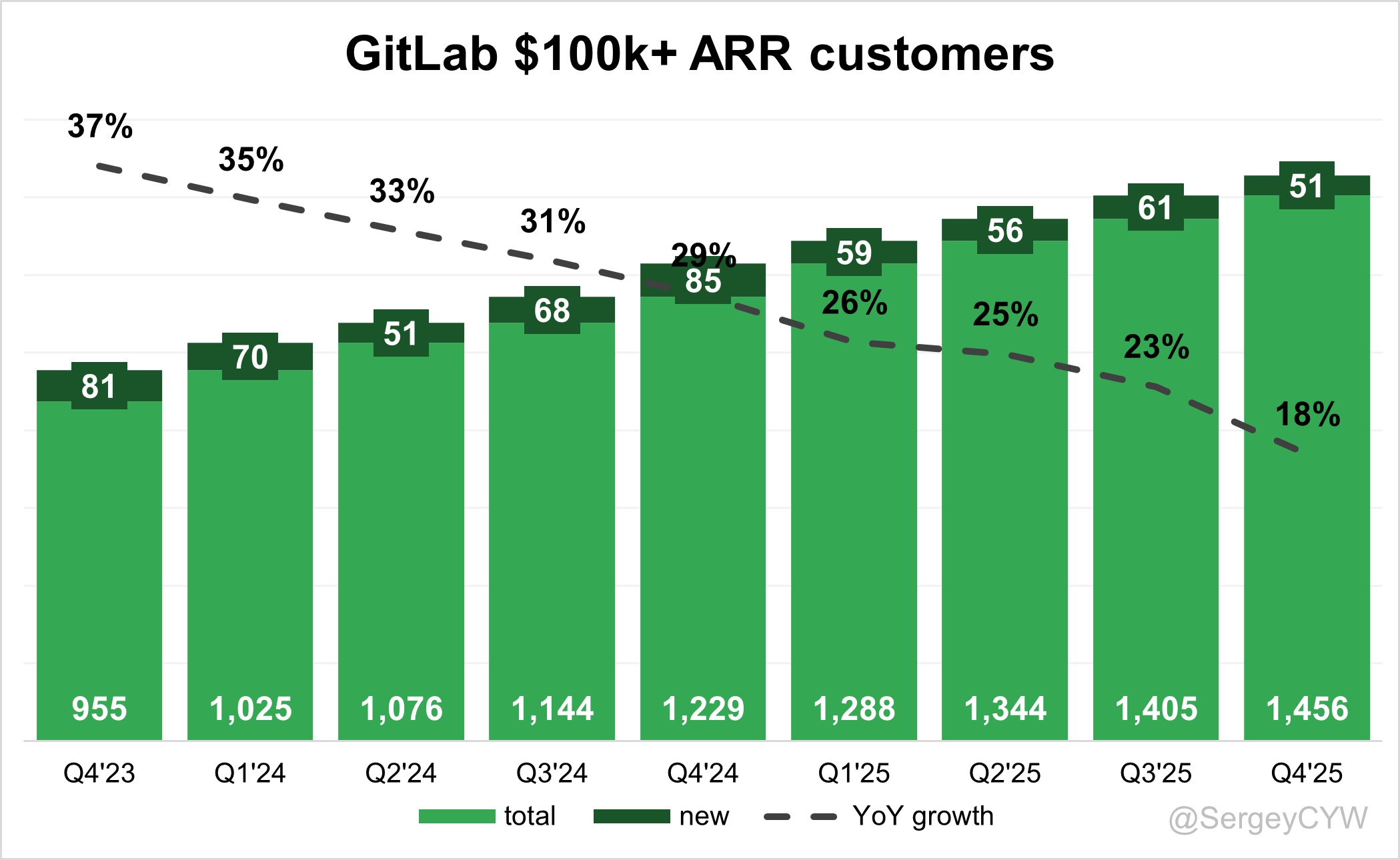

➡️1,456 $100k+ customers (+18.5% YoY, +51)

Operating expenses

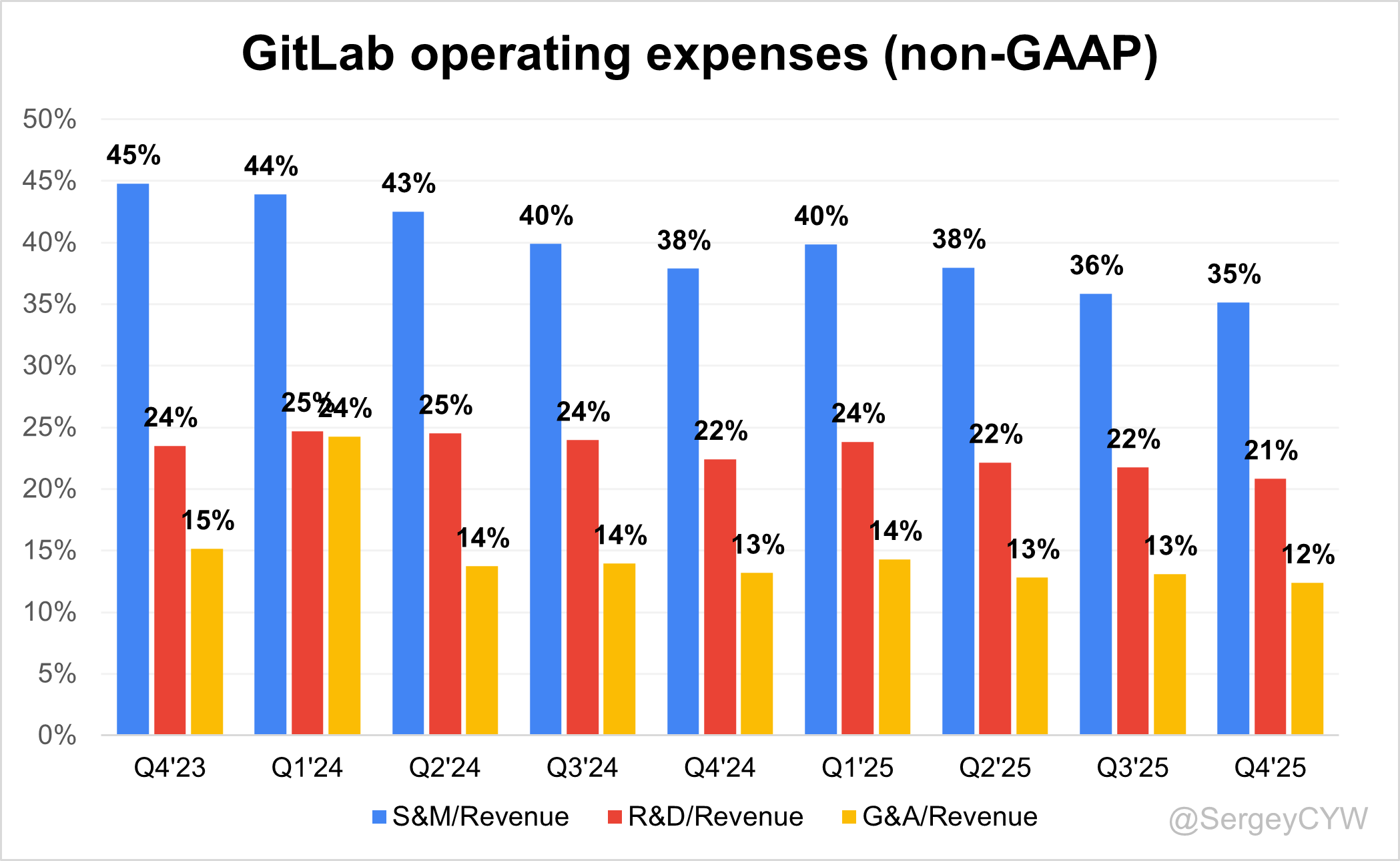

↘️S&M*/Revenue 35.1% (-2.7 PPs YoY)

↘️R&D*/Revenue 20.8% (-1.6 PPs YoY)

↘️G&A*/Revenue 12.4% (-0.8 PPs YoY)

Quarterly Performance Highlights

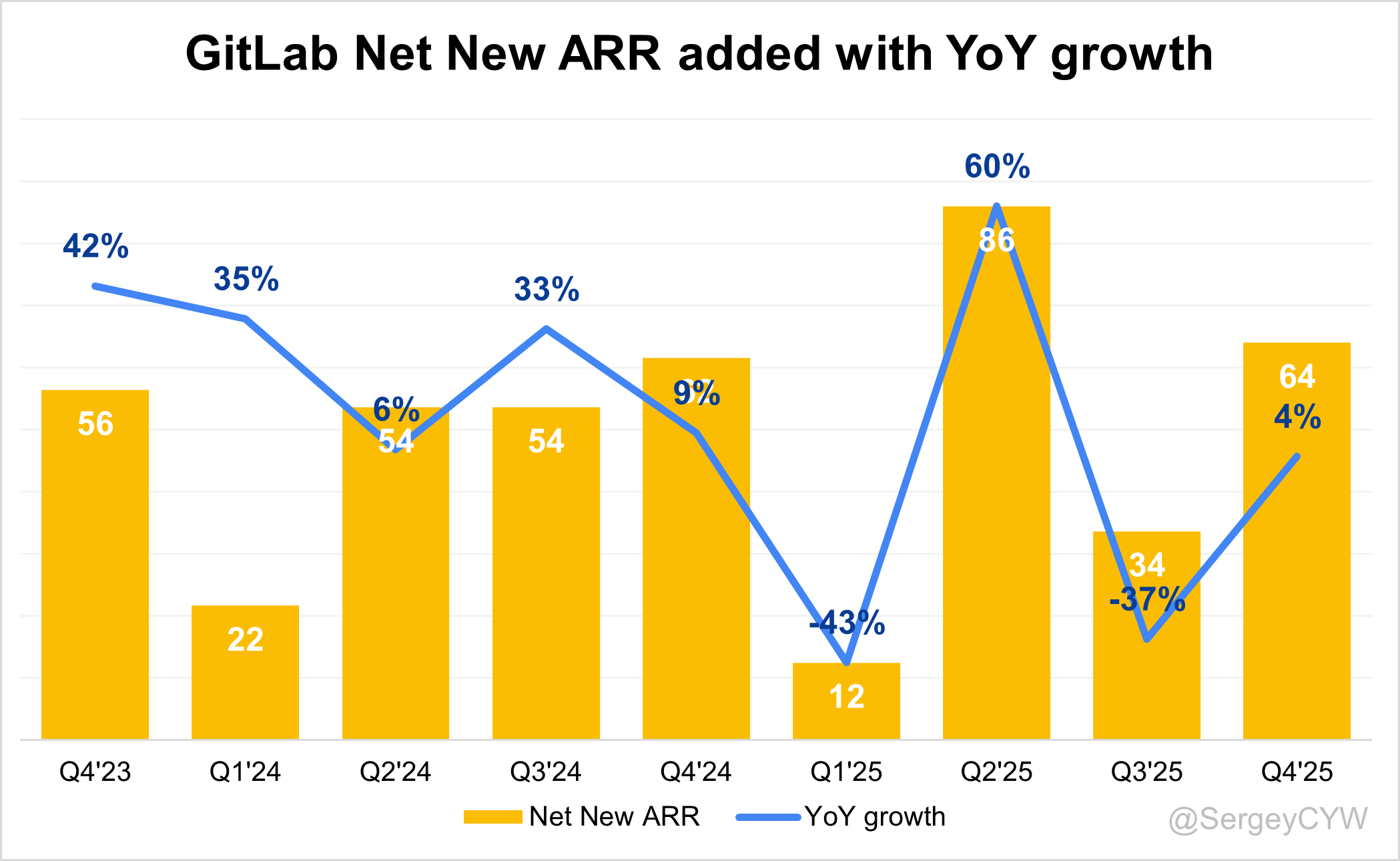

↗️Net New ARR $64M (+3.9% YoY)

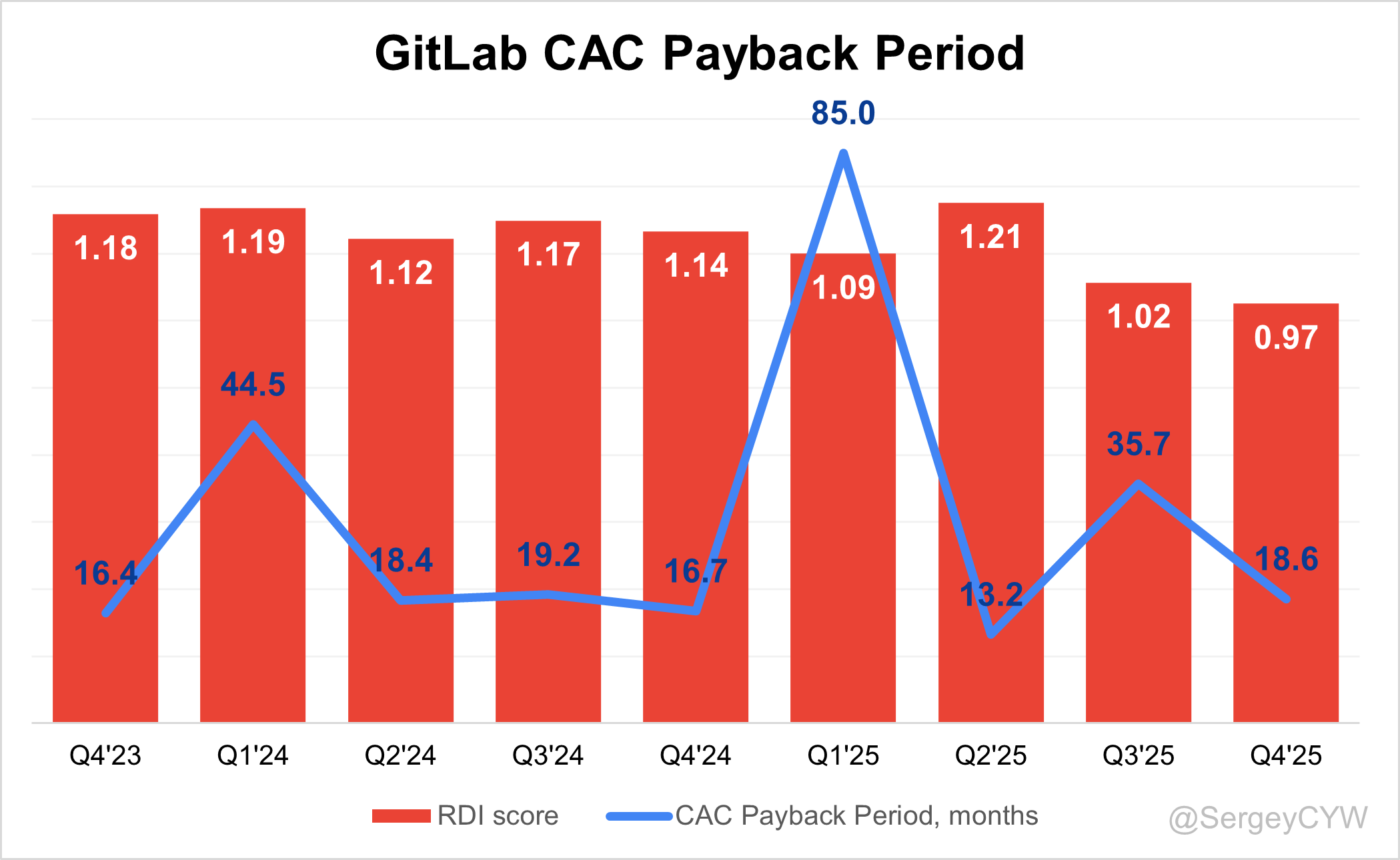

↗️CAC* Payback Period 18.6 Months (+1.8 YoY)🟡

↘️R&D* Index (RDI) 0.97 (-0.17 YoY)🟡

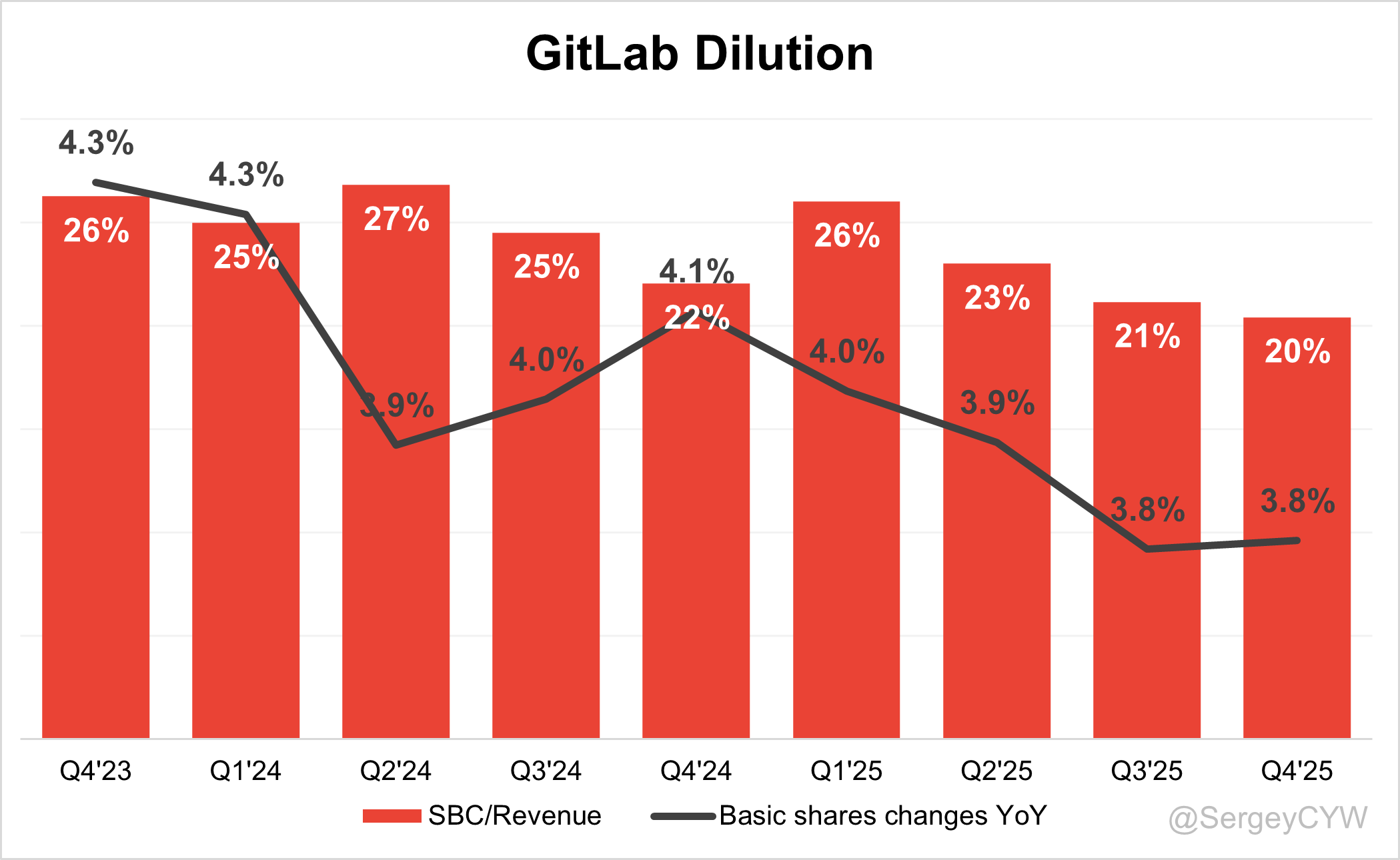

Dilution

↘️SBC/rev 20%, -0.7 PPs QoQ

↗️Basic shares up 3.8% YoY, +0.0 PPs QoQ

↘️Diluted shares down -0.5% YoY, -0.5 PPs QoQ🟢

Guidance

↘️Q1’26$253.0 - $255.0M guide (+18.4% YoY) missed est by -0.8%🔴

↘️$1,099.0 - $1,118.0M FY guide (+16.0% YoY) missed est by -1.2%🔴

Key points from GitLab’s Fourth Quarter 2025 Earnings Call:

Financial Performance

GitLab closed fiscal 2026 with strong financial results and crossed a major milestone as annual recurring revenue exceeded $1 billion. Total revenue reached $955 million, representing 26% year-over-year growth. Profitability improved significantly. Non-GAAP operating margin rose to 17%, expanding about 680 basis points from the prior year. Free cash flow increased to $220 million, up 83% year over year, with more than 7 percentage points of margin expansion.

Fourth-quarter results exceeded guidance. Revenue totaled $260 million, growing 23% year over year and beating expectations by roughly 3.5 percentage points. Non-GAAP operating margin reached 20.5%, approximately 5 percentage points above guidance. Around $3 million of the revenue beat came from non-recurring factors, including favorable foreign exchange and JiHu performance.

Customer expansion supported revenue growth. GitLab reported 10,682 customers with at least $5,000 ARR, representing over 95% of total ARR. Enterprise demand remained the main growth driver. Customers generating more than $100,000 ARR increased 18% to 1,456 accounts, representing over 75% of ARR. High-value customers also expanded rapidly, with more than 155 accounts exceeding $1 million ARR, up 26% year over year.

Retention remained strong. Dollar-based net retention reached 118%, while gross retention stayed above 90%. Remaining performance obligations totaled $1.1 billion, growing 20% year over year. Current RPO increased 24% to $719 million.

Jessica Ross, Chief Financial Officer

“FY2026 and Q4 delivered the highest net new ARR year and quarter ever. Because our model is ratable, revenue today reflects bookings decisions made several years ago.”

DevSecOps Platform

GitLab’s DevSecOps platform remains the company’s core growth engine. The platform integrates source code management, CI/CD pipelines, security testing, compliance enforcement, and deployment automation into a single environment. Enterprises adopt the platform to consolidate fragmented development tools and simplify engineering operations.

Enterprise customers continue expanding platform usage after initial adoption. Deployment usually begins with repository management and expands to CI/CD, security, and governance workflows as engineering teams scale.

Growth data reflects enterprise demand. GitLab ended the year with 10,682 customers generating more than $5,000 ARR. The number of customers generating over $100,000 ARR rose to 1,456, while customers exceeding $1 million ARR surpassed 155. Expansion among large organizations remains consistent with gross retention above 90% and net retention at 118%.

AI-driven development increases platform relevance. Coding assistants generate software, but organizations still require infrastructure for version control, testing pipelines, compliance monitoring, and deployment governance.

Lower-end segments show weaker demand. Around 20% of ARR comes from price-sensitive customers, including SMB and mid-market organizations facing tighter technology budgets. Public sector demand also fluctuated and represents roughly 12% of ARR.

Bill Staples, Chief Executive Officer

“GitLab sits at the heart of how enterprises build and deliver software. As AI accelerates development, security, compliance, and governance become even more critical.”

Bill Staples, Chief Executive Officer

“When every developer has access to the same models, code generation becomes a commodity, and the bottleneck shifts to everything after the code—reviews, pipelines, security, and deployment.”

Duo Agent Platform

GitLab introduced the Duo Agent Platform, a major product innovation that embeds artificial intelligence directly into software workflows. The system enables AI agents to automate operational development tasks while operating within GitLab’s governance framework.

Architecture supports collaboration between developers and AI agents. Workflow orchestration coordinates tasks, contextual data provides lifecycle visibility, and guardrails enforce security and compliance policies.

Early enterprise deployments show meaningful productivity gains. One airline with a 3,000-person engineering organization deployed the platform to automate dependency updates, vulnerability remediation, and cloud migration. Roughly 90% of component updates now run autonomously, reducing routine engineering work.

An insurance company used the platform during an internal AI innovation program. The initiative improved compliance monitoring, developer onboarding efficiency, and modernization of legacy systems.

Revenue impact will emerge gradually. GitLab launched the platform shortly before the earnings call. Around 70% of revenue comes from self-managed deployments, which require internal upgrades before enabling new features. Historically, about two quarters are required for half of customers to upgrade.

Bill Staples, Chief Executive Officer

“We launched GitLab Duo Agent Platform to reposition GitLab for the AI era, enabling organizations to deploy AI agents across the full software lifecycle.”

Bill Staples, Chief Executive Officer

“Before AI, our platform reduced friction for developers. Now it reduces friction for both agents and the humans managing them.”

GitLab Ultimate

GitLab Ultimate represents the company’s primary enterprise offering. The tier includes advanced security scanning, governance tools, compliance controls, and software supply chain protection.

Ultimate adoption continues to grow and now accounts for 56% of total ARR. Large enterprise contracts increasingly include the offering. During the fourth quarter, 9 of the 10 largest deals involved GitLab Ultimate.

Security usage within the platform expanded rapidly. Projects running security scanning increased more than 60% year over year, while security projects per seat rose nearly 30%. Growth reflects enterprise demand for integrated security within development pipelines.

Large customers continue expanding platform usage over time. The global employment platform Indeed upgraded to Ultimate to deploy security and compliance capabilities across thousands of developers. Pipeline activity increased 80% while infrastructure costs declined.

Premium-tier adoption slowed in smaller organizations. A 50% price increase in Premium introduced several years earlier created price sensitivity among smaller customers.

Bill Staples, Chief Executive Officer

“Ultimate is now 56% of ARR and accounted for nine of the ten largest deals this quarter.”

GitLab Dedicated

GitLab Dedicated provides a managed single-tenant deployment for large enterprises requiring strict compliance and security controls. The offering allows companies to run GitLab within isolated cloud infrastructure while maintaining regulatory requirements.

Demand for managed infrastructure continues to grow. SaaS revenue, which includes GitLab Dedicated deployments, represents about 32% of total revenue and increased 38% year over year.

Enterprises increasingly adopt the model as part of broader digital transformation strategies. Indeed expanded its relationship with GitLab by moving to GitLab Dedicated to support thousands of developers and modernize internal infrastructure.

Another major contract came from a semiconductor manufacturer involved in the global AI supply chain. The company selected GitLab Premium and GitLab Duo Enterprise for more than 5,000 users after evaluating competing development platforms.

Infrastructure expansion carries financial implications. GitLab expects gross margin to decline from 89% in FY2026 to roughly 85–87% in FY2027 due to higher operating costs associated with SaaS infrastructure and AI workloads.

Bill Staples, Chief Executive Officer

“Enterprises increasingly want a platform that supports large-scale development with strong governance, and GitLab Dedicated delivers that in a managed environment.”

Product Innovation

GitLab maintains a rapid innovation cycle. The company has delivered 172 consecutive monthly product releases, reflecting continuous development of the platform.

Several new monetization features are planned for FY2027. Upcoming capabilities include artifact management, software supply chain security, and integrated secrets management. The features will be introduced as optional add-ons rather than full platform upgrades.

Revenue contribution during FY2027 is expected to be limited. Management expects meaningful monetization beginning in FY2028 as enterprise adoption increases.

Bill Staples, Chief Executive Officer

“Customers consistently tell us they want more ways to unlock incremental value, which is why we are introducing new monetization capabilities each quarter.”

AI Consumption Pricing

The Duo platform introduces a hybrid pricing structure combining subscription licensing with consumption-based billing. Customers receive bundled AI credits as part of existing subscriptions.

Premium subscriptions include roughly $12 in AI credits per seat, while Ultimate subscriptions include $24 per seat. Additional usage can be purchased through credits priced around $1 per credit.

The model allows customers to experiment with AI features without signing new contracts. Increased usage converts into larger credit commitments, which are recognized as recurring subscription revenue.

Bill Staples, Chief Executive Officer

“Duo Agent Platform introduces usage-based pricing alongside our seat model, aligning revenue directly with the value delivered by AI automation.”

Partnerships and Ecosystem

GitLab continues expanding its partner ecosystem to accelerate platform adoption. A large portion of the customer base operates self-managed installations, which slows deployment of new features.

Approximately 70% of revenue comes from self-managed deployments. Customers upgrade software gradually, and historically more than half adopt new releases within two quarters.

Collaboration with system integrators and technology partners helps customers upgrade infrastructure and deploy new capabilities faster.

Bill Staples, Chief Executive Officer

“We are working closely with partners to accelerate upgrades and unlock AI capabilities for our customers faster.”

Enterprise Customers

Enterprise organizations remain the primary growth driver. GitLab reported 10,682 customers with more than $5,000 ARR, accounting for over 95% of total ARR.

The number of customers generating more than $100,000 ARR reached 1,456, representing more than 75% of total ARR. High-value accounts expanded further, with over 155 customers exceeding $1 million ARR, up 26% year over year.

Large customers typically expand usage across multiple product tiers, including CI/CD automation, security scanning, governance capabilities, and deployment management.

Bill Staples, Chief Executive Officer

“We added the largest number of $1 million customers in GitLab’s history during Q4.”

Customer Success

GitLab highlighted Indeed as a long-term example of its expansion model. The company adopted GitLab in 2015 for source code management and upgraded to GitLab Premium in 2020 to support CI/CD automation.

In 2024, Indeed moved to GitLab Ultimate, deploying security and governance capabilities across thousands of developers. The upgrade produced an 80% increase in pipeline activity while lowering infrastructure costs.

Indeed recently expanded further by adopting GitLab Dedicated, integrating the platform into its infrastructure modernization strategy.

Mercedes-Benz represents another major enterprise deployment. Modern vehicles now contain large volumes of software code. GitLab supports thousands of developers across multiple regions within Mercedes-Benz and serves as a central platform for software-defined vehicle development.

Bill Staples, Chief Executive Officer

“Mercedes-Benz’s expansion illustrates our compounding growth potential as software becomes central to modern vehicles.”

Competitive Position

Developer tools competition intensified due to rapid growth of AI coding assistants. Most competing products focus on code generation and developer productivity.

GitLab positions itself differently. The platform manages software execution infrastructure, including repositories, pipelines, security checks, and deployment governance.

AI assistants generate code, but organizations still require systems that control testing, compliance enforcement, and production deployment. GitLab focuses on the operational layer where software moves from development to release.

Bill Staples, Chief Executive Officer

“Coding assistants improve authoring, but GitLab governs whether the software can actually be deployed in production.”

Market Challenges

GitLab reported several areas of demand softness. Public sector budgets remain uncertain following recent funding disruptions. Government customers represent roughly 12% of ARR.

Price-sensitive customers also experienced pressure. SMB and parts of the mid-market represent about 20% of ARR and face tighter technology budgets and staffing constraints.

Some enterprise contracts slipped into FY2027 due to customer restructuring or layoffs in industries such as retail.

Jessica Ross, Chief Financial Officer

“We observed continued weakness in price-sensitive segments, particularly SMB customers with limited budget flexibility.”

Capital Allocation

GitLab maintains a strong balance sheet with approximately $1.3 billion in cash and investments. The board authorized the company’s first share repurchase program totaling $400 million.

The program aims to offset dilution from stock-based compensation and capture value during periods when the stock trades below management’s internal valuation.

Capital allocation priorities include investment in product development, expansion of go-to-market capacity, and maintaining financial flexibility.

Outlook

GitLab guided FY2027 revenue between $1.099 billion and $1.118 billion, representing 15–17% growth. The forecast reflects the subscription model, where revenue growth follows earlier bookings trends.

Management expects FY2027 to focus on operational scaling and execution. Investments will support sales expansion, AI product development, and improved customer onboarding.

Enterprise demand remains strong and retention levels remain stable. AI capabilities create additional long-term revenue opportunities.

Long-term strategy positions GitLab as the orchestration layer for AI-driven software development, where developers and autonomous agents collaborate within a unified DevSecOps environment.

Bill Staples, Chief Executive Officer

“We believe GitLab has the ingredients to become a generational company, with deep customer relationships and a platform built over many years.”

Thoughts on GitLab Earnings Report $GTLB:

🟢Positive

• Revenue $260.4M (+23.2% YoY) beat estimates by 3.5%; EPS $0.30 beat by 30.4%

• Fiscal 2026 revenue $955M (+26% YoY); ARR exceeded $1B milestone

• Operating margin 20.5% in Q4; 17% FY operating margin, up 680 bps YoY

• Free cash flow $220M (+83% YoY) for FY2026

• Enterprise expansion continues: 1,456 customers $100K+ ARR (+18.5% YoY)

• Large accounts growing: 155+ customers above $1M ARR (+26% YoY)

• Net new ARR $64M (+3.9% YoY); highest ARR expansion year in company history

• Operating expense discipline improving: S&M 35.1% of revenue (-2.7 pp YoY), R&D 20.8% (-1.6 pp), G&A 12.4% (-0.8 pp)

• Share repurchase program $400M announced with $1.3B cash balance

🟡Neutral

• Gross margin 88.9% (-2.3 pp YoY) due to higher infrastructure and AI costs

• FCF margin 16.0% (-13.3 pp YoY) impacted by investment and timing effects

• 10,682 customers (+8% YoY) reflects stable but moderate customer growth

• AI monetization early stage; Duo Agent adoption depends on self-managed upgrades (~70% of revenue)

🔴Negative

• RPO $1.10B (+16.4% YoY) and billings $339M (+19.7% YoY) show growth slower than revenue

• FY2027 revenue guidance $1.099B–$1.118B (+15–17%) below expectations by ~1.2%

• Q1 guidance $253M–$255M (+18.4% YoY) missed estimates by ~0.8%

• Dollar-based net retention 118% vs 119% last quarter

• CAC payback 18.6 months (+1.8 YoY) indicates slower sales efficiency

• Public sector demand uncertain, representing about 12% of ARR

• Price-sensitive segment (~20% of ARR) showing weaker expansion

• Enterprise deals slipped into FY2027 due to layoffs and restructuring in some industries

• Gross margin expected to decline to 85–87% in FY2027 from 89% due to SaaS and AI infrastructure costs

Thank you for reading!

Follow me for more frequent updates on X/Twitter and Threads, and on LinkedIn. For visual infographics, check out Instagram, and for portfolio changes, follow me on SavvyTrader.

Disclaimer: This earnings review is for informational purposes only and does not constitute financial, investment, or trading advice.