CrowdStrike Earnings & Broadcom, Veeva Q1 2026 Snapshot

$CRWD, $AVGO, $VEEV Earnings analysis with review of financial performance, key metrics, operating expenses, dilution, customer growth, future outlook

Table of Contents

Detailed Earnings Analysis:

CrowdStrike CRWD 0.00%↑ .

Earnings Snapshot:

Broadcom AVGO 0.00%↑ , Veeva Systems VEEV 0.00%↑ .

CrowdStrike

Financial Results:

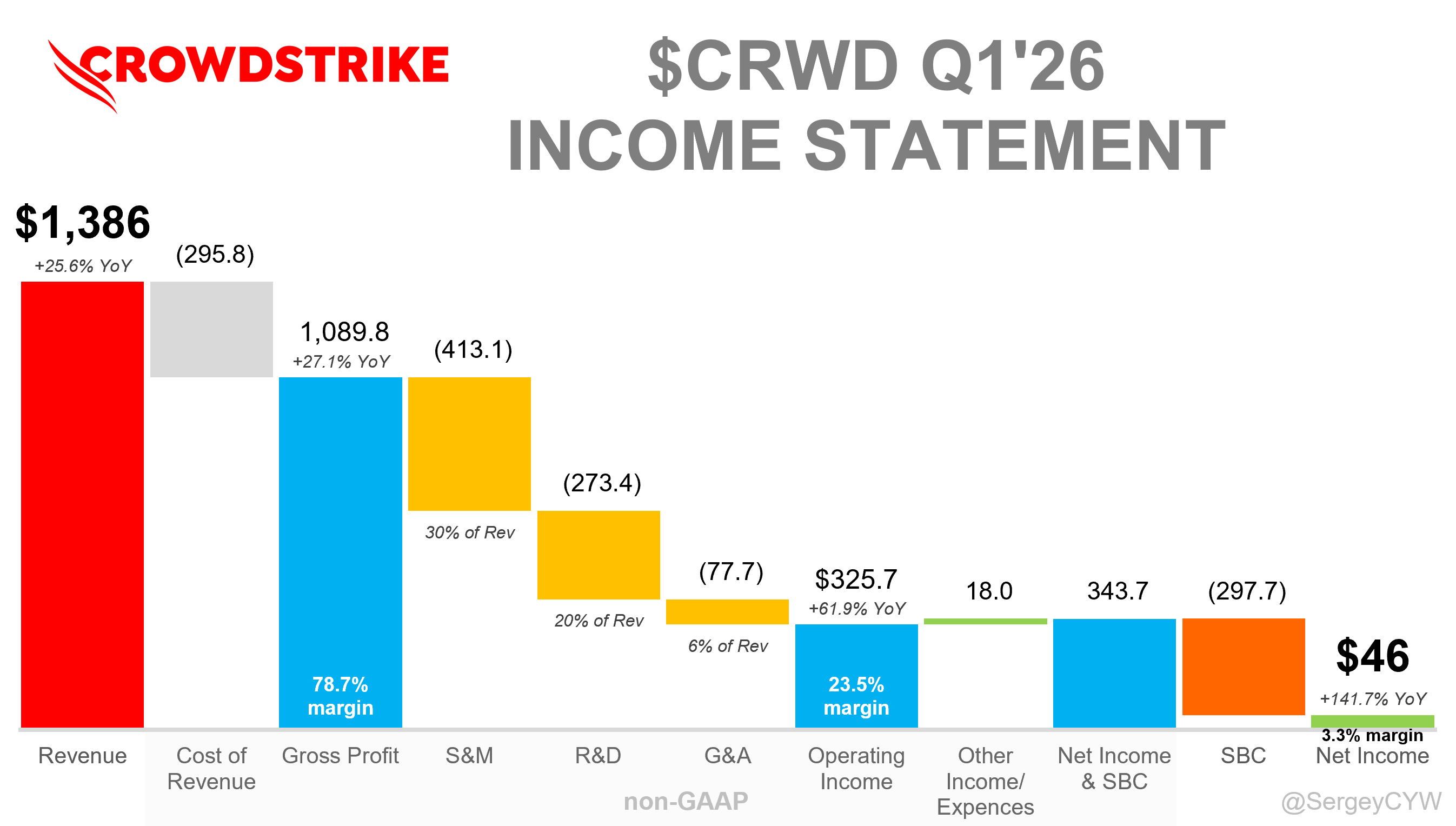

↗️$1,386M rev (+25.6% YoY, +6.1% QoQ) beat est by 1.7%

↗️GM* (78.7%, +1.0 PPs YoY)

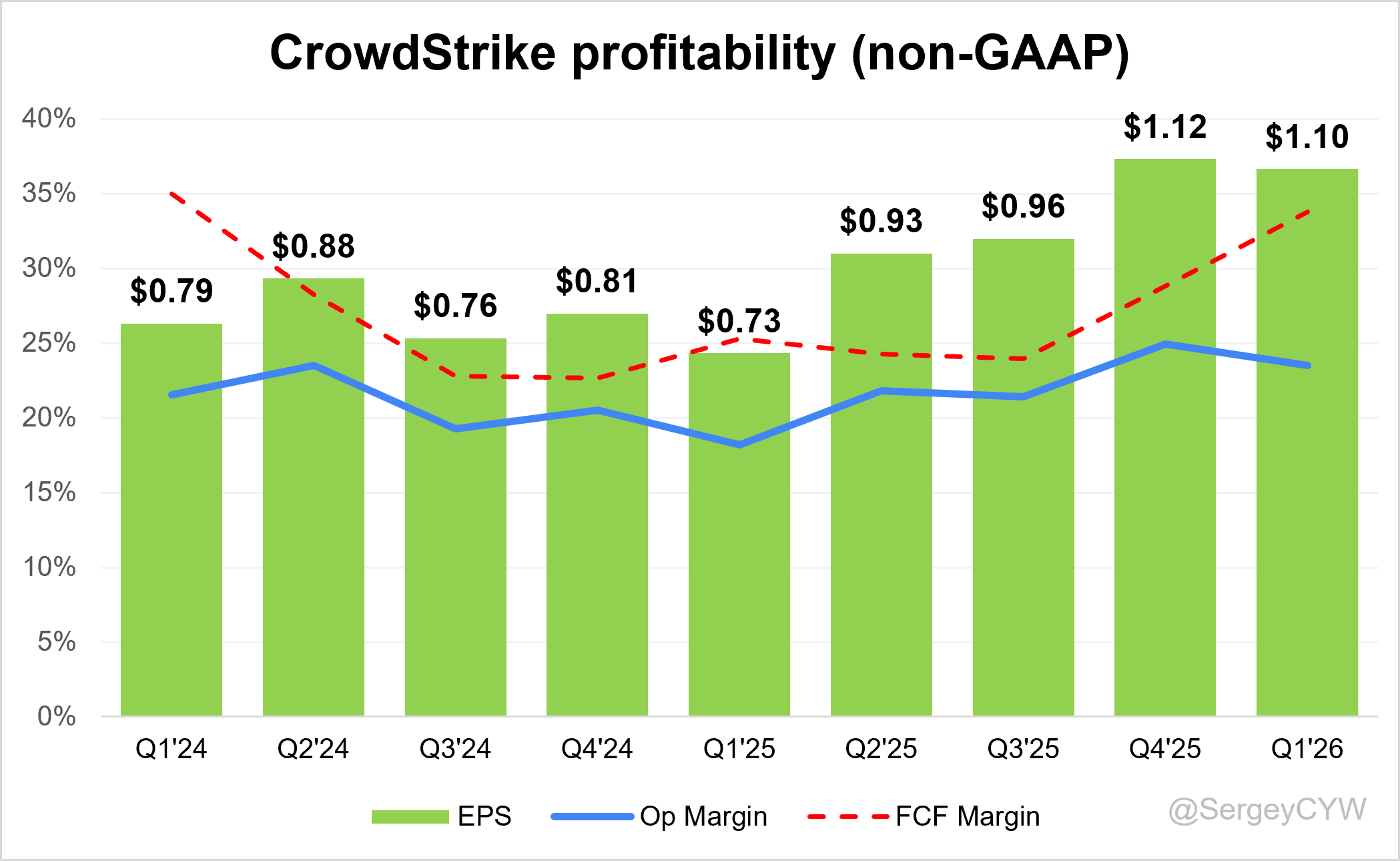

↗️Operating Margin* (23.5%, +5.3 PPs YoY)

↗️FCF Margin (33.8%, +8.5 PPs YoY)

↗️Net Margin (3.3%, +13.3 PPs YoY)

↗️EPS* $1.10 beat est by 2.8%

*non-GAAP

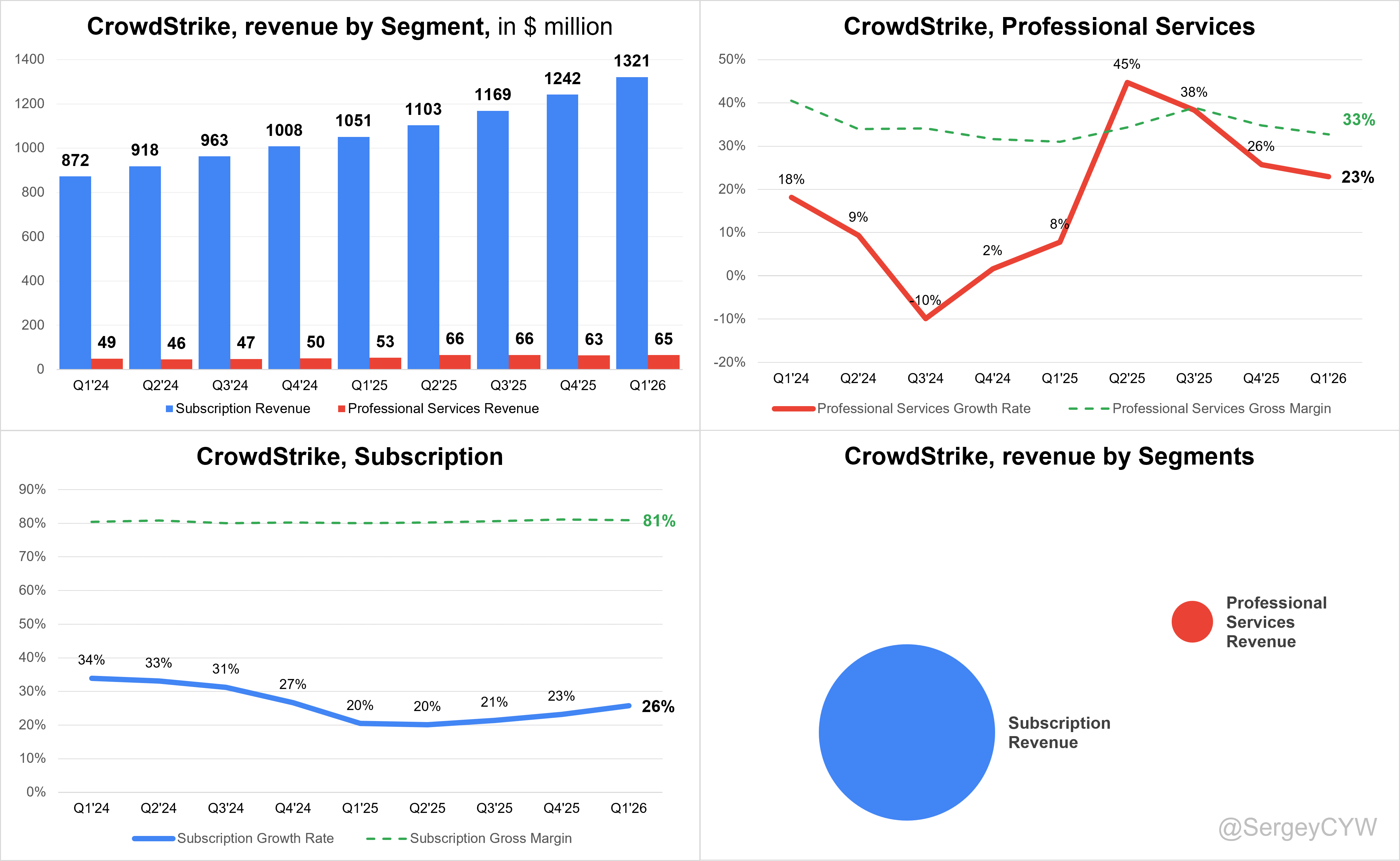

Revenue By Segments

Subscription

↗️Subscription Revenue $1,321M (+25.7% YoY)🟢

↗️GM* (80.9%, +0.9 PPs YoY)

Professional Services

➡️Professional Services Revenue $65M (+22.9% YoY)🟡

↗️GM* (32.7%, +1.7 PPs YoY)

Key Metrics

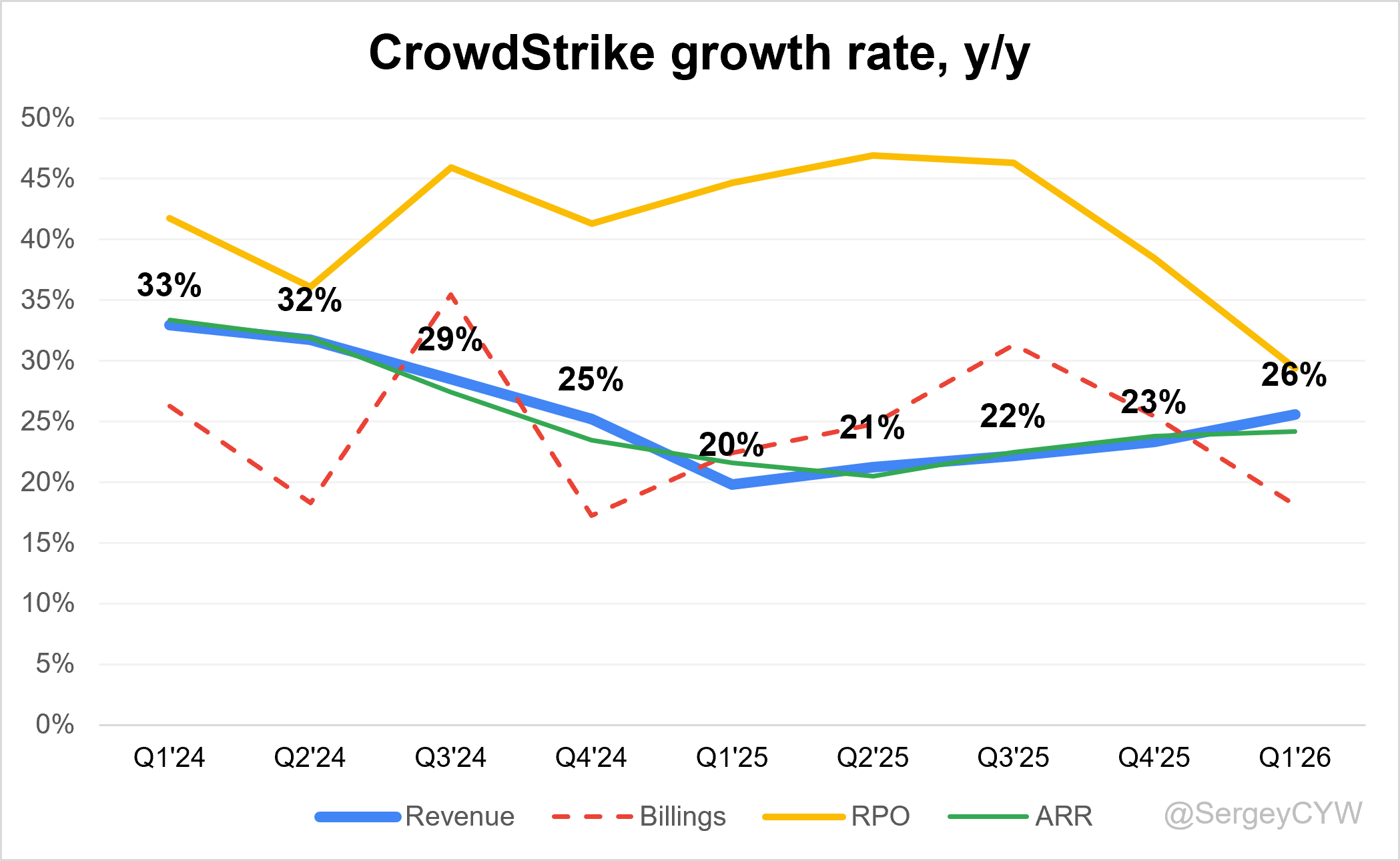

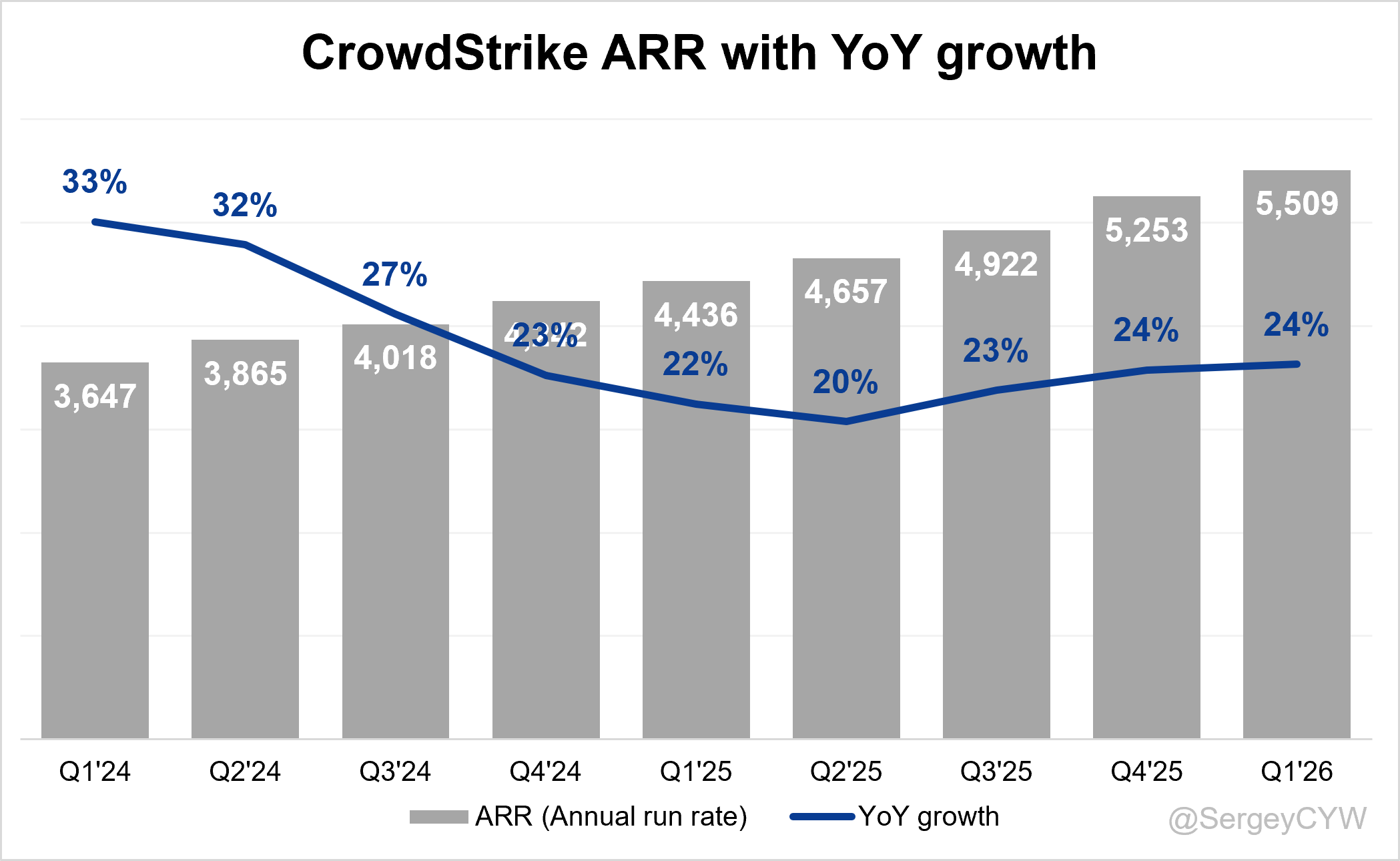

➡️ARR $5.51B (+24.2% YoY, +256 net new ARR)🟡

↗️RPO $8.80B (+29.4% YoY)

➡️Billings $1,354M (+18.2% YoY)🟡

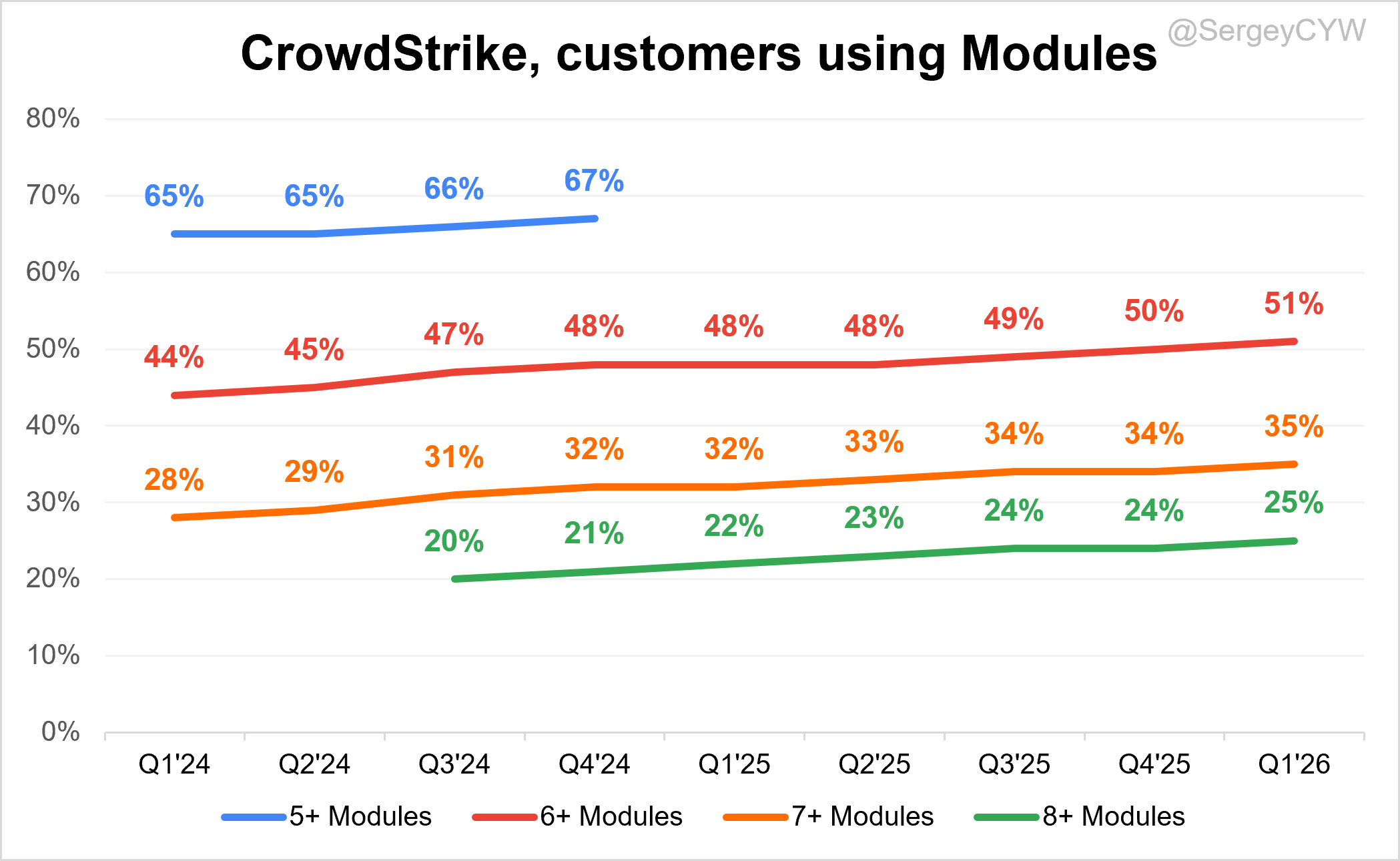

Customer Engagement with Multiple Modules

↗️% of customers using 6+ Modules (51%, 50% LQ)

↗️% of customers using 7+ Modules (35%, 34% LQ)

↗️% of customers using 8+ Modules (25%, 24% LQ)

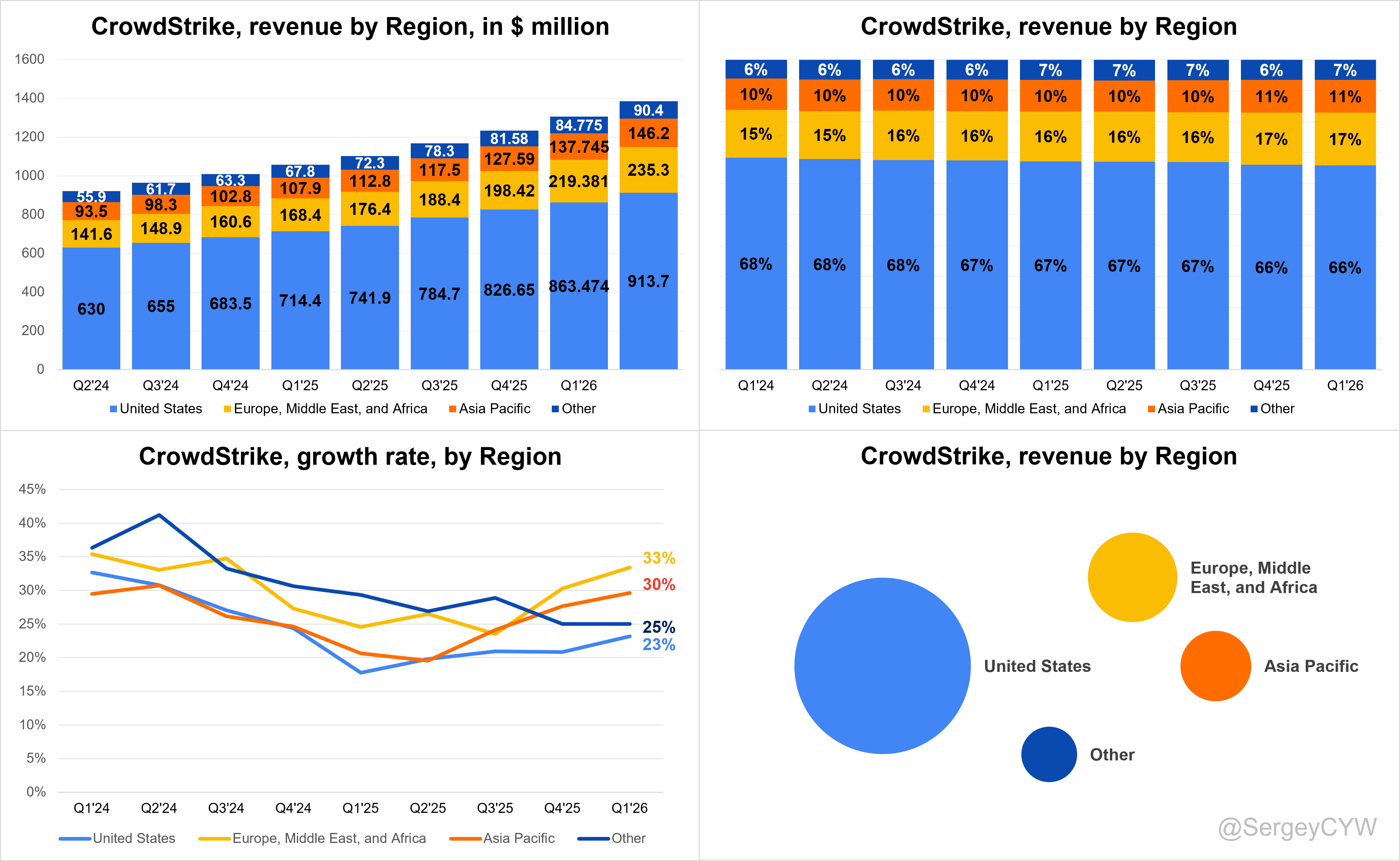

Regional Breakdown

↘️United States $913.7M rev (+23.2% YoY, 66% of Rev)

↗️Europe, Middle East, and Africa $235.3M rev (+33.4% YoY, 17% of Rev)

↗️Asia Pacific $146.2M rev (+29.6% YoY, 11% of Rev)

↘️Other $90.4M rev (+25.0% YoY, 7% of Rev)

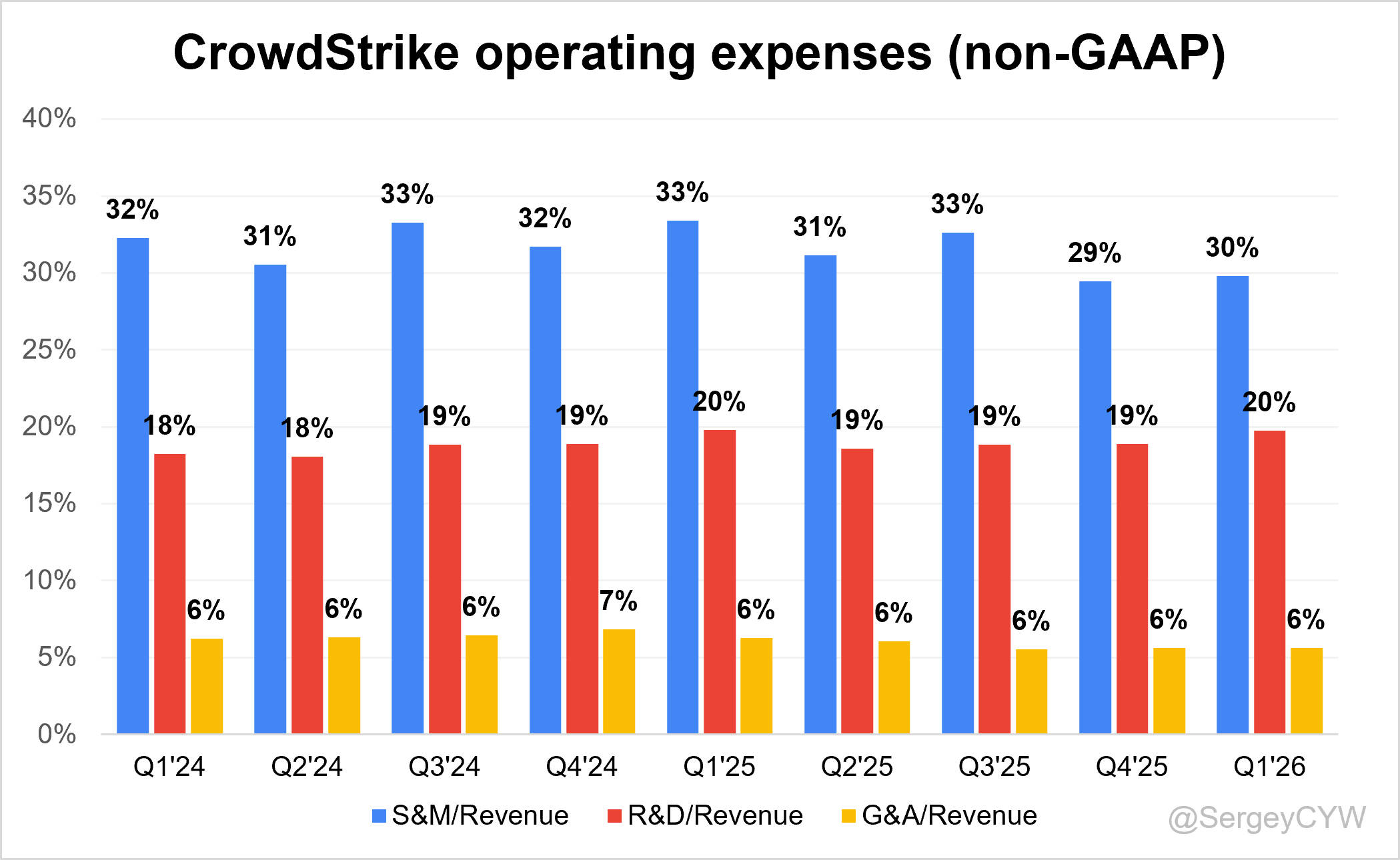

Operating expenses

↘️S&M*/Revenue 29.8% (-3.6 PPs YoY)

↘️R&D*/Revenue 19.7% (-0.0 PPs YoY)

↘️G&A*/Revenue 5.6% (-0.7 PPs YoY)

Quarterly Performance Highlights

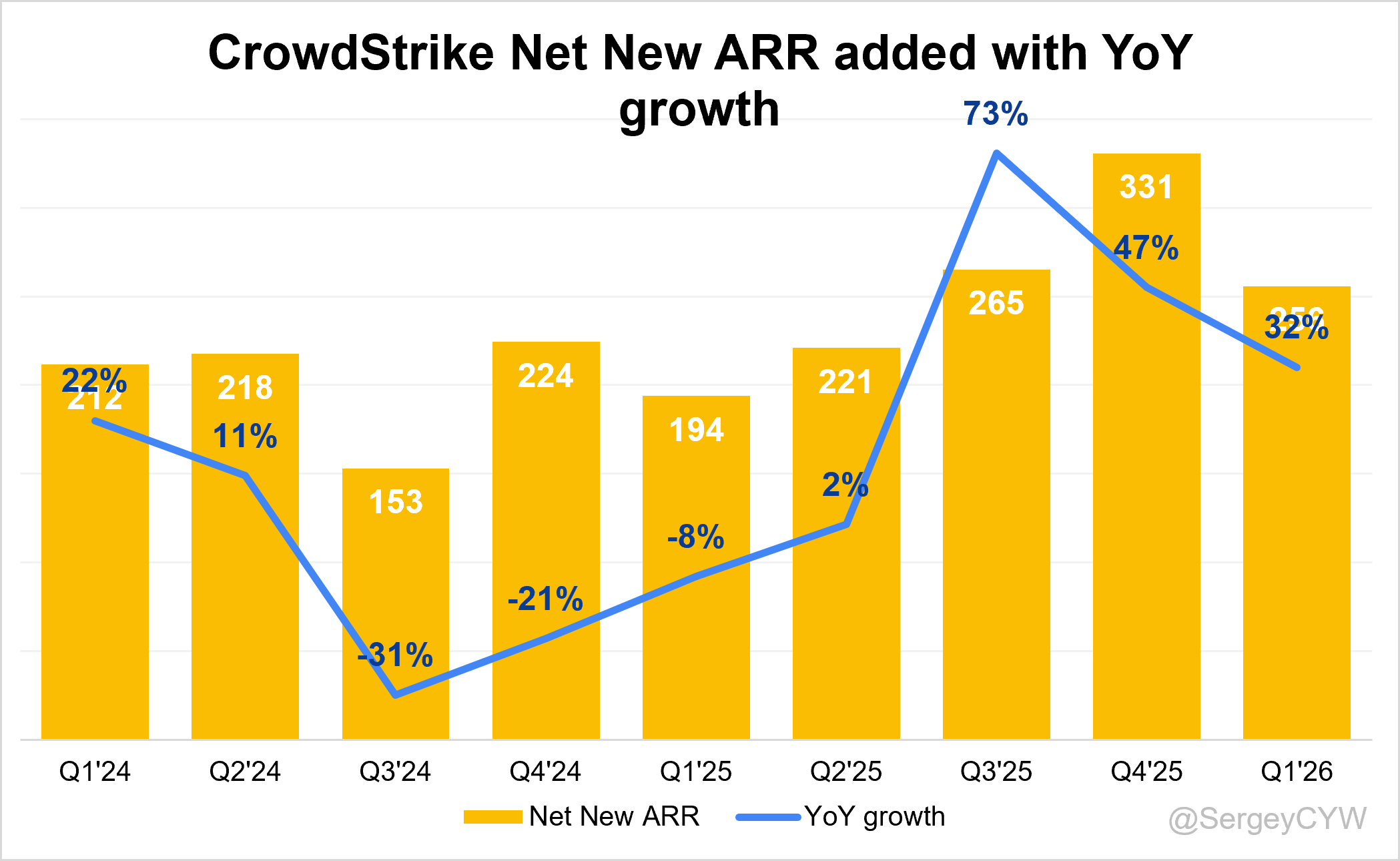

↗️Net New ARR $256M (+32.0% YoY)

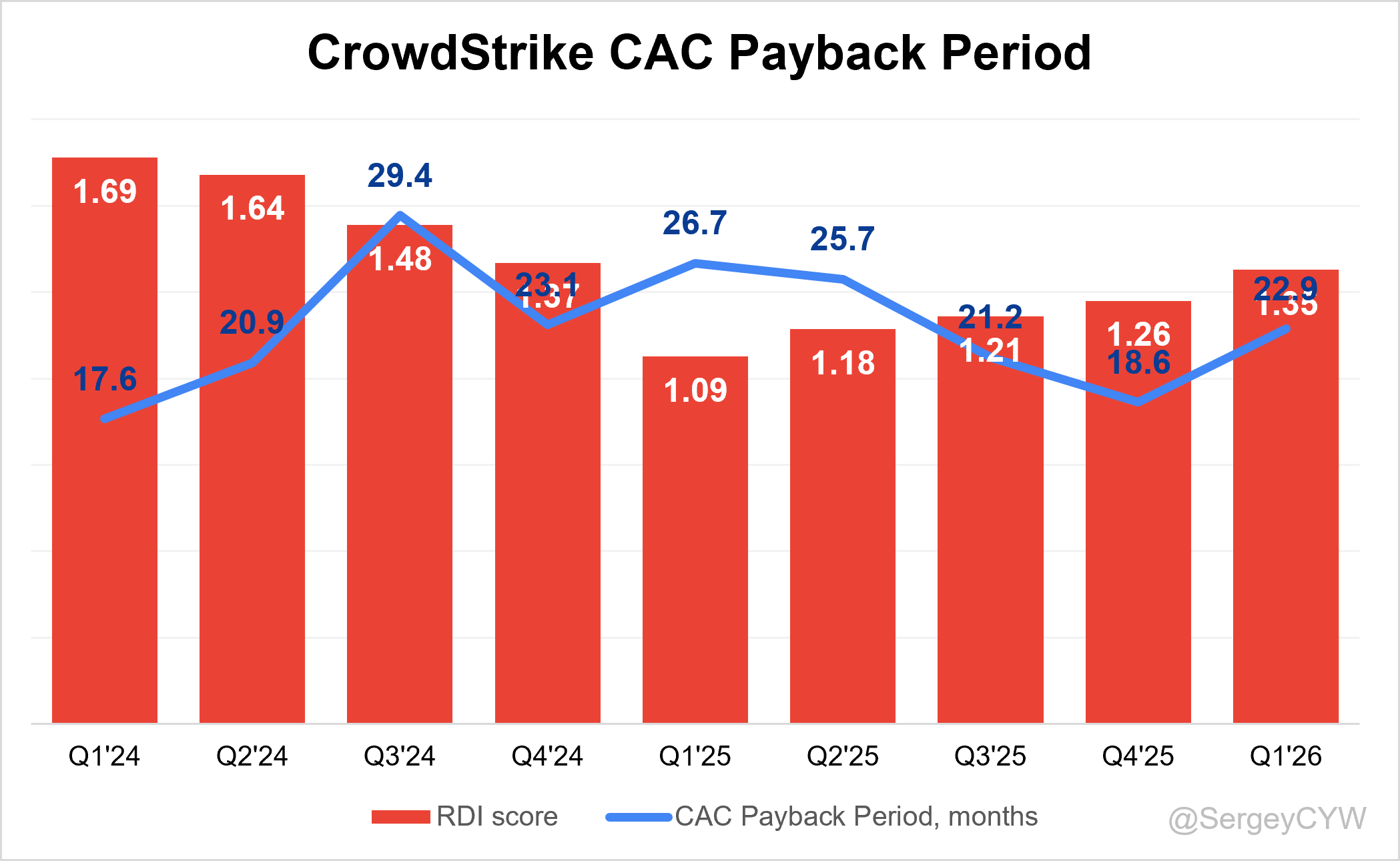

↘️CAC* Payback Period 22.9 Months (-3.8 YoY)🟢

↗️R&D* Index (RDI) 1.35 (+0.26 YoY)🟢

Dilution

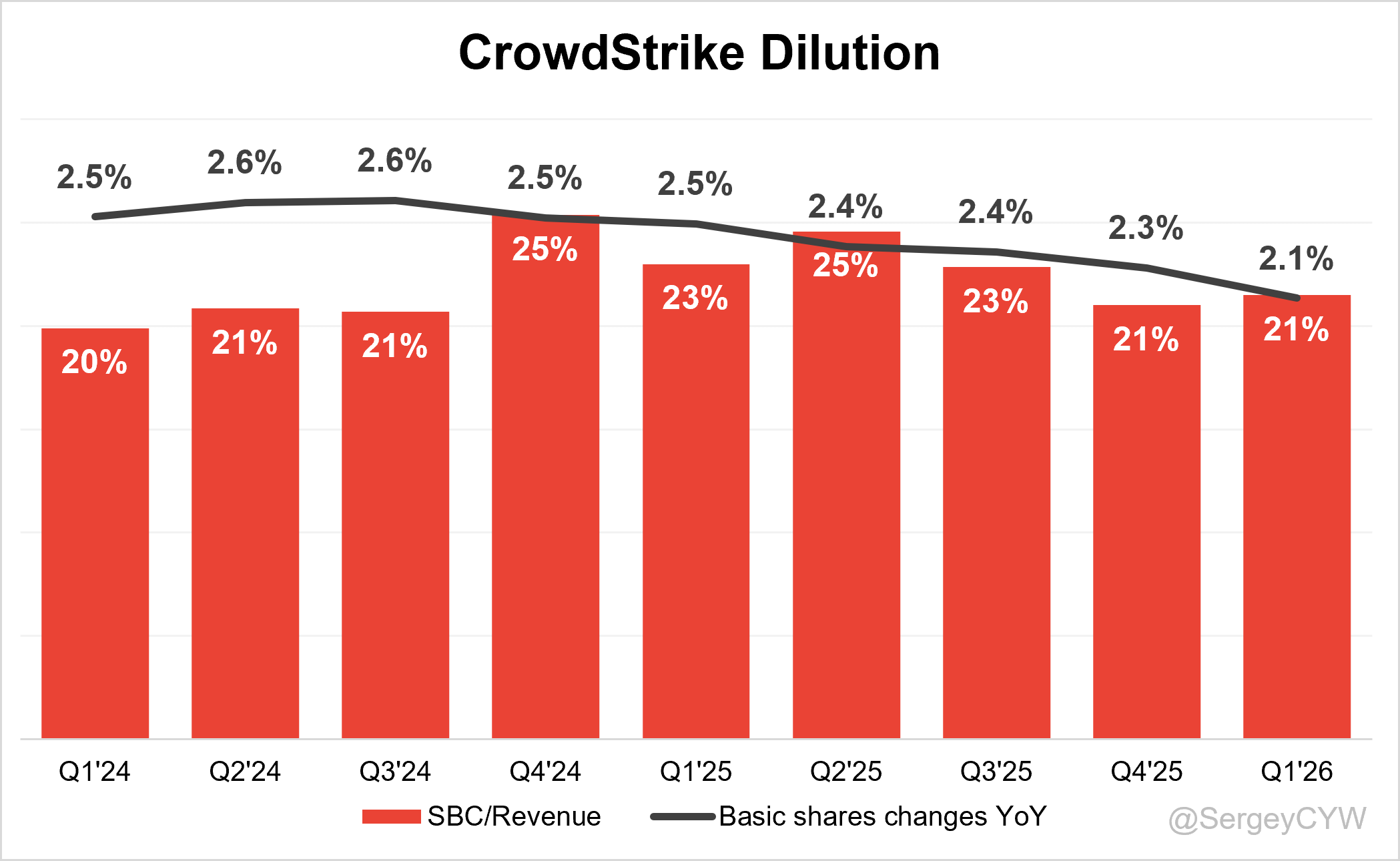

↗️SBC/rev 21%, +0.5 PPs QoQ

↘️Basic shares up 2.1% YoY, -0.1 PPs QoQ

↗️Diluted shares up 3.8% YoY, +1.9 PPs QoQ

Guidance

↗️Q2’26 $1,436.0 - $1,442.0M guide (+23.1% YoY) beat est by 0.4%

↗️$5,914.7 - $5,958.7M FY guide (+23.4% YoY) raised by 0.5% beat est by 0.6%

Points from CrowdStrike’s First Quarter 2026 Earnings Call:

Financial Performance

CrowdStrike delivered a strong Q1 FY2027, with growth accelerating at scale. Net new ARR reached $255.8 million, up 32% year over year, above guidance and a Q1 record. Ending ARR rose to $5.51 billion, up more than 24% year over year. Revenue reached $1.39 billion, up 26%, marking the fourth straight quarter of revenue growth acceleration.

Profitability improved alongside growth. Non-GAAP operating income reached $325.7 million, equal to a 24% operating margin, up 530 basis points year over year. Non-GAAP net income was $283.4 million, or $1.10 per diluted share. GAAP net income was positive at $27.8 million.

Cash generation was a standout. Operating cash flow reached $590.9 million. Free cash flow reached a record $468.5 million, equal to 34% of revenue. Free cash flow Rule of 40 was 59, improving for the fourth consecutive quarter. Cash and equivalents ended at $4.55 billion. CrowdStrike repurchased $176 million of stock at an average price of $365.63, with $1.3 billion remaining under authorization.

Falcon Platform

Falcon is being positioned as the security layer for enterprise AI adoption. The platform now spans endpoints, cloud workloads, identities, SaaS applications, exposure management, SIEM, AI agents, and data flows.

George Kurtz, Chief Executive Officer and Founder

“To secure AI, organizations need the Falcon platform. To deliver the platform, you need the right go-to-market model. Flex is the commercial harness to drive secure AI adoption.”

AI adoption increases machine activity, agentic workloads, identities, API calls, and runtime risk. Falcon is designed to observe and control activity where attacks execute.

Commercial traction remained strong. CrowdStrike cited an eight-figure new-logo win with a major U.S. government agency. Falcon replaced legacy antivirus, operating-system EDR, and legacy vulnerability management across more than 200,000 hosts.

Falcon is becoming a consolidation platform. Customers are replacing older tools and expanding into adjacent modules. The main challenge is proving AI-driven platform expansion can convert into durable ARR, not only short-term demand.

Falcon Flex

Falcon Flex remains one of CrowdStrike’s strongest financial indicators. The company added more than 300 Falcon Flex accounts in Q1. Flex accounts reached more than $1.9 billion in ending ARR, up 99% year over year.

Flex gives customers a committed spending model across modules. Customers can start with endpoint and later add AI DR, Identity, Cloud, SIEM, Exposure Management, or SaaS protection without restarting procurement.

Re-Flex metrics show strong expansion. CrowdStrike reached 480 Re-Flex customers, nearly 25% of all Flex customers. Average Re-Flex uplift was 26%. Average Re-Flex timing was seven months, ahead of renewal.

More than 130 customers have Re-Flexed multiple times. Average ARR uplift for multi-Re-Flex customers was 51% over the original commitment.

George Kurtz, Chief Executive Officer and Founder

“Customers are coming back multiple times, and they’re continuously spending more, consolidating on CrowdStrike.”

The main challenge is pricing flexibility. AI products may move toward credits, tokens, or usage-based models. Falcon Flex can support the shift, but customers still need spend predictability.

Falcon Cloud

Falcon Cloud Security had another strong quarter, supported by demand for AI infrastructure protection. The product is shifting from cloud posture management toward runtime protection and control.

George Kurtz, Chief Executive Officer and Founder

“Cloud had another strong quarter as enterprises continue securing their AI infrastructure. Concern around elevated risk from new frontier models has pushed customers to harden their cloud environments.”

AI workloads increasingly run in cloud environments, containers, Kubernetes infrastructure, and long-running agentic systems. Visibility alone is not enough. Customers need enforcement.

A key proof point was an eight-figure win with a high-performance AI chip company. CrowdStrike secured rapidly expanding Kubernetes-managed data center and cloud environments tied to AI infrastructure growth.

George Kurtz, Chief Executive Officer and Founder

“When you think about cloud security, for a long time, it was about posture management. In the AI world, it’s really about runtime protection and control.”

Cloud security benefits from the AI buildout across chips, hyperscalers, neoclouds, data centers, and agentic applications. Competition remains high, so CrowdStrike must prove runtime security plus platform integration can outperform standalone cloud posture tools.

Falcon Shield

Falcon Shield delivered strong growth, with ending ARR up nearly 4x year over year. The product is gaining relevance as SaaS applications become agentic attack surfaces.

George Kurtz, Chief Executive Officer and Founder

“Falcon Shield had another stellar quarter with ending ARR growing nearly 4x year-over-year as organizations secure their SaaS agentic attack surface.”

AI agents can access workflows, permissions, data, and automated actions across business applications. SaaS security is becoming more strategic as agent activity expands.

Falcon Shield helps secure the SaaS layer of AI adoption. The product is moving beyond SaaS posture and configuration visibility toward protection for agent interactions with SaaS systems.

Rapid ARR growth signals strong adoption from a smaller base. The main challenge is market education, as many enterprises are still learning how AI agents change SaaS risk.

Falcon Identity

Falcon Identity Protection is becoming more important as AI agents create new identity risk. Every agent needs an identity, and every identity needs governance. Enterprises also need to separate human activity from machine activity.

George Kurtz, Chief Executive Officer and Founder

“In the AI era, every agent needs an identity, every identity needs governance, and every enterprise is realizing they can’t tell human from machine in their environment.”

The key innovation is the combination of Falcon Next-Gen Identity with SGNL. SGNL adds real-time, policy-based authorization for agentic workloads. The platform helps control what agents can and cannot do across applications and systems.

A major American healthcare company selected Falcon Next-Gen Identity and SGNL in a seven-figure expansion. The goal was to govern AI-agent access across the enterprise.

Next-Gen Identity net new ARR growth accelerated versus Q4. SGNL is being positioned as a control plane for agentic identity. The category remains early, and many customers are still moving from problem awareness to formal deployment.

George Kurtz, Chief Executive Officer and Founder

“SGNL delivers granular, policy-based authorization over agentic workloads in real time. This is the identity opportunity in the AI era.”

Charlotte AI

Charlotte AI is becoming the intelligence layer across Falcon. Ending ARR accelerated sequentially over Q4. Charlotte triages alerts, correlates telemetry, and automates investigations at machine speed.

George Kurtz, Chief Executive Officer and Founder

“Charlotte AI, where ending ARR accelerated sequentially over Q4, is now the reasoning engine across Falcon, triaging alerts, correlating cross-domain telemetry, and automating investigation at machine speed.”

Charlotte strengthens Falcon’s data advantage by converting security telemetry into automated analyst work. The product also supports the company’s AI SOC strategy.

AgentWorks extends Charlotte’s role. Partners including Accenture, AWS, Anthropic, Deloitte, NVIDIA, OpenAI, and Salesforce are building specialized AI security agents on Falcon data.

Charlotte AI helps CrowdStrike move customers away from manual alert management toward AI-speed security operations. The main challenge is proving productivity gains at scale in a market where AI security assistants are becoming common.

George Kurtz, Chief Executive Officer and Founder

“The result, a security operations center that runs at AI speed, orchestrated by Charlotte, extended by the ecosystem, and grounded in the richest telemetry in the industry.”

Next-Gen SIEM

Next-Generation SIEM was one of the strongest growth areas. The business exceeded $600 million in ending ARR. Combined ARR from Next-Gen SIEM, Cloud, and Identity surpassed $2 billion.

CrowdStrike positions Next-Gen SIEM as the operating system of the AI SOC. The product targets legacy SIEM pain points: cost, data volume, slow workflows, and analyst fatigue.

A major customer win came from an eight-figure new-logo deal with a major fuel retailer. CrowdStrike replaced a legacy SIEM, a next-gen EDR product, and software from a network security hardware vendor.

Charlotte AI’s autonomous triage helped reduce manual alert management and begin the customer’s AI SOC transition.

George Kurtz, Chief Executive Officer and Founder

“The performance and price superiority of Next-Gen SIEM, combined with Charlotte AI’s autonomous triage, eliminates swivel chair alert management, successfully starting this customer’s AI SOC journey.”

Success is coming from legacy SIEM displacement and increased data ingestion needs. The challenge is migration complexity, as customers often move carefully when replacing core SOC infrastructure.

Product Innovation

Product innovation is centered on AI security. Key initiatives include Project QuiltWorks, AI Detection and Response, AgentWorks, Charlotte AI expansion, SGNL, and Seraphic.

George Kurtz, Chief Executive Officer and Founder

“Within days of Anthropic’s Project Glasswing and OpenAI’s TAC, we announced Project QuiltWorks to unite and mobilize the industry around Mythos readiness.”

Project QuiltWorks focuses on vulnerability discovery, prioritization, remediation, and executive communication. It helps customers assess readiness for frontier AI risk.

George Kurtz, Chief Executive Officer and Founder

“QuiltWorks is a phased process of vulnerability discovery, prioritization, remediation, and then executive communication.”

In one engagement, EY used Falcon Exposure Management and frontier models at a Fortune 100 account and uncovered more than 45 million vulnerabilities. The engagement also created opportunities for Falcon Exposure Management, Falcon for IT, and Next-Gen SIEM.

CrowdStrike closed the SGNL and Seraphic acquisitions in Q1. The acquisitions contributed $7.8 million of acquired net new ARR, within the expected $5 million to $8 million range. SGNL strengthens authorization for agentic workloads. Seraphic adds browser and web security capabilities.

AI Detection and Response (AI DR)

AI Detection and Response is one of the most important growth stories. AI DR ending ARR grew more than 250% sequentially. Q2 pipeline already exceeded $50 million.

Management believes AI DR can become larger than EDR. EDR protects hosts. AI DR protects data, models, prompts, agents, identities, infrastructure, and the interaction layer.

George Kurtz, Chief Executive Officer and Founder

“As I look forward, I see AI DR as a larger opportunity than EDR.”

CrowdStrike sees a structural advantage from its existing endpoint sensor. Agents run on endpoints, make tool calls, access files, invoke APIs, and move data. Falcon can detect, block, and respond where AI activity runs.

George Kurtz, Chief Executive Officer and Founder

“While competitors may provide AI visibility, only CrowdStrike can detect, block, and respond where AI actually runs.”

An automotive financial services leader added AI DR to more than 30,000 hosts for shadow AI visibility and protection. The deal was a seven-figure win and a greenfield upsell using the same Falcon sensor.

Customers

Customer demand was broad-based. Management cited strong module adoption, strong gross and net retention, competitive displacements, and a record Q2 pipeline.

Burt Podbere, Chief Financial Officer

“This strength is reflected in our continued strong retention rates, increased module adoption, third consecutive quarter of ending ARR growth acceleration for the endpoint business, and Q2 record pipeline.”

Endpoint growth accelerated for the third consecutive quarter. Adoption remained strong across Next-Gen SIEM, Cloud, Identity, Falcon Shield, Falcon Exposure Management, Falcon for IT, and AI DR.

Falcon Flex shows clear expansion strength. Re-Flex customers expanded early and often. Average uplift was 26%, while customers with multiple Re-Flex events reached 51% average ARR uplift over the original commitment.

George Kurtz, Chief Executive Officer and Founder

“As soon as Project Glasswing and Mythos were announced, a deluge of customer, prospect, and partner inquiries followed. Post-Mythos threat landscape readiness reached a fever pitch, with the primary question being, is my organization protected?”

Large Wins

A major U.S. government agency signed an eight-figure new-logo deal. CrowdStrike replaced legacy antivirus, operating-system EDR, and legacy vulnerability management across more than 200,000 hosts.

George Kurtz, Chief Executive Officer and Founder

“Illustrating this was an eight-figure new logo land in a major U.S. government agency. We replaced a legacy AV, an operating system EDR, and a legacy vulnerability management point product across more than 200,000 hosts.”

An automotive financial services leader added AI DR to more than 30,000 hosts in a seven-figure win. The customer used AI DR for shadow AI visibility and protection.

A major fuel retailer signed an eight-figure new-logo deal for Next-Gen SIEM. CrowdStrike replaced a legacy SIEM, next-gen EDR, and software from a network security hardware vendor.

A high-performance AI chip company signed an eight-figure cloud security deal. CrowdStrike secured expanding Kubernetes-managed data center and cloud environments tied to AI infrastructure growth.

A major American healthcare company selected Falcon Next-Gen Identity and SGNL in a seven-figure expansion. The customer needed governance for AI-agent access across the enterprise.

Partnerships

Partnerships strengthened the AI security narrative. CrowdStrike said it was the only cybersecurity company selected by both Anthropic and OpenAI from the start to secure frontier AI model programs.

George Kurtz, Chief Executive Officer and Founder

“CrowdStrike is the only cybersecurity company to secure both Anthropic and OpenAI’s introduction programs from the very start.”

Project QuiltWorks expanded into a broad ecosystem. Accenture, EY, IBM, Kroll, and OpenAI joined first. Armadin, Cognizant, HCLTech, Infosys, KPMG, NTT Data, Tata Consultancy Services, and Wipro joined later.

Insurers including Coalition, Liberty Mutual Insurance, Lockton, Resilience, and Marsh joined to help underwrite frontier AI model risk for enterprises.

AgentWorks expanded the partner network further. Accenture, AWS, Anthropic, Deloitte, NVIDIA, OpenAI, and Salesforce are building specialized security agents on Falcon data.

CrowdStrike also appointed Dr. Bartley Richardson as Chief AI and Autonomous System Officer. He joined from NVIDIA, where he led agentic AI and cybersecurity AI.

Stock Split

CrowdStrike announced its first stock split as a public company: a four-for-one forward stock split.

George Kurtz, Chief Executive Officer and Founder

“Given the strength of this quarter and our confidence in what’s ahead, I’m announcing CrowdStrike’s first stock split as a public company.”

Shareholders of record after market close on June 25, 2026 will receive three additional shares for each share held after market close on July 1, 2026. Split-adjusted trading is expected to begin on July 2, 2026.

Burt Podbere, Chief Financial Officer

“Stockholders of record after the close of market on June 25th, 2026, will receive an additional three shares of common stock for every one share held after the close of market on July 1st, 2026, with trading on a split adjusted basis expected to commence at market open on July 2nd, 2026.”

The split does not change business value. It lowers the per-share price and may broaden investor access.

CrowdStrike also provided split-adjusted EPS guidance. Q2 FY2027 non-GAAP EPS is expected to be about $0.29. Full-year FY2027 split-adjusted non-GAAP EPS is expected to be $1.22 to $1.24.

Challenges

The main challenge is execution. CrowdStrike is building a large AI security narrative, but several markets remain early.

George Kurtz, Chief Executive Officer and Founder

“The gap between AI adoption and AI protection is the widest asymmetry in security since the cloud transition, and it’s moving faster.”

AI DR is growing fast, but the category is still new. Pipeline strength must convert into durable ARR.

Enterprise AI adoption is still in early stages. Developer use is leading adoption, while broader enterprise rollout may take more time.

George Kurtz, Chief Executive Officer and Founder

“The adoption front runs the security piece of it. That’s why so many CISOs, CIOs, and CEOs are calling us saying, ‘We need something to keep up with the adoption of AI.’”

Pricing may also evolve. AI products could shift toward token-based or usage-based models. CrowdStrike must balance flexible consumption with customer budget certainty.

Future Outlook

CrowdStrike raised its FY2027 outlook, supported by stronger demand, record Q2 pipeline, AI tailwinds, high retention, module adoption, and platform consolidation.

George Kurtz, Chief Executive Officer and Founder

“What I see is AI driving structural demand for cybersecurity that compounds, not decelerates.”

For Q2 FY2027, expected ARR is $5.793 billion to $5.795 billion, up 24% year over year. Net new ARR is expected at $284 million to $286 million, up 28% to 29%. Revenue is expected at $1.436 billion to $1.442 billion, up about 23%.

For FY2027, expected ARR is $6.532 billion to $6.556 billion, up 24% to 25%. Net new ARR is expected at $1.279 billion to $1.303 billion, up 27% to 29%. Revenue is expected at $5.915 billion to $5.959 billion, up 23% to 24%.

Non-GAAP operating income is expected at $1.452 billion to $1.480 billion. Non-GAAP net income is expected at $1.263 billion to $1.285 billion.

Free cash flow guidance remains strong. Q2 free cash flow margin is expected at 24.5%, the seasonal low. Full-year free cash flow margin is expected to be at least 30%.

Net new ARR seasonality is expected at 42% in the first half and 58% in the second half. Free cash flow dollars are expected to split 46% in the first half and 54% in the second half.

Key points on CrowdStrike Earnings Report:

🟢Positive

Revenue reached $1.386B, up 25.6% YoY and 6.1% QoQ, beating estimates by 1.7%.

Net new ARR reached $256M, up 32% YoY, showing stronger demand momentum.

Free cash flow margin expanded to 33.8%, up 8.5 percentage points YoY.

Operating margin improved to 23.5%, up 5.3 percentage points YoY, showing better efficiency.

EPS was $1.10, beating estimates by 2.8%.

Subscription revenue reached $1.321B, up 25.7% YoY, with 80.9% gross margin.

RPO reached $8.80B, up 29.4% YoY, supporting future revenue visibility.

Customer module adoption improved: 51% use 6+ modules, 35% use 7+, and 25% use 8+.

Falcon Flex accounts exceeded $1.9B in ending ARR, up 99% YoY.

AI DR ending ARR grew more than 250% sequentially, with Q2 pipeline above $50M.

Next-Gen SIEM exceeded $600M in ending ARR; combined Next-Gen SIEM, Cloud, and Identity ARR surpassed $2B.

CrowdStrike raised FY2027 guidance, with expected revenue of $5.915B–$5.959B, up 23%–24% YoY.

🟡Neutral

ARR reached $5.51B, up 24.2% YoY, but growth was marked as stable rather than accelerating.

Billings reached $1.354B, up 18.2% YoY, slower than revenue growth.

Professional services revenue was $65M, up 22.9% YoY, solid but less central than subscription growth.

U.S. revenue was $913.7M, up 23.2% YoY, representing 66% of revenue.

International growth was stronger: EMEA up 33.4%, Asia Pacific up 29.6%.

Q2 revenue guidance of $1.436B–$1.442B implies 23.1% YoY growth, slightly above estimates by 0.4%.

The 4-for-1 stock split may improve accessibility.

AI security demand is early. Management sees strong demand, but adoption still needs broader enterprise rollout.

SBC/revenue was 21%, up 0.5 percentage points QoQ, keeping dilution pressure elevated.

🔴Negative

Diluted shares rose 3.8% YoY and 1.9% QoQ.

Billings growth of 18.2% YoY lagged revenue growth of 25.6% YoY.

Pricing may become more complex as AI products move toward credits, tokens, or usage-based models.

Cloud security and SIEM remain competitive markets; CrowdStrike must keep proving platform value against standalone vendors.

My thoughts on CrowdStrike ER:

Overall, this was a strong quarter. Revenue growth accelerated to +25.6% YoY, while full-year guidance was raised by approximately 0.5%. If the company beats next quarter’s guidance by a similar margin, revenue growth would remain around +25% YoY.

That said, I was expecting management to provide a stronger outlook. Given the company’s significantly expanded valuation multiples prior to earnings (EV/Sales of 36.5x and Forward P/E of 154x), the market appears to have been expecting more as well, which likely explains why the stock fell 11.2% after earnings.

On the positive side, profitability continues to improve across all major metrics:

Non-GAAP gross margin increased to 78.7%, up +1.0 percentage point YoY

Non-GAAP operating margin increased to 23.5%, up +5.3 percentage points YoY

GAAP net margin improved from negative territory last year to positive territory this year

CrowdStrike product adoption improved across all customer cohorts, with the percentage of customers using 6+, 7+, and 8+ modules each increasing by +1.0 percentage point QoQ.

Management stated that retention remained strong. Based on those comments, it is reasonable to assume that DBNR remained around last quarter’s 115% level.

Cloud security and SIEM remain highly competitive markets, but CrowdStrike continues to execute well. Next-Gen SIEM benefited from AI-driven growth in data volumes, surpassing $600 million in ending ARR. Combined ARR across Next-Gen SIEM, Cloud, and Identity exceeded $2 billion.

Management emphasized that increasing agentic AI activity is raising the value of data ingestion and driving stronger demand for AI-speed security operations.

Falcon Flex accounts exceeded $1.9 billion in ending ARR, up 99% YoY, helping customers expand across multiple modules as AI security requirements evolve.

Falcon Shield also delivered impressive growth, with ending ARR increasing nearly 4x YoY.

AI-related product traction was visible in several specific metrics. AI DR ending ARR grew more than 250% sequentially, with the Q2 pipeline already exceeding $50 million. AI DR is growing rapidly, although the category remains very early, and AI-related products may eventually transition toward token-based or usage-based pricing models.

CrowdStrike is clearly benefiting from AI tailwinds and also from the broader trend of platform consolidation.

Management remains extremely optimistic about the company’s future.

George Kurtz:

“What I see is AI driving structural demand for cybersecurity that compounds, not decelerates.”

He also added:

“As I look forward, I see AI DR as a larger opportunity than EDR.”

Management further highlighted that CrowdStrike was the only cybersecurity company selected by both Anthropic and OpenAI from the beginning to secure frontier AI model programs, which is a meaningful validation of the company’s position in AI security.

On the negative side, although ARR growth accelerated, it remains below revenue growth. Growth in billings and RPO slowed significantly, although RPO growth still remains ahead of revenue growth for now.

In addition, I expected a stronger outlook for the next quarter. Based on the guidance provided, management appears to be signaling stabilization of revenue growth rather than further acceleration, which likely contributed to the market’s disappointment despite what was otherwise a strong quarter.

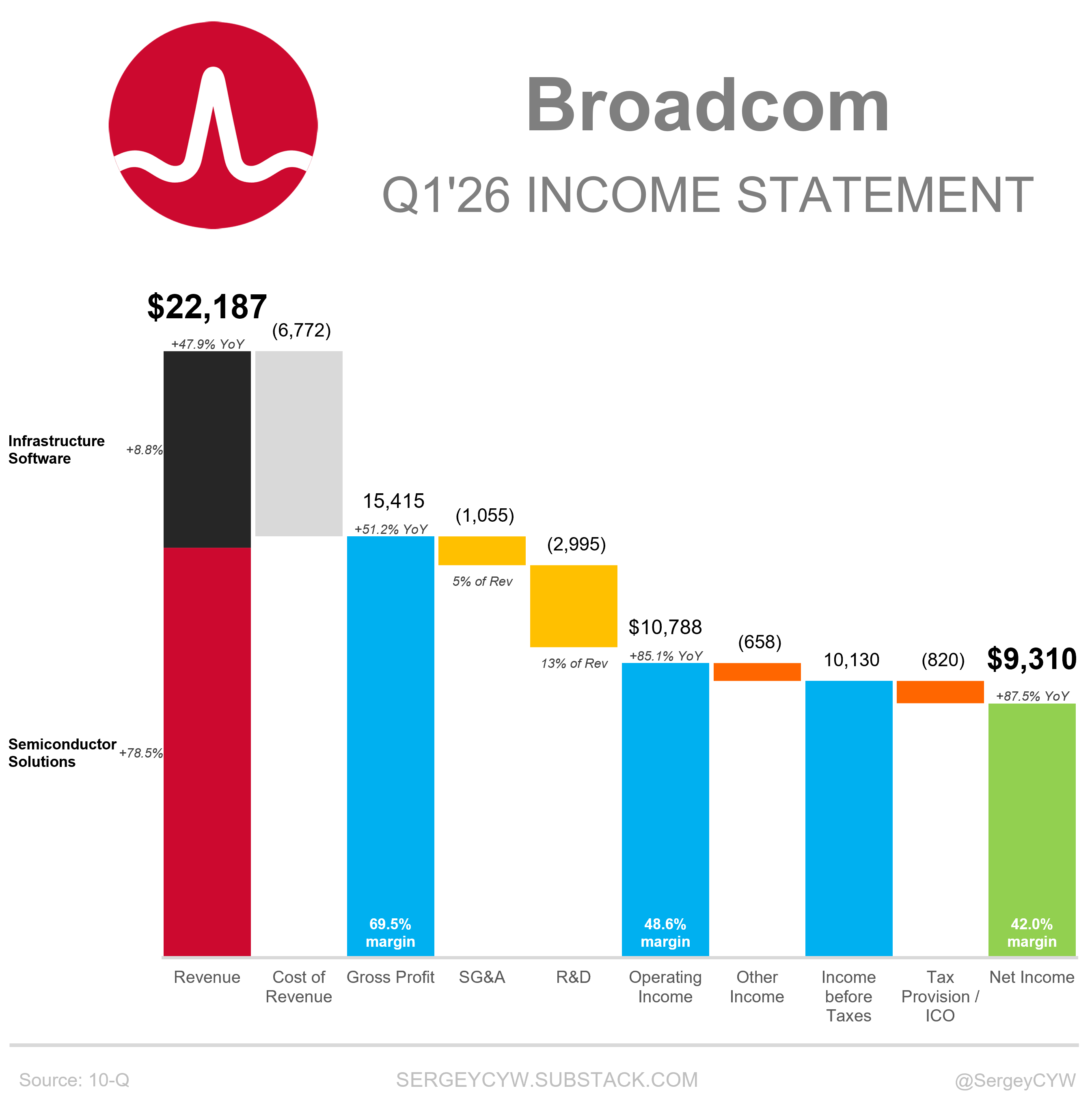

Broadcom

$AVGO delivered another strong quarter. Broadcom is becoming one of the key infrastructure suppliers behind frontier AI compute.

Q1 2026 (Q2 FY2026) Revenue reached $22.2B, up 48% YoY, with Semiconductor Solutions growing 79% YoY to $15.0B. The AI semiconductor business was the standout: $10.8B in revenue, up 143% YoY, supported by demand for custom XPUs and high-speed networking.

The most important signal was not just what Broadcom shipped, but what customers ordered.

AI semiconductor bookings were over $30B in the quarter versus $10.8B shipped. Management also said visibility now extends into 2028, which is unusual for a semiconductor business and reflects the long planning cycles around wafers, memory, power, and data-center capacity.

The 2026 and 2027 trajectory is the core bull case:

2026 AI semiconductor revenue target: $56B

2027 AI semiconductor revenue target: over $100B

2028: expected continued growth

Broadcom also highlighted long-term relationships with Google, Anthropic, OpenAI, Meta, and two additional customers. These are not simple purchase orders. They are multi-generation, multi-gigawatt compute roadmaps.

Networking remains an underappreciated part of the story. It represented nearly 40% of Q2 AI revenue, though management suggested a more normalized level may be closer to 30%. Either way, AI clusters need more than accelerators. They need switching, SerDes, PCIe, DSPs, optics, lasers, NICs, and fabric solutions.

The margin profile also remains impressive. Operating margin was around 67%, adjusted EBITDA margin was 69%, and free cash flow reached $10.3B, or 46% of revenue. This is not a “growth at any cost” AI story. Broadcom is scaling revenue while generating significant cash.

The main question: expectations.

Q2 revenue guidance of $29.4B was above consensus, but AI semiconductor guidance of $16B appears below some buyside expectations around $18B. That likely explains part of the negative stock reaction despite the strong headline numbers.

Broadcom’s fundamentals look exceptional, but expectations are also very high. The debate is shifting from “Is AI demand real?” to “Can Broadcom execute this multi-year ramp fast enough to satisfy the market?”

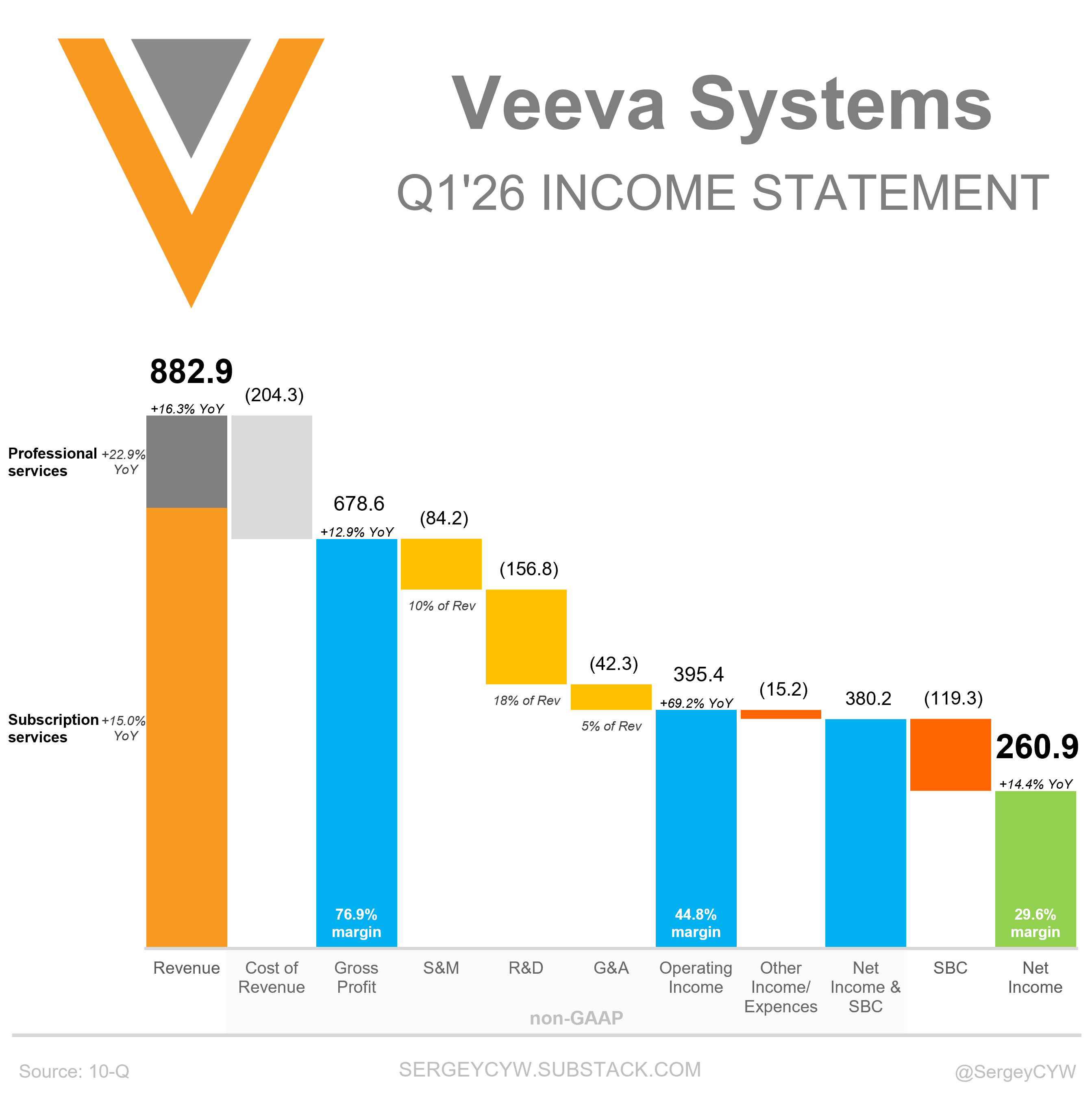

Veeva Systems

Veeva delivered a strong Q1’26. Revenue grew 16.3% YoY to $882.9M, beating estimates by 3.0%. EPS came in at $2.24, ahead by 5.2%. Billings increased 19.1% YoY to $871M.

Profitability.

Non-GAAP operating margin expanded to 44.8%, up 14.0 percentage points YoY. OCF margin reached 127.7%, up 12.1 points YoY. Few software companies are producing this level of profitability while continuing to invest across CRM, Development Cloud, Crossix, Ostro, Vault AI, and Falcon.

Subscription revenue grew 15.0% YoY to $730.2M, while professional services revenue increased 22.9% YoY to $152.8M.

Non-GAAP gross margin declined 2.3 points YoY to 76.9%. Subscription gross margin fell 1.3 points to 86.8%, while professional services gross margin declined 4.0 points to 29.5%. The decline is manageable, but investors will likely watch whether additional AI and services investments create further pressure.

The most important long-term development is Falcon.

Management is positioning Falcon as AI-powered “agentic labor” for life sciences. The goal is not simply assisting users but automating repetitive, high-volume work currently handled by people.

Early use cases include clinical trial document processing, safety case intake, regulatory correspondence, metadata extraction, quality checks, and TMF filing.

Veeva’s advantage is its position as a system of record across life sciences. AI agents become more valuable when connected to structured workflows, trusted applications, and proprietary data.

Management also indicated Falcon should complement, not cannibalize, the core business. Customers still need Veeva’s systems of record, while Falcon adds a new layer of automation on top.

Beyond AI, execution remained strong.

Crossix continues benefiting from growing pharma digital advertising spend and expanding measurement capabilities across channels such as OpenEvidence and Meta.

Vault CRM momentum remains solid, with more than 150 customers live and over 40 migrations completed. Recent wins included Teva and Merck KGaA.

Guidance was steady. Q2 revenue is expected at $902M-$905M, representing roughly 14.5% YoY growth. FY26 revenue guidance was raised to $3.635B-$3.645B, implying approximately 13.9% YoY growth.

The key question is whether Falcon evolves into a significant new revenue stream. If it does, Veeva’s growth profile could look very different over the next several years.

Q1 reinforced the core investment case: strong execution, expanding profitability, and a credible path to monetizing AI within life sciences.

Thank you for reading!

Follow me for more frequent updates on X/Twitter and Threads, and on LinkedIn. For visual infographics, check out Instagram, and for portfolio changes, follow me on SavvyTrader.

Disclaimer: This earnings review is for informational purposes only and does not constitute financial, investment, or trading advice.