Confluent Q1 2025 Earnings Analysis

Dive into $CFLT Confluent’s Q1 2025 earnings with review of financial performance, key metrics, operating expenses, dilution, customer growth, future outlook

Financial Results:

↗️$271.1M rev (+24.8% YoY, +22.5% LQ) beat est by 2.7%

↗️GM* (78.6%, +1.6 PPs YoY)

↗️Operating Margin* (4.3%, +5.8 PPs YoY)

↗️FCF Margin (1.8%, +16.4 PPs YoY)

↗️Net Margin (356.9%, +399.7 PPs YoY)🟢

↗️EPS* $0.08 beat est by 14.3%

*non-GAAP

Revenue by Segment

↗️Subscription Revenue $260.9M rev (+26.1% YoY, 96% of Rev)

↗️Cloud $142.7M rev (+33.6% YoY, 53% of Rev)

↘️Services $10.2M rev (-1.3% YoY, 4% of Rev)

Key Metrics

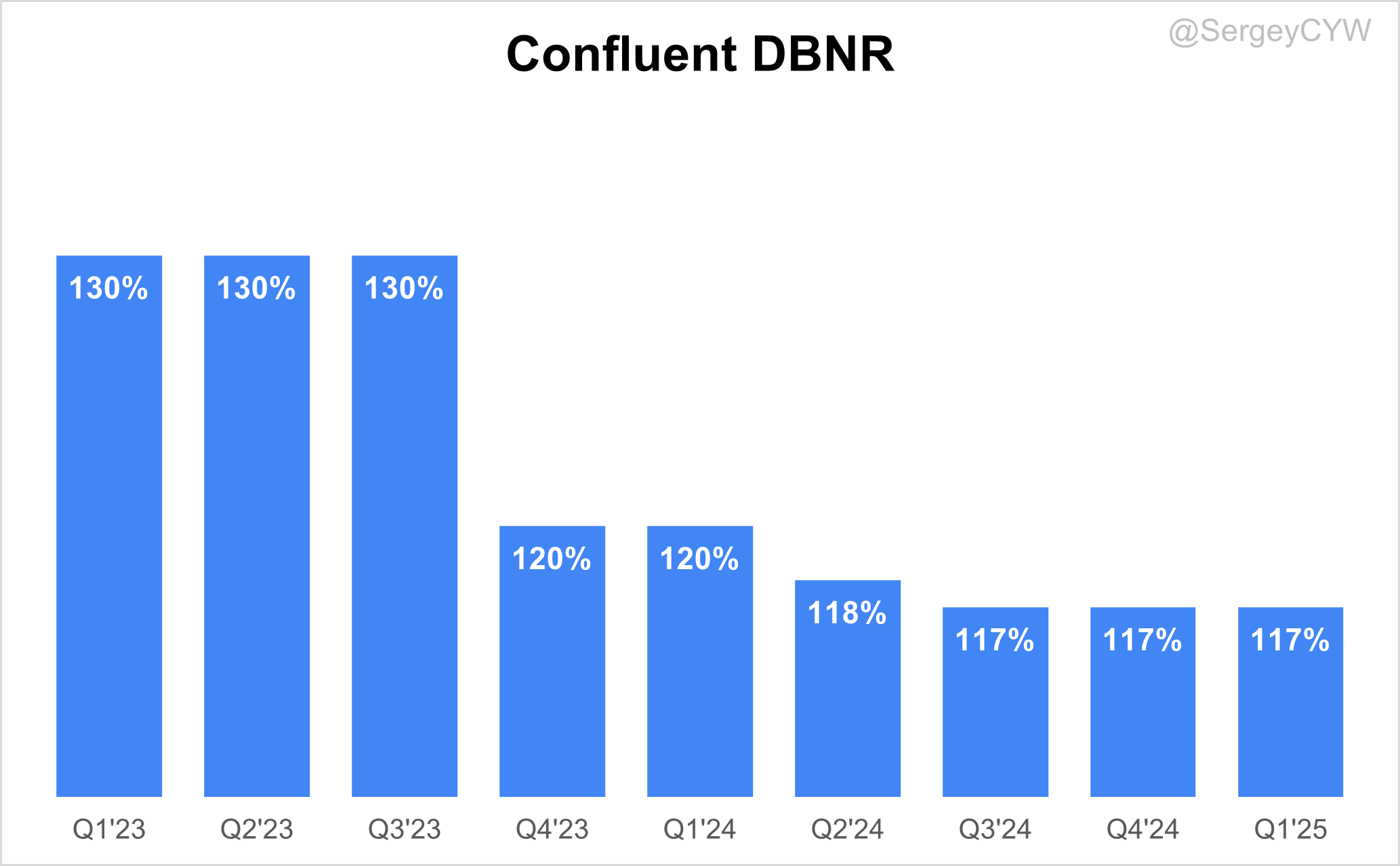

➡️DBNR 117% (117% LQ)

➡️RPO $1,016.10M (+20.9% YoY)🟡

➡️Billings $267M (+15.3% YoY)🟡

Customers

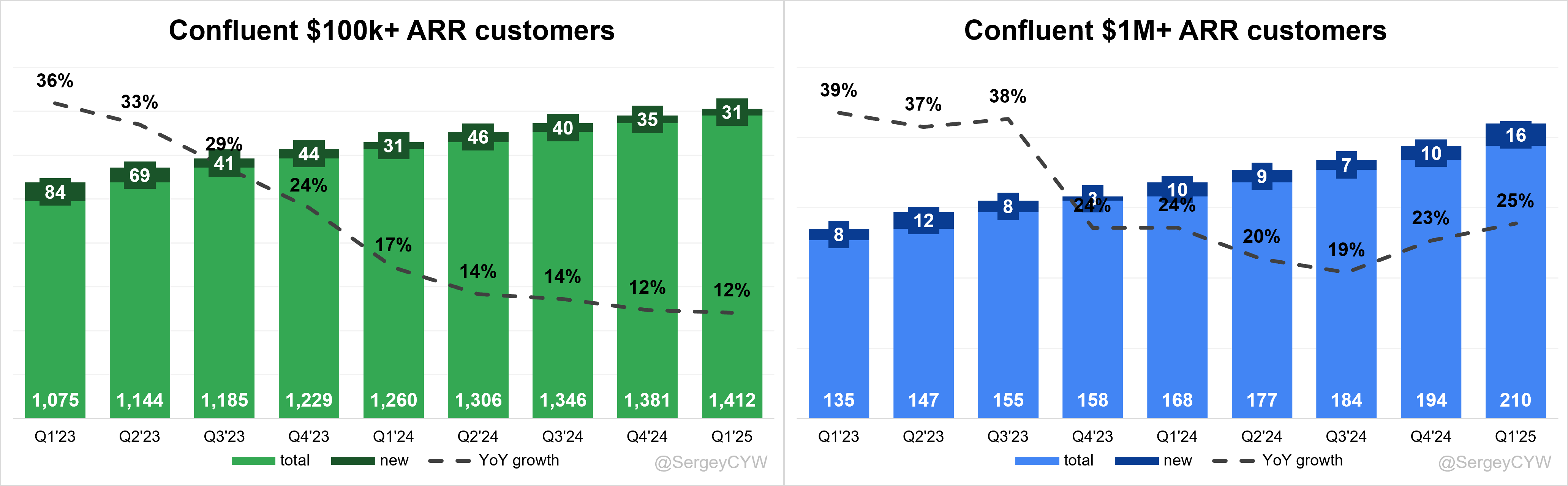

➡️1,412 $100k+ customers (+12.1% YoY, +31)🔴

↗️210 $1M+ customers (+25.0% YoY, +16)🟢

Regional Breakdown

↘️United States $156.4M rev (+22.8% YoY, 58% of Rev)

↗️International $114.7M rev (+27.7% YoY, 42% of Rev)

Operating expenses

↘️S&M*/Revenue 41.5% (-2.5 PPs YoY)

↘️R&D*/Revenue 23.4% (-0.5 PPs YoY)

↘️G&A*/Revenue 9.5% (-1.1 PPs YoY)

Quarterly Performance Highlights

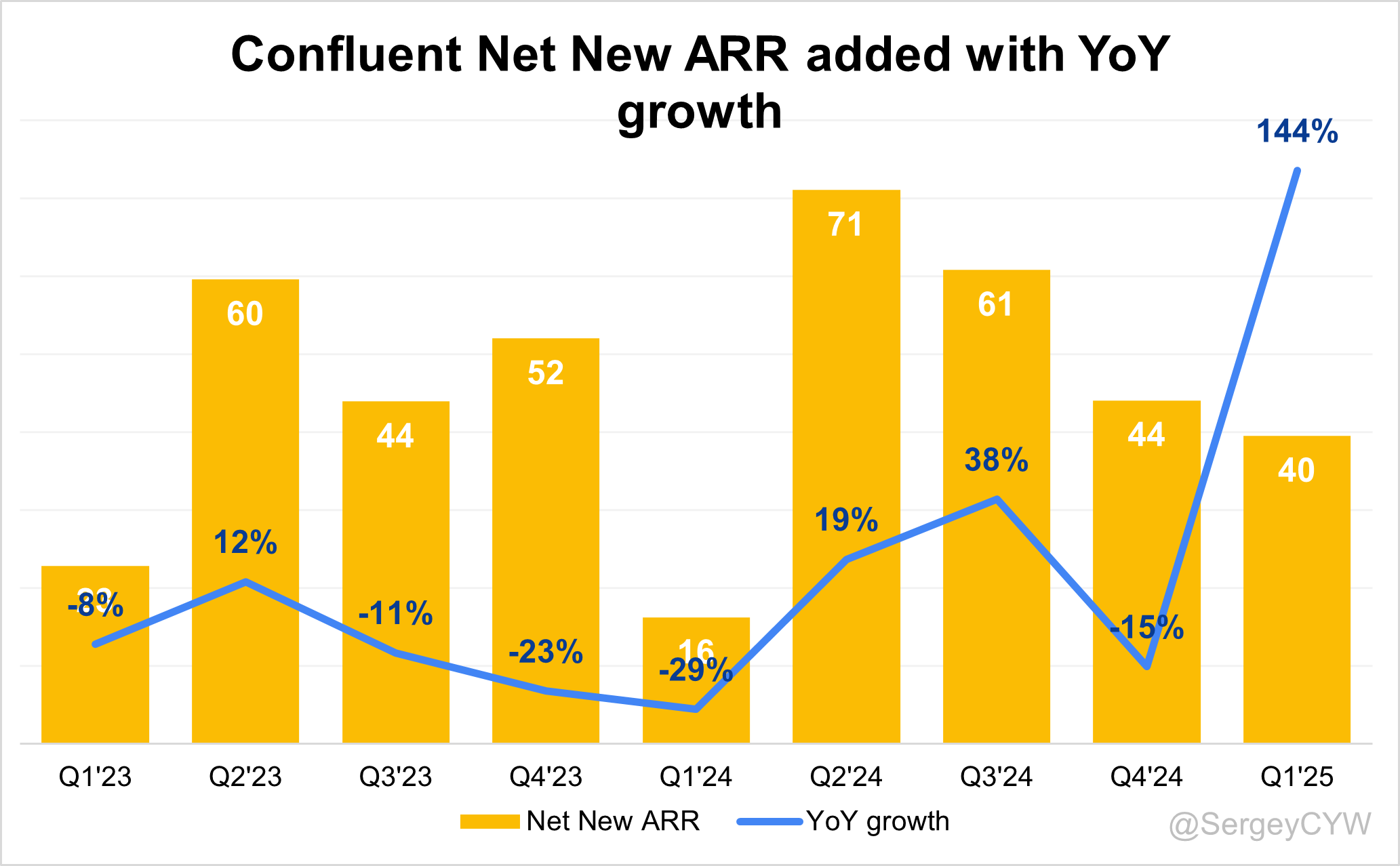

↗️Net New ARR $40M (+143.8% YoY)

↗️CAC* Payback Period 42.1 Months (-41.4 YoY)🟢

↗️R&D* Index (RDI) 1.06 (+0.13 YoY)🟢

Dilution

↘️SBC/rev 37%, -3.7 PPs QoQ

↗️Basic shares up 6.9% YoY, +0.3 PPs QoQ🔴

↘️Diluted shares up 5.0% YoY, -0.7 PPs QoQ🟡

Guidance

➡️Q2'25 $267.0 - $268.0M guide (+19.0% YoY) in line with est

↘️$1,100.0 - $1,111.0M FY guide (+19.9% YoY) lowered by -0.9% missed est by -1.2%🔴

Key points from Confluent’s First Quarter 2025 Earnings Call:

Financial Performance

Confluent reported $260.9M in subscription revenue in Q1 FY2025, up +26% YoY, exceeding the top end of guidance. Confluent Cloud and Platform combined represented 96% of revenue. Non-GAAP operating margin improved to 4.3%, up +6 percentage points YoY, above the 3% guidance. Subscription gross margin rose +100 bps YoY to 81.7%, driven by cloud efficiency. EPS reached $0.08, beating estimates by 14.3%. Adjusted free cash flow margin was 1.8%, excluding a ~14 pp one-time compensation impact. Share count stood at 367.8M basic and 380.9M diluted shares.

Confluent Platform

Confluent Platform (CP) revenue grew +18% YoY to $118.2M, its highest Q1 growth in three years. Growth was driven by OEM partnerships, strong international demand, and increasing adoption in on-prem and hybrid environments. Seven of the 16 new $1M+ ARR customers were CP-led. CP plays a central role in regulated industries, with 50% of new $1M+ customers operating in hybrid setups.

CP innovation continued with integration of Apache Flink, expanding use case flexibility for real-time stream processing. Management noted that CP performance may vary quarter to quarter due to deal timing and emphasized evaluating its trajectory on a 12-month basis.

Confluent Cloud

Cloud revenue reached $142.7M, growing +34% YoY, and now represents 55% of subscription revenue. SMB usage remained stable, while large enterprise consumption slowed in March, with no rebound in April. The company forecasts cloud mix rising to 58% by Q4 FY2025, increasing ~1 pp per quarter.

Cloud growth benefited from enhancements like Freight Clusters and WarpStream, aimed at high-throughput use cases. Cloud continues to be the primary channel for new customer acquisition, especially among AI-native and digital-first companies.

DSP Expansion

The Data Streaming Platform (DSP) suite—Connect, Flink, Govern, TableFlow—is now a key growth vector. DSP components outpaced core cloud growth in Q1. 13 of the 16 new $1M+ ARR customers included DSP adoption.

TableFlow launched GA on AWS with strong pipeline momentum. Flink adoption is accelerating across inventory, fraud detection, and e-commerce use cases. DSP remains in early ramp and is not yet included in short-term guidance. Broader deployment across cloud regions and integration with Delta Lake and Databricks Unity are in progress.

Kafka Conversion

Confluent targets a $100B+ TAM by converting 150,000+ open-source Kafka users. The strategy emphasizes 3x lower TCO, performance, and operational efficiency.

Odyssey switched from open-source Kafka, boosting developer velocity by +40%. Booking.com consolidated critical workloads using Confluent to enable a unified trip experience. A top-20 global bank, now spending $5M+ ARR, increased spend by +30% in Q1 and estimates 3x cost savings over self-managed Kafka.

Apache Flink

Flink is core to DSP and is embedded in both Cloud and CP. It enables high-frequency stream processing in real time using SQL and Java. A luxury goods company with 6,000+ stores adopted Flink to deduplicate inventory data and trigger real-time customer alerts, driving e-commerce revenue.

Flink supports mission-critical workloads and GenAI data pipelines. Management is investing in optimization and scale to support enterprise migrations.

WarpStream Growth

WarpStream, Confluent’s diskless Kafka-compatible engine, is gaining traction for high-throughput, low-latency workloads. Integrated with Freight Clusters, it writes directly to object storage, delivering ~3x lower cost than self-managed Kafka.

Early adopters include Cursor and other GenAI firms. Wins are attributed both to the WarpStream pipeline and Confluent’s broader go-to-market team. Expansion will require validation, performance benchmarking, and deeper DSP integration.

AI Use Cases

Confluent serves as the real-time data supply chain for AI. It enables GenAI systems to ingest live context and supports real-time agents that act on streaming data. Use cases are growing in both GenAI-native companies and large enterprise AI deployments.

AI Customer Adoption

AI-native startups like Cursor and Thinking Machines are leveraging Confluent for low-latency streaming pipelines. WarpStream and Flink are critical for these AI workloads. Management sees enterprise GenAI as its largest long-term monetization opportunity.

TableFlow Launch

TableFlow officially launched GA on AWS in Q1. It provides real-time streaming into cloud-native table formats (Delta Lake, Iceberg). It is priced independently and drives adoption across Flink and Kafka. Expansion across all major clouds and Databricks integration is underway.

Customer Metrics

Confluent ended Q1 with 6,140 customers, adding +340 net new, the highest since Q1’22.

$20K+ ARR customers rose to 2,487, up +41 QoQ, now representing 95%+ of ARR.

$100K+ ARR customers reached 1,412, up +31 QoQ, accounting for 90%+ of ARR.

$1M+ ARR customers grew to 210, up +16 QoQ, a record.

13 of 16 new $1M+ customers adopted DSP. 50% operated in hybrid cloud and on-prem environments.

GRR remained above 90% and NRR was stable at 117%.

Strategic Customer Wins

Odyssey improved developer agility by +40% after adopting Confluent and automating streaming workflows.

Booking.com replaced in-house Kafka with Confluent to streamline scaling and enable connected experiences across flights, hotels, and rentals.

A top-20 global bank transitioned workloads to Confluent over five years, achieving 3x cost efficiency and expanding cloud usage for fraud detection and compliance.

A luxury conglomerate uses Confluent and Flink for real-time stock visibility and order alerts, improving customer experience and revenue.

Strategic Partnerships

Confluent was named Google Cloud Partner of the Year for the sixth time.

OEM partnerships, particularly internationally, contributed to strong CP performance.

Ryan McBann was promoted to Chief Revenue Officer, unifying sales, customer success, and operations.

OEM deals played a key role in multi-year CP contracts.

Market Challenges

Larger customers began optimizing cloud costs and slowed new use case additions in March. SMB usage remained stable. April showed no recovery, prompting conservative planning.

Management noted the current optimization trend differs from past cycles where usage rebounded. The outlook now assumes no near-term recovery in large customer cloud consumption.

Lowered Guidance

FY25 subscription revenue is guided to $1.10–$1.11B (+19–20% YoY).

Operating margin expected at ~6%, EPS at ~$0.36, and adjusted FCF margin ~6% (excluding 3–4 pp comp impact).

Sequential cloud mix forecasted to rise to 58% by Q4.

No acceleration assumed in the second half of FY25.

Outlook

Confluent is positioned to capture long-term growth through open-source conversions, DSP expansion, AI data pipelines, and strong CSP and OEM partnerships. Its hybrid architecture and multi-form factor deployment model provide flexibility across cloud, on-prem, and edge. Margin expansion, new product launches, and broader customer diversification support durable, profitable growth.

Management comments on the earnings call.

Product Innovations

Jay Kreps, Co-Founder and Chief Executive Officer

“We just released TableFlow as GA in AWS—great early signs for that. And then Flink is succeeding really nicely both in the cloud as well as in CP. We’ve added this to our CP offering and picked up some really sizable customers on that doing awesome use cases.”

Jay Kreps, Co-Founder and Chief Executive Officer

“TableFlow is a very easy product to enable for existing data. You can just turn it on—it doesn’t require a ton of development work. As we crack this and learn how to take it to market, we believe it can ramp relatively quickly.”

Confluent Cloud

Jay Kreps, Co-Founder and Chief Executive Officer

“We did see a bit of lower consumption in our larger customers on the cloud side. It was a combination of optimizations and slower addition of new use cases. That wasn’t across the customer base—our smaller customers didn’t show that pattern.”

Rohan Sivaram, Chief Financial Officer

“For our cloud business, some of our larger customers began slowing the pace of new use case addition and focusing on cost optimization efforts in March. These trends have continued into April. We believe it’s prudent to assume there will not be a near-term rebound in consumption.”

DSP Expansion

Jay Kreps, Co-Founder and Chief Executive Officer

“Our DSP offerings are on a great success trajectory—significantly outgrowing the core cloud business. A lot of enthusiasm from customers. It’s still early innings for offerings like Flink and TableFlow, but there’s great initial success.”

Jay Kreps, Co-Founder and Chief Executive Officer

“We ultimately don’t bake a ton of DSP product success into our guidance. Something like TableFlow that’s just coming out to GA—we’d have internal goals, but we wouldn’t attach something to financial plans until we see performance.”

Kafka Evolution

Jay Kreps, Co-Founder and Chief Executive Officer

“The opportunity in open-source Kafka is massive. We estimate over 150,000 organizations use Kafka today. Our total cost of ownership advantage is a key lever helping us retain customers and tap into the broader open-source community.”

Jay Kreps, Co-Founder and Chief Executive Officer

“Customers believe that for every dollar they spend with us, they would otherwise spend $3 managing Kafka themselves.”

Apache Flink

Jay Kreps, Co-Founder and Chief Executive Officer

“Flink is succeeding really nicely both in the cloud and in CP. We’re seeing it used to migrate dozens or hundreds of processing jobs over from existing systems. We’re investing in ensuring we can deliver against large enterprise migrations.”

WarpStream Expansion

Jay Kreps, Co-Founder and Chief Executive Officer

“We’ve done that in both our cloud and with WarpStream—we’re actually very intelligent about the use of storage. Freight Clusters use a pure diskless approach. There’s a lot of sophistication in the storage layer and it matters a lot in cost-performance trade-offs.”

Jay Kreps, Co-Founder and Chief Executive Officer

“We’ve definitely had some really nice customer wins with WarpStream. It filled a natural niche in our product portfolio and was ready to sell—we knew it could hit the ground running, and that’s what we’ve seen.”

AI and Streaming

Jay Kreps, Co-Founder and Chief Executive Officer

“We’ve seen success in two dimensions with AI. First, selling to AI-native companies like Cursor. Second, powering enterprise AI use cases. We act as the data supply chain to feed context into AI systems, and support agents acting on real-time data.”

Jay Kreps, Co-Founder and Chief Executive Officer

“The use of AI agents is shifting data use upstream into real-time flows. This lets data land in analytics environments faster and become a key part of AI applications.”

Customers

Rohan Sivaram, Chief Financial Officer

“We ended Q1 with approximately 6,140 customers, representing a sequential increase of 340 customers—our highest net add since Q1 of 2022.”

Rohan Sivaram, Chief Financial Officer

“Our $1 million+ ARR customer count grew to 210, up 16 sequentially—our best quarter in net adds for this cohort. And 13 of those 16 customers had DSP in the deal.”

Jay Kreps, Co-Founder and Chief Executive Officer

“Odyssey turned to us when their Kafka-based infrastructure became too brittle and hard to scale. With Confluent, they accelerated feature development by 40% and unlocked new digital revenue opportunities.”

Jay Kreps, Co-Founder and Chief Executive Officer

“A top-20 global bank that spends over $5 million annually with us recently increased their spend by over 30%. They estimate they save 3x by using Confluent versus managing Kafka themselves.”

Strategic Partnerships

Jay Kreps, Co-Founder and Chief Executive Officer

“We’re honored to be named a Google Partner of the Year for the sixth time. This recognition reflects the strength of our partnerships with leading cloud providers to help customers build the next generation of applications.”

Rohan Sivaram, Chief Financial Officer

“CP momentum was driven by early traction in our partner ecosystem. OEMs showed particular strength, especially in international markets.”

Challenges

Jay Kreps, Co-Founder and Chief Executive Officer

“There’s a bit of an oscillating pattern in large customer behavior—optimization followed by growth. In more certain times, we would assume a rebound. But in this environment, we’re taking a more conservative view.”

Jay Kreps, Co-Founder and Chief Executive Officer

“We’ve seen stability in April, but no immediate rebound after the slowdown in March. We don’t see a systematic demand softening, but we’re cautious given the uncertainty.”

Guidance Lowered

Rohan Sivaram, Chief Financial Officer

“We are widening our revenue guidance range and embedding a modest decline in growth rates from Q2 through Q4 due to changes in cloud consumption behavior. We're not assuming a rebound as we’ve seen in past optimization cycles.”

Rohan Sivaram, Chief Financial Officer

“We now expect cloud subscription revenue mix to be approximately 58% by Q4, increasing by about one point per quarter.”

Future Outlook

Jay Kreps, Co-Founder and Chief Executive Officer

“Our hybrid architecture, platform completeness, and positioning in real-time data streaming give us a durable growth foundation. We’re not making a hard bet on cloud or on-prem—we’re built to win regardless of deployment choice.”

Rohan Sivaram, Chief Financial Officer

“We are guiding to 19% to 20% growth at greater than a $1 billion scale, with a setup that assumes no acceleration in the back half of the year. That gives us confidence despite uncertain macro conditions.”

Thoughts on Confluent Earnings Report $CFLT:

🟢 Positive

Revenue reached $271.1M (+24.8% YoY), beating estimates by 2.7%

Subscription revenue was $260.9M (+26.1% YoY), 96% of total

Confluent Cloud grew to $142.7M (+33.6% YoY), 53% of revenue

Net new ARR rose to $40M (+143.8% YoY)

EPS of $0.08, beating by 14.3%

Non-GAAP operating margin improved to 4.3% (+5.8 pp YoY)

Free cash flow margin was 1.8%, up +16.4 pp YoY

$1M+ customers reached 210 (+25% YoY, +16 QoQ)

Odyssey improved dev velocity by +40%, top-20 global bank grew Confluent spend +30% QoQ

R&D Index rose to 1.06 (+0.13 YoY)

S&M/revenue fell to 41.5% (-2.5 pp YoY)

G&A/revenue fell to 9.5% (-1.1 pp YoY)

🟡 Neutral

RPO reached $1.02B (+20.9% YoY)

Billings came in at $267M (+15.3% YoY)

DBNR remained flat at 117% QoQ

Cloud mix expected to rise to 58% by Q4

TableFlow launched GA on AWS, scaling under way

Diluted shares up 5.0% YoY, SBC/rev improved to 37% (-3.7 pp QoQ)

International revenue grew +27.7% YoY, now 42% of total

Flink and WarpStream adoption growing, but still early in enterprise rollout

🔴 Negative

$100K+ customers grew to 1,412 (+12.1% YoY, +31 QoQ), slower than prior quarters

Services revenue declined -1.3% YoY, now 4% of total

U.S. revenue growth lagged at +22.8% YoY

FY25 revenue guidance of $1.10–$1.11B was lowered by -0.9%, missing estimates by -1.2%

Guidance assumes no acceleration in H2 cloud growth due to macro uncertainty

Large customer cloud consumption slowed in March; no rebound in April

Basic shares increased +6.9% YoY

Management flagged potential variability in CP deal timing impacting quarters

Thank you for reading!

Follow me for more frequent updates on X/Twitter and Threads, and on LinkedIn. For visual infographics, check out Instagram, and for portfolio changes, follow me on SavvyTrader.

Disclaimer: This earnings review is for informational purposes only and does not constitute financial, investment, or trading advice.