Axon Enterprise Q3 2024 Earnings Analysis

Dive into $AXON Axon’s Q3 2024 earnings with review of financial performance, key metrics, operating expenses, dilution, customer growth, future outlook

Financial Results:

↗️$544M rev (+31.6% YoY, +34.6% LQ) beat est by 3.4%

↘️GM (60.8%, -1.0 PPs YoY)🟡

↗️GM* (63.2%, +1.1 PPs YoY)

↗️Adj EBITDA Margin (26.7%, +4.5 PPs YoY)

↗️FCF Margin (11.9%, +0.2 PPs YoY)

↗️Net Income Margin* (20.8%, +2.1 PPs YoY)

↗️EPS* $1.45 beat est by 21.8%🟢

*non-GAAP

Revenue By Segments

TASER

↗️$221.7M TASER rev (+36.4% YoY)

↘️GM (60.8%, -1.7 PPs YoY)

Sensors and other

➡️$120.0M Sensors and other rev (+16.5% YoY)

↘️GM (41.4%, -3.8 PPs YoY)

Axon Cloud

↗️$202.5M Axon Cloud rev (+36.9% YoY)

↘️GM (72.3%, -0.1 PPs YoY)

Key Metrics

↗️NRR 123% (122% LQ)

↗️Total company future contracted revenue $7.71B (+32.5% YoY)

↗️ARR $885M (+35.7% YoY)🟢

Operating expenses

↘️SG&A*/Revenue 25.2% (-1.5 PPs YoY)

↘️R&D*/Revenue 14.3% (-0.5 PPs YoY)

Quarterly Performance Highlights

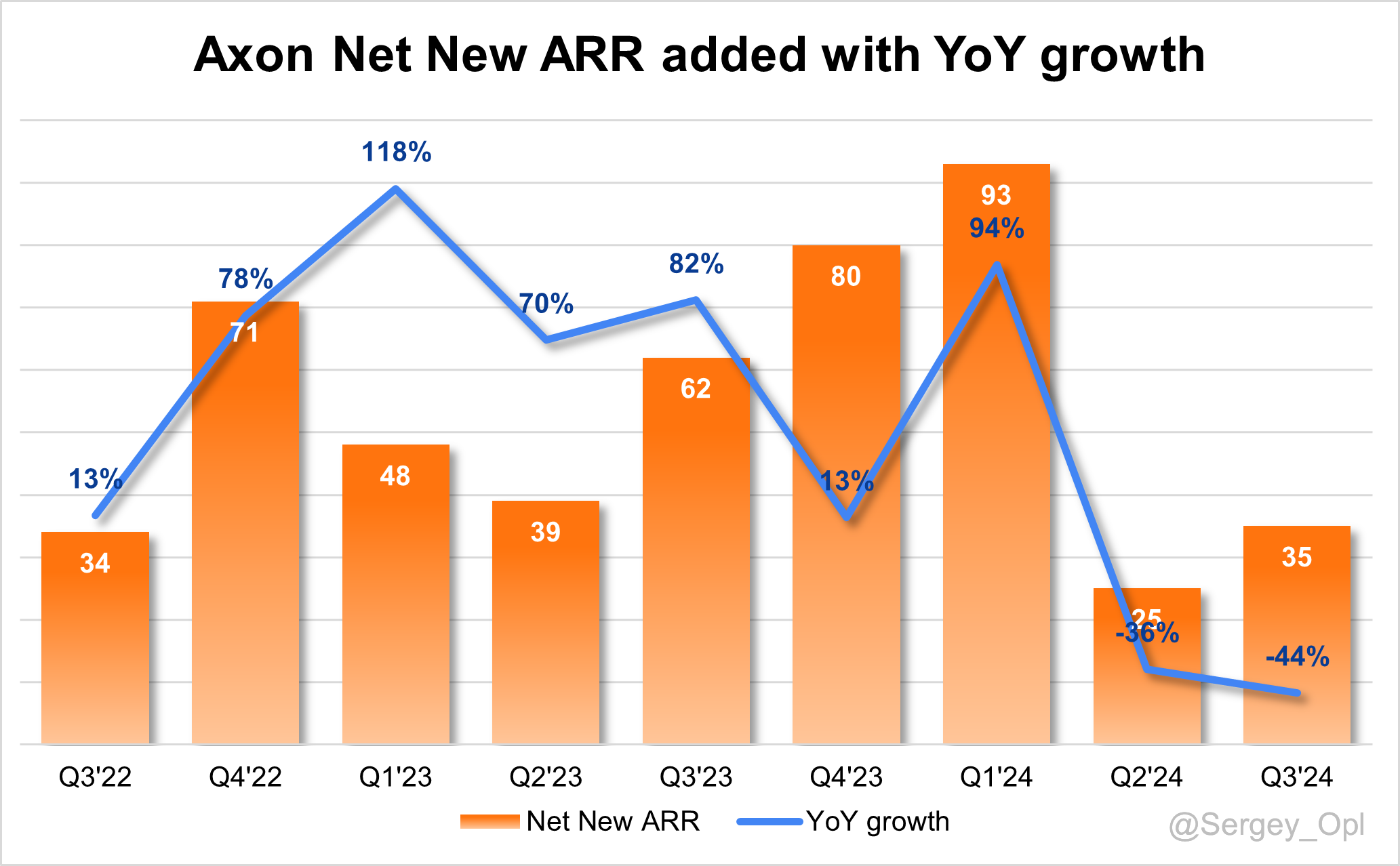

↘️Net New ARR $35M (-43.5% YoY)

↗️CAC* Payback Period 16.2 Months (15.9 LQ)

Dilution

↗️SBC/rev 19%, 3.9 PPs QoQ

↗️Basic shares up 1.2% YoY, 1.16 PPs QoQ

↗️Diluted shares up 2.8% YoY, +0.5 PPs QoQ

Guidance

↗️Q4'24 $560.0 - $570.0M guide (+30.7% YoY) beat est by 3.5%

↗️$2,070.0M FY guide (+32.4% YoY) raised by 1.0% beat est by 1.5%

Key points from Axon’s Third Quarter 2024 Earnings Call:

Financial Performance

Axon reported robust financial growth in Q3 2024, marking its 11th consecutive quarter of over 25% YoY growth. Revenue rose 32% YoY to exceed $2 billion annualized, surpassing previous guidance. Adjusted EBITDA margin reached 26.7%, reflecting Axon’s focus on both revenue expansion and operational efficiency. Q3 bookings exceeded $1 billion, setting a record on both absolute and normalized five-year bases. Annual recurring revenue (ARR) grew 36% YoY to $885 million, demonstrating high demand and a strong customer retention rate of 123%. Axon raised its full-year revenue guidance to $2.07 billion, targeting an EBITDA margin of 24.6%, despite expected seasonal costs in Q4 due to acquisition integrations and year-end expenditures.

ARR and Future Contracted Revenue Growth Slowing

Future contracted revenue reached $7.7 billion by Q3 2024, reflecting a 33% YoY increase. This figure represents contracted values projected to convert to revenue in future periods, providing a solid foundation for Axon’s long-term revenue stability and underscoring strong demand in law enforcement and public safety verticals.

While ARR increased 36% YoY to $885 million, this growth decelerated slightly, reflecting product maturity and seasonal booking trends. This deceleration is attributed to software booking timing, seasonality, and deployment variances for products like Axon Fleet. Axon noted that quarterly ARR fluctuations are anticipated due to booking cycles and customer procurement timing but highlighted a stable long-term growth trajectory supported by its expanding AI solutions and recurring revenue model. Axon’s strategy to mitigate ARR deceleration includes multi-product and bundled offerings, such as the AI Era bundle, encouraging customers to adopt a suite of products under one subscription model. Axon projects the ARR slowdown to moderate as products like Draft 1 and the AI Era bundle gain traction, expanding Axon’s penetration in both existing accounts and new segments.

Product Updates

Axon leveraged AI to drive product innovation, introducing the AI Era bundle, which centers on the Draft 1 transcription tool. Draft 1 streamlines report writing, reducing administrative time for law enforcement agencies. The AI Era bundle is priced at $199 per month, strategically designed to offer bundled savings and generate predictable recurring revenue for Axon. The AI suite is structured to evolve, keeping pace with the rapidly advancing technology landscape.

TASER

TASER 10 demand nearly doubled compared to prior models, with TASER revenue growing 36% YoY, marking the strongest growth in over two years. TASER 10’s enhanced range and capacity position it as a non-lethal firearm alternative in the U.S. and international markets. Axon expects continued international demand, particularly in regions where firearms are less prevalent, viewing TASER 10 as transformative for non-lethal defense solutions. TASER cartridge sales showed quarterly variability due to deployment plan cycles, but overall demand remained robust.

Sensors

Sensor revenue increased 18% YoY, driven by Axon Body 4 camera demand. Fleet revenue displayed variability due to RFP timing and deployment cycles, though the sensor division's growth highlights sustained demand for body-worn camera upgrades. The Fusus acquisition is expected to further enhance sensor offerings, integrating multiple camera feeds into a real-time ecosystem that supports Axon’s public safety mission.

Axon Cloud

Cloud and services revenue grew 36% YoY, led by strong software adoption. ARR from cloud solutions saw significant growth, underscoring Axon’s shift towards digital services. Future Contracted Revenue stands at $7.7 billion, up 33% YoY, reinforcing growth in Axon’s SaaS and cloud offerings.

Expanding Capabilities in Drones

Through its acquisition of D Drone and partnership with Skydio, Axon advanced its position in drone technology for public safety, particularly with its “Drone as a First Responder” (DFR) initiative, which provides real-time situational awareness through automated drone deployment. As regulatory landscapes shift, Axon expects growth in counter-drone solutions, especially for advanced detection and response needs. The D Drone acquisition also introduces Axon to new markets, including critical infrastructure and military applications.

Customer Success Stories and Product Adoption

Draft 1, Axon’s transcription tool, is reducing report-writing times from 30-45 minutes to under 5 minutes, allowing officers to focus on field duties. In a video by California’s Campbell Police Department, Draft 1 enabled officers to prioritize community engagement and safety. Campbell PD successfully integrated Axon’s TASER devices, body cameras, and Fusus real-time video feeds, significantly boosting its public safety capabilities—a model particularly impactful for small-to-medium agencies with limited resources.

Federal and Enterprise Customer Engagement

Axon’s federal bookings in Q3 surpassed previous full-year figures from a few years ago. Four of Q3’s top 10 domestic deals came from federal agencies, including DHS, IRS, and Amtrak, showing high demand for Axon’s public safety technologies in federal sectors. Axon’s Justice and enterprise segments are also growing, with several Fortune 500 companies trialing Axon products for retail security. Fusus integration further strengthens Axon’s role in a public-private safety network, enabling seamless data-sharing between private enterprises and public safety agencies.

International Expansion

International bookings grew 40% YoY, with high demand across geographies, particularly where TASER serves as a primary non-lethal defense. Axon’s focus on federal partnerships abroad and targeted expansions into markets like military, infrastructure, and law enforcement supports Axon’s international growth strategy. Axon anticipates significant potential for TASER 10 and Fusus in international markets with strict gun regulations.

Future Outlook

Axon’s 2025 guidance targets $2 billion in revenue, expected a year ahead of schedule, with sustained growth above 20% annually. The company aims for a 25% EBITDA margin in 2025, leveraging product innovation, expanded AI offerings, and international market penetration. Axon’s forward strategy is to capitalize on ongoing demand for cloud-based solutions, a consolidated AI strategy, and expanding government budgets in public safety, positioning the company to sustain growth and deliver consistent financial results over both the short and long term.

Management comments on the earnings call.

Product Innovations

Rick Smith, CEO

"Our focus on product innovation is about giving our customers cutting-edge tools to meet their needs in real-time. With the AI Era bundle, we’re delivering not just a feature, but a transformative solution that supports our customers in critical tasks like streamlining report writing and enhancing situational awareness. Our goal is to keep evolving as technology advances, ensuring we’re always delivering maximum value."

Axon Cloud

Brittany Bagley, CFO

"We’re seeing sustained growth in our cloud and services revenue, driven by high software adoption rates across our customer base. Future Contracted Revenue of $7.7 billion underscores the demand for our SaaS and cloud-based offerings. By focusing on ARR from cloud solutions, we’re solidifying our strategic shift to digital services, which supports long-term stability and growth."

Drones

Rick Smith, CEO

"Our drone and counter-drone initiatives are designed to address the critical need for enhanced situational awareness. With the Drone as a First Responder program, we’re enabling agencies to respond in real-time, providing immediate insights that support ground units. The D Drone acquisition positions us as a leader in the drone space, ready to meet the growing demand for automated and real-time drone capabilities in public safety."

Customers

Josh Isner, Chief Operating Officer

"We put our customers at the center of everything we do. Whether through innovative solutions like Draft 1 or by listening to their insights during our ‘Week of the Customer,’ we’re committed to building products that make a real difference. Every customer success story is a testament to our mission of delivering meaningful solutions that empower law enforcement and public safety."

International Growth

Cameron Brooks, Head of International

"Our international expansion strategy is focused on building strong relationships with federal governments abroad and entering new markets like military, infrastructure, and law enforcement. With high demand for products like TASER 10, we see tremendous growth opportunities in markets with strict gun regulations, where non-lethal solutions are vital."

Challenges

Brittany Bagley, CFO

"As we navigate quarter-to-quarter ARR fluctuations, we're focusing on mitigating impacts by offering multi-product and bundled solutions, like the AI Era bundle. This strategic approach encourages customers to adopt comprehensive solutions, supporting growth even as we manage the seasonal and deployment-related variances that come with ARR deceleration."

Future Outlook

Josh Isner, Chief Operating Officer

"Our forward strategy is to keep growing above 20% annually, with a target revenue of $2 billion for 2025. We’re building momentum in product innovation, AI expansion, and international reach. By continuing to invest in our technology and customer relationships, we’re positioning ourselves for strong and sustained performance well into the future."

Thoughts on Axon Enterprise ER $AXON:

🟢 Pros:

+ Revenue growth rate is +31.6% YoY. If the company beats its forecast by 3.4%, as it did this quarter, next quarter’s growth is projected to be 30.2%.

+ Full-year 2024 guidance was raised by 1.0%.

+ Dollar-Based Net Retention (DBNR) increased to 123%.

+ Annual Recurring Revenue (ARR) is growing at +36%, outpacing revenue growth.

+ Total company future contracted revenue is growing +32.5%, faster than revenue, though growth has slowed from +40% last quarter.

+ The company is improving margins and profitability.

+ Non-GAAP Gross Margin is strong at 63.2%, up from 62.1% in Q3 of last year.

+ Management noted that Draft One was very well received by customers, introducing the AI Era bundle centered around the Draft 1 transcription tool.

🟡 Neutral:

+- Axon Cloud revenue growth rate slowed to +37% YoY but remains strong and continues to outpace overall revenue growth.

+- Weak addition of net new ARR, with only +35 added, a -44% decrease YoY.

+- Stock-Based Compensation (SBC) as a percentage of revenue increased to 19%, up from 15% last quarter.

+- Weighted-average number of diluted common shares rose by 2.8% YoY.